I went online recently to explore certain hard-core taboo subjects. I looked up words we don’t talk about in polite company. Certainly not in front of the children. Words like Trust Fund. Inheritance. Aristocracy.

I’m interested in the fact that when it comes to these concepts we don’t openly agree on what kind of society we want.

For example, it’s clear to me from the major tax reform of December 2017 – which raised the estate tax exemption for a married couple to $22.36 million from the previous $11.18 million exemption – that we as a society want more trust fund kids. Trust fund kids are great. Surely, despite our political differences, that’s something we can all come together around as a nation?

Trust Fund

Speaking of which, in the past year I agreed to be a trustee for some family members. I received copies of their “Last Will and Testament” documents. I’m really a “backup” trustee, in the sense that I’m a trustee only in the unlikely circumstance that my relatives die young, while their children are quite young themselves.

Clearly my relatives did well picking a good trustee. But what is the right age of inheritance?

A main point of the written will on which I am named trustee is to ensure that if my relatives die early their two children do not receives big piles of money at too early an age. They stand to receive one-third of the inheritance upon reaching their 30thbirthdays, and the remaining two-thirds of their inheritance upon their 35thbirthdays. If their parents live a long and full life, the children will inherit money significantly older than that, there will be no restriction on their inheritance, and my own role becomes unnecessary, as we all hope it will be.

The idea here, according to my relative who asked me to be the trustee, is to delay as long possible the pile of money that her girls could inherit. I asked my relative how and why she chose those ages of inheritance. Why not 25? Or 45? Why not give it all to them?

Says the mother of the girls, “I just came up with those ages based on my own experience and my reading that most young people who inherit money lose it before long. We ran them past the attorney and he seemed to agree, so we went with it.” So not a lot of science, just recognizable common sense.

I hope you realize I was being sarcastic above about trust fund kids. My relatives – like most thoughtful people – don’t want to create trust fund babies either. They want their children to become hard-working adults whose professional lives are already in full swing – their mid-30s – before they get money that could demotivate them or encourage bad habits.

When you jump down the rabbit-hole of the trust fund sub-genre of personal finance literature you’ll find interesting articles like “Confessions of A Trust Fund Baby.”

I’ll summarize for you a few of my findings based on this reading:

Coke, booze, Ecstasy, and clubbing really is more plentiful among the trust fund set.

It’s a lot easier to take certain poorly paid jobs, in certain expensive cities, if you have a trust fund.

Money is a delightful safety net, but cannot confer meaning.

As a reader of Anthony Trollope and Jane Austen novels, I suppose I’ve long had this interest in trust fund kids. None of the main characters in these 19thCentury romances actually works for a living. The only question is how much annual income they may each depend on without working, and what suitable romantic matches may be made to help or hinder their continuing in the style to which they’ve become accustomed. This was all discussed in the 19thCentury without shame and without a sense that being a trust fund kid implied you were a wastrel. In fact, not working for a living was the key sign that you were a worthy person, a gentleman or a gentlewoman.

In the 20thand 21stCentury by contrast – and in contrast to my sarcastic comments above – we mostly carry a combination of worry about and contempt for trust fund kids. That’s not necessarily fair to the kids – they didn’t choose to inherit the money. But I think it’s interesting that our collective attitude is at odds with the direction of estate tax legislation.

Estate Tax Changes

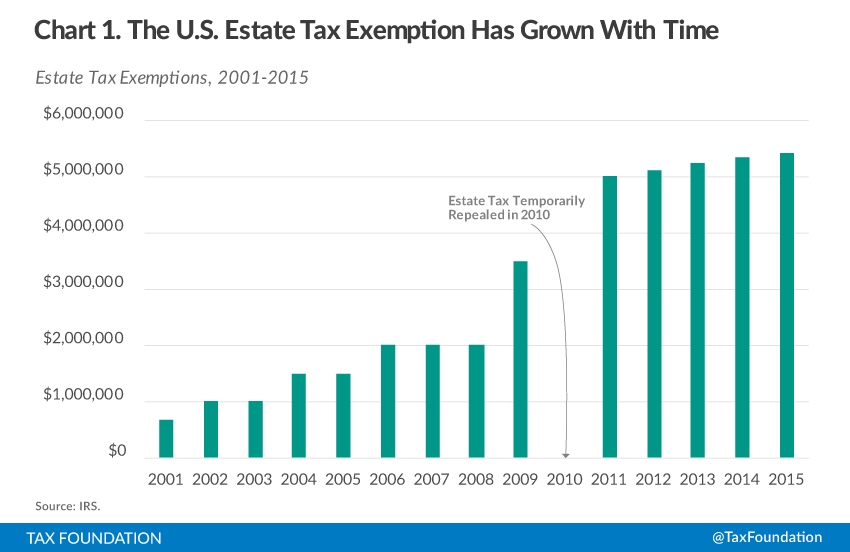

The tax-free inheritance number has climbed dramatically since 2000. When President George W. Bush came into office, children of wealthy parents could inherit up to $1.35 million tax free. The estate tax – the tax imposed on amounts above that exclusion – stood at 55 percent.

Under Bush, the exemption number began to climb steadily year by year to $4 million, while the tax rate fell to 45 percent. During the Obama era, the tax exemption jumped further and then climbed annually to $10.86 million. Meanwhile, the tax rate dropped to 40 percent. Now with the 2017 reform, lucky heirs can inherit from their parents up to $22.36 million, tax free.

Our tax system is increasingly designed to return us to the 19thCentury, even if the way we think about wealth concentration and inheritance remains rooted in the 20thCentury. As a country it feels like we have this weirdly bipolar and contradictory attitude toward trust fund kids.

I think we should just admit we prefer an aristocracy. The plain fact is we’ve steadily reformed our tax laws throughout the 21stCentury so that we can have more of it.

One of Piketty’s main goals is to understand the conditions under which concentrated wealth can emerge, persist, vanish, and perhaps reappear.

Piketty’s unique offering, I think, it that he (along with colleagues) built the most complete, historical, transnational data-set on wealth distribution. Specifically, he allows us to compare three centuries of wealth data in France and the UK. He also built the most complete data sets on wealth in Germany, Italy, Scandinavian countries, Japan, and the United States.

Through that longitudinal data we get to see what has changed over the centuries, and where we stand today, compared to the past. We also get to see how the United States stacks up against other wealthy countries.

I’m late to the party in reviewing Piketty’s book – published in 2014 – but I think it doesn’t matter. He’s got centuries of data behind him and the book has a long shelf-life ahead of it.

All inequality discussions are political

Even engaging in a discussion about inequality involves political and normative choices. What we choose to measure, for example, has a great effect on what conclusions we draw.

Readers of Piketty’s work, naturally, come armed to the fight with political agendas. I know I do, and you do too. I happen to think inequality is a defining problem of our time. Others may not agree. ‘How much does inequality matter’ is a deeply political question in and of itself.

Piketty offers a great example of this, when he cites governmental measures of inequality. Traditionally, OECD governments present the ratio between the 90th (top) percentile of income and the 10th (bottom) percentile of income as a proxy for income inequality. Problematically, Piketty points out, this so-called P90/P10 ratio completely ignores the vast concentration of wealth within the top 1% of many countries. The bottom 9% portion of the top 10% in the United States, for example, look like pikers compared to the top 1%, a fact that the P90/P10 ratio tends to hide.

Additionally, the ratio will not indicate what portion of national income the top 10% earns, whether it’s 20% as in the case of Scandinavian Europe in the 1980s, 50% as in the case of the contemporary United States, or 90% in the Belle Epoque era of Britain and France preceding World War I. By choosing to present the P90/P10 ratio, governments choose the ‘chaste veil of official publications,’ a set of data that obscures as much as it enlightens.

War as Equalizer

The devastating wars of the 20th Century destroyed so much concentrated wealth in Britain and France (in addition to Germany and Japan, obviously) that they literally upended the social order. Piketty’s data shows how wealth concentration with the Top 10% and 1% in these countries plummeted in the first half of the 20th Century.

Wealth inequality stayed relatively tame in the decades following World War II, before ticking upward in the 1980s and beyond. An easy explanation for renewed wealth concentration may be changing tax rates, especially following the Reagan & Thatcher revolutions in the Anglo American countries.

Austen & Trollope & an Economist’s style

I have long looked to Jane Austen and Anthony Trollope as sources of information on the meaning and use of wealth, so I was pleased to see Piketty do the same.[2]

Jane Austen

Outside of these 19th Century literary references, Piketty does not rely on metaphors, popular writing, or anecdote. He’s an economist, primarily focused on his data and formulas to explain wealth creation. Like a serious economist, he takes great pains to explain his data collection methods and to circumscribe his conclusions. This makes for drier writing, but high credibility.

The Piketty thesis, in a thumbnail sketch

Piketty has a math-based worldview on how wealth becomes concentrated, and how it may inevitably lead to inequality in the future. I’ll attempt to concisely describe it here, so that you may mention it casually and sophisticatedly at your next cocktail party to impress your friends. You are welcome.

In the first section of the book, he builds the case that the proportion of national income that goes to ‘labor’ (what people get paid to do in exchange for the application of their time and talents) versus what goes to ‘capital’ (financial returns that accrue to an accumulated stock of wealth) is a key set of numbers to study in a national economy.

A key number for measuring this is what he calls the national “capital/income ratio” – which measures the stock of accumulated wealth of a country compared to the flow of total national income in any given year.

Typically we might see that the national wealth in a developed country is five or six times greater than the country’s income.

This ratio allows Piketty to measure – over time and across countries – the amount of money that ‘capital’ earns each year versus what ‘labor’ earns each year.

A household analogy for the capital/income ratio

To break that down into household terms and in numbers that our brains can handle, we might say that the capital income ratio of my household could be five if, for example, I boasted of a personal net worth of $500,000 and an annual income of $100,000. I mention the household analogy to illustrate the capital/income ratio as just a way of comparing the fixed accumulated store of wealth with a flow of annual income. Piketty focuses on measuring this number for countries over time, counting the entire national ‘store of wealth’ and the entire national ‘income.’

Second number: % annual return on capital

The reason why the national capital/income ratio matters is that it allows Piketty, and us, to see how much of national income is earned by ‘labor’ versus how much is earned by ‘capital.’ To do this, we need to know what the overall annual ‘rate of return’ on capital is in any national economy. This rate of return is just like how it sounds: If I invest $100,000 for example, do I make 2% on my money, or 6%, or 15%? An individual’s return on investment will depend on the particular investment of course – a bank CD vs. a bond vs. a stock vs. a rental property vs. an angel investment in a startup – to cite a few well-known possible investments. That aggregate national ‘return on investment’ will be the average of all these investments across millions of households and firms.

We might find, and Piketty does, that the average national return on capital often fluctuates in the 4 to 5% range over time.

Certainly Austen and Trollope generally assumed a 5% return on capital. A gentleman landowner who could count on 5,000 pounds per year in income might have been able to value his holdings – although voluntary land-sales were all but forbidden back then – at around 100,000 pounds.

Putting them together – income from capital

A fundamental math formula underpinning Piketty’s book is that the capital income ratio, multiplied by the return on capital, tells us what the overall proportion of income derived from capital is in a national economy. Money either comes from working (labor) or from investing (capital) and it helps us to be able to calculate what portion comes from capital.

Piketty, and we, care about this because it’s the beginning for understanding how wealth grows on wealth and how, possibly, an increasing rate of wealth inequality may in certain circumstances acquire a sort of mathematical inevitability.[3]

To return to a household analogy for a moment – which may help explain what Piketty measures at the national level – we could say again that I have a capital/income ratio of five. That’s based on my presumed $500,000 household net worth and $100,000 annual income (and $500K/$100K is five).

We could then assume that my return on capital (picture my $500K invested in ‘capital stock’ although in reality it might be entirely tied up in my house, but whatever) as 5%. When we multiply 5 fives 5% we get 25%, which represents the ‘annual income derived from capital’ of my household for example.

That annual income derived from capital – at the national level – is what Piketty takes great pains to build historical data around, and to track through time and across countries. We can see from the first math formula that the capital/income ratio determines to a great extent how much of national income will go to holders of capital (in simpler terms, holders of wealth. In simplest terms, how much goes to capitalists rather than workers.)

Piketty tracks the decline in ‘annual income derived from capital’ from the early Twentieth century through World Wars One and Two, but then the steady increase in the annual income derived from capital since the 1950s, as a way to understand changes throughout the last century.

A second math formula

Upon this foundation, Piketty introduces a second math formula. The capital/income ratio will tend to converge toward, over the long run, the ratio of the national savings rate divided by the growth rate of the economy.

A country with a high savings rate will tend, over time, to have a higher capital/income ratio. A country with a low growth rate (because the growth-rate number is in the denominator of the formula) will tend to also have a high capital/income ratio. Both of these situations we might expect will tend to exasperate inequality, as more of a nation’s wealth goes to capital, rather than labor.

By contrast, we would expect high growth rates in the economy over time to lower the capital/income ratio, and over time to lower the percent of income that goes to capital, rather than labor. That might correlate over time with lower inequality.

In either case, small changes in the economic growth rate can have great effects on the capital/income ratio over the long run. This second formula’s predictive capacity, Piketty clarifies, only works over the long run, possibly over decades. Nevertheless, he argues that its effects are constant and unavoidable.

Viewing the future

From a predictive perspective, Piketty would point to the savings rate, the economic growth rate, and the return on capital as the key measures of whether inequality will tend to increase or decrease in a national economy over time. Lower savings rates should lead to higher equality of wealth. Lower returns on capital should also leader to higher equality. But perhaps the biggest determinant of future equality is the growth rate of the economy.

And to simplify 600 pages of complex economic thought: Looking forward the slower secular growth in the economy of developed countries may inevitably doom these economies to increasing rates of wealth inequality.

A further summary of his data: The United States and Britain and France continue to move in a trend – begun in earnest in the 1980s – toward wealth concentration that will resemble the Belle Epoque of 19th Century Britain and France.

When we see the trends, it’s not hard to become alarmed about increasing concentration of wealth forming a sort of permanent aristocracy over our nominal democracies. Piketty urges us to note the data, note the trends, and try to understand the dangers to capitalism and democracy in the long run.

Policy Recommendations

Merely studying inequality is a political and moral choice, but making policy recommendations is obviously even more so. Here is where Piketty’s critics have mostly directed their fire.

Although I love his data and analysis, I am less certain that I will adopt Piketty’s prescriptive worldview on policies.

Piketty favors a progressive annual tax on large fortunes, as a way to combat the inevitability of wealth concentration. To the extent that would involve an estate tax, I am on board. The annual tax on wealth is obviously a further step altogether, since it would occur once a year. I can easily imagine the steps wealthy households would immediately take to avoid this tax, but Piketty nevertheless makes the case.

He also proposes a kind of global tax on capital, which as Piketty readily admits, is hard to imagine becoming a reality right now, both mechanically and politically. Banking coordination and reporting would be a crucial first step. This seems a long way off.

Piketty also favors an increased marginal income tax rate – possibly as high as 80% – on the highest earners in the United States. Although tax revenue from such a high rate on a small number of earners would be minimal, Piketty makes the case that the step would go some way toward reducing the concentration of income-capture by a small cohort of super managers, probably by voluntary compensation policy changes by large firms.

In each of these tax proposals Piketty seeks not to generate much revenue or replace existing tax regimes, but rather to regulate capitalism itself. If capitalism tends toward oligarchic concentrations of wealth – as the first ¾ of the book argues – his goal is to preserve the good of capitalism (efficient allocation of resources, high productivity gains) while mitigating the effects of the bad.

Capital isn’t the last word on these issues, but a key starting point for a discussion on the state of things.

Please see related posts:

[1] My summary of Kennedy: First, great powers become great based on their economic strengths. Second, great powers subsequently take on imperial obligations, which require increasingly larger military expenditures. Third, great powers sink under the cost of their military obligations. Like clockwork! And it doesn’t bode well for the current hegemon, with a military budget bigger than the next seven biggest militaries, combined.

[2] He also references the novels of Honore de Balzac, who I have not yet read. But I will someday.

[3] Unless counteracted by policies – like taxes – or exogenous events – like wars. Describing these counterbalancing forces take up a significant portion of the book.

I thought I’d heard all the important arguments on the topic, and then this economist comes along with a totally bonkers idea that will never work.

“Hahaha, that Atkinson, what a goofy dreamer” I said to myself.

And then, over the next few days, I kept thinking about one of his totally bonkers ideas. It gnawed at me. And I realized that – practical and political objections be damned! – that is a pretty awesome idea.

That’s the way I feel about Atkinson’s ‘Universal Inheritance,’ which goes something like this.

Every eighteen year-old, upon gaining the right to vote, automatically receives an ‘inheritance’ from the federal government of some amount of money. Atkinson proposes a universal inheritance in the UK of 5,000 pounds, or about US$8,100 per kid.

Now, as a father I’ll be the first one to say, instinctually, kids shouldn’t inherit money. I mean, their brains have under-developed frontal lobes! They’re undeserving and can’t handle that kind of responsibility.

Also, as an American deeply immersed in the dominant financial paradigm that ‘Money for Nothing’ works as a Dire Straights anthem but not as social policy, my first grumbly thought about this idea was ‘those kids will probably just squander their $8,100!’

I can already picture the insidious marketing campaigns launched by Las Vegas casinos as soon my legislation for ‘universal inheritance’ for 18 year-olds passes Congress.

Because of curmudgeonly American fathers like me and similarly grumpy readers like you, clearly Atkinson’s universal inheritance has ZERO chance of happening anytime soon in the United States. Yet I’m intrigued by the thought experiment so let me tell you why I see this as an interesting, possibly awesome, idea.

And by the way, for those of you reading this, who picture a Red Socialist hammer and sickle above my head, I really don’t see this in bleeding-heart liberal terms. I see it as an affordable solution to a failure of the free market, the under-development of talent in an economy.

For the poor but ambitious, could a universal inheritance be the key to continuing their education?

For a huge number of 18 year-olds today, a lack of capital will prevent their enrollment in the next educational program beyond high school, whether that’s an apprenticeship/internship at a business, an associate’s degree, a state college, or an elite four-year private university.

Yes, scholarships exist in limited form to help some of those kids, and yes, some of the ambitious poor will manage to bootstrap their way to educational success. But even those lucky few will find financial roadblocks that scholarships don’t cover, like SAT prep courses, application fees, book fees, and transportation costs.

Clearly, with the cost of higher education these days, a $8,100 inheritance doesn’t get you very far along in a multi-year degree program. But it might be enough to make a start possible.

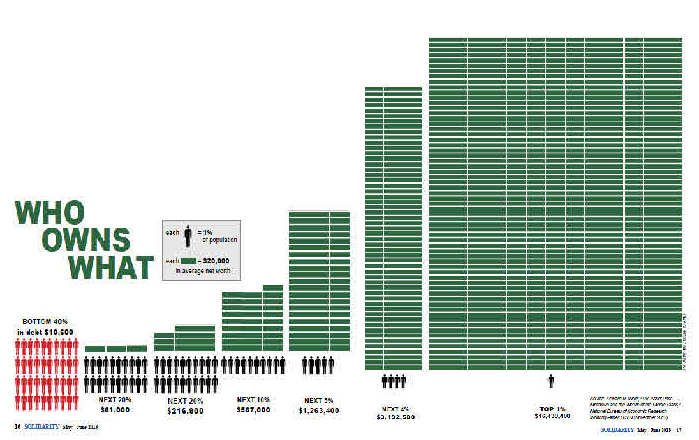

Who Owns What In America?

Why do I like the idea of a ‘universal inheritance’ rather than just further federal subsidies for student loans? I think because the universal inheritance is more flexible – it allows for more solutions than simply more ‘higher education.’

In my optimistic imagination the starter funds of a universal inheritance prevent the national tragedy of young people stuck in an economically-inefficient rut.

For a cohort of eighteen year-olds, a lack of capital may prevent their move from one employment backwater (a small town, a one-company suburb, a dying inner-city) to a more vibrant economy, in need of young workers.

In Queens, New York last month the young woman helping us at the car rental counter mentioned that “If I could just get $5,000 together somehow, someway, I could finally pursue my dream of moving down to Florida and becoming a designer. But until then, I’m stuck here.”

The way she described it, her $5,000 dream in life seemed like it might be years away. I’m picturing this universal inheritance as a one-time opportunity, if used wisely, to fulfill a dream otherwise impossible for children who come from poorer households.

I obviously don’t know what household situation the counter worker at Budget Rental comes from. I do know $5,000 doesn’t hold back other children, who drew a luckier lottery ticket by virtue of their birth family, from pursuing their life’s dream.

For the poor and entrepreneurially ambitious, could a universal inheritance be the key to starting a business?

The bus or the airplane ticket out of town. The first few months’ rent away from home. The new clothes for work, or for a job interview. The tools of a trade. The instruction manuals or training software and laptop. The initial inventory for a sales project. Partial tuition to a computer coding school.

With approximately 4.3 million 17 year-olds in the US, the annual cost of the universal inheritance program could be around 35 billion.

Clearly, the universal inheritance would make little difference to 18 year-olds from the top 10 percent of households, who control over 70 percent of the nation’s wealth, and even less difference to the top 1 percent of households who control close to 35 percent of the nation’s wealth. For them, this universal inheritance is just a lovely perk, a nice trip to Europe or an extra cushion for college expenses.

What that means, in practical terms, is that half of all teenagers become adults with no capital from their families at all to assist their next move in life, whether it’s work or further education.

In my optimistic imagination this one-time infusion of capital for everyone could create some opportunities.

See upcoming post:

The only feasible way ‘Universal Inheritance’ happens

Next January, when I receive the proceeds for a house I’m selling, I’m considering converting 70K from my TIAAF-CREF Traditional IRA into a Roth IRA, and paying taxes to do that that. I could then make my 7 grandchildren the beneficiaries and plan to not spend any of the Roth IRA myself unless I was desperate. I am 72 years old now, and my seven grandchildren range in age from 4 to 18. Could you make a spreadsheet to show me – and them – how nice that would be for them if I died at 90 and they received tax free income until they are all age 72 themselves?

Thanks, Julie from Massachusetts

Dear Julie,

Thanks for your question. You’ve highlighted one of the cool and little-discussed features of the Roth IRA, a potentially magical low-cost estate-planning tool for passing on tax-free income to young heirs.

The Roth IRA magic I’m about to describe happens because of three features unique to Roth IRAs.

First – unlike a traditional IRA – all withdrawals from an inherited Roth IRA are tax free to the beneficiary. Roth IRAs, we recall, require income taxes to be paid up front, either when a contribution is made, or in the case of Julie, when an existing Traditional IRA converts to a Roth IRA.

Second – also unlike a traditional IRA – you are not required to make any withdrawals from your Roth IRA in your own lifetime. If you can manage to survive without pulling out money from your Roth – as Julie referenced in her question – then you can leave that much more money for your heirs.

Third – heirs can withdraw money slowly enough from their inherited Roth IRA that their little nest egg can actually grow over time. The IRS has a schedule for inherited IRAs that shows how to calculate just how slowly money may be withdrawn.

By exactly how much money will the grandchildren benefit, and how does it all work?

Tax Free Inheritance!

The total value

I’ll take Julie’s example and run through the numbers, but let me hit you with the punch-line first:

Julie’s nest egg would produce nearly $1.2 million of tax free income for her grandchildren.

Here’s some fine print on that punchline: $1.2 Million of tax-free income assumes Julie starts with $70,000 next year; She dies at age 90; all of her grandchildren take only their minimum distributions until they turn 72; the accounts earn 6% per year; and each grandchild receives the total remaining value of their inherited Roth IRAs at age 72.

If I keep all of those above assumptions, except I dial down the annual return to a more conservative 3% return per year, her grandchildren receive $273,054 in total tax free income.

But what about the following?

If I dial up the annual return to a more optimistic 10% per year, her grandchildren would receive a total of $9.2 million in tax free income. 1

Now that I have your attention, how does the Roth IRA achieve this magic trick?

The magic happens over two phases, Julie’s life, and her grandchildren’s lives.

Julie’s Life

Traditional IRAs 2 require an owner to withdraw a portion of their retirement account as income every year after age 70.5. The IRS publishes a list for IRA owners age 70.5 and older about their required minimum distribution, roughly determined by the retiree’s expected remaining lifespan.

According to the IRS, A 72-year old like Julie would be required to divide the value of her IRA by 25.6 (the same divisor goes for all 72 year-olds), and take at least that amount out of her traditional IRA as income. 3

With a $70,000 Traditional IRA, Julie must withdraw at least $2,734.38 at age 72, (because that’s $70,000 divided by 25.6).

With a $70,000 Roth IRA, however, she is not required to withdraw anything.

If Julie is able to survive on rice and beans (and Social Security, and other savings) without drawing from her Roth IRA, the account will certainly grow for the next 18 years. At a 6% annual growth rate, her Roth IRA would reach $188,494 when she reaches age 90. At which point we assume each of 7 grandchildren inherits a Roth IRA worth $26,928 (because that’s $188,494 divided 7 ways).

The grandchildren’s lives

An inherited Roth IRA requires an heir to make minimum withdrawals, but in small amounts determined by the age of the heir. The minimum withdrawal amount is determined by the value of the Roth IRA divided by the expected lifespan of the heir.

The key here to the Roth IRA magic is that Julie’s grandchildren are relatively young, and the IRS allows young people with a long expected lifespan to withdraw money from inherited IRAs quite slowly.

So slowly, in fact, that each grandchild’s account is likely to grow over time, under reasonable annual return assumptions.

The eldest grandchild

Julie’s eldest grandchild, now age 18, would be aged 36 when Julie is 90. The grandchild could elect to take the inherited $26,928 all at once, but would be advised not to do so.

Instead, she should allow the account to grow over time, kicking off a growing amount of tax free income per year over the course of her lifetime.

At age 36, the eldest grandchild has an expected remaining life of 47.5 years, so could elect to take the minimum of tax free income of $555 (because that’s $26,928 divided by 47.5).

With that minimum withdrawal, assuming a 6% return, the account will grow each year. Withdrawals will increase each year as well, up to $4,136 when she is 72 years old, when the account will be worth $67,424.

The youngest grandchild

For the youngest grandchild, the deal is even sweeter. She would inherit $26,928 at age 23. Her original minimum withdrawal of tax free income would be $448 (that’s $26,928 divided by her expected remaining lifespan of 60.1 years). Minimum withdrawals would grow up to as much as $7,090 by age 72, at which point the account would be worth $109,903.

The younger the heir, the higher the potential for maximizing this Roth IRA magic, which can produce tax free income for life, long after the original retiree has passed.

In the most optimistic scenario, if markets return over the next 100 years at the rate they have in the past 100 years (a key “if”) Julie’s conversion of her relatively modest $70K Traditional IRA into a Roth IRA would produce close to $10 million in future tax free income for her grandchildren.

Incidentally, even though past performance is not indicative of future results, the S&P500 (including reinvestment of dividends) has earned 11.7% over the past 40 years. ↩

Just like other retirement accounts such as 401Ks and 403bs ↩

As a retiree ages and her remaining lifetime shortens, the IRS requires the retiree to divide by a smaller number, leading to higher distributions. A 90 year old must divide her traditional IRA account value by 11.4 for example, so would have to take out a minimum of $6,140 on a $70,000 account (because that’s $70,000 divided by 11.4). ↩

I’m interested in the fact that when it comes to these concepts we don’t openly agree on what kind of society we want.

I’m interested in the fact that when it comes to these concepts we don’t openly agree on what kind of society we want. I hope you realize I was being sarcastic above about trust fund kids. My relatives – like most thoughtful people – don’t want to create trust fund babies either. They want their children to become hard-working adults whose professional lives are already in full swing – their mid-30s – before they get money that could demotivate them or encourage bad habits.

I hope you realize I was being sarcastic above about trust fund kids. My relatives – like most thoughtful people – don’t want to create trust fund babies either. They want their children to become hard-working adults whose professional lives are already in full swing – their mid-30s – before they get money that could demotivate them or encourage bad habits. As a reader of Anthony Trollope and Jane Austen novels, I suppose I’ve long had this interest in trust fund kids. None of the main characters in these 19thCentury romances actually works for a living. The only question is how much annual income they may each depend on without working, and what suitable romantic matches may be made to help or hinder their continuing in the style to which they’ve become accustomed. This was all discussed in the 19thCentury without shame and without a sense that being a trust fund kid implied you were a wastrel. In fact, not working for a living was the key sign that you were a worthy person, a gentleman or a gentlewoman.

As a reader of Anthony Trollope and Jane Austen novels, I suppose I’ve long had this interest in trust fund kids. None of the main characters in these 19thCentury romances actually works for a living. The only question is how much annual income they may each depend on without working, and what suitable romantic matches may be made to help or hinder their continuing in the style to which they’ve become accustomed. This was all discussed in the 19thCentury without shame and without a sense that being a trust fund kid implied you were a wastrel. In fact, not working for a living was the key sign that you were a worthy person, a gentleman or a gentlewoman. Under Bush, the exemption number began to climb steadily year by year to $4 million, while the tax rate fell to 45 percent. During the Obama era, the tax exemption jumped further and then climbed annually to $10.86 million. Meanwhile, the tax rate dropped to 40 percent. Now with the 2017 reform, lucky heirs can inherit from their parents up to $22.36 million, tax free.

Under Bush, the exemption number began to climb steadily year by year to $4 million, while the tax rate fell to 45 percent. During the Obama era, the tax exemption jumped further and then climbed annually to $10.86 million. Meanwhile, the tax rate dropped to 40 percent. Now with the 2017 reform, lucky heirs can inherit from their parents up to $22.36 million, tax free.

A version of this post ran in the

A version of this post ran in the