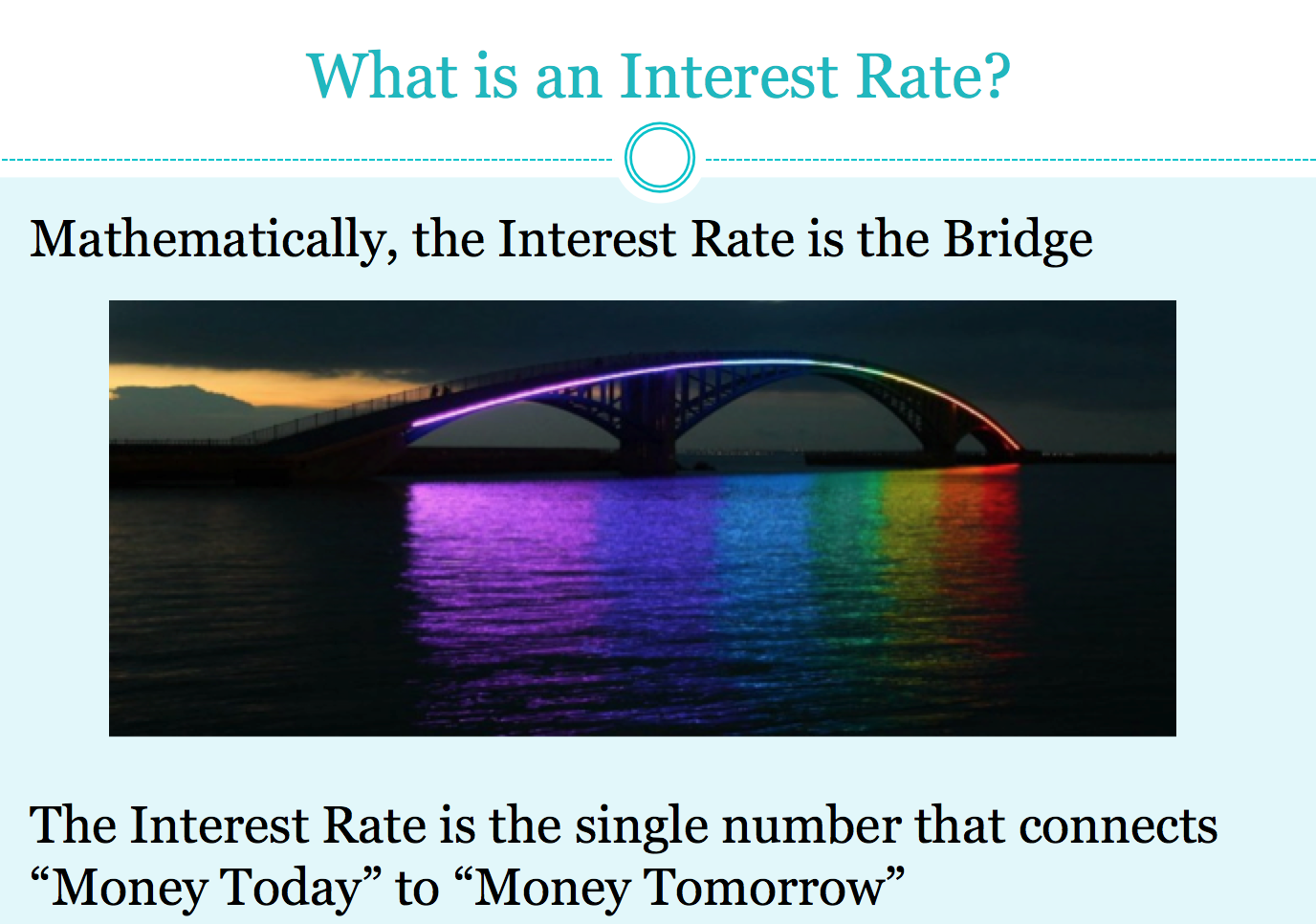

Why is money today more valuable than money in the future? In this lecture to students at Trinity University (in San Antonio, TX) I review four reasons why in any real-world scenarios I can think of, a reasonable person would give me less than $100 today in order to receive $100 from me one year from now.

To dig into the math of compound interest, discounted cash flows, and interest rates (or yield) its useful to review the practical fact – employed in all banking, insurance, borrowing/lending, and investing activities – that money today is worth more than money tomorrow.

In order to not play hide-the-ball with this video, here are my four reasons for why money today is not equal, and is more valuable, than money in the future:

1. Expected inflation (aka expected loss of purchasing power in the future)

2. Expected return (holders of capital demand a positive return on capital)

3. Risk of future payment (aka credit risk or counterparty risk)

4. Liquidity of capital provider (relative scarcity today raises value of money today for capital provider)

For all four of these reasons (and possibly more) holders of capital can demand a positive return, or interest rate, for the use of their capital. This justification for charging interest, or demanding a positive return on capital, or yield, is the foundation of every financial transaction.

In my ongoing, epic, lonely, quest to convince an indifferent world that the compound interest formula will clothe the downtrodden, feed the grey whales, prevent the coughing sickness and otherwise save the planet, I offer this video explanation for what the compound interest formula does.

I’m teaching personal finance to college kids this semester, so I plan to offer these video snippets on a semi-regular basis. I’m still new to video, so (gentle) criticism, (thoughtful) suggestions, and (full-throated) praise are all welcome!

We meet the narrator/protagonist Iris, a 20-something wannabe dancer in the big city, with multiple body piercings, dead-end jobs, and out-of-control credit card debt. She’s not exactly the profile of someone from whom I’m looking to learn about finance, even if I am – admittedly – picturing Rooney Mara in the starring role.

In the first chapter, Iris receives a very stern, one-way talking-to, by her tone-deaf dentist about the evils of credit card debt. The author seems to have set up the dentist as a foil to contrast with Iris’ eventual money mentor.

The dentist – I’m picturing Steve Martin in this hyper-talkative, annoying role – represents both preachy personal finance books, as well as any smarmy adult who does not take the time to understand the particular challenges of the heavily indebted.

Would you learn finance from this person?

Finally, we meet the Money Mentor, Saidah, as the we’ve-seen-this-cliché-before wise African-American woman. Believe me when I say I was skeptical of this Oprah-meets-Sonia-Sotomayor-fairy-godmother character.

The weird thing is this: I really enjoyed the book.

Iris/Rooney Mara doesn’t live like me, but Crawford writes well enough to create a sympathetic character.

Ninety-five percent of us have probably felt like her at some point – there’s not enough at the end of the month to pay all of our bills. We don’t know who to ask for help. Maybe we should just give in to the feeling that it can’t get any better and sink further into the debt? Is it all just too hard to get ahead so why bother?

One-half of all Americans do carry a credit card balance month to month.

Most of us do need a wise money mentor in our life, and typically the adults in our life either do not have the answers, or do not have the empathy to show us where to find them.

Saidah understands because, as we learn, she once faced heavy debts herself. Saidah listens, and Saidah suggests solutions. When Iris inevitably ignores her suggestions, Saidah repeats herself patiently.

I expected Iris to meet Saidah and then, in the typical arc of redemption stories, suddenly get her act together and pay off her debts.

But Crawford is a better writer than that. He depicts a fuller story of one step forward, two steps back for Iris. Things get worse before they get better. Like all of us, Iris vacillates between self-pity and self-confidence, good decisions and bad, willful blindness and occasional insight, eagerness to see her mentor and avoidance of her mentor from shame at her poor choices.

I knew The Money Mentor was a keeper when I got to the chapter when Iris watches It’s a Wonderful Life, and she’s inspired by the Christmas classic to take an important step forward in her journey to solvency. Careful readers of Bankers Anonymous will recognize that the movie similarly touched me.

In Iris’ case, the realization that she needed help from others led her to try Debtors Anonymous, a 12-step support group for people ready to make a change in their relationship to debt.

Money problems stem from a cash-flow deficit and our own psychological relationship with money. Solving the problem of high interest debt requires a combination of psychological change and cash flow management.

Many finance books I have read risk erring on the side of the dentist – a tone-deaf, one-way lecture on the right way to be.

But who wants to hear that? Most of us do not learn that way.

Crawford’s fictional fable allows space for the psychological, the irrational, and the personal in addressing our finances. I really liked this one.

1. Being a non-equity partner attorney is tough these days, and

2. NY City is expensive these days.

Both of these points are, undoubtedly true, as far as they go. On the other hand, what an idiotic piece.

Here’s a great example of making 2 true points, while overall missing The Truth of this unfortunate bankrupt attorney’s situation. The Truth is this: this guy’s lifestyle and expenses clearly didn’t match his earnings. Full stop.

This isn’t meant to blame or shame the attorney, who obviously is suffering from an inability to budget, and now has the ignominy of getting his personal financial situation described to the millions of readers of the New York Times.

But rather, its meant to point out that the Financial Infotainment Industrial Complex – of which the New York Times is the most important and highest quality member – can take a few pieces of data and shape an entirely bizarrely wrong narrative out of it.

When my four year old is given a Connect-The-Dots exercise in pre-K, we might be alarmed if she took the three black dots set up in the shape of a triangle and drew a highly accurate rendition of Edvard Munch’s The Scream. (Impressed, of course, but alarmed).

James Stewart, are you so far enmeshed in the New York City mindset that your main point about going bankrupt on $375K a year is that non-equity partners sure have it tough? That is alarming. Not impressed.

One reason to study and understand a crisis like 2008 is to avoid repeating it. George Santayana’s pithy justification for historical review – “those who do not learn from history are doomed to repeat it,” – is apt, and not just because my father-in-law is a Santayana scholar.[1]

Another reason to study the 2008 crisis is to respond appropriately with a public narrative, and ultimately with financial policy, based on what we learned. I frequently shake my head at both the public narrative about what happened, and I also grit my teeth about financial policy. So I keep looking for the best accounts of the crisis.

Lanchester’s I.O.U. is one of the best. He’s a stunningly clear writer who usefully adopts colloquial language to explain financial concepts. Most non-finance readers need analogies and narratives to grasp a synthetic credit default-swap CDO, and Lanchester wields these beautifully.

Lanchester was researching contemporary City of London[2] life for his excellent Capital – which I reviewed here – when he realized that the financial innovations of The City were:

Fascinating in and of themselves

Completely opaque to non-financial people

Suddenly wreaking havoc around the world

The result is a clear, entertaining, and informative analysis of the causes of the crisis. Lanchester’s review is more comprehensive about the global financial system, for example, than Michael Lewis’ more narrowly-cast The Big Short, which relied on a few closely-drawn characters and their profitable trade against the sub-prime mortgage market.

Unlike the US-oriented histories of the 2008 crisis, Lanchester writes from the UK perspective, rounding out what we may already know from Andrew Ross Sorkin’s Wall Street-oriented Too Big To Fail, for example.

Lanchester reviews the proximate causes of the crisis

a) Extraordinary, hidden leverage in the world’s largest banks (Chapter 1)

b) Financial innovation in securitization models but with limited actual historical data behind the models (Chapter 2)

c) An over-reliance on home ownership as an investment, both in the UK as well as in the USA (Chapter 3)

d) A system of mortgage underwriting and securitization that removed consequences from the originators (Chapter 4)

e) An intellectual failure to consider our tendencies to misunderstand risk (Chapter 5)[3] and

f) A blindness of regulators to the hints of future disaster (Chapter 6).

Lanchester does not risk readers’ ire by shifting some portion of responsibility for the crisis from lenders to borrowers – something I actually appreciated about Edward Conard’s Unintended Consequences – but he’s got a satisfactorily complete narrative of the causes of the crisis.

Have you read a book yet on the 2008 Crisis that is funny, clear, accurate, and in plain English?

[1] Can I interest you in Santayana’s most accessible work, the 1935 novelThe Last Pilgrim? This edition is edited by my father-in-law, and overall, good stuff. Among other things, The Last Pilgrim offers an interesting view of turn-of-the-last-century Boston Brahmin life. Boston Brahmins were, and are, some impressively thrifty folks.

[2] “The City of London,” or “The City” for non-financial folks does not mean the whole municipal entity including Buckingham Palace and Parliament and all the rest, but rather is shorthand for the capital city’s financial sector. In the UK when people say “The City of London” they mean the equivalent of saying “Wall Street” in the U.S.

[3] Lanchester acknowledges an intellectual debt to Nassim Taleb in this chapter, from his excellent books Fooled by Randomness and Black Swan.

I wrote a few days back about how Reinhart and Rogoff’s serious, academic, review of past and prospective debt restructurings seemed to provide policy support for financial repression – such as capital controls, fixed currency regimes, highly regulated banks, and hidden taxes on savings through forced public pension investments.

This post highlights one of my favorite things – intellectual, counter-intuitive, irony. In particular I enjoy the irony of political affiliations that the Reinhart Rogoff paper inspires.

I don’t know Professors Carmen Reinhart and Kenneth Rogoff’s political views, and in the most important sense they don’t matter. They’re economists, not political leaders.

In the post-2008 Crisis world, one of the ideological fault-lines has been to what extent governments should borrow and spend today, as a counter-cyclical buffer to the extremes of the economic downturn. Or conversely, whether the heavily-indebted governments of the developed world need to pare down their already-extensive borrowing, to avoid an even more disruptive crisis of fiscal insolvency.

Paul Krugman – from the political left – has carried the banner for more debt-financed government spending.

Regardless of the professors’ politics, the political right has adopted Reinhart and Rogoff’s work studying the history of debt restructurings as academic ammunition in favor of the budget austerity favored by the political right. This is logical.

I guess that’s why I enjoyed the irony that I recently wrote about, namely that their recent paper appears to justify financial repression. The right-leaning austerity camp is probably the last group who would approve of an interventionist financial regime such as currency controls, explicit and hidden taxes on savings, and a heavily regulated banking sector.

Meanwhile, from the left, the critics of Reinhart and Rogoff’s history of debtors’ profligacy argue in favor of a much more severe regulatory regime when it comes to banking. The natural political affiliations seem flipped in this situation.

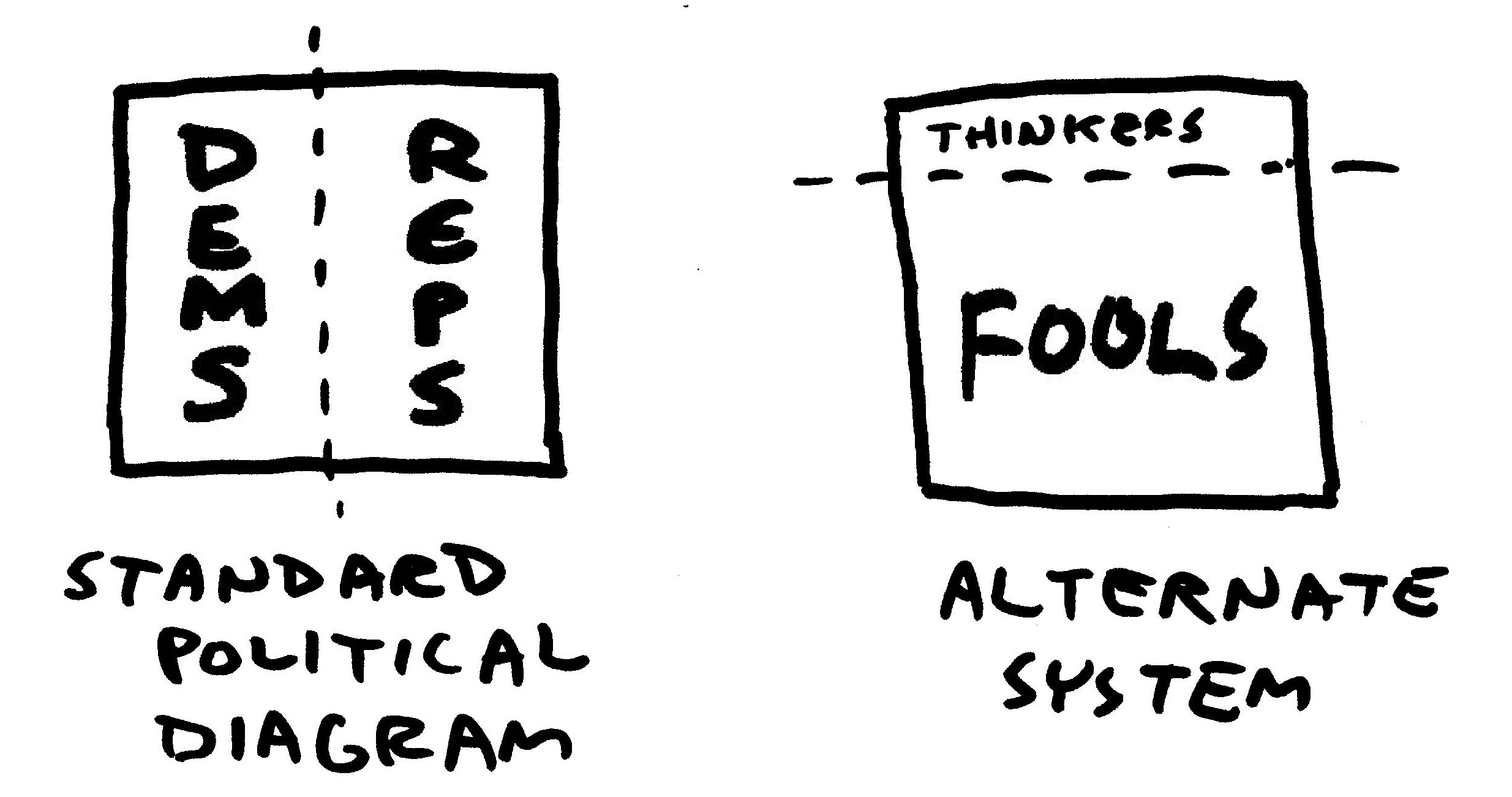

Of course, the challenge as always is to figure out what we really think about complex topics, rather than just adopt what ‘our side’ thinks on a complex topic. All of that reminded me of our tendency toward policy tribalism.

4. A sovereign wealth fund to spread common ownership and

5. A public bank

Importantly, he cited Franklin Roosevelt, Martin Luther King, and some presumably left-leaning academics as supporters of his ideas.

Next, Dylan Matthews wrote a right-wing Op-ed for Ezra Klein’s Wonkblog, advocating the exact same policies, but citing conservative support for the ideas, such as The American Enterprise Institute, Milton Friedman, and Charles Murray.

The reaction: conservatives hated the first article and supported the second, while liberals, of course, praised the first and panned the second.

Klein goes on to cite the work of Stanford psychologist Geoffrey Cohen, who has shown that we consistently form our opinions about policies based on who we think supports the ideas – rather than the specific ideas themselves.

Do we really support the policy? Or do we just support it because our political tribe supports it? Are we thinking about stuff for ourselves or just figuring out which side our people are on?

To use a sports analogy (that I’m not sure really works): Do we really care about the guys on our team, or are we just rooting for laundry?[1]

[1] When he played for my team, Johnny Damon represented the paragon of lovable caveman-hood. But when he left for the Yankees, all that overdeveloped forehead (from, um, vitamin supplements I guess?) seemed gross. When he played for my team, Wes Welker was a virtuous, fast-as-a-tiny-quantum-electron, tight-end. When he crushed my spirit this past weekend with Satan Manning, well then. Welker is such a loser and a sell-out, in his goofy space helmet.