“If a family was sending their child to college this fall, AND they were fully able to pay cash (from an educational tax deferred plan) what would their monthly contributions look like for the previous eighteen years?

Assumptions – gross household income in 2014 is $100,000, and was steady but average 2% less each previous year.

Total annual expense $40,000 year one (includes living expenses). Expense increases by 3% each year.

Student earns degree in 4 years. Returns would track S&P 500 (or other index) to keep it simple.

18 years ago, this disciplined family started socking away $X each month in preparation?”–Todd R.

Todd, Thanks for the good question.

We could calculate this a few different ways, some easy and some complex.

I’ll start with the easy.

Simplest answer: $4,990 per year, or approximately $416/month.

Let me break down this simplest calculation to show the assumptions underlying it.

I assume each contribution is made on the first day of the year, and each contribution enjoys a full years’ growth at the assumed rate of return.

I assume the family makes 18 years’ worth of contributions to an education fund, starting in the year of the child’s birth and continuing non-stop through matriculation at college. I assume the family continues to fund the same amount in years 19, 20, 21 and 22, but that money does not get any return on investment. It just goes toward expenses.

I assume the costs of college, in years 19, 20, 21 and 22 are $40,000, $41,200, $42,436, and $43,709, respectively, reflecting the annual 3% rise listed in your scenario.

I assume a steady, 5% return on investment, every year, year in and year out, for 18 years.

I’ve ignored the income portion of your scenario for the moment.

After this I’ll update with other ways to answer the question, but I think this is a reasonable first approximation.

One concluding, scary, thought: NOBODY I know is saving $416 per month, from the month of their child’s birth.

My main take-away from looking at my own family’s EFC estimate on the College Board site was jaw-dropping because there is Just.No.Way.

Where would an ordinary (non-wealthy) family be able to come up with that kind of cash to pay for college? Every year? For just one kid?

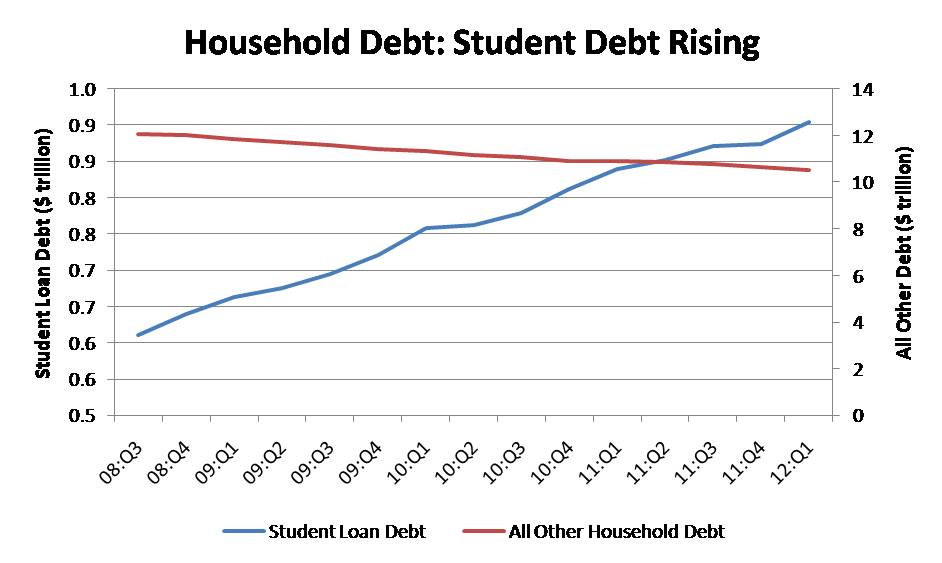

The answer, of course, is that very few families can come up with that kind of money, so students and their families take out extraordinarily large student loans.

The New York Times Op-Ed explains the pernicious effect of the federal government-calculated EFC. When all families receive a ‘government number’ it sets an artificially high floor for college tuition prices.

The Op-Ed also explains why some high-priced private universities may offer cheaper educational access to students than public universities, via the private universities’ generous financial aid packages.

The article also helpfully reviews some of the not-applicable, and not-generous, federal grant money available to families.

Finally, the Op-Ed recommends that Congress drastically cut the EFC by 75%, to reflect the fact that tuition cost hikes since 1980 have drastically outstripped inflation.

This proposal will not go over well in higher education circles, to say the least. Fortunately for colleges and universities, according to the article, they have spent a half-billion dollars lobbying Congress in the past 5 years, the eighth-highest special interest category.

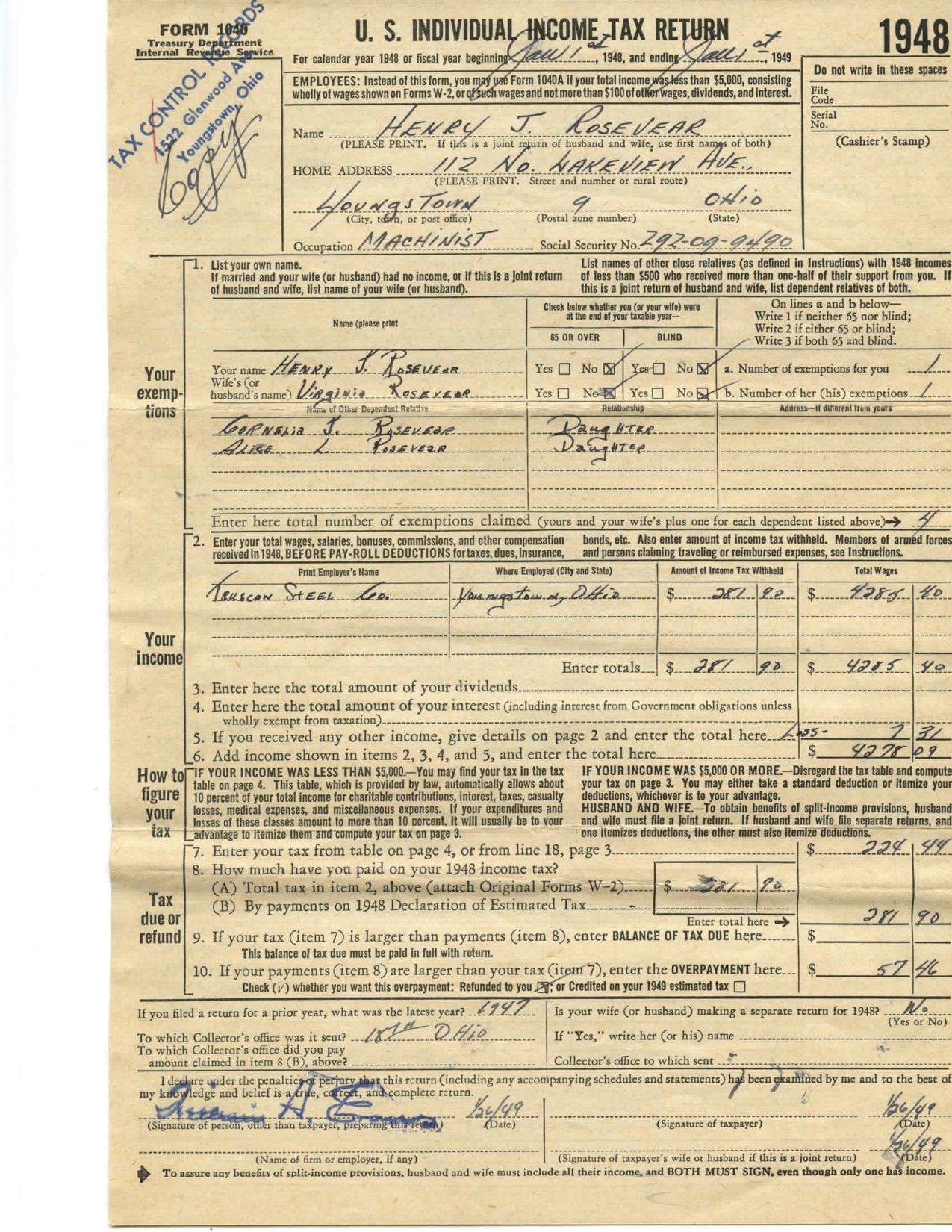

My friend – whose grandfather worked in the steel industry in Youngstown, OH – found his old tax return and thought Bankers Anonymous readers would get a kick out of it.

I don’t know why I get a kick out of it, but I do.

Some things remain the same from those times until now, including incurring a ‘loss’ on rental property.That trick never goes out of style.Rents, however, have gone up considerably since the $210/year for a duplex rate in 1948.I can see on the form that he bought the duplex for $11,000 in 1948, so I guess he didn’t need to make that much in rent.

His income as a machinist for the Truscan Steel Company totaled $4,285, and since he’d already had $281.90 withheld, he qualified for a refund of $57.46, according to this return. Hopefully he stayed far away from the 1948 equivalent of an H&R Block refund anticipation loan.

The biggest change from then until now – besides the nominal level of prices – is the relative simplicity of the tax form. It looks like he filled this out in about 10 minutes.

As I look forward (with dread) to spending hours gathering tax information this coming week, only to pay thousands to my accountants, I wish doing ones taxes was not so complicated. The complication itself leads to sub-optimal outcomes.

A friend sent me an article this week regarding some of College Advisor Julie’s comments about the rise in college administrators.

The article, linked to here, presents the following dramatic assertions:

1. Non-academic administrative positions at Universities have doubled in the last 25 years, without a proportionate increase in students served.

2. During that same time period, part-time and teaching-assistants (lower-cost labor) have increased from 1/3 to 1/2 of all teaching assignments at colleges and universities.

3. Inflation-adjusted tuition (meaning: real-term dollars) has doubled at private colleges and universities, and tripled at public colleges and universities in 25 years.

Ohio State has the Highest Paid Public University President

The article has a colorful quote from economist Richard Vedder, responding to the claim by university administrators that they are doing everything to cut costs:

“I wouldn’t buy a used car from a university president,” said Vedder. “They’ll say, ‘We’re making moves to cut costs,’ and mention something about energy-efficient lightbulbs, and ignore the new assistant to the assistant to the associate vice provost they just hired.”

That’s pretty mean, but also funny.

At this point I need to apologize to my close family members currently serving in university administration. Hey, at least you’re not a (ex-)banker!

Michael: Hi, my name is Mike and I used to be a hedge-fund manager.

Julie: I’m Julie. I am a college advisor for over 25 years.

Michael: Does college as traditionally understood – a four-year institution – make sense anymore? The clear alternatives are:

1. Community college for a few years and then enroll and do the final years for your terminal degree

2. Or online learning

3. Returning to more vocational learning.

Julie: I think all three of those have to be much more heavily explored. The only predictor of graduation from college now is family income. Scores, or grades, do not predict graduation from college, only family income. This is not the meritocracy that we like to think we have. It’s really sad that that’s the case. I would like to see, instead of more and more beautiful and elaborate live-away-from-home paradises at higher and higher costs, with many many more administrators, I would like to see some change along those lines, those three that you mentioned, and see if we can get back to some sort of reality.

WHAT DOES COLLEGE REALLY GIVE US?

Michael: In your opinion, what does college at this point really give you that can’t be otherwise obtained online or with more vocational training? Is there something that you just can’t get or are we just not exploring deeply enough what you can get? I’m interested historically, 50 years ago versus today but also just today and for the next 30 years; do we just have the wrong model or is there something intrinsically essential to the traditional four-year college model that you really can’t reproduce in any other way?

Julie: I would find it hard to know what that is. I think the kind of education that my students get in high school is I think life changing and it’s a very intense experience intellectually as well as in terms of the skills. The whole myth of the “college experience”: living away from home probably for the first time, it seems to be very heavily involved in alcohol consumption.

I’m not saying this is new but I just don’t know that it’s absolutely necessary. I also think that many students are not getting an exciting intellectual experience. They’re in big lecture halls, if they even go to the lecture. Class participation is based on pushing a clicker to show you’ve been there. Is that really going to get them much, change them in some fundamental way for the better? I’m not convinced. I think we really need to rethink a lot.

Michael: It’s pretty grim sometimes when I think about it. College at the elite level seems to be somewhat about training the mind a little bit; a lot about cultural capital you acquire through friendship networks and broadening your horizons. Whatever small community you came from suddenly is expanded. Then in a large sense it seems to be market signaling to potential employers and potential mates and potential colleagues; that I’m a person of your group, as shown by my degree from that institution you’ve heard of. That seems to be a lot of value, like buying a brand. It’s not the value we admit that it has, which is supposed to be “I got a great education.” But it seems that’s a very small part of it.

Julie: Granted, it’s certainly what a lot of my families want and what I got and you got. But that’s just a very small number of people in this country that are going to end up with that little extra branding.

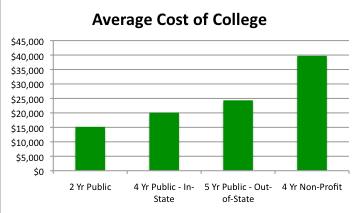

IS A PRIVATE COLLEGE AT $50,000 A Year A GOOD DEAL?

Michael: Outside of the market signaling and cultural capital you acquire at an elite place, what are you getting for something below that, but you’re still paying pretty much full freight at $50,000 a year? Is that a good deal?

Julie: I think it’s okay if you have a lot of money and you want to spend it. But I don’t think it’s a great deal. It’s hard for me to think there are places where you should spend 50,000 dollars instead of 25,000 dollars. Now, granted, a great many people are going to get financial aid and decent merit aid, so for the majority of people it isn’t a question of 24,000 versus 55,000. There’s going to be a narrower gap. But for you who just went online and found out that you’re supposed to come up with the first 50,000, you could go to the University of Texas for probably 20,000. What would make you think that you’d want to mortgage your life and your child’s life to spend the extra $30,000 per year?

Michael: It’s got be very worthwhile.

Julie: Yeah and I’m not sure that anyone is offering that big a difference, even if we compared top status with University of Texas status. That’s a lot of difference, unless you really are rich.

TEXAS GOVERNOR RICK PERRY PUSHES A $10,000 COLLEGE DEGREE

Michael: One of the agendas of Texas Governor Rick Perry, interestingly enough, is instituting the 10,000 dollar a year undergraduate education,[1] which is so far mostly talked about rather than implemented. It’s not available yet, I don’t think.[2] But it’s seemingly a big agenda of his. It seems to be something we would applaud and you would think this is technologically available and totally necessary. If you could get the learning part of it not to be out of reach at 10,000 dollars a year, it would be harder to acquire the cultural capital of living together but as you said; much of that may be beer-based.

Julie: I am a big believer that many, many things about education require some group activity with a teacher. But that doesn’t have to be – and I don’t really see a great deal of value in – the 250 people in the lecture hall being lectured to by the professor. I cannot see why a lot of stuff couldn’t be done online. And of course a lot of the students know it’s online and they don’t go to the big lecture. And then save the money for the small encounters with the other students and the teacher. Which would then we hope some of that would really be meaningful.

Michael: If Rick Perry was really able to institute the 10,000 dollar undergraduate education in Texas, that would be pretty transformative. I think people would pay attention. It seems the market for undergraduate education is ripe for a disruptive innovation there. I think it’s a bubble, and if interest rates change, that bubble could burst and these not-quite -top-tier colleges could be in deep trouble trying to justify – why are you charging $50,000 when this other group has figured out how to provide essentially the same product for $10,000? It would be interesting to see. It’s a neat idea of an experiment. It seems like the industry is ripe for disruption that way.

TX Gov Rick Perry as an undergrad. Could he disrupt the college education industry?

EUROPEAN AND ASIAN UNIVERSITIES ARE DIFFERENT

Julie: I would be very interested. Keep in mind that in Europe and Asia, developed countries, there is no great tradition that the majority of students go off and live in a dorm for four years. That’s a luxury item that we’ve invented. That’s not to say people aren’t doing that, some people, but it’s much more common that you go to university in your area, your town.

Michael: Living at home, saving that money, and spending only on tuition.

Julie: Yeah, and some great universities have operated that way in Germany, France, and elsewhere. I would like to see much more emphasis on how can you have your big lectures done for less, and if it has to be electronically that’s okay with me, and then how can you have some meaningful student involvement with their peers and teacher in a way that really works. A section of 40 people, that doesn’t work. I’m now ready for a lot of experimentation.

I’ve loved being educated. I love working in the school. I’m definitely not one to feel people don’t need more education but we really need to be thinking of some different models. We need to be thinking of lifetime learning. We need to think about whether our government policies need to be directing and encouraging students to certain kinds of careers as opposed to others.

We have no national policy that pushes some of the education we know we need to push, such as engineering, science, math. Other countries have maybe too rigid a policy. Ireland has decided it’s going to come back from its financial debacle by having the government be very involved in what it’s going to support in terms of education. That’s what is going to put them back on their feet. Maybe that’s a model that would be way too coercive for us. But is it really a good idea that we have no national policy that I can discern?

Michael: They’re going to determine how many engineers per year, how many dentists per year, that kind of thing?

Julie: They’re certainly going to put their money where they think the economy should be going. We’re not doing that.

[1] I had this wrong in the interview – Its actually $10,000 total, a much more ambitious target. Here’s some more information on the plan. The Austin-American Statesman says the target is sort-of, kind of, reachable.

[2] Actually – My information in this interview was not correct. It is available. But it’s not very widespread yet. The program requires a student to accumulate many college ‘credit hours’ during high school, it may rely heavily on online learning, and the $10,000 all-in cost usually does not include books.

In this interview, Julie – a college advisor, offers her perspective on the rising cost of college, which has become financially unfeasible for most middle class families in the last 25 years.

Michael: Hi, my name is Mike and I used to be a hedge-fund manager.

Julie: I’m Julie. I am a college advisor for over 25 years.

Michael: I’m interested in the perspective of a private college school college guidance counselor. But understanding that for many or the majority of people, they are not in private school, so your financial picture will be a particular slice of American life. In your experience have parents typically prepared for the cost of college by the time the student is getting to their junior year, or are they taken by surprise?

Julie: Actually my parents are not particularly rich. We’re not in a very affluent area and so a lot of my students have financial aid at our school, even though we’re only a day school and don’t have a very high tuition.

Most parents, however, have not been able to prepare for college because if they are thinking in terms of a private college in the northeast where we live, the cost now is 55,000 dollars or as much as 60,000 dollars. It’s very hard to save that money, even if you start the day the child was born. That’s a very hard thing to prepare for.

Julie’s school

CALCULATING BORROWING NEEDS FOR COLLEGE

Michael: I went to the College Board site that you pointed out to me, and inputted some of my information. Indeed, although we don’t feel like we have a lot left over at the end of any month or year, it’s a 49,000 dollar estimated obligation according to the College Board, for a typical four-year college. It’s kind of a scary experience to put in your numbers and think I’m not wealthy; I’m just kind of ordinary getting by here, and yet the institutions are basically saying “thanks for your numbers; you’re going to pay-“

Julie: 200,000 dollars at least for college. You’re the banker. How much would someone have to be saving every day, every year, from the day a child is born to have 200,000 dollars by the time the child was 18? Even if they got 8% return, which they’re not getting anymore, how much would they have to be saving every year?[1]

Basically I will mention to people you’ve got to run these numbers and that was junior year I brought it up. But they [the parents] don’t want to run them because they don’t want to know. So senior year rolls around and they may not have even run the numbers. Then I can’t give very good advice because if they have 200,000 in the bank or they have a very high income which means they could scrape up 50,000 a year, after taxes, that’s one thing. But that’s not the majority of people.

If they’re not going to get very much in financial aid, they really need to be thinking what is a lower cost college, what could I have instead. That’s going to have to be either a state university, possibly a Canadian university. Maybe they could go overseas, but they can’t go to a private college in the northeast.

Michael: Among the private school families then that you’re dealing with, what percentage of parents or kids or the combination are willing to forego the high cost, presumably higher status college to go for the lower-cost approach? What percentage of your 25-30 students are actually making that choice at the end of the senior year?

URGING AGAINST TOO MUCH DEBT

Julie: That’s a good question. Last year I had a lot of students who at my urging were trying to avoid high debt. The problem is that you can get into a college that costs 55,000. Your parents can maybe come up with some money, and then the college might even give you 15,000 or 20,000 but there could then be this gap between what you can squeeze out from the home income and the small amount of financial aid you’re eligible for. That gap can be easily filled by borrowing by the student. The colleges will help arrange for the kid to borrow 15,000 or 20,000 dollars. I don’t want them to do that.

Michael: To what extent are those families who are choosing to fill the gap with 25,000 dollars of a student-loan debt, in your opinion are they fully understanding the implications of the debt or are they saying there’s nothing more important than a college education for my child so I’m doing it, or do you think they’re closing their eyes and doing what we would in another context say it’s really irresponsible to run up 25,000 dollars of credit-card debt? Yet they’re doing it in another form through student-loan debt because student-loan debt is considered good debt. Are your families walking into this with their eyes open?

Julie: Recently, I think a lot of them have taken my advice, which is they don’t want to do that. They’ll choose the option that has the lowest debt. But that will still be at least 5,000 dollars for the student. If you can get into Harvard, maybe it’ll be less. Wellesley – that’s pretty good financial aid. There are a few places that are so rich they really give significantly better financial aid than every place else. But most students are facing at least, if the parents don’t have the full amount, at least $5,000 a year in debt.

Michael: Which is $20,000 at the end of four years.

Julie: Right, but most of the packages will be closer to $12,000 to $15,000 per year.

HISTORICAL COMPARISON

Michael: So you’re getting up to $45,000 dollars worth of debt or $60,000 dollars worth of debt for a 22-year old. What is the historical comparison? Have you been doing this for close to 30 years, what was it like 30 years ago?

Julie: The problem is my children went to college 20-30 years ago. It was expensive but it was manageable. But in the last 25 years, the rate of increase of the cost of college has been astronomically much higher than the regular cost of living increase. You have 2-3% cost of living increase and you’ve got 7-8% every year compounding in the cost of college. The numbers now simply don’t work. What was a sacrifice for people 20-30 years ago is now simply an impossibility without tremendous debt. Of course, the starting, average salary for a college graduate has actually in real dollars declined over the last 20 years. It’s a pretty scary situation.

IS THE COST OF COLLEGE A BUBBLE?

Michael: In financial terms there seems to be an analogy between, say, the housing bubble that we experienced from 1998 to 2008 in which that asset price – housing price – went up by 10-15% per year, year-over-year, and yet peoples’ incomes didn’t increase to that extent. If the nominal rate of inflation is 2%, and the price of college is going up 7% year-over-year for 10-15 years, it does seem to be an unsustainable sort of asset-price bubble, analogous to the housing market.

Julie: What you have are the most expensive, elite colleges, are heavily populated by very affluent people, even though a place like Harvard or Princeton will give tremendous financial aid; they still have 75% of their applicants, are pretty well off.

Michael: One of the thoughts I had in your discussion of the asset-price bubble of college tuition, if indeed that’s what it is, is the relationship between the cost of debt which got very low – the cost of mortgages, mortgage rates were very low while asset prices were going up. At the same time analogously the student loan debt is extremely cheap from an interest rate perspective, which kind of helps subsidize the extraordinary principal amounts of student-loan debt. If it’s at 3.5% you can carry 50,000 dollars, whereas if it was at 8% or 10%, where it might have been 30 years ago in the ’80s, you can’t really carry 50,000 dollars worth of debt as easily.

But it’ll be interesting, as it is real estate reacts very quickly to changes in interest rates, if interest rates go up, real estate prices typically drop quickly. It’ll be interesting and unpleasant presumably for universities, if interest rates go up and suddenly people can’t really carry 50,000 dollars of what was previously 3% debt, then becomes 7% debt. There has to be a reaction to that, although the government is heavily involved in the student-loan market, keeping it low.

Julie: There’s no question that if the government had not been subsidizing these loans and making them so easy to get, that we’d have a different situation. On the one hand, we’d have even more of a premium on being well off to be able to go to college. On the other hand, colleges might not have been able to increase their costs and prices as they have by 7% and 8%. Because where would the money have come from? A few elite schools are going to be able to price it at almost anything, but I don’t really see how all the small private schools that are not highly regarded are going to be able to keep up this situation.

COLLEGES GET PRETTY MERCENARY

Julie: I’ve had people come to my office who are representing the college, and they’re admissions officers out recruiting. I’ll say what about this student, would this be a likely fit for your college? Would she fit the profile for admission? If I mention the person is a full pay, they’ll say “Yeah yeah, full pay, I think they’ll probably get in.”

Michael: That’s pretty mercenary.

Julie: It’s pretty bad. But they’re just being truthful. That’s now almost your best bet for admission, not at the most competitive school, but at many, many, being a full pay is going to be very useful to you. And if you’re a full pay at any college other than the most elite, you’re likely to get a discount. For a college that charges $55,000 and you’re basically a full pay, they’ll discount it by $10,000 or even $15,000 because they’d rather get someone who’s paying $40,000 than have to subsidize someone who can only pay $10,000 or $20,000. That’s what the whole merit aid system is; it’s a subsidy for the people who are basically full pay but might come to your school, your college if they’ll discount the tuition. Outside the elite colleges, all schools are giving merit aid, discounting the price. The discount is bigger for students with high scores and good grades.

Michael: Is there any good news? What kind of students get financial aid or merit aid or sport scholarships or international students? What do colleges actually pay for, anything happy?

Julie: Anything happy? They’re trying. The colleges aren’t trying to rip people off. But they have for some reason felt that their college needed to be spending money and raising their price by 7% or 8% when inflation wasn’t anywhere near there. That’s where I’m critical of the colleges. I’m critical of this huge change in how many teachers there are. There isn’t a huge change. But how many administrators there are, there’s a huge change. Why is that? What became so hard to manage?

Michael: The mean version would be the students need to have their coddled lives, but maybe I just sound like an old person resenting those college students having a good time.

Julie: I don’t think it’s probably related to the kids as much as bureaucracy tends to grow. That’s just the way it is. And if the money is there – or seemed to be there – because it was easy to borrow it, for the students, where would be the incentive for them to lower prices, never mind hold the line?