I’m a markets guy who believes in applying economic principles to situations requiring innovation and the allocation of scarce resources. Which probably explains why I think it’s so important to also point out the hard limits to markets. There are big downsides and limits to thinking like an economist. The COVID-19 vaccine development and rollout is case study for examining what free markets are specifically not useful for.

“Health care should be run more like a private business,” is one of the more misguided statements that well-meaning people like to make, up there alongside the equally misguided “schools should be run more like a private business.”

The miracle of this vaccine development and initial rollout in one year’s time can not be understated. This is an unprecedented scientific achievement. It should be understood not as a victory of market-based economics, but rather the opposite: the extraordinary application of central government planning. Sometimes, in the good old US of A, we forget this point.

The Trump administration made the correct call last Spring to directly fund six different private pharmaceutical companies to research, test, and manufacture vaccines. This initial $10 billion federal government investment – called “Warp Speed” – allocated in March 2020 was upped to $18 billion by October 2020. A seventh company, Pfizer, did not receive funds for research, but did receive a guaranteed order for 100 million doses. By guaranteeing demand for hundreds of millions of doses, the federal government induced pharmaceutical companies to essentially ignore market signals like risk, profit, and loss. The Warp Speed program understood that some unproven vaccine products might not work, and that hundreds of millions of manufactured doses could be wasted. And that was ok.

Markets are great for some things. But they would never have achieved this vaccine miracle in one year. Vaccine development driven by the private sector historically happens in the five to fifteen year time frame, but we obviously did not have that time. Pharma companies with an unproven product and uncertain demand would never have ramped up to manufacture enough doses by early 2021. The federal government – everybody’s favorite punching bag – made the correct choice to pay for it anyway, in the interest of speed.

That’s how vaccine research and manufacturing was not left to the free market of efficient supply and demand signals. Now, when it comes to getting shots in arms, again we see the limits of economic-thinking.

For the next few months of the vaccine rollout we face a classic economics problem: too much demand and not enough supply. To vaccinate 80 percent of the US population we need more than 250 million doses (or actually double that, as the Pfizer and Moderna vaccines each require two shots.) For now, however, we’re living the reality of severe shortages, crashing websites. Unavailable appointments and online signups that get filled within 6 minutes of opening. High anxiety.

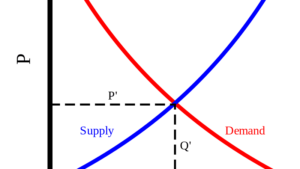

The usual supply and demand curve approach

The vaccine is free. But there’s not enough of it. Many of us expect to be waiting 3 or 6 months to get it. In the midst of severe scarcity, it feels like society is on a knife’s edge right now, looking for signs that some people are cutting the line. Who is using their money, or privilege, or network to get what other people need?

The “markets” solution to a situation like this – in a different context – would be to allow prices to determine who gets the scarce thing. That is clearly a moral monstrosity. In the coming weeks, the media will cover the issue of what celebrity, rich person, or government official cut the line to get the free, but scarce vaccine. But we all understand that a market-based solution to vaccine rollout – “who can pay the most right now?” or “who has power and influence?” – is morally abhorrent.

Looking forward a bit to a few months from now – hopefully in three months but possibly six months from now – we will have the opposite economics problem related to the vaccine. Too much supply and not enough demand. I’m referring to polls back in December in which only 42 percent of Texans indicated they would sign up to get a vaccine. Soon we will have plenty of vaccine supply. But if a large plurality of Texans and Americans decline to get it, we may be unable to achieve the 80 percent herd immunity that public health experts say is necessary to stop the pandemic entirely.

Bob Litan

How would an economist solve that problem? I asked economist Robert Litan from the Brookings Institution, who has argued for substantial payments to induce vaccinations to get us more quickly to herd immunity. He says we should pay people a lot.

“I think if you tell people $1,000, and then especially for a family of four, that’s $4,000, you’re talking real money. And I think at $1,000 you could get [anti-vaccine] people to switch,” he told me. He even had a clever finance-based incentive to encourage speedy vaccinations within society. Litan proposed that all citizens would be given an amount like $200 up front, with a promise of the $800 remainder when the United States as a whole achieved 80 percent vaccination.

Karl and Adam

As Litan explained, “So what that does is it gives tremendous incentives to tell your friends, whether in real life or on social media, to go out and get the shot, because then we can all get the money.”

For my part, I loved his idea. It would get herd immunity results fast. It uses “market incentives” as a carrot to induce desired behavior. The $300 billion or so it would cost would be a lot cheaper than the massive and complicated federal bailouts we’ve already resorted to.

Medical ethicists, however, hate this idea. Although small payments would be appropriate for convenience’s sake – such as transportation or a small snack – large payments on the order of magnitude suggested by Litan would be considered coercive. It is apparently not ok to force people to choose between putting something in their body – however safety tested we believe the vaccines to be at this point – and a large payment like $1,000. So we have important ethical limits to applying an economic or markets perspective to the conundrum of vaccine rollout.

In sum, when it comes to our health, economic efficiency is not the right watchword. Fairness and health outcomes are better guides. Enjoy your Socialism, everybody.

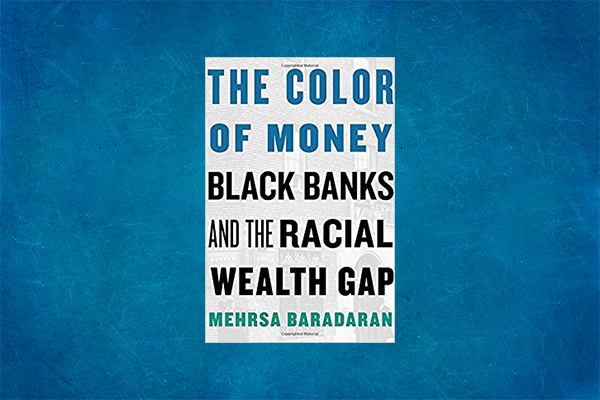

In a narrow sense Baradaran’s book is about the history of black-owned and black-customer-oriented banks. It’s a history without a lot of happy success stories. The story of the Freedman’s Bank, established in 1865 with Lincoln’s signature and a Congressional mandate to help build assets among the newly freed slaves in the South, ends in catastrophe when the (white) managers engage in a combination of speculation and fraud. Decades before the establishment of the FDIC, the bank failure caused direct financial losses to its black customers and a total loss of trust in the traditional banking system.

Of that experience, W.E.B. Dubois would say

“Not even ten additional years of slavery could have done so much to throttle the thrift of the freedmen as the mismanagement and bankruptcy of the series of savings banks chartered by the Nation for their special aid.”

Black Capitalism

In a broader sense, Baradaran’s story is a lesson in the complicated story of “black capitalism” and the 150-year debate within and without the African-American community about separatism versus integration for gaining political and economic power with respect to the majority culture. Beginning just after Emancipation and until the present day, leaders of the black community have urged strength through channeling the “black dollar,” whether through patronizing black-owned businesses or depositing money in black-owned banks. The success or failure of this approach can’t be determined definitely, although Baradaran provides numerous examples of the start-and-stop nature of the efforts. There aren’t a lot of consistent examples where it has worked well.

In fact, a central thesis of Baradaran’s book is that black banks not only cannot thrive outside of the majority culture – collecting black deposits and funneling capital back into the white system – but that they remain inherently weakened by the separation. Serving a depositor community with higher rates of poverty, while lending to a community with depressed housing values, has been a recipe for undercapitalized, unprofitable banks, at least historically. As she documents, the market forces that might outweigh these weaknesses – such as charging higher rates of interest on loans or offering lower rates on deposits haven’t worked either, and they open up the banks to charges of predatory practices.

The black banks might be the victims of (or left weaker by) the larger system, but are often perceived as part of a power structure that’s “disloyal” to the black community. And that’s when they do normal things that banks do.

One of the most interesting sections is Baradaran’s focus on the uses that the Nixon administration – and the federal government before and after Nixon – makes of the idea of “black capitalism.” In Baradaran’s telling, and there’s plenty of evidence in the book of this, Nixon sought to co-opt, blunt, or redirect Black Power through programs that seemed to celebrate and support “Black Capitalism.” But “Black Capitalism” programs historically function as a decoy for the black community and an appeal to the white community, rather than representing something fundamental or substantive.

The “capitalism is the answer” approach of Nixon was then recreated and expanded by Clinton and Obama, and Baradaran remains deeply skeptical of their efficacy as well.

The Southern Strategy

On the even more cynical side of political strategies, Baradaran directs the reader to an (in)famous interview by Republican strategist Lee Atwater, in 1982, about the “Southern Strategy.” I hadn’t heard of the interview before, and happened to locate it on Youtube recently, on the same day as the Senate vote on tax reform. I feel like this is an interview everybody should know about, in which Atwater sort of gives away the whole game, saying:

There’s a part of all contemporary politics wrapped in a nutshell in this recording, so I’m sort of shocked I’d never been directed to this before. But…that’s why we read a history like Baradaran’s about a subject on which we know very little. You should listen to Atwater in the YouTube clip but here’s the gist:

“You start out in 1954 saying Nig–, Nig–, Nig–. By 1968 you can’t say Nig__, that hurts you, backfires. So you say stuff like, uh, forced busing, states’ rights, and all that stuff, and you’re getting so abstract. Now, you’re talking about cutting taxes, and all these things you’re talking about are totally economic things and a byproduct of them is, blacks get hurt more than whites.”

The overlap of listening to Atwater, and the “Tax Reform” rush by the Senate in November 2017 suggested to me that little has changed since 1982.

Capitalism itself

In the broadest sense, The Color of Money spoke to me as a fundamental critique of capitalism itself, via a funny coincidence in my own life. I happened to be reading the book while a teacher friend invited me to lecture to high school senior AP students on a passage from Adam Smith’s The Wealth of Nations. Of course I felt the need to explain to the students the foundational nature of the text – Smith basically kicked off the invention of Classical Economics.

And yet, reading the passage in the light of the history of black capitalism, Smith’s words sound absurd.

In Chapter 10 of The Wealth of Nations, titled “Of Wages and Profit in the Different Employments of Labor and Stock,” Smith writes:

“The whole of the advantages and disadvantages of the different employments of labour and stock must, in the same neighborhood, be either perfectly equal or continually tending to equality….”

Ok, so here we have a classical economics trope on equilibrium between capital and labor, which has certainly not yet come true. BUT! Smith brings in his conditions, in the next paragraph, for how equilibrium and equality will occur:

“This at least would be the case in a society where things were left to follow their natural course, where there was perfect liberty, and where every man was perfectly free both to chuse what occupation he thought proper, and to change it as often as he though proper.”

Ok, so this passage was published in 1776 – a time of an active slave trade and even slave-like working conditions in Smith’s home country of Scotland.

The “perfect liberty” he describes was not true then, and it hasn’t been true yet in the last 150 years. So as I was teaching this passage to the high schoolers, and thinking over Baradaran’s book, the absurdity of classical economics based on this “perfect liberty” just seemed a perfect/imperfect point/counterpoint.

I’m a capitalist, and I’m not willing to give up on the system yet. But Baradaran’s book is just one reminder of the absurdity of some of Adam Smith’s foundational statements about capitalism. There’s nothing inevitable about equality or equilibrium at all. Smith passage just seems absurd. The market actually requires laws and justice and redress, in order to let the market do its thing, effectively.

One of Piketty’s main goals is to understand the conditions under which concentrated wealth can emerge, persist, vanish, and perhaps reappear.

Piketty’s unique offering, I think, it that he (along with colleagues) built the most complete, historical, transnational data-set on wealth distribution. Specifically, he allows us to compare three centuries of wealth data in France and the UK. He also built the most complete data sets on wealth in Germany, Italy, Scandinavian countries, Japan, and the United States.

Through that longitudinal data we get to see what has changed over the centuries, and where we stand today, compared to the past. We also get to see how the United States stacks up against other wealthy countries.

I’m late to the party in reviewing Piketty’s book – published in 2014 – but I think it doesn’t matter. He’s got centuries of data behind him and the book has a long shelf-life ahead of it.

All inequality discussions are political

Even engaging in a discussion about inequality involves political and normative choices. What we choose to measure, for example, has a great effect on what conclusions we draw.

Readers of Piketty’s work, naturally, come armed to the fight with political agendas. I know I do, and you do too. I happen to think inequality is a defining problem of our time. Others may not agree. ‘How much does inequality matter’ is a deeply political question in and of itself.

Piketty offers a great example of this, when he cites governmental measures of inequality. Traditionally, OECD governments present the ratio between the 90th (top) percentile of income and the 10th (bottom) percentile of income as a proxy for income inequality. Problematically, Piketty points out, this so-called P90/P10 ratio completely ignores the vast concentration of wealth within the top 1% of many countries. The bottom 9% portion of the top 10% in the United States, for example, look like pikers compared to the top 1%, a fact that the P90/P10 ratio tends to hide.

Additionally, the ratio will not indicate what portion of national income the top 10% earns, whether it’s 20% as in the case of Scandinavian Europe in the 1980s, 50% as in the case of the contemporary United States, or 90% in the Belle Epoque era of Britain and France preceding World War I. By choosing to present the P90/P10 ratio, governments choose the ‘chaste veil of official publications,’ a set of data that obscures as much as it enlightens.

War as Equalizer

The devastating wars of the 20th Century destroyed so much concentrated wealth in Britain and France (in addition to Germany and Japan, obviously) that they literally upended the social order. Piketty’s data shows how wealth concentration with the Top 10% and 1% in these countries plummeted in the first half of the 20th Century.

Wealth inequality stayed relatively tame in the decades following World War II, before ticking upward in the 1980s and beyond. An easy explanation for renewed wealth concentration may be changing tax rates, especially following the Reagan & Thatcher revolutions in the Anglo American countries.

Austen & Trollope & an Economist’s style

I have long looked to Jane Austen and Anthony Trollope as sources of information on the meaning and use of wealth, so I was pleased to see Piketty do the same.[2]

Jane Austen

Outside of these 19th Century literary references, Piketty does not rely on metaphors, popular writing, or anecdote. He’s an economist, primarily focused on his data and formulas to explain wealth creation. Like a serious economist, he takes great pains to explain his data collection methods and to circumscribe his conclusions. This makes for drier writing, but high credibility.

The Piketty thesis, in a thumbnail sketch

Piketty has a math-based worldview on how wealth becomes concentrated, and how it may inevitably lead to inequality in the future. I’ll attempt to concisely describe it here, so that you may mention it casually and sophisticatedly at your next cocktail party to impress your friends. You are welcome.

In the first section of the book, he builds the case that the proportion of national income that goes to ‘labor’ (what people get paid to do in exchange for the application of their time and talents) versus what goes to ‘capital’ (financial returns that accrue to an accumulated stock of wealth) is a key set of numbers to study in a national economy.

A key number for measuring this is what he calls the national “capital/income ratio” – which measures the stock of accumulated wealth of a country compared to the flow of total national income in any given year.

Typically we might see that the national wealth in a developed country is five or six times greater than the country’s income.

This ratio allows Piketty to measure – over time and across countries – the amount of money that ‘capital’ earns each year versus what ‘labor’ earns each year.

A household analogy for the capital/income ratio

To break that down into household terms and in numbers that our brains can handle, we might say that the capital income ratio of my household could be five if, for example, I boasted of a personal net worth of $500,000 and an annual income of $100,000. I mention the household analogy to illustrate the capital/income ratio as just a way of comparing the fixed accumulated store of wealth with a flow of annual income. Piketty focuses on measuring this number for countries over time, counting the entire national ‘store of wealth’ and the entire national ‘income.’

Second number: % annual return on capital

The reason why the national capital/income ratio matters is that it allows Piketty, and us, to see how much of national income is earned by ‘labor’ versus how much is earned by ‘capital.’ To do this, we need to know what the overall annual ‘rate of return’ on capital is in any national economy. This rate of return is just like how it sounds: If I invest $100,000 for example, do I make 2% on my money, or 6%, or 15%? An individual’s return on investment will depend on the particular investment of course – a bank CD vs. a bond vs. a stock vs. a rental property vs. an angel investment in a startup – to cite a few well-known possible investments. That aggregate national ‘return on investment’ will be the average of all these investments across millions of households and firms.

We might find, and Piketty does, that the average national return on capital often fluctuates in the 4 to 5% range over time.

Certainly Austen and Trollope generally assumed a 5% return on capital. A gentleman landowner who could count on 5,000 pounds per year in income might have been able to value his holdings – although voluntary land-sales were all but forbidden back then – at around 100,000 pounds.

Putting them together – income from capital

A fundamental math formula underpinning Piketty’s book is that the capital income ratio, multiplied by the return on capital, tells us what the overall proportion of income derived from capital is in a national economy. Money either comes from working (labor) or from investing (capital) and it helps us to be able to calculate what portion comes from capital.

Piketty, and we, care about this because it’s the beginning for understanding how wealth grows on wealth and how, possibly, an increasing rate of wealth inequality may in certain circumstances acquire a sort of mathematical inevitability.[3]

To return to a household analogy for a moment – which may help explain what Piketty measures at the national level – we could say again that I have a capital/income ratio of five. That’s based on my presumed $500,000 household net worth and $100,000 annual income (and $500K/$100K is five).

We could then assume that my return on capital (picture my $500K invested in ‘capital stock’ although in reality it might be entirely tied up in my house, but whatever) as 5%. When we multiply 5 fives 5% we get 25%, which represents the ‘annual income derived from capital’ of my household for example.

That annual income derived from capital – at the national level – is what Piketty takes great pains to build historical data around, and to track through time and across countries. We can see from the first math formula that the capital/income ratio determines to a great extent how much of national income will go to holders of capital (in simpler terms, holders of wealth. In simplest terms, how much goes to capitalists rather than workers.)

Piketty tracks the decline in ‘annual income derived from capital’ from the early Twentieth century through World Wars One and Two, but then the steady increase in the annual income derived from capital since the 1950s, as a way to understand changes throughout the last century.

A second math formula

Upon this foundation, Piketty introduces a second math formula. The capital/income ratio will tend to converge toward, over the long run, the ratio of the national savings rate divided by the growth rate of the economy.

A country with a high savings rate will tend, over time, to have a higher capital/income ratio. A country with a low growth rate (because the growth-rate number is in the denominator of the formula) will tend to also have a high capital/income ratio. Both of these situations we might expect will tend to exasperate inequality, as more of a nation’s wealth goes to capital, rather than labor.

By contrast, we would expect high growth rates in the economy over time to lower the capital/income ratio, and over time to lower the percent of income that goes to capital, rather than labor. That might correlate over time with lower inequality.

In either case, small changes in the economic growth rate can have great effects on the capital/income ratio over the long run. This second formula’s predictive capacity, Piketty clarifies, only works over the long run, possibly over decades. Nevertheless, he argues that its effects are constant and unavoidable.

Viewing the future

From a predictive perspective, Piketty would point to the savings rate, the economic growth rate, and the return on capital as the key measures of whether inequality will tend to increase or decrease in a national economy over time. Lower savings rates should lead to higher equality of wealth. Lower returns on capital should also leader to higher equality. But perhaps the biggest determinant of future equality is the growth rate of the economy.

And to simplify 600 pages of complex economic thought: Looking forward the slower secular growth in the economy of developed countries may inevitably doom these economies to increasing rates of wealth inequality.

A further summary of his data: The United States and Britain and France continue to move in a trend – begun in earnest in the 1980s – toward wealth concentration that will resemble the Belle Epoque of 19th Century Britain and France.

When we see the trends, it’s not hard to become alarmed about increasing concentration of wealth forming a sort of permanent aristocracy over our nominal democracies. Piketty urges us to note the data, note the trends, and try to understand the dangers to capitalism and democracy in the long run.

Policy Recommendations

Merely studying inequality is a political and moral choice, but making policy recommendations is obviously even more so. Here is where Piketty’s critics have mostly directed their fire.

Although I love his data and analysis, I am less certain that I will adopt Piketty’s prescriptive worldview on policies.

Piketty favors a progressive annual tax on large fortunes, as a way to combat the inevitability of wealth concentration. To the extent that would involve an estate tax, I am on board. The annual tax on wealth is obviously a further step altogether, since it would occur once a year. I can easily imagine the steps wealthy households would immediately take to avoid this tax, but Piketty nevertheless makes the case.

He also proposes a kind of global tax on capital, which as Piketty readily admits, is hard to imagine becoming a reality right now, both mechanically and politically. Banking coordination and reporting would be a crucial first step. This seems a long way off.

Piketty also favors an increased marginal income tax rate – possibly as high as 80% – on the highest earners in the United States. Although tax revenue from such a high rate on a small number of earners would be minimal, Piketty makes the case that the step would go some way toward reducing the concentration of income-capture by a small cohort of super managers, probably by voluntary compensation policy changes by large firms.

In each of these tax proposals Piketty seeks not to generate much revenue or replace existing tax regimes, but rather to regulate capitalism itself. If capitalism tends toward oligarchic concentrations of wealth – as the first ¾ of the book argues – his goal is to preserve the good of capitalism (efficient allocation of resources, high productivity gains) while mitigating the effects of the bad.

Capital isn’t the last word on these issues, but a key starting point for a discussion on the state of things.

Please see related posts:

[1] My summary of Kennedy: First, great powers become great based on their economic strengths. Second, great powers subsequently take on imperial obligations, which require increasingly larger military expenditures. Third, great powers sink under the cost of their military obligations. Like clockwork! And it doesn’t bode well for the current hegemon, with a military budget bigger than the next seven biggest militaries, combined.

[2] He also references the novels of Honore de Balzac, who I have not yet read. But I will someday.

[3] Unless counteracted by policies – like taxes – or exogenous events – like wars. Describing these counterbalancing forces take up a significant portion of the book.

Looking for a last minute book to purchase this holiday season for the bright business or economics student in your life? Perhaps the student in your life appreciates mixing economic theory with murder, as in The Mystery of the Invisible Hand by Marshall Jevons.

Marshall Jevons is the pseudonym of economics professors Kenneth Elzinga of the University of Virginia and the late Trinity University economics professor William Breit.

Professor Breit was a beloved figure on campus at Trinity in San Antonio, TX before he passed away in 2011, remaining connected to students and his department in the years following his retirement.

Elzinga and Breit created the fictional murder-solving Harvard economist Henry Spearman.

Spearman – who wins the Nobel Prize in Economics at the start of this novel – applies economics principles to solve murders. Think Hercule Poirot meets Milton Friedman.

Trinity University in San Antonio, TX

In The Mystery of the Invisible Hand – the fourth in a series of Spearman mysteries, the economist-detective arrives as a visiting professor at Monte Vista University in San Antonio, TX – a transparent portrayal of San Antonio’s Trinity University.

Each chapter begins with a passage or quip from a famous economist.

Inside jokes of the economics profession abound – like naming a character Bruce Goolsby, a thinly disguised reference to Austan Goolsbee, Chairman of the Council of Economic Advisors under President Obama.

The humor of Breit and Elzinga shines through in their light satire of academic politics and foibles.

We meet the hard-charging Trustee Annelle Cubbage – heir to a Texas ranching fortune – who wants the best that money can buy. Cubbage wants what she wants, when she wants it. Cubbage creates the “Cubbage Visiting Nobel Professorship” that brings the Nobel Laureate Spearman to Monte Vista University.

The anxious scholar Jennifer Kim – untenured – hesitates awestruck in the face of Spearman’s awesome reputation.

Meanwhile, the art professor Michael Cavanaugh resents the high pay of his economist colleagues at Monte Vista. By his view, they lack appreciation of art for art’s sake.

Visiting artist-in-residence and painting genius Tristan Wheeler cuts a romantic swath through the hearts of Monte Vista scholars – including some professors’ wives – before his mysterious death.

Spearman observes – like a careful anthropologist of the academic world – how the seating arrangement at the Monte Vista University President’s dinner establishes the relative ranking of dinner invitees.

Elzinga and Breit clearly met all of these characters on their real life campuses during their academic careers.

San Antonio readers will appreciate the economic explanation of the cost of the Spurs’ stadium, as well as financial theories on the funding of the fictional “Travis Museum,” modeled after the SAMA.

Spearman solves the murder through an epiphany in the midst of an economics lecture at Monte Vista University, applying economic analysis to intuit the motive of the killer.

Those of you who – like me – prefer your financial and economic theories presented with a spoonful of sugar to help the medicine go down, will enjoy this murder mystery set in the Montevista neighborhood of San Antonio.