In a recent post I mentioned that business owners may – among other benefits of entrepreneurship – achieve some tax savings. This week, inspired by my words, you’ve decided to hang a shingle.

However, you need money. But where can you get money for a small business?

Let me tell you all the great ways.

Inherit the money

I can’t recommend this highly enough. Your first $5.45 million of inherited money comes to you tax-free! Up from $5.43 million way back in 2015! And you don’t even have to work for it! Let’s make this happen, people!

Sadly, you need to be born into the right family, which is tricky to make happen on purpose. Also sadly, a beloved family member has to die at the right time. This is impractical for most of us. Let’s review the other great ways.

A bank loan

Naturally, you could simply walk into your bank and tell them about your great skills, customers, and market plan. Your friendly banker pulls your credit report and quickly understands your business plan. You’ll walk out with the money you need to grow and expand your small business. It’s so cool. This is the best way to get money for your small business.

Ha-ha. Just kidding. This is the worst way, because banks don’t actually lend money to new small businesses.

When you try this (Actually I don’t recommend trying this, but feel free to knock yourself out) your friendly banker will ask for two years of financial records and business tax returns. Then you try to tell him about your great skills, customers, and market. He will stubbornly return to your lack of two years’ financial records. Eventually you realize this is a dead end.

A friend or family loan

Let’s pretend your friend or family member (hereafter known as “framily”) has money, understands you, and wants to help. Your framily1 doesn’t need to pull credit or make you wait for two years worth of business financials. Your framily lends you just the right amount of money, and she only asks for an affordable interest rate in return. Maybe best of all, when your small business succeeds wildly, by taking a loan you keep all the business ownership to yourself, so you can get rich without having to share that wealth with your framily. This is the very best sort of money for your small business.

No, wait, it’s totally not.

First of all, your small business faces very uncertain prospects in its first few years, at best a ‘feast or famine’ type of profitability. A fixed rate loan, with the obligation to make regular payments – every single month – invites disaster. Many months, especially in the beginning, you might find it impossible to pay your loan.

Which of course leads to the second issue of borrowing from your framily. Defaulting, or even asking to restructure a loan from framily will put grave stress on your closest relationships. In sum, never get a business loan from a friend or family member.

Equity investment

Well now, wait a minute, clearly the best way to raise money for your new small business is to approach your framily, and instead of getting a loan, you get a direct equity investment. You sell part ownership in your business. Your framily believes in you and is flexible and, unlike in the case of a loan – which requires fixed monthly and possibly unaffordable payments – you only need to share profits (eventually!) with your new co-owner(s). Clearly this is the very best way to raise money for your small business.

No, sorry, this is a terrible idea. Been there, done that.

In the best case, you’ve given up too much of your future profits to someone else.

In the more probable worst case (Remember, most small businesses fail in the first few years!) you have now lost the money of your closest relationships, in addition to losing your hopes, dreams, and income source.

In my own case, I lost the money of my best friend, mother, and eight-grade English teacher, among others. This isn’t fun. Be sure to budget in money for therapy, which isn’t cheap, either.

How about instead of friends and family, you raise equity from professional angel investors or venture capitalists? This may remove the therapy part of the equation if you fail, because we may feel less remorse after losing the money of professional investors. On the other hand, the professional investors will likely negotiate a better deal for themselves than would your framily. They are the shark at the poker table and you are the fish. So if you do well with your small business you’ve probably given up too much of your future profits.

Crowd-sourcing

I don’t believe in this except for non-profits and marketing purposes

I have not yet mentioned new-fangled techniques for raising money, such as crowd-sourcing.

Call me old school, but I have yet to hear of a legitimate for-profit business that effectively crowd-sourced money. I believe in crowd-sourcing as a great marketing tactic, and possibly great for non-profit or charitable projects as a result, but I don’t think it works for most small businesses.

My point

What’s my point in raising and then rejecting all of the available small-business financing options?

Simply this. It’s really, really hard to raise money for a small business. If you know a successful small business owner, give her a hug. She deserves it.

In an upcoming post – just so I don’t leave you bereft of hope – I’ll mention a few small business financing alternatives that you could try.

After I wrote this I Googled ‘framily’ and found it’s a phrase used by Verizon to pitch their phone plans. Ugh. Really didn’t mean to be promoting them. ↩

One thing worse than paying our taxes is the idea that other people avoid paying their fair share of taxes.

On the subject of tax avoidance by other people, I can think of at least three principal feelings. As the kids say, I feel all the feelings.

Outright tax fraud

People everywhere on the political spectrum can get angry about outright tax fraud, whether it’s hiding income in offshore accounts to avoid income taxes or shielding inheritances from estate taxes.

A new book by Gabriel Zucman The Hidden Wealth of Nations estimates the size of offshore wealth at $7.6 trillion worldwide, or 8 percent of global wealth. In the US, Zucman estimates $35 billion in lost tax revenue per year due to hidden assets. Meanwhile, governments worldwide lose up to $200 billion in annual revenue from hidden tax havens, with a significant burden of this $200 Billion in fraud falling on developing countries’ governments.

Wealthy folks hold financial assets principally in Switzerland, Luxembourg, and known tax havens such as Cyprus or a myriad of islands in the Caribbean.

One exception to my outrage, I suppose, is petty tax fraud such as when my barista fails to report to the IRS each and every dollar she removes from the tip jar at the end of the day. In that sense the minor scale of her tax fraud diminishes my outrage, as well as the fact that the barista isn’t herself wealthy. Also she supplies my drug of choice. Still, fraud is fraud, and it’s never cool.

Clever tax avoidance

My feelings slide from “outrage” over to the milder “envy” when I read about some billionaires’ strategies to legally avoid taxes, such as the strategies explained recently in the New York Times. In an article titled: “For The Wealthiest, A Private Tax System That Saves Them Billions” the authors describe leading hedge fund founders whose investments in Bermuda-based insurance companies reduce their tax bills.

Their ability to guide tax legislation through Congress and to finance presidential campaigns does stick in my craw quite a bit, and should offend those of us who still hold out hope for our democracy. On the other hand, most of the specific clever tax avoidance that the article describes can be described as the benefits of simply owning a business – albeit in their cases, big ones.

Now, of course, you could decide to hate the fat cat hedge fund guys who simultaneously write the rules on creating income tax loopholes and then nimbly leap through those holes to the tune of billions in annual savings. I think generating that outrage is the main point of the New York Times article, and I don’t blame you too much for feeling that way.

Alternatively, you could decide not to hate the player and just to hate the game. By that I mean, understand that a major part of the ‘scandal’ exposed by the article is simply the trick of turning ordinary (high tax-rate) income into long-term (lower-tax rate) capital gains. The other trick – and this is really simple – is to invest in a business that appreciates tremendously in value over a long period of time but that only gets taxed when you sell it. And then don’t ever sell it. Like, to take an example I recently wrote about, buying a stock and holding it for thirty years, or for forever.

Look, I don’t intimately know all their tax tricks, but hedge funders investing in offshore insurance companies mostly just extend this year’s short-term income (a nearly 40 percent tax rate this year) into long-term capital gains (a 20 percent tax rate, eventually). It’s legal. It’s clever. I’m envious, but I’m not particularly angry.

This is basically how Warren Buffett famously pays a lower tax rate than his secretary. When you read about Buffett or Facebook’s Mark Zuckerberg merely claiming the proverbial $1 per year in salary, you really shouldn’t be impressed with their admirable lack of avarice. Rather, you should note their tax savvy. They make their money through (tax-advantaged) business ownership rather than through (tax-disadvantaged) wages.

It’s an open debate – actually it’s not, but maybe should be? – whether labor ought to be taxed at a higher rate than capital, as it is today. But those are the rules. And remember the Golden Rule you learned in Kindergarten, “He who has the gold, rules.” So save your hate for the player and just hate the game.

Imitation: Own a Business

By the way, if you personally want to start to save money on taxes like a baller, you need to own your own business.

I’m not your accountant, and you really shouldn’t take tax advice from some blogger you found online. But you should set up your own business – like today – if you want to reduce your personal tax bill.

Will you use a cellphone and monthly internet service for your business? What about a computer for record-keeping? Or perhaps a car with your business logo on it? If you are in the 25 percent income tax bracket, and those are legitimate business expenses, all of these will cost you 25 percent less, in after-tax terms.

If the business you own happens to pay you annual profits in dividends, you might enjoy favorable income tax treatment, when compared to taxes on ordinary wages.

If you can control the timing of when you actually get paid by the business you own, you may realize considerable income tax savings through timing your income from one year to the next. If your business makes an expensive investment this year that happens to reduce your annual profit, you may end up paying little to no taxes this year, even as your business grows.

So, my journey from outrage, to envy, to imitation can be summed up as:

Workers of the World, Unite! Start up your business today! You have nothing to lose but your chains (And your top tax rates!)

Unfortunately, as Marx and others discovered with the Communist Revolution, this is easier said then done.

First things first,1 never buy a lottery ticket. Seriously, ever.

Having said that, obviously I did buy a few this past week because, you know, I’m an irrational human.

I’ll be the first to admit it. I also sometimes buy “King Size” Reese’s peanut butter cups (that’s the four-in-one size) in the checkout line at the grocery store and, man, they’re gone by the time I make it to the car. So, I allow myself bad decisions from time to time.

But this is not confession-time with Mike. Rather, it’s financial math-time, with a Powerball lottery theme.

A friend asked me over Facebook whether it made more sense (when he wins the whole shebang this week) to take the lump sum or 30 annual payments.

Another example of bad decisions by me.

What I’m not analyzing

Now, I can think of lots of valid ways to answer the annuity versus lump sum question, and I’m going to skip most of these to focus simply on the mathematical way to think about it. In that sense, I will be simplifying the issue terribly – disregarding factors such as personal circumstance, economic utility, needs and wants of heirs and recipients, current and future rates of taxation, variations on self-control, and personal health/longevity. I only want to use the example of the lottery to illustrate some important financial mathematics.

And before you decide to skip the math analysis (because math is soooo boring, blah blah blah), just know that this math formula is the basis for ALL fundamental investing – All bond analysis, all stock analysis, all real estate investing, all business investments. Everything. If you don’t use this math, you’re just guessing. Well, even if you do use this math, you still may be guessing, but you’re guessing less than you would have guessed without the math.

The math is called “Discounting Cashflows,” and probably by now you’ll have wised up to the fact that I’m piggy-backing on the Powerball lottery story to slip in a lesson on what forms part of the most powerful financial math in the universe.

So like I said, I’m skipping whether you think you’ll live for another 30 years and whether that makes you want to gratify your material wants this year. I’m skipping the issue of taxes partly because we don’t know what tax rates will be like over the next thirty years, and also because taxes are part of the reason why lotteries in particular are a mug’s game.2 I’m skipping the issue of squandering all the money3 this year versus stretching out your squander over 30 years. I’m skipping whether you have great philanthropic desires that may be satisfied this year or in later years when you (finally!) acquire more maturity and thoughtfulness.

Ok, with all that throat-clearing and telling you what I won’t analyze, let’s move to the mathematical issue of:

Annuity versus lump sum

What the math explained below can tell you, precisely, is whether a lump sum today is worth more or less than a 30-year annuity payout, given your % return assumptions.

To properly compare your lump sum option today to the 30 annual payments option, you first have to assume a % annual ‘return’ that you would expect to be capable of generating those annual payments.

Introducing: “Discount Rate”

The assumed “% annual return” I mentioned in the previous sentence goes by a couple of different names when you do this math. The alternate names include Annual Return, IRR (Internal Rate of Return), or Yield. The best math name for this particular situation is Discount Rate, but in practice it ends up meaning the same thing as those other names.

How do we come up with an assumed Discount Rate? There’s some art here as well as science, and a useful Discount Rate for this situation adds up factors such as inflation, prevailing interest rates, and the riskiness of each annuity payment. Without getting into a tangential detour about coming up with the ‘right’ number for the ‘Discount Rate,’ on lottery payments4, I’ll just grab one for now and move on to showing the math. Let’s call the right Discount Rate on future annuitized lottery payment 3%.5

Discounting future cash flows

Money arriving one year from now – or 30 years from now – is always worth less to me than money in my bank account today.6 We can understand this intuitively by thinking about the fact that you can’t literally buy beer and a hamburger today with money promised to you one year from now. Also, in one year, or thirty years, your circumstances may change, which would make you value money in your bank today above money owed to you in the future. Also, future promises are inherently risky. What if the person owing the money, or the lottery commission for that matter, never pays you in the future? What if inflation reduces the purchasing power of the future money? For all these reasons, we say that money today is worth more than the same (aka ‘nominal’) amount of money in the future.

But how much more? The point of discounting future cash flows mathematically is to turn that intuition I describe in the prior paragraph into a precise number telling me ‘how much more’ I value today’s money than future promised money.

This is the heart of comparing my lottery lump sum to a series of 30 annual payments. It’s also the heart of figuring out how much money I’ll earn if I buy a bond at a set price, or a stock at a set price, or a rent-generating piece of commercial real estate, or a profitable business. In essence, in each of these situations, I’m asking how much would I pay today to generate a series of future payments, at a given assumed rate of return?

Would you just tell me the math already? Geez!

Ok, fine. Let’s say you win the total Powerball payout this week (as of this writing) of $1.5 Billion. And let’s say the annuity deal is you can receive 30 equal payments of 50 million each year7, starting one year from now.8 And let’s say the lump sum offer today (as of this writing) is $930 million. Which one is worth more, the lump sum or the 30 annuitized payments?

Our math challenge is to ‘discount’ each of those 30 payments of $50 million into an equivalent value in today’s dollars. That consists of 30 different calculations. What is $50 million – one year from now – worth today? What is $50 million – 5 years from now – worth today? For that matter, what is $50 million – arriving thirty years from now – worth today?

Each of the separate 30 annuity payments gets discounted separately. Mathematically, 1 year from now is different from 2 years from now which is different from 30 years from now. For simplicity’s sake, I’m going to stick with a single Discount Rate – the same 3% – for each future payment.9 Also, to do this right, you’ll want to open up a spreadsheet right about now. If you are mildly competent with Excel,10 you can follow the math below by creating the following formula, and then reproducing the formula thirty times, one for each year’s annuity payment. And if you are mildly comfortable with Excel, the reproducing of the formula part should take you about 12 seconds. It’s an autofill function.

A little Algebra

Sorry about this, but I’m going to mention some algebra. This won’t hurt a bit. Just hold your breath, and…The algebra formula for discounting any future payment into today’s money is PV = FV/(1+Y)^N. Don’t worry, I’ll define everything…Ok, release breath. Phew.

In the formula you can represent Discount Rate as ‘Y’ or as in this case as ‘r.’ Doesn’t matter.

In that formula PV (Present Value) means the value of money today (which is what you want to solve for, in order to compare with the lump sum), and FV means the Future Value of the annuity payment, which in the case of the Powerball example we’ve said is $50 million.

Also in that formula Y is what I’m using for the Discount Rate, which I’ve decided for the time being is 3%. And N is the number years from now that the future payment arrives.

So, to discount a Powerball annuity payment arriving one year from now I’d say that the Present Value (PV) is equal to $50 million/(1+3%)^1. Which, my Excel spreadsheet tells me, is $48,539,758. In plainer English, I should equally value $48,539,758 today, or $50 million set to arrive one year from now.11

To discount a Powerball annuity payment arriving two years from now I’d say that the Present Value (PV) is equal to $50 million/(1+3%)^2. Which, my Excel spreadsheet tells me, is $47,125,979. In plainer English, I should equally value $47,125,979 today, or $50 million set to arrive two years from now.

To give you a sense for the power of discounting, my Excel tells me that the $50 million payment arriving 30 years from now is equivalent to $20,585,997 in today’s money. You can check that math yourself by plugging in $50 million/(1+3%)^30 into Excel, or your calculator.

To solve the lump sum versus annuity question, I’d set up my Excel spreadsheet to give me a value for each of the thirty annuity payments of $50 million. Like I mentioned, this takes approximately 12 seconds for someone mildly comfortable with setting up formulas in Excel.

Once you have a value for each of the 30 payments, discounted to the present day (aka the Present Value of each of the 30 payments) then you add them all up, and compare them with the lump sum.

When I add up thirty annual payments of $50 million each, each discounted at a 3% Discount Rate between one and thirty years from now, I get a total value of $979,726,641.

Assuming my 3% Discount Rate is the right one, I can compare that value to the lump sum offer (which I mentioned above, and as of this writing) of $930 million. Since the bigger number is the sum of the annuitized payments, then I can say that the 30 annuitized payments are a ‘better deal,’ in pure financial terms, than the lump sum.

But notice something

The mathematical answer to the ‘lump sum versus annuity’ question depends entirely upon inputting a specific, assumed, Discount Rate. Change the Discount Rate, and the ‘correct’ answer changes.

If I assume a 4% Discount Rate, for example, the value of next year’s payment declines to $48,071,757 – because that’s $50 million/(1+4%)^1, and the sum of all annuity streams is only worth $864,271,673. At a 4% Discount Rate, the lump sum value of $930 million dwarfs the value of the annuity payments.

What would make the ‘correct’ Discount Rate change? In the case of guaranteed Powerball lottery payments, the most probable influence would be inflation. If the world suddenly expected 5% annual inflation for the next thirty years, for example, then the correct Discount Rate would be something above 5%, and the lump sum begins to look far more valuable than the annuity. On the other hand, low inflation and continued low interest rates would make the annuity payments relatively more valuable, because we could imagine inputting a Discount Rate even less than 3%.

Two other small points

By the way, I can set my programmed spreadsheet to tell me what the ‘Discount Rate’ is that the Powerball folks use, which turns out to be (if you use my assumptions) approximately 3.4%.12

The second small point is that if you know the Discount Rate that Powerball uses (like 3.4% in my example), you could reasonably say that your ‘investment hurdle’ for taking the lump sum is 3.4%. What I mean by that is that if you take the lump sum, and then can reliably compound an investment return on that money – not spending, just investing! – above 3.4% every year for the next 30, then you could end up with more money in the end than you would through the annuity option.

A reminder

Discounting cashflows only answers one aspect of the lump sum versus annuity question. Remember what I started out saying, which is that there are a ton of factors I’m not considering, in my interest in showing some elegant math. But at least we have a mathematical answer to the question of ‘should I take the sump sum or the annuity?’

An exhortation

I’m going to make up a statistic which, while not exactly true,13 is at least ‘truthy:’ Less than one person in a hundred understands how to do discounted cashflows math.

I believe deeply that everybody should understand discounting cashflows, in a ‘you should know this to be an adult in the world’ kind of way. Your bank understands this math and uses it to profit from transactions with you. Your insurance company uses this math when calculating your rates, and has a complete advantage over all its customers who cannot do this math. All of Wall Street is built entirely on the discounted cashflows formula.14

You really don’t need to understand the lump sum versus annuity question for this week’s Powerball. You do, however, need it for life.

Note: This is not a self-portrait

Conclusion

Real talk time: You’re not going to win Powerball. Lotteries are terrible.

But if you managed to spend some time with a spreadsheet to compare the lump sum versus annuitized payout as a result of fantasizing about the Powerball drawing, well then I’d say you’ve gained something this week. And properly deployed, what you’ve gained by understanding discounting cash-flows math could – and I mean this totally in earnest – make you wealthy in the long run.

Learning this math – and not some lottery fantasy – will make you a winner this week.

“…I’m the realest.” At least, that’s how I wanted to end the sentence. Because I’m So Fancy. ↩

In other words, considering taxes will muddy up the elegant and essential mathematic point I’m trying to make. ↩

Obviously I want to use the delightful phrase “on hookers and blow,” the proverbial natural beneficiaries of your squander. ↩

Ok, I’ll indulge in a little tangent here. The biggest influence on a thirty-year lottery payment guaranteed by a state in the US is probably the expected rate of inflation. If you think the rate of inflation will average, say, 2% over the next 30 years, then most of the Discount Rate will be made up of this. The ‘risk’ of non-payment by a state-sponsored lottery commission is low. And yes, I’m ignoring you preppers who stock up on canned goods and ammo for the imminent implosion of constitutional order, who say the state will likely dissolve over the next 30 years, with federal fiat money replaced by Bitcoins. Whatever, dude. ↩

Again, I’m not saying this is the ‘right’ Discount Rate, I’m just saying let’s pick a number so I can illustrate the math formula. Then you get to change the Discount Rate to whatever you want it to be, and come up with a different analysis of the relative merits of lump sum versus 30 years of annuity payments. ↩

The concept in this paragraph is short-handed in finance circles as ‘The Time Value of Money.’ ↩

By the way, it doesn’t matter for the math example, but the actual Powerball pays in increasing annuity amounts each year. So on a $1.5 Billion prize, presumably the initial payments are less than $50 million and the later payments exceed $50 million. But I’m going for simplicity here. ↩

Also, technically, when you win Powerball you get an immediate lottery payment straight away, followed by 29 future years of annuity payments. So the math in real life varies a little bit from my example. But since nobody reading this will be winning, and playing Powerball is an exercise in fantasy anyway, I think it’s appropriate to disregard actual real-life technicalities in the interest of learning some math. ↩

But you wouldn’t have to. If you had paranormal insight into some event happening 15 years from now (like Miley Cyrus gets elected President) and some resultant uptick in either inflation or just risk, you could build a simple math model that assumes 3% discount rate for the first 15 years, and then a 7% discount rate for years 16 through 30. Knock yourself out! Vote Cyrus! ↩

Now that I’ve introduced Excel into my method, you clever Excel-using people are going to want to tell me about a shortcut for doing present value with fixed annuity payments at fixed intervals. But there is a method to my madness in explaining the ‘long way.’ That Excel shortcut can do annual and regular discounting fine, but is not as flexible as it should be for all cases of discounting future cashflows. Shortcuts won’t help you with irregular future cashflows that arrive at irregular times. Learning the discounted cashflows math the ‘long way,’ applicable for every case, is a far more valuable skill, in my opinion. ↩

Important Note/Correction…A number of you did this math and found slightly different values. I should have clarified: When setting up my spreadsheet I always use actual dates of payment to generate the compounding period N. So for example I set up an original date of 1/1/16 and annuity payments made annually on 1/1/17, 1/1/18, etc. When you use actual dates you get an N of 366/365 (instead of 1) in 2016 (it’s a leap year) and the Actual#days/365. I didn’t clarify that in the original version of this post. Using a simple 1,2,3 etc for N isn’t wrong, It’s just I’m in the habit of using actual dates for investments and I did it this time without pointing it out. The good news: Some of you checked out the math with your spreadsheets! ↩

Update: The NYTimes has a a good article in which the reporter notes the lottery uses an assumed Discount Rate – to convert $1.5Billion in annuity payments into a $930 million lump sum – of 2.843%. The Times guy, I believe, has access to – or figured out – the exact schedule of payments, which includes a schedule of increasing annual payments, rather than the equal payments like I used in my spreadsheet. My number assumes 30 equal payments in years 1 through 30, and the real schedule is an upfront payment immediately, followed by 29 increasing annuity payouts in years 1 through 29. Since I don’t know the exact increasing schedule of Powerball between years 1 through 29, I’m going to just stay focused on my math formula. ↩

My wife, who spent her formative years in College Station TX, asked me “why don’t Aggies eat barbecue beans?” Answer: “Because they keep falling through the holes in the grill.”

That’s not nice at all! And, most likely, not even true! Although I can’t be sure because I’ve only visited College Station myself a few times.

Aggie jokes popped into my mind because CardHub.com, an online aggregator of credit card information, published a mildly interesting report this past week ranking US cities in terms of their average expected time to pay off credit card debt.

The Ranking

Aggies, brace yourselves. College Station ranked 2,547 out of 2,547 cities. That’s dead last in the entire country in terms of capacity to pay off credit card balances in a timely way. Ugh.

It got me thinking about how the home of a distinguised research institution would have the ignominious distinction of being last in the country in terms of credit card debt sustainability.

By contrast, CardHub lists the city with the #1 ranked fastest time-to-payoff credit card debt as Cupertino, CA.

Methodology

CardHub’s method for rankings went as follows. They figured out average income per household in each of 2,547 cities, according to the US Census, as well as the average credit card balance in each city, as provided by credit bureau TransUnion.

CardHub assumed a 14% annual percentage rate on balances – and then assumed an affordable payment of existing balances each month, adjusted for average income in the city.

Using that data, CardHub calculated how many months – on average – it would take the residents of a city to pay off their credit card debt.

I describe their report as only “mildly interesting” because while it purports to show something novel about average indebtedness by municipality, it’s actually an interesting example of how financial statistics may mislead and just reflect demographics.

Is it just wealth?

Cupertino, CA – the #1 ranked city in the CardHub study – is an address which you may recognize as the home of Apple, the world’s most valuable company.

Of the top 10 cities ranked by time-to-payoff – all but one are in tech-rich California cities or affluent suburban-Boston cities of Massachusetts such as Lexington or Arlington. Of the top 30 cities, many others are recognizably wealthy suburbs, including Bloomfield Hills, MI, McLean, VA, and Chevy Chase, MD.

So I guess one way to look at these rankings is just to notice that residents of high-income and wealthy cities can pay off their debts more easily while residents of poorer cities – by definition – will take longer to pay off their debts. That’s sort of obvious, and also not very funny at all.

Another Aggie joke

But did you hear the one about the Aggie who won the Texas lottery but was told he’d have to receive the money in 20 yearly installments instead of a lump sum? He was so angry! “In that case,” he said, “just give me my dollar back!”

Ok, that isn’t nice at all, either. Also, seriously, you should never play the lottery.

Or another factor?

Besides the high income and wealth factor, which I think is sort of obvious (and again, not that funny) I was wracking my brain to figure out how a college town in Texas ranks dead last nationwide in terms of time-to-pay-off credit card debt.

The best I came up with is that a plurality of the population of College Station, TX is actually students – who naturally earn practically nothing – but who do incur credit card debt in the ordinary course of their studies.

I’m pretty sure my theory is correct. According to the US Census the median age of a College Station resident is 22.3 years, compared to the median age in the United States of 37.2. Furthermore, the population of College Station in 2010 was about 94,000, while Texas A&M reported a student population that year of about 49,000. So I think what CardHub’s time-to-payoff credit card rankings really highlight – at least at the bottom – is a population of students, in their debt-incurring phase of life, rather than their earnings phase of life.

College Students

Supporting my theory about the preponderance of a student population of a city is the fact that other cities ranking in the bottom of CardHub’s list of 2,547 include other college towns like San Marcos, TX (#2,532 and the home of Texas State University) and Provo, UT (#2,531 and the home of Brigham Young University).

So, I’ve come to believe, Aggies and College Station TX can’t be razzed for ranking dead last in the country on this measure. It’s just a demographic anomaly of a student-dominated city population. I spoke to Jill Gonzalez, an analyst at CardHub, who seconded my analysis, and named for me some other prominent college towns that ended up on the bottom of the list.

A third Aggie joke

Meanwhile, my father-in-law, a long-time Texas A&M professor and Aggie booster, sent me a link to Aggie jokes online, and I appreciated the one about what Aggies think Cheerios are: Donut seeds.

I like that one. Personally, I will never see Cheerios the same way again.

The actual point

Ok, the (semi) serious point of looking at a financial ranking like “time to payoff credit card debt” is that statistical financial rankings like this can often obscure reality. CardHub’s ranking of cities may be interpreted as a demographic ranking of wealthy cities at the top and college towns at the bottom.

Very likely the Aggies of College Station, TX aren’t worse at handling credit card debt than the rest of the country. They’re just students who haven’t begun to register any income yet.

Still, it’s tempting to make a make a few jokes, no? I’ll probably be run out of town for this post.

Editors Note: To avoid hate-mail from Texas A&M boosters, I’ve decided to remain anonymous, except for the fact that a version of this ran in the San Antonio Express News.

In November I took my five-year-old’s life savings (mostly tooth-fairy money and birthday gifts) and bought her 4 shares in Disney stock via a custodial (UTMA) account.

Fellow readers of If You Give a Pig a Pancake will already be familiar with the idea that certain actions lead inevitably to reactions. You see, if you give a pig a pancake, next thing you know she’s going to want syrup. And if you give her syrup, she’s going to get all sticky and ask for a bath. And if you buy Disney shares with your five year-old’s tooth-fairy money, next thing you know you’re going to walk into her room to say good night, and…

“Daddy?”

“Yes, Sweety?”

“I want to sell my Disney shares.”

“Um, what? No. No! NO! Stop!”

“But I don’t like that all my money is gone from my bank.”

“Gah!”

You see, right there, that’s the problem with five-year-olds and their stock portfolios. They buy the thing and then they want to sell it.

Actually, no, that’s not the problem of five year-olds.

That, right there, is the problem with all people and their stock investments. They want to sell them. They don’t like that the money leaves their bank account. And the value can go down. I’m here to say: Don’t sell. No matter what.

The whole darn thing won’t work if you sell.

Magical Fairy Dust

You see, stocks produce magical pixie dust if you treat them right. Buy them in diversified bundles (like a mutual fund!) Then treat them with benign neglect over the next, say, thirty years, and you will be rewarded with a pot of gold at the end of the thirty-year rainbow. Tinkerbell herself couldn’t produce anything more magical than your diversified – hopefully low cost! – mutual fund.

Ok, let me stop here for moment. Maybe pigs, pancakes, pixies and pink castles are not getting the message of NEVER SELLING across strongly enough.

Let me change the channel so abruptly you will be left breathless. For our next analogy, let’s go to the darkest moment in Western Civilization over the past century.

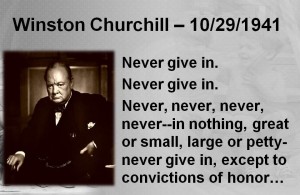

Never Give In

I’ve been reading a lot about Winston Churchill’s life lately. I can’t recommend William Manchester’s three-part biography series The Last Lionhighly enough. Summarizing 3,000 pages of Manchester’s biography into a three-word motto for Churchill’s life would go like this: “Never Give In.”

In 1940, when the Nazis controlled all of Europe between Norway and Greece, with America isolationist and Russia in a cynical alliance with the Nazis, and only the British, alone, standing against Hitler, Churchill never gave in. As he said in 1941, before the US entered the war:

“Never give in, never give in, never never never – in nothing, great or small, large or petty – never give in except to convictions of honour and good sense.”

The Nazis embodied the darkest, mostly beastly version of humanity. They built the greatest military force Europe had ever seen, fueled by sadism, racist ideology, and terror. First Czechoslovakia, then Poland, then Norway, Holland, Belgium and finally France succumbed in mere weeks to brutal blitzkrieg invasions. Imagine today’s ISIS, only they had already conquered all of Europe, with the largest and best-trained army in the world, led by a charismatic psychopath fulfilling his long-promised destiny of racial genocide.

England, with Churchill at the head, stood alone. Prominent members of the British government in 1940 called for making the best peace compromise possible with Hitler. Hitler himself assumed Britain would ask for a peace settlement, so he could focus on conquering his next goal, Russia.

Churchill never wavered.

On June 4th, 1940, having lost ally France in a matter of weeks, and having barely escaped with the tattered remains of the British Expeditionary Force from Dunkirk, Churchill never considered capitulation to the Nazis. He relayed the defeat to the House of Commons, but said:

“We shall go on to the end, we shall fight in France, we shall fight on the seas and oceans, we shall fight with growing confidence and growing strength in the air, we shall defend our island, whatever the cost may be, we shall fight on the beaches, we shall fight on the landing grounds, we shall fight in the fields and in the streets, we shall never surrender.”

Never Sell

Bucked up by that example of Churchill’s spirit, let me re-summarize my approach to stocks: “Never Sell.”

“Never, never, never, sell.”

Can I be any clearer?

But, but, but

But interest rates are going up!

But the Democrats (or Republicans, or Trumpians or whomever) might win and everything’s going to collapse!

But oil prices!

But ISIS!

Stop being a five-year-old. Be Churchill.

Incidentally, at times, she unveils her stubborn Churchillian resolve to never give in, like when I ask her to put on her shoes when we’re already late to get somewhere.

Can you picture me, scaring the living daylights out of my five year-old with this Churchillian bedtime story about never never never never selling? Don’t worry, I didn’t do that. (As far as you know.)

I can assure you of this: She will not be selling her Disney stock.

In a recent post I mentioned that business owners may – among other benefits of entrepreneurship – achieve some tax savings. This week, inspired by my words, you’ve decided to hang a shingle.

In a recent post I mentioned that business owners may – among other benefits of entrepreneurship – achieve some tax savings. This week, inspired by my words, you’ve decided to hang a shingle. Let’s pretend your friend or family member (hereafter known as “framily”) has money, understands you, and wants to help. Your framily1 doesn’t need to pull credit or make you wait for two years worth of business financials. Your framily lends you just the right amount of money, and she only asks for an affordable interest rate in return. Maybe best of all, when your small business succeeds wildly, by taking a loan you keep all the business ownership to yourself, so you can get rich without having to share that wealth with your framily. This is the very best sort of money for your small business.

Let’s pretend your friend or family member (hereafter known as “framily”) has money, understands you, and wants to help. Your framily1 doesn’t need to pull credit or make you wait for two years worth of business financials. Your framily lends you just the right amount of money, and she only asks for an affordable interest rate in return. Maybe best of all, when your small business succeeds wildly, by taking a loan you keep all the business ownership to yourself, so you can get rich without having to share that wealth with your framily. This is the very best sort of money for your small business. Well now, wait a minute, clearly the best way to raise money for your new small business is to approach your framily, and instead of getting a loan, you get a direct equity investment. You sell part ownership in your business. Your framily believes in you and is flexible and, unlike in the case of a loan – which requires fixed monthly and possibly unaffordable payments – you only need to share profits (eventually!) with your new co-owner(s). Clearly this is the very best way to raise money for your small business.

Well now, wait a minute, clearly the best way to raise money for your new small business is to approach your framily, and instead of getting a loan, you get a direct equity investment. You sell part ownership in your business. Your framily believes in you and is flexible and, unlike in the case of a loan – which requires fixed monthly and possibly unaffordable payments – you only need to share profits (eventually!) with your new co-owner(s). Clearly this is the very best way to raise money for your small business.