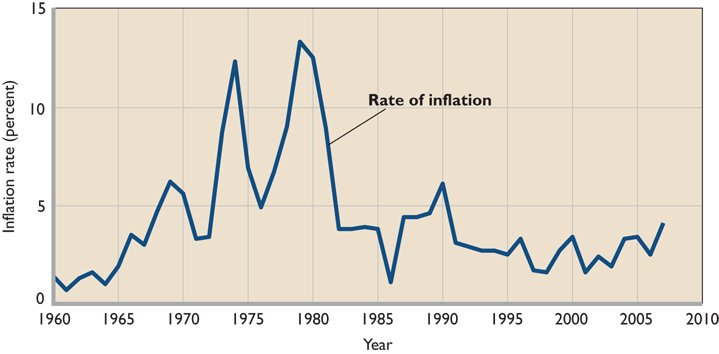

“Given the staggering debt of the United States and Congress’ seemingly laissez-faire attitude and impotence towards addressing it, I am starting to be concerned about the value of U.S. currency. Historically, wars and corrupt governments have led to hyperinflation in other countries where the costs of goods and services skyrocket. The likelihood of this happening in the U.S. may seem remote but it is not impossible. Are there ways for individuals to protect themselves from this?” — Dom D. From San Antonio

I really like this question. Dom recognizes our unprecedented current debt situation and the unfortunate parallels with other countries where hyperinflation followed. I have no idea what’s going to happen.

If it’s comforting, hyperinflation would require a failure by the Federal Reserve to do its job. The Fed withstood the last few years better than most institutions. But, yeah, increased inflation seems increasingly likely for the reasons Dom named. So what to do?

The Fed has to fail for hyperinflation to happen

Something to remember about inflation is that if the underlying economy is unchanged but the amount of available currency doubles, it is reasonable to assume that the price of things approximately doubles. This is bad when we have to pay for things. It is not necessarily bad if the price doubles of things that we already own. Things that you could own, which should double in price if the supply of money doubles, include real estate and stocks. As a result, these make for very good inflation hedges.

So the first great way to hedge against inflation is to own a business, or preferably many businesses. Some insist on the hard way to do this.1 I would like to focus everyone’s attention on the lazy way – my preferred way – which is to own hundreds or even thousands of businesses through a single low-cost diversified stock mutual fund. In an inflationary environment, successful businesses raise prices in response to their higher costs. Successful businesses adjust dynamically to earn profits despite inflation.

Similarly it is reasonable to expect – all else being equal – that a stock worth $100 today will be worth $200 tomorrow, if the amount of currency doubles overnight. One explanation for the record rise of the stock market in the last few months – the one I find most plausible – is that the Fed has dramatically increased the supply of currency in the economy. The record stock market rise is probably a specific form of inflation hitting one very visible corner of the overall economy.

The second great hedge against inflation is to own real estate in advance of inflation. For starters, try to own your home. And then live in it for a long time. The price of your home should appreciate roughly at the rate of inflation. That’s the definition of a good hedge. Let’s say, for example, you own a home today worth $250,000. And then we suffer a patch of 10% annual inflation for ten years. Your house at the end of 10 years will be worth a little over 648 thousand dollars. Compound interest math uses the same formula as inflation math.

Homeownership is good

Now, here’s an even more interesting twist on inflation hedging via home ownership. The triple lindy inflation hedge, if you will. Are you ready for it?

Do you have a long-term fixed-rate (let’s say, 30-year) mortgage on your house?

Ta da! You did it. You are amazing. Have you ever thought about being a hedge fund manager?

Here’s why this is an amazing inflation-hedging tool. Using the previous example, as your home value leaps upward over 10 years of 10% annual inflation from $250K to $648K, your 30-year fixed rate mortgage decreases dramatically, both in nominal and real terms. Using a standard 30 year amortization schedule, your mortgage would pay down from $200K to $162K during the first ten years. At the end of ten years, a $162K amount of debt on a house worth $648K is actually pretty easy to handle. You moved from owning $50K in home equity to $486K in home equity, nearly a ten-times increase.

Also, just as money isn’t worth as much following inflation, debts are also not worth as much in an inflationary future, so $162K in debt is not as big a deal in that future as it would be today. In other words, being a borrower during an inflationary period is actually a powerful inflation hedge. (Provided, of course, your debt has a fixed rather than variable interest rate.)

By owning your home with a mortgage, you’re a fancy inflation hedger, and you didn’t even know it.

Next, what should you specifically not do if you anticipate future bouts of inflation?

Do not buy fixed income products for any investment purposes. Traditional fixed income investment products include bonds, bond funds, annuities, and CDs. Inflation absolutely wrecks the value of these fixed income investments. Even money market funds, savings accounts, and cash could be considered fixed income, just with an extremely short (same day) maturity date. If your net worth or income is in any of these fixed income products, inflation will unfortunately destroy your wealth.

Not an inflation hedge I endorse!

Next, do not buy gold as an inflation hedge. Gold is a pretty but useless metal sold by preying on the fears of unsophisticated financial minds. I understand you don’t believe me, because of all those plausible sales pitches on your video screens, but it’s true.

Also, do not buy bitcoin as an inflation hedge. Bitcoin is a fake currency, neither useful for buying beer nor paying taxes. It has no legal use case and produces no wealth, except for people hyping you to buy it, based on the greater fool theory of speculation.

In sum, own your own home, own some businesses either directly or through the stock market, and if you must borrow, then borrow at a fixed interest rate. Avoid the standard inflation-hedge scams.

Avoid Bitcoin

What I really like about the previous two sentences is that in anticipation of heavy inflation – and I can not emphasize this strongly enough – you should pursue the exact same investment actions I would advise to anyone who is not anticipating a future bout of heavy inflation.

Did you catch that? It’s important. Do exactly the same prudent things you should always do.

Finally, is Dom’s scenario likely to come to pass? I don’t know. Neither does anyone. Pundits who predict the economic future with certainty are fools or confidence men to be deeply distrusted.

I have personally (but silently) expected significant inflation since aggressive interest rate drops in September 2001. I’ve been wrong every time.

Although, maybe not. Come to think of it, my home value and my stock index funds have suffered quite a bit of inflation over the past twenty years. Haven’t yours?

Did you notice the weird stock market that emerged, Gorgon-like, from the Upside Down in December 2018?

We’re living this Stranger Things market because the Federal Reserve holds all the keys. The December 2018 panic – a 15 percent peak-to-trough drop in the S&P500 – scared all the adults so much that between January and July 2019 we’ve been living the chain reaction. When I say adults – in my analogy – I mean the Federal Reserve, which sets short-term interest rate policy.

The July 30-31stmeeting of the Federal Reserve this week may (or may not!) resolve this Upside Down world. By Upside Down I mean all traditional good news for the economy is bad for stocks, because interest rates might stay the same or go up, which could in turn tank the market. Bad news for the economy, on the other hand, is good, because the Fed could cut rates and therefore juice markets further.

Got it? It’s the Upside Down. Love is Hate, No is Yes, War is Peace. I’ll come back to that upcoming Federal Reserve meeting, but first…

I have a weakness for counter-intuitive truths, contrarian wisdom, and oxymoronic statements, especially when it comes to money and markets. This week’s summer reading was Wall Street Journal reporter and economist Greg Ip’s 2015 book Foolproof: Why Safety Can Be Dangerous and How Danger Makes Us Safe

Of course I would fall for a book with the subtitle “Why Safety Can Be Dangerous, and How Danger Makes Us Safe.”

Ip’s main point is that when we act to reduce risks in one place today, we may create greater risks for tomorrow. Or we may unknowingly create risks for other people, in unexpected ways or places. When we seek perfect stability or the absence of volatility, we create unstable systems. Ip cites mid-twentieth century economist Hyman Minsky, who summarized this big idea as “stability is destabilizing.”

A few analogies Ip employs:

Suppressing natural forest fires on national park land may, ironically, create the conditions for uncontrollable wildfires in the future. Small controlled burns, by contrast, reduce the chance of big conflagrations.

The introduction of padded helmets in professional football may have increased the risk of both brain and bodily injury in players, because bigger and faster players tackle head first. Rugby players, by contrast, don’t suffer the same types of brain and spinal injuries because they don’t play with the same head-first recklessness that helmets encourage.

Our reaction to catastrophic-seeming risks like airline crashes and nuclear power plant meltdowns can increase risky behavior – like driving more, or shifting to other, long-term deadlier energy sources.

The Federal Reserve historically has attempted to lower the risk of big blowups by inducing smaller economic slowdowns, like setting a controlled burn to reduce the chance of a big out-of-control forest fire.

As an economist, Ip urges us to think about how seemingly risk-reducing behavior can, counter-intuitively, create greater risks in the future. The attempt to smooth over all dangers completely can make an entire whole system riskier, or create unanticipated risks later on.

To prevent this, in macroeconomic terms, the Federal Reserve often attempts to play a key role in setting a controlled fire, in order to prevent an uncontrolled wildfire. William McChesney Martin, former Federal Reserve Chairman (1951-1970) classically described this action as “take away the punch bowl just as the party gets going,” by raising rates when the economy gets too strong. This sounds good in theory, although it’s always controversial and based on guesswork when implemented in real life.

Incidentally – about that July 30-31stFederal Reserve meeting – markets clearly anticipate a rate cut. Which also strikes me as something coming from the Upside Down.

With risky asset prices (real estate, stock market indexes) at an all-time high and unemployment at a 50-year low, the traditional macroeconomic case for a Fed interest rate cut in July 2019 is – in a word – absent.

It’s difficult, but maybe necessary, to set small fires to prevent the big fires

In the past, we’d expect a rate hike, not a rate cut, under these booming economic conditions. The Fed would seek to set a controlled burn now, in order to prevent a massive forest fire later. Interest rate cuts, by contrast, were a rarely-used emergency tool for cushioning against recession, boosting confidence in the face of tight lending or adverse shocks to the economy. None of that is apparent now.

Under similar situations of asset price inflation and low unemployment – 1991, 2000, 2006 – the discussion was always about raising interest rates. By classic standards, a rate cut at the end of this month seems insane. But what the heck do I know? It’s just what markets currently expect in our Stranger Things economy.

The Personal Investments Application of This Idea

By the way, moving from macroeconomic theory to personal investments, I think the most important application of Ip’s thesis – although he never spells it out in his book – is in our personal asset allocation choices.

Specifically, should we choose “dangerous” assets like stocks, or “safe” assets like bonds and annuities? Because the perceived riskiness or safety of these assets seems clear in the short term, but counter-intuitively flips in the long term.

The truly dangerous investment– if we’re talking about a long-term project like living comfortably in retirement – comes from “safe” seeming assets like bonds and annuities. For middle-income folks, the true investment danger is that we will outlive our money, a danger that bonds and annuities tend to aggravate rather than alleviate.

Stocks, when given decades to grow, – and diversified, of course – tend to lower our personal risk of outliving our money. In order to be safe in retirement, we need to choose risky in our investments.

When it comes to Federal Reserve policy, we need to focus our worries about the correct thing. Hint: It’s not inflation. Also, it’s not recession. Also, It’s not the rate of interest rate hikes.

It’s the Fed’s independence. Even President Trump agrees with me. Although admittedly, for reasons diametrically opposed to my reasons.

After three interest rate hikes earlier in 2018, the Federal Reserve will raise short-term interest rates one more time this year. The Fed will likely rise another 1 percent over the next two years, according to their future guidance, and barring unexpected developments like war or recession.

The fact that Trump is unhappy is not particularly surprising. In fact, White House grumbling about the Federal Reserve is a common enough theme over the last eighty years. Not using Trump’s uniquely colorful language, mind you, but it’s still not wholly new.

History of Presidential Jawboning

Political leaders in power always want pro-growth policies. Low unemployment and high asset prices tend to make leaders look good. Presidents generally don’t want the Federal Reserve to – in Fed Chairman’s William McChesney Martin’s famous phrase “take away the punch bowl just as the party is getting started.” President Nixon reportedly blamed his 1960 loss to Kennedy as a result of Fed Chairman Martin’s tight monetary policy of high interest rates.

President Johnson complained as well, saying “Martin, my boys are dying in Vietnam, and you won’t print the money I need.”

President Nixon reportedly both put pressure on Martin’s successor at the Federal Reserve Arthur Burns to keep interest rates low and money flowing during his 1972 re-election, which he handily won. Paul Volcker, Fed Chairman during the 1980s, published a book in late October 2018 in which he claims President Reagan’s Chief of Staff James Baker told him in 1984: “The president is ordering you not to raise interest rates before the election.” Volcker adds to the story that the Federal Reserve at the time had no plan to raise interest rates.

George HW Bush was upset in the fall of 1992 that the Fed was raising interest rates, before he went on to lose his re-election to Bill Clinton.

President Clinton’s budget chief Leon Panetta and later Chief of Staff twice tried to preempt the Federal Reserve, saying at his 1993 confirmation hearing “we ought to have cooperation from the Federal Reserve,” meaning lower interest rates, and then in a 1995 interview “it would be nice to get whatever kind of cooperation we can get to get this economy going,” referring again to Federal Reserve policy. Despite the instincts of leaders in power, Federal Reserve observers think we have made a lot of progress since the bullying of President’s Johnson and Nixon.

Presidents George W. Bush and Barack Obama avoided appearing to try to influence interest rate policy. Inevitably, political leaders oppose higher interest rates because they reduce business borrowing, risk increasing unemployment, and knock down asset prices of real estate and stock markets. Political leaders want lower interest rates – it’s stimulative to the economy, and therefore helpful for their political prospects.

Volcker’s legacy

Since Paul Volcker famously raised interest rates early enough in the Reagan presidency to tame inflation in the early 1980s, the Fed has built a rock-solid reputation as independent from political influence. It is believed to manage the money supply without favor or political influence, giving investors worldwide confidence in the dollar.

OldSchoolCool: Paul Volcker

The key question then is whether Trump’s attacks on the Federal Reserve will have an effect. We need to hope they do not. Just as the greatest risk to Trump’s presidency is not the independence of the Fed, neither is the greatest risk to the US economy inflation or the rise in unemployment, the two typical concerns of the Federal Reserve.

Rather, the greatest risk to the US economy is that people the world over would come to believe that the US Federal Reserve is not acting independently of political pressure. A primary reason the dollar still remains the global reserve currency of choice is that global allocators of capital believe the Federal Reserve is not captive to the US political system.

In a clever take that emphasizes a silver lining in the storm clouds, the Wall Street Journal’s Spencer Jakab recently argued that Trump’s recent Fed bashing is actually a good thing, since it proves that the Fed is willing to do an unpopular thing for the right reasons. Since it continues to defy Trump’s wishes, we should be happy that the Federal Reserve is under attack. I mean, I guess? Like a Category Five hurricane slamming against the retaining wall protecting the coastal city is a good thing, because it didn’t break the wall this time, and that shows us how strong the retaining wall is right now. So, yay, hurricanes? I’m sorry, that logic is bass-ackwards.

The real risk

We can survive a recession. We would have a harder time surviving the loss of confidence that would follow if Trump could jawbone the Fed into keeping rates low, for political purposes.

We can survive a little inflation. A little inflation does not make us much closer to Venezuela. Rather, a political leader who can get what he or she wants with monetary policy does make us a lot more like Venezuela.

The Federal Reserve has raised short term interest rates three times already this year by one-quarter percent, and it seems poised to do so again in December, even though it left rates unchanged this week. Over the next two years, barring an unanticipated war or recession, the Federal Reserve will raise short-term rates by another percentage point.

We may have different reasons for benefiting from higher or lower interest rates, depending on whether we are primarily borrowers or savers, employers or employees, exporters or importers, young or old.

The effects of rate hikes on the economy are complex and incredibly important. But we probably think of interest rates and the Federal Reserve a bit like changes to the earth’s climate – massive forces shifting ominously, seemingly far beyond our individual control. We vaguely understand them to have huge implications. We’d like to know more, but how?

There are two big questions to understand today about the Federal Reserve and rising interest rates.

First, what is the relationship between inflation and interest rate hikes?

Second, what is the proper relationship between political leaders and the Federal Reserve?

I’ll talk about the inflation question here and leave the political question of the Federal Reserve for a later post.

From a multi-decade perspective, we’re moving from artificially low interest-rates – dating back to a period that started with the 9/11 attacks and were renewed by the 2008 financial crisis – to a more “normal range” interest rate environment.

In normal times, the Federal Reserve raises rates when it worries about inflation, and it lowers rates when it worries most about unemployment. The Fed’s not worried about unemployment – currently at a 49-year low. Instead, the Fed seeks to keep inflation in check. But because inflation apparently isn’t rampant, the Fed can take it’s time with gradual rate hikes.

One of the great economic mysteries of the last decade is the absence, or at least inconsistency, of observable inflation, despite the fact that the Federal Reserve pulled out all the stops to make lots of money available in the years following the 2008 financial crisis. Pretty much every observer, even supporters of the post-2008 crisis policy of easy-money-plus-low-interest-rates, predicted a significant uptick in inflation. That, seemingly, was the price we had to pay to kickstart the economy.

But then, it didn’t happen. Or it didn’t happen in the way we expected. From the beginning of 2010 through September 2018, the Consumer Price Index – a traditional measure of inflation – rose only 16.4 percent. Annual inflation averaged less than 1.7 percent in that period, which is totally non-threatening. Consumer inflation from 2010 to today is like the dog that didn’t bark in the night.

We can be a bit more sophisticated though in understanding different types inflation and what it means for different people in an economy.

Inflation types

We should be aware of least three different types of inflation.

There’s the traditional type of consumer price inflation we see, which shows up in the price of gasoline, the stuff we buy at WalMart, health care, tuition, and the cost of a pizza on a Friday night. I know you think you’re paying too much lately for this stuff, but compared to other decades consumer inflation has been pretty modest.

At least two other types of inflation matter as well, however, asset price inflation and wage inflation.

Asset price inflation shows up as the increase in the price of real estate and the stock market. We generally cheer this type of inflation as a healthy sign of economic growth, although it’s not a purely good thing, depending on who you are.

To pick one real estate measure for example, the St. Louis Federal Reserve House Price Index for Texas has risen by 49.8 percent since the beginning of 2010. In other words, even though consumer goods cost just 16 percent more, houses in Texas cost 50 percent more than they did in 2010. What about stocks? To pick another measure, the Russell 2000 Index of small capitalization stocks is up 150% since the beginning of 2010. The rise in stocks isn’t entirely inflation, as its partly due to retained profits and buybacks, but inflation is part of that 150% rise in stocks.

So, is asset inflation good or bad? It depends.

Where you stand depends on where you sit

If you’re a twenty-something or thirty-something trying to save for your first home purchase, and home prices rise by 5-10 percent each year over a decade, this type of inflation actually hurts your plans. Similarly, for a young person trying to accumulate a retirement account nest egg through stock investing, a rising stock market is actually quite a bad thing. A twenty or thirty-something saver and investor should fear asset price inflation because it makes their wealth-building plan much harder to enact.

Interest rates hikes have traditionally had a dampening effect on asset price inflation.

An employer, obviously, will experience wage inflation as a big problem, one that directly cuts into the cost of doing business and profits. A worker, by contrast, directly benefits from wage inflation.

I mention all these different types of inflation because interest rate hikes tend to dampen all three types – consumer, asset price, and wage inflation. Depending on who you are, higher interest rates will affect you in different ways, even though we typically only think of consumer inflation. Are you a worker or an employer? Are you an importer or an exporter? Are you young or old? Are you a borrower or a saver?

With observable consumer inflation so low, does it even make sense for the Federal Reserve to raise interest rates? President Donald Trump doesn’t think so. He has argued in recent weeks that the Fed is “loco,” and that “my biggest threat is the Fed,” and because “you don’t see that inflation coming back” that he disagrees with the Federal Reserve’s moves to hike interest rates.

Traditional bankers won’t like this blog post. But you know what? Many people don’t like their own banks, and many people aren’t being served well by our banking system. I’m intrigued by recent proposals to fix a gap in the deposit-taking function of banking, specifically a US Postal Bank on the one hand, and an even more disruptive idea of a Federal Reserve bank account – known as a FedAccount – available to individuals and businesses.

Postal Banking

Senator Kirsten Gillibrand (D-NY) introduced a bill in April to revive US Postal Service banking, something that we used to have. It began in 1910 under President William Howard Taft until it was ended by Lyndon Johnson in 1966, according to banking scholar and University of George law professor Mehrsa Baradaran, in her Ted Talk on postal banking.

In the Gillibrand proposal, the Post Office would offer free deposit accounts for amounts up to $20,000. For-profit banks tend to ignore small depositors as unprofitable, or they charge high checking account fees to make up for that unprofitability.

The Post Office already has branches everywhere, including in “banking deserts” that have been abandoned by community banks as unprofitable, and where check cashers and payday lenders have moved in. While the Post Office by charter must be financially self-sustaining, it has a history of subsidizing services for the public, as it does for example when it unprofitably delivers mail to remote rural areas.

In Gillibrand’s proposal, personal loans of $500 could also be offered. Her proposal came with an unreasonably low rate for this type of personal loan. But even at rates as high as 20 to 25 percent, it wouldn’t be hard to offer an interest rate that reflected the risk of these loans, while still undercutting payday lenders.

The people who would be most helped by postal banking are the estimated 10 million US households who are “unbanked.” Among the very poor, up to 10 percent of disposable income gets used for basic financial services, such as check-cashing and payday loans.

The FedAccount

But how about an even more intriguing and radical solution proposed last month, that would help not only the poor, but the wealthy and everyone in between from small businesses to you and me?

The proposal by three economists and former US Treasury officials is to offer a FedAccount – free checking accounts of any size at the Federal Reserve to individuals and business. The Federal Reserve currently only has deposit accounts for financial institutions.

In a fiat money system like ours, as you hopefully already know, money is a kind of collective fiction we all weirdly agree to. The beautiful thing about the Federal Reserve is that they are the dream weavers of this fiction. They invent money. An electronic ledger in a FedAccount with your money will always be there basically because the Federal Reserve says it’s there, and they perform magic.

When you can invent money there’s no problem whatsoever guaranteeing unlimited amounts of money both to the under-banked poor and the extremely wealthy. A $100 deposit by a poor person will always be there. A 100 million deposit by a wealthy person will always be there. 100 percent guaranteed.

The FedAccount could also handle merchant processing for free between FedAccounts, something that businesses currently pay extraordinary amounts of money to credit card and debit card companies to do. Small businesses in particular, with little negotiating power against credit card companies, could reap huge savings on processing fees. Eliminating those fees would ultimately lower costs for consumers. Also, a business using its FedAccount should be able to receive payment on the same day, which could be a life-saver to cash-strapped businesses.

Is a FedAccount a threat to traditional banking as currently provided by a combination of megabanks and smaller private community banks? I don’t think so. If the Fed Account stayed out of the lending business it should not threaten legacy banks.

What about costs to create the program? The Federal Reserve already keeps deposit accounts for all banks, so adding that capability for individuals and businesses would be simply a matter of straight-forward software programming.

How could this all be free? The Federal Reserve earns profits on financial assets it owns, and sent $98 billion, $92 billion and $80 billion in excess profits to the US Treasury in 2015, 2016, and 2017.

Would it need an army of customer-service employees? Doubtful.

With an easy phone app I know it could attract most of my deposits. I don’t need to talk to banking employees about my account. When was the last time you had an important and helpful conversation with a bank employee regarding your checking account? I’m guessing for most of us, approximately, never?

I can anticipate a libertarian aversion to these expanded government-as-banker roles. Would government banking be competent? Would it protect privacy? As the proposers of FedAccount argue, the Treasury processes billions of payments per year, and disburses millions of Social Security checks per month, basically without a problem.

The Federal Reserve handles $3 trillion worth of Fedwire payments per day. They’re good at this stuff. Unlike the private banking sector, which has to be regulated and subsidized to keep it from periodically failing, the Federal Reserve doesn’t need a subsidy and implied public bailout. Remember, it can create money virtually whenever it needs to. It’s magic.

On the issue of privacy and government intrusion, the FedAccount would be an option, not a requirement. People who fear government intrusion could continue to only patronize private banks.

Look, I wouldn’t bet a single dollar of mine that the low-cost, needed, solution of FedAccounts will happen in our lifetime. We’re talking about something that would make every for-profit banker in the country nervous. And nervous bankers make for a powerful lobby. But I’d be up for it.

The US Postal Bank as proposed by Gillibrand is more modest in scope and has a successful historical precedent. That one’s not impossible in the medium term, and it’s also worth trying.

This is a long post about how Trump has specifically threatened to cause an economic or financial crises through either a trade war or through undermining the US monetary system and credit.

Similar to a security crisis, I can’t sleep because I worry Trump may inadvertently cause an economic crisis, which he may then uses as a pretext for further authoritarian moves.

Look, this can’t be a prediction about “what’s going to happen” with the economy under Trump. Most of the time when we talk about markets responding to a presidency, we are finding false signals in noise or we’re predicting things that are really unknowable.

I do worry, however, about two specific economic problems that Trump has promised to cause: Trade wars, and interference with US financial strength through the bond markets and Federal Reserve. The long-term problem with an economic crisis – besides the obvious pain and suffering – is a societal desperation that allows an authoritarian to make bold moves otherwise unavailable to him.

Let’s start with trade.

In the arena of international trade, Trump’s “plans” – such as they are – could and would cause a worldwide trade-war and global recession. He launched his presidential campaign pledging massive 35% tariffs on our major trading partner Mexico. He reiterated his plans many times on the campaign trail to retaliate both against Mexico, and against companies like Ford Motor that may move manufacturing jobs to Mexico. By the way, 16% of our national exports go to Mexico.

Trump pledged to withdraw not only from the recently-negotiated Trans-Pacific Partnership but also to renegotiate or withdraw from 1994’s North American Free Trade Agreement with major trading partners Canada and Mexico. By the way, 19% percent of all U.S. exports go to Canada.

Trump’s promises mark a very big shift in US policy and leadership.

The problem with unilateral trade sanctions like this is:

They don’t stay unilateral. Countries affected will obviously retaliate against us with their own trade sanctions, and;

The United States would probably be in violation of international trade systems like the WTO.

The globalization of trade since the end of World War II – and in particular since the end of the Cold War – has greatly favored the United States, even if the effects of trade hurt particular industries or geographies. A reversal of that trade situation – championed by Trump as he champions those most hurt by globalization – will make us all poorer.

At the same time, high tariffs are unlikely to bring back manufacturing jobs. The bad news[1] is that we pay people too much in this country and we enforce too many worker protections to make many manufacturing jobs viable here.

Trump has promised a trade war, but without a chance that it could possibly “work” in the sense of bringing back many jobs for those most affected by globalization.

Now, maybe Trump is just kidding about his trade war plans. Maybe its just a goof, indicating his direction of thought, but he won’t enact anything as crazy as what he’s promised?

Commerce Secretary Wilbur Ross

His selection of billionaire investor Wilbur Ross for Commerce Secretary, however, indicates Trump’s seriousness about protective tariffs. Ross made his career as an extraordinarily successful vulture investor in beaten-down industries such as steel and coal, domestic industries buffeted in part by regulations and high worker-costs, but also by international trade.

In 2002 and 2003, Ross bought up bankrupt steel-producers LTV Corporation, Acme Metals and Bethlehem Steel.

A well-timed 30% tariff on imported steel in 2002 enacted during the George W. Bush Administration helped raise the value of Ross’ steel holdings, which he eventually sold to Indian-owned Mittal Corp in 2005.

Incoming Commerce Secretary Wilbur Ross likes steel tariffs

Ross has indicated his support for both Trump and the idea of protective tariffs, and he clearly has the business experience to know that trade protection can enrich the owners of certain industries.

While higher steel prices help steel workers and owners, however, they hurt other industrial companies – like the auto or construction industries – that need to buy steel at the lowest price possible.

Trade wars can benefit some select sectors and people even while most of us end up poorer through higher costs. International trade has been a major generator of wealth since the end of World War II, with the United States as its biggest cheerleader. I’m afraid Trump intends to kill the golden goose, with severe economic consequences.

Undermining financial strength

The second economic crisis threatened by Trump is his promise to weaken the Federal Reserve. It will take some wise financial counseling to explain to Trump why his threats do not really help the United States. He has not shown evidence, however, that he can take that kind of advice, or learn from it.

I worry that over the next two years Trump will have the ability to reshape the Federal Reserve in ways that undermine one of the central bank’s key strengths – its independence from politics.

Janet Yellen, Chair of Federal Reserve

The Fed is the quasi-public, semi-mysterious, massively-powerful, independent central bank for the United States. It’s an “independent” regulator, meaning it technically doesn’t report to Congress or the U.S. president. Given its mystery and importance, critics on the Left and Right often seek to curb the power of the Fed. Anything that powerful must be part of some kind of conspiracy, right?

President-Elect Trump — who served as human fly-paper for the bad economic ideas of fringy cranks throughout his campaign — caught this wave too. He accused the Fed of being in the tank for the Obama administration. Like the Republican Party, the Democratic Party, the FBI, the Electoral College, and the media to name a few — the Fed — Trump complained, was part of an unfair conspiracy against him.

But then Trump went further down an even darker path in attacking the Fed. In “Donald Trump’s Argument For America,” released in the days before the election, he linked images of Fed Chair Janet Yellen to the well-known faces of financiers George Soros and Goldman Sachs CEO Lloyd Blankfein, as part of a “global elite” conspiring against ordinary Americans. All three are Jewish, of course, and the ad recalled anti-Semitic conspiracy theories that follow the vile and fictional “Protocols of the Elders of Zion.” Whether Trump claims that Yellen is in the tank for his opponents, or whether he winks knowingly at anti-Semites about a global Jewish conspiracy, he has set the stage to justify curbing the Fed’s independence.

This video:

This should trouble us tremendously. The U.S. is a country that — despite the confounding popularity of the Kardashians — retains an outsized role in the global economy. One of America’s greatest strengths as a financial power is the belief that its central bank is not unduly subject to political control from any particular party or faction.

Usually when we talk about policies from the Fed, we don’t focus on Democrats and Republicans or Liberals and Conservatives, but rather “Hawks” and “Doves.”

In simplest terms, a “hawk” tends to worry about inflation more than unemployment, and pushes the board to raise interest rates quickly enough to avoid unexpected inflation. A “dove,” conversely, worries more about unemployment than inflation, and would tend to want to keep interest rates low as long as possible, to juice economic activity even if it spurs a little bit of inflation. I’m simplifying here, but these are the broad strokes.

A key point, though, is that a Fed governor — whether hawk or dove — is supposed act independently from politics. Almost as important is the idea that a Fed governor seems to act independently from politics. We count on the appearance of independence as much as the reality.

The first guarantee of independence is that the seven board members, known as governors, serve 14-year terms, thus guaranteed to outlast any U.S. President. A bit like justices appointed to the Supreme Court for life, Fed governors therefore should not owe their ongoing positions to any particular political faction. The next guarantee of central bank independence is that the Fed Chair is nominated by the President from among the governors and gets appointed to a four-year term that does not coincide with a President’s four-year term. Janet Yellen, the current Fed Chair, plans to stay in office at least through her term in 2018.

Inflation spikes correspond with political interference with the Fed

The specter of political interference in Fed policy has darkened our political scene before. Economist and former Minneapolis Fed President Narayana Kocherlakota recently wrote about historical problems when the executive branch interferes with the US Fed. During and following World War II, the Fed kept long-term rates artificially low to allow the government to borrow cheaply. Inflation soared to nearly 10 percent by the time the Korean War began in 1950. Later, Narayana reports, Presidents Johnson and Nixon pressured the Fed to stimulate the economy, leading in part to astronomical inflation of the ’60s and ’70s that peaked at 14 percent in 1980.

With President Trump able to appoint a new Fed chair and vice-chair in 2018, plus the chance to fill two more currently open spots on the Board of Governors, a real point of pressure exists. By 2018, he will have appointed four of seven Fed governors. Would Trump show restraint, or would he pressure the Fed to support his agenda?

Authoritarians, as a rule, cannot stand independent central banks. They don’t like the idea that some entity independent of them can wield vast power over both the real economy and banking institutions.

The U.S. enjoys a massive financial subsidy because, up until now, the wealthy of the world trust that our currency will not be suddenly inflated away to worthlessness. An independent Fed assures the world that authoritarians cannot bend monetary policy to their will. But authoritarian regimes, the kind that curb central bank independence, never get trusted with this kind of financial status, as a place where global holders of capital want to park their surpluses.

There are many areas where Trump’s actions might undermine our strengths as a country. Attacking the independence of the Fed is one of the most important ones to watch out for.

Threatening bond markets

Last but certainly not least, it takes a long time (dating back to Alexander Hamilton!) to build up the kind of credit the United States gets for political independence in monetary policy, as well as the kind of trust that attracts global capital to fund our government. It probably only takes one aggressive authoritarian to make that capital flee. And if it flees quickly, that alone can cause a financial crisis.

During the campaign last Summer, Trump argued that if the US borrowed too much, he would simply re-negotiate our debts.

“I’ve borrowed knowing that you can pay back with discounts. [As President,] I would borrow knowing that if the economy crashed, you could make a deal.”

Um. Wut.

Holy fucking shit. Gah. That’s not how it works with the US bond market. You don’t default (that’s what “making a deal” means) on the US bond market. Or at least, you don’t get to do it more than once. Because suddenly you’re Argentina, or Ecuador, or Ukraine when it comes to your ability to borrow.

He’s talking about treating our country like one of his Atlantic City casinos, walking away and stiffing our lenders. If bond investors took him seriously and literally (like I do) we’d have an immediate financial panic. Personally I think Trump’s attitude towards US sovereign debt is the scariest thing he’s ever said, in terms of a threat to the continuation of the United States of America as we know it.

And that’s saying a lot, considering what’s come out of his mouth or Twitter account.

Who will be to blame?

If an economic or financial crisis occurs under a Trump administration, I don’t see the events as something that would cause Trump to reflect on his actions or take responsibility for his errors. I think he will see the crisis he caused as an opportunity to blame his enemies.

An economic crisis – like a security crisis – can make people desperate for action, any action (however rash) to make it better. People who are angry or fearful about losing their jobs or financial status or fortunes are more likely to turn a blind eye to constitutional encroachments.

Those constitutional encroachments are in the end what I’m most worried about, and are what I will write about next.