I spilled considerable ink this Spring bashing all manner of insurance products peddled as investment products. I base my un-sell of insurance products on their complexity, illiquidity, mediocre returns, and high costs. Now I will pull some of my punches and give a more moderated view of some annuity products.

The summary of my more moderate views: Some people are happy with their variable annuities and have had good returns, without paying excessive fees. If you already own an annuity product, I don’t think you should necessarily sell it right now, or right away. Finally, fixed rate annuities are at least simple. I like simple.

Don’t get me wrong. I don’t actually endorse these things.

Annuities generally put me in a dark place.

Other than their complexity, illiquidity, mediocre returns, and high costs, I like annuities just fine.

It’s like that awful joke: “Other than that, Mrs. Lincoln, how did you like the play?”

Other than that Mrs. Lincoln, how did you like the play?

I’ve received numerous responses from insurance salespeople this Spring about how weak my arguments are regarding annuity products. I read their responses and think of Upton Sinclair’s wisdom: “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Occasionally, when feeling cheeky, I respond to those emails, with Sinclair’s words.

But a thoughtful column-reader recently responded to my variable annuity-bashing by sharing his carefully kept spreadsheet of his variable annuity with Vanguard, which he bought in 2004. Quite frankly, he’s has been happy with it ever since.

His annuity owns a mixture of seven different equity-based Vanguard mutual funds. Whereas most variable annuity funds I’ve seen charge 1.5 to 2.5% management fees, his funds average 0.55% management fee, which I find utterly reasonable. In addition, the “mortality and expense risk charge” accompanying variable annuity funds – which typically runs from 0.4% to 1.75% across the industry – is a mere 0.17% at Vanguard. Again, quite reasonable.

Not coincidentally, he’s happy to report, his returns since 2004 have been quite competitive.

With a starting value of $110 thousand in early 2004, his funds grew to $340 thousand by mid-May 2019. That’s a 7.7% annual return over a little more than 15 years.

That compares pretty well with an 8.7% return including reinvestment of dividends of the Wilshire 5000 Index of the broad US stock market, or an 8.3% return for the S&P500 index of large US companies. Given mutual fund management costs, I’d say his 7.7% annual compound return on his variable annuity is as good as one could reasonably expect.

His stated reason for purchasing a variable annuity product, rather than a straight brokerage product, is to simplify passing on wealth to his heirs. His belief is that the variable annuity will pass smoothly to his intended beneficiaries without the risk of going through a probate court. I am no estate-planning expert, but if this gives him peace of mind, then that’s great.

One of the distinguishing characteristics about this variable annuity investor is that he was not sold the product by a commissioned salesperson. That partly explains his low costs.

My second moderating comment about various annuity products is that I would not presume to tell anyone to sell theirs, if they already own one. That’s a question that I get asked whenever I talk about how terrible they are.

So I’ll say it clearly: If you have an annuity already, don’t sell it right away. Often in personal finance matters, inaction is the best course. This is because action is costly, and other alternatives could be worse. Maybe what’s done is done. Maybe your annuity works for you. Maybe you have plenty of money already. I’m mostly talking about what you should not buy in the future.

Without knowing anything about your specific situation, a plausible solution to your problem of “I’m currently paying into a terrible annuity product, what do I do?” is to cease paying in to that product, starting paying for a better product, and then over time evaluate whether and how the existing annuity you bought can play a reasonable role in your long term financial plan.

And then finally, what about a fixed rate annuity?

I recently received a quote from my preferred insurance provider for a fixed rate annuity. I wanted to know, assuming I turned over $100,000, what kind of monthly lifetime income could I lock in? The answer is $391.64 per month, for life. I’m 47 years old. Were I older, the monthly payment would be higher, since I’d be more likely to die quicker.

The expected return on my fixed rate annuity was 3%. I don’t find that sufficient. I would never advise anyone with a net worth less than, say, $5 million, to buy one of these.

On the other hand, it’s very straightforward. We can all have different preferences for risk. Some annuities, especially fixed rate annuities, provide certainty. Fixed rate annuities like this are terrible for growing wealth, but have the advantage of simplicity. I like simple. And no fees. You turn over your $100 thousand. You lock in $391.64 for life. They are easily explained and understood. They never let you down.

Except under conditions of medium to high inflation. Other than that though, they’re safe.

A version of this post ran in the San Antonio Express News and Houston Chronicle.

Another reason I don’t like fixed rate, fixed index, and variable annuities is their low returns and high costs. These are directly related. The higher the costs to you, the lower your returns.

To begin with the simplest of the three types, fixed rate annuities are the exception in that they do not charge high fees. In fact, generally they don’t charge you any fees at all. Instead, they offer you very low returns.

I recently pulled some quotes from my preferred insurance company. For amounts less than $100,000 I could earn 2.6% guaranteed on a fixed rate annuity for the next five years, and I could earn 3% if I invested more than $100,000. I checked rates with another provider online and received quotes in the similar range of 2.8% and 2.95% respectively. That rate changes over five years. Mine had a minimum reset rate of 1.3%, after the five year term.

What should we think about these rates?

With a product like this, you should always reasonably expect that the annual return on a fixed rate annuity, adjusted for inflation and taxes, will be approximately zero. That’s not a typo. That’s just a rule of fixed rate annuity products and risk-less products in general.

Now, figuring the returns of fixed index and variables annuities is trickier because they are somewhat market driven and depend on what you pick as underlying investments and risks. But we can understand what the costs are, and therefore their expected underperformance versus comparable assets you could buy from a brokerage company.

With a variable annuity you have the chance to purchase mutual funds similar to funds at a brokerage account. Costs will weigh down your returns, however.

The management fees of mutual funds offered inside a typical variable annuity are typically very high. In the 2018 Brighthouse Financial Life (formerly MetLife) policy variable annuity contract I reviewed, the costs of mutual funds ranged from a low of 1.56% to a high of 2.71%. Hello? 1987 just called, and it wants its mutual fund fees back.

The cheapest 1.56% fund was a stock index fund which low-cost brokerages offer at 0.05% – or 31 times cheaper elsewhere. I really didn’t enjoy the 1.66% fees quoted on the Blackrock Ultra Short Bond Portfolio. That fund has a 10 year return of 0.39% – meaning you could have locked in huge losses after fees for the past decade, on a product supposedly meant to preserve capital. These types of egregious fund management costs are the rule, not the exception, when it comes to most variable annuity fund offerings I’ve reviewed. The Teacher’s retirement System (TRS) in Texas just capped mutual fund fees inside variable annuities at 1.75% following a “reform” in October 2017, to go into effect in October 2019. These fees are, in a word, bad. Even after that “reform.”

Why are the fees so high? I have a theory, and it goes something like this.

Insurance companies can impose huge fees on variable and fixed index annuities because they have selected their customers very carefully. Only people who don’t know what they are doing would select these providers and these products. So in essence they can charge whatever they like.

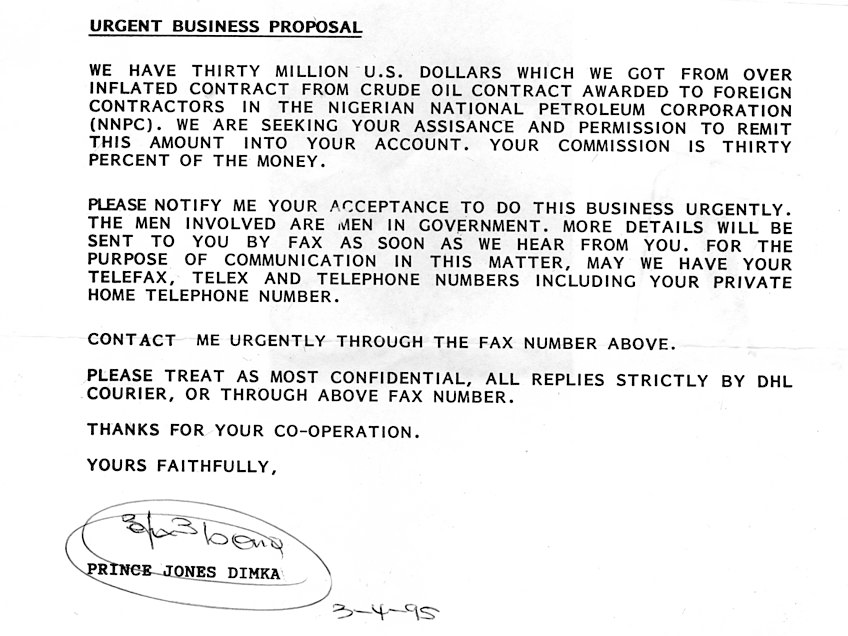

They employ psychology similar to how the “Nigerian Prince” scam artist who supposedly wants to wire you $10 million will purposefully misspell words in the solicitation email. The Nigerian Prince scammer knows that any target victim who replies has no powers of discernment. The misspelling in the email is a purposeful selection process by which the scammer chooses the right kind of victim.

Seems legit, right?

Similarly, whenever a public school employee sets up a “finance and retirement discussion” meeting with a commissioned insurance salesperson, the salesperson can have high confidence that the teacher has absolutely no idea what they are doing financially. The result: high fees, with impunity!

Of course, there are more fees after that.

Arguably the main service an insurance company provides with variable and fixed index annuities is a lifetime guarantee of payments, because they employ actuarial math that helps them make educated guesses about how long you’ll live. That seems like a service. And the insurance company seems to be taking a risk on you.

Ah, but they aren’t, not really. These complex annuities also charge a fee on your account called the “mortality and expense risk charge” – offloading that specific risk that you live too long – to you.

The 2018 Brighthouse contract I reviewed charged 1.2% per year for this “mortality and expense risk,” and the industry range is an extra 0.4 to 1.75% per year on these products. The lesson: If you charge high enough fees, you don’t end up taking a risk.

Finally, here’s my least favorite of all the low-return/high cost features of fixed index annuities.

This gets a bit technical, but bear with me, because this is really how the sausage is made.

The insurance company calculates the ‘growth’ in your fixed index account value based on the change in value of a stock market index over a year, but does not take into account dividends or the reinvestment of dividends that you would get, were you invested in the market directly through a brokerage account.

Over long periods of time working towards retirement – I’m talking about decades – the growth of your investment may be in substantial part due to dividends. Because of the way the company calculates returns, however, you probably don’t get the return on dividends from a fixed index annuity.

Does this matter? Oh yes.

Let’s say you had $100,000 in an S&P 500 brokerage account beginning in May 1989, held until May 2019. The return on the index over 30 years, considering only index price changes, is 7.7%.

However, the return on the index over 30 years, including the reinvestment of dividends, is 9.9%.

Hmm. Is that annual 2.2% difference a big deal? Yes it is. It’s the difference between ending up 30 years later with $818,000 or $1.6 million. But if you, as a fixed index annuity investor don’t get the credit for dividends or the reinvestment of dividends, who kept that money? Do I have to spell this out for you?

Over a long period of time, you may be leaving half your investment gains with the insurance company.

When you are a hammer, everything looks like a nail. Similarly, when you are an insurance company or commissioned insurance salesman, the investment solution everyone needs for retirement is an annuity. It’s what you sell.

As I do not sell annuities, all I can say is: Don’t buy these.

A version of this rant ran in the San Antonio Express News and Houston Chronicle.

Fixed rate annuities, fixed index annuities, variable annuities – how do I hate thee?

I’m not recommending this book. I haven’t read it. I just like the double-entendre of “Cons” = Convicts and “Pros = Only professional salespeople could like this.

Let me count the ways, for they are plural.

Let’s start with annuities’ complexity. In a future post I will address their mediocre returns and high fees.

Complexity matters because of a basic rule of financial products I just made up which, if you read it out loud, will sound a lot like your Miranda Rights:

“You and your money have the right to simplicity. Whatever you can’t understand can and will be used against you by the financial service provider.”

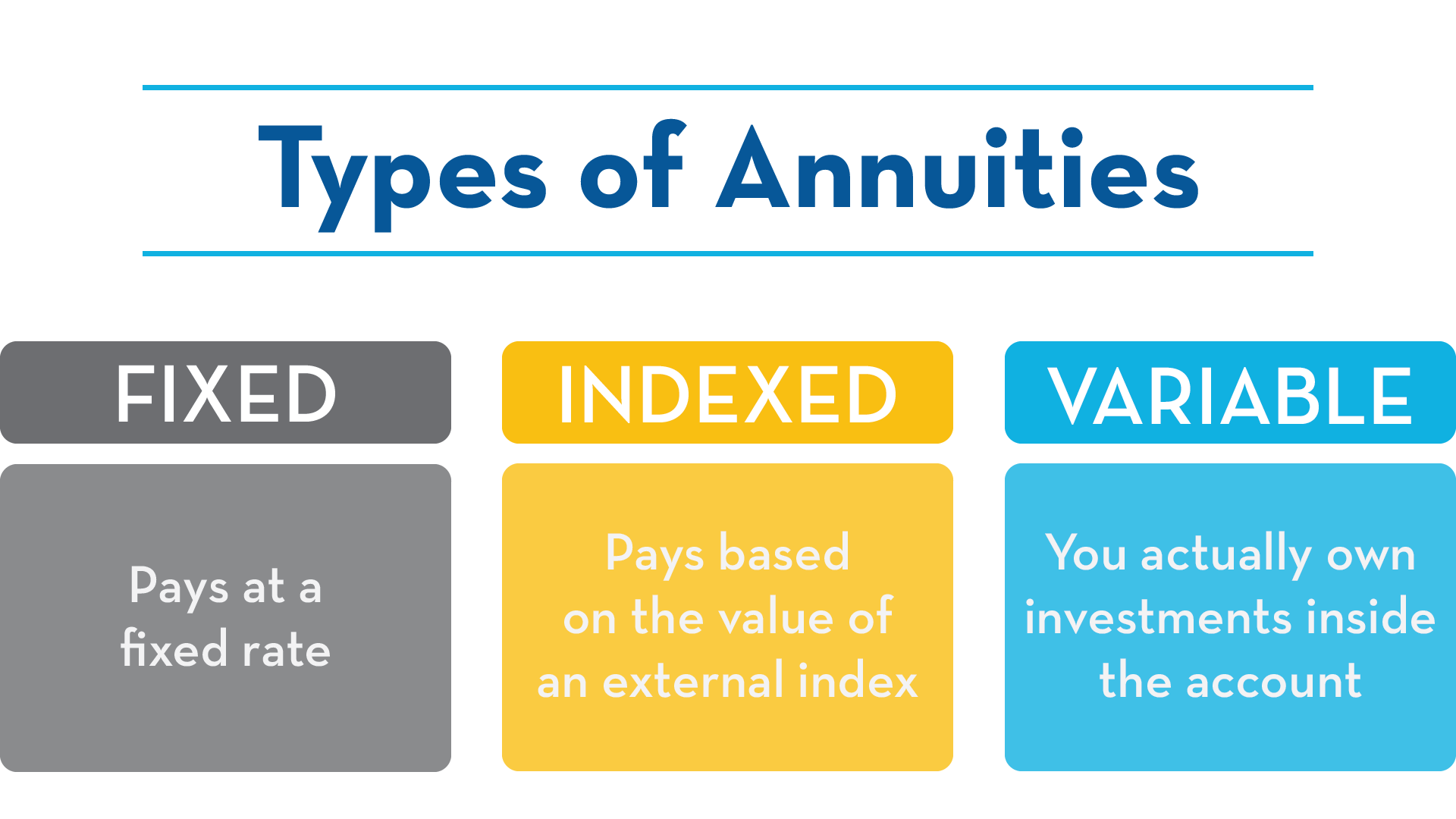

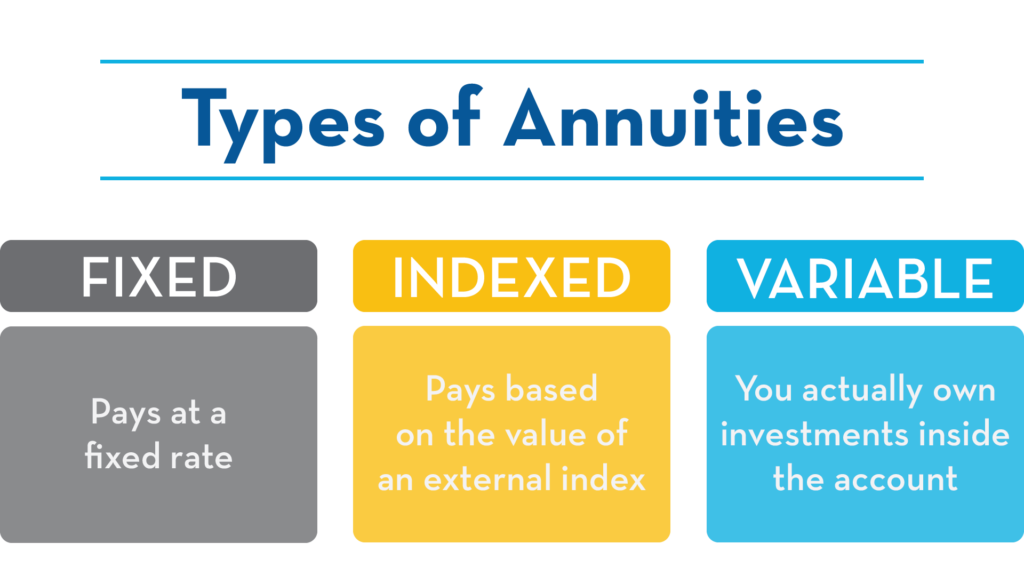

Annuities come in three main flavors.

The vanilla flavor – fixed rate annuities – are actually decently simple. These are not evil. You give money to the insurance company, either all at once or over time, and they agree to give you back your money in equal monthly payments, either for a fixed amount of time or more typically for the rest of your life, guaranteed. The only fancy complex math going on in the background of fixed rate annuities is an actuarial guess about when you’ll die.

The other two flavors – the confusingly named fixed-index annuity, and its close cousin the variable annuity – are far more complex. Their structures vary from company to company, so in describing them I can point out the possible complications, but the specifics will be hidden from you somewhere in the fine print of your contract. Like an Easter egg hunt, but far, far more costly.

The other flavors start out with opaque calculations as the insurance company collects your money over time. At some point when you’re done giving money over they morph into a simpler fixed annuity. In this way, the fixed index and variable annuities are like hungry fuzzy caterpillars, disgusting to look at. Eventually, however, they annuitize and become simpler fixed rate annuity butterflies.

In prepping this review I read every word of some of the most boring variable annuity product plan documents you can imagine. Three different company contracts from 2008, 2014, and 2018, plus The National Association of Insurance Commissioner’s Buyer’s Guide To Deferred Annuities.

So, about the complexity of fixed index annuities, and their variable annuity cousins. Both give the buyer exposure to “the market,” but in an indirect way.

With a fixed index annuity you give your money to an insurance company and they promise to credit your account with some of the gains associated with a stock market index, such as the S&P500 of large cap companies or the Russell 2000 index of small cap companies. But exactly how they do that is usually calculated in a complex way. The basic value proposition from the insurance company is that they say you can participate on the upside when the stock mark appreciates, but they will provide some protection from loss when the stock market drops below the amount you put in, or drops below the previous year’s highwater amount. It’s a kind of “some market upside and some safety” combo platter. Sometimes that protection is against a 10% drop in the market, sometimes it’s against any loss of principle.

But how do they provide this “safety?” A bunch of ways. Sometimes the contract limits your upside by a “participation amount,” like 80% of the index gains. So if the market index returns 10%, you get credit for just an 8% annual gain. Another feature might be a “performance cap” that limits the amount an insurance company will need to credit you with, in a bull market. The market went up 12%? Sorry, your gains are only 9%. You might pay a “Spread Rate” which is a % of market gains, by which your insurance company subtracts your returns. Spread Rate doesn’t sound like a fee, but that’s what it is.

A particularly devious way to limit your returns is to only credit the price change of an index, but not the dividends you would have received if you owned the index in a brokerage account. As I’ll explain in a future column, that might mean you’ve left half your gains on the table.

with guaranteed benefit riders. Helping to Protect your Income. in Unpredictable Markets. Variable Products: Are Not a Deposit of Any Bank • Are Not FDIC Insured by Any Federal Government Agency • Are Not Guaranteed by Any Bank or Savings Association • May Go Down in Value. ML

How does the company handle all this complexity?

As Jefferson Bank’s contract clearly states, “Subsequent Accumulation Unit Values for each Sub-Account are determined by multiplying the Accumulation Unit Value for the immediately preceding Valuation Period by the Net Investment Factor for the Sub-Account for the current period.”

It goes on like this for a couple of pages. I’ve read all the words and my head hurts.

Let’s go to the AXA Equitable document, to figure out our “Guaranteed Annual Withdrawal Amount” or (GAWA). Well, you see it’s, the, um:

“The sum of contributions that are periodically remitted to the PIB variable investment options, multiplied by the quarterly Guaranteed Withdrawal Rate (GWR) in effect when each contribution is received, plus

The sum of (i) transfers from non-PIB investment options to the PIB variable investment options and (ii) contributions made in a lump sum, including but not limited to, amounts that apply to contract exchanges, direct transfers from other funding vehicles under the plan, and rollovers) that are allocated to the variable investment options, multiplied by the Guaranteed Transfer Withdrawal Rate (GTWR) in effect at the time of the transfer or contribution, plus

The sum of any Ratchet Increase.”

Got it? As the teens would say: “Ratchet, dude”

Ok, here’s what you do need to know. You can’t independently observe their math. You own rights to a complex derivative – that’s not what they call it, but that’s what it is – and only they can tell you what that derivative is worth.

Variable Annuities should come with a 2-word review “Shit Sandwich” Nigel Tufnel: “They can’t print that!”

With a regular brokerage account, by contrast, you would see an observable market price for a mutual fund, or a stock or a bond, or an ETF.

Remember, anything you don’t understand can and will be used against you.

Do you want your money back yet? You can’t have it.

Generally once you’ve annuitized, you can’t accelerate or change your fixed rate annuity. Prior to annuitization, you can have some, but you will probably pay surrender or withdrawal charges on any fixed index or variable annuity that you want to get out of. You may be able to get 10% of your money back each year without penalty, but for additional money you should expect to pay a 5% fee under many contracts, with a slowly declining penalty amount per year.

So that’s the story on complexity and illiquidity. I’ll tell you next time about the bad returns and the high fees.

A version of this post ran in the San Antonio Express News and Houston Chronicle.

I argued in recent posts here and here that public school employee 403(b) retirement plans are confusing to enroll in and full of extremely expensive options, and that the bad program design seems to be on purpose, as it serves one particular industry1, at the expense of retirees.

The situation is so obviously bad that I figured surely public school employee advocates would be working hard to correct this problem. I reached out to public school advocates, as well as to the Teachers Retirement System (TRS) and legislators, hoping to find some good news.

I have no good news to report.

But first, I want to clarify a point that may have gotten lost in my attack on the status quo of 403(b) plans. I do not want to leave anyone with the impression that 403(b) plans should be ignored as a retirement tool by school district employees. Nothing could be further from my beliefs.

Between the automatic payroll deduction and tax advantages of 403(b)s, combined with the fact that TRS pensions won’t cover enough costs in retirement and the lack of Social Security for 95 percent of school districts in Texas, these defined contribution plans ought to be a key tool for retiring comfortably.

The fact that the status quo design of these programs is objectively terrible shouldn’t dissuade you from participating in them, or in an Individual IRA, if you know how to do that, and properly navigate your way to good products. Some how, some way, you need to put some retirement money away in addition to your TRS pension, which will prove insufficient, unless you put in a full 43 years to qualify for 100 percent of your last five years’ salary. Got it? Good.

Now, I have my hair on fire about 403(b) program design, so I began calling around to public school employee advocates. We need some allies here.

I called the Texas State Teachers Association (TSTA), with a statewide membership of 65,000 and an affiliation with the National Education Association (with 3 million members). Spokesman Clay Robison told me, “Generally, we’re in favor of defined benefits,” by which he means the guaranteed TRS pension that employees qualify for over time. When I tried to shift the conversation toward 403(b) plans, he wanted to emphasize that their organization believes defined contributions are “obviously riskier,” and that recent studies show retirees benefit more from defined benefits (like TRS) rather than defined contributions like 403(b)s. Robison continued, “Our focus is keeping the teacher’s retirement program sound, and keeping the system from moving from a defined contribution to a defined benefit plan. If teachers want to invest in a defined contribution plan, that’s entirely up to them.”

To my pressing that fixing 403(b) plan design doesn’t take away from the TRS pension, he replied, “We’re focused on the defined benefits plan, because we’re convinced it’s the best option and it’s less risky. The TRS is a sound pension plan. Managed by professionals. For those that can afford extra, that’s their business.” Ok, then.

I spoke with Bobbye Patton, past President (2012-2014) of the Association of Texas Public Educators, a non-union organization representing 80,000 members statewide. She said the issue of 403(b) plan reform has simply never come up within her organization. “I cannot remember that our association has talked about the 403(b). It’s always been focused on the retirement system itself.

“We have our TRS (pension). As far as I know, nobody pushes ideas about the 403(b). As teachers, we don’t understand it. We don’t fully understand what it would do for us.” Alrighty then.

Calls to the San Antonio Teachers Alliance, a local affiliate of the Texas AFT, and itself a state member of the national AFLC-CIO, did not get returned as of this writing.

I spoke to Rebecca Merrill, Chief Strategist at TRS itself, which is legislatively charged with administering and executing 403(b) rules statewide.

I wanted to know whether they are aware of the problems of 403(b) plan design, specifically forbidding school districts from designing a better system through a bidding process and negotiation. She assured me they understand the issues well.

“I don’t think its any secret that we’ve said ‘if it’s the legislature’s will for teachers to pay as low fees as possible, they should empower district to issue RFPs (Requests for Proposals) and negotiate lower costs.’” I asked if TRS itself could negotiate better terms for school district employees at the state level.

Merrill responded, “We feel like we can’t. The legislation provides for an open access system. The industry pushed back and said the legislature wants choice.”

To be fair, Merrill points that certain very heavy sales load charges on funds were dropped in the 2017 reform, and I agree that’s good. Merrill also pointed out that allowable fee caps on products were lowered, although I still believe the move to be very incremental only.

In reviewing the results of 2017 reform of fees within the 403(b) plan, I expressed to Merrill that this was “reform” that only an insurance company could love.

Merrill responded, “We made some recommendations for the (TRS) Board to go in a different direction. The Board did adopt some rule changes, including the fee caps. The Board heard from industry, and they heard from staff. We had a big dialogue with the industry. The industry wanted to make sure that advisors could be compensated. We worked through it the best we could.” At the end of the day, however, Merrill believes TRS cannot make the rules around 403(b) plans, nor can it interpret policy. “We are mindful that how 403(b) is implemented is a legislative question.”

Emailed questions and call to the office Representative Diego Bernal, San Antonio Democrat and Vice Chair of the House Education Committee went unanswered. Emailed questions and a call to the office of Senator Paul Bettencourt, Houston Republican and member of the Senate Education Committee as well as an advocate for shifting away from defined benefits and toward defined contribution plans, went unanswered.

And that, folks, is the depressing state of the world, with respect to the perfectly legal highway robbery going on with school district employees’ defined contribution plans.

Don’t look to teachers lobbies, the legislature, or TRS itself to fix this anytime soon.

School district employees in Texas attempting to fund their own retirement – through 403(b) defined contribution plans – face a garbage fire of bad choices.

A neutral and expert observer – anyone not directly benefitting from insurance industry money – can look at the retirement options mandated by school districts and see a rigged game.

Problem of Choice

How is the game rigged? Let’s start with the 403(b) plan problem of “choice.”

School district employees typically have access to a 403(b) plan – a tax-advantaged retirement savings plan through automatic payroll deduction. 403(b) plans as designed and regulated in Texas appear uniquely suited to make a lot of money, not for school district employees, but rather for the insurance industry.

Here’s the first problem with the 403(b) options, because of regulatory and legislative restrictions. In Texas, as in other states like California and Ohio, school districts may not be proactive or selective about what retirement companies and products teachers may access. This is known as an “any willing vendor” rule, according to school district retirement consultant Cecile Russell.

I imagine this “any willing vendor” idea was once sold to legislators as reasonable because it encouraged “choice,” which sounds appealing at first glance. What it actually does is stuffs the menu of investment options to a ridiculous point with insurance companies and insurance products.

Better Design

A better program design, better than this “any willing vendor” model, would involve limiting choices in 403(b) plans to low-cost and appropriate retirement products. A better plan would be designed by experts with fiduciary responsibility looking out for the best interest of school employees. Just as private sector 401(k) designers have to do. School districts in Texas are not allowed to do this with their 403(b) plans.

In Texas the Teachers Retirement System has approved 65 separate vendor companies. There are actually 74 approved vendors listed by TRS but some of those are affiliated companies. These vendors in turn offer 10,520 eligible investment products to school district employees.

That’s the first problem. Having 10,520 choices is not good. It’s a behavioral finance nightmare which produces what an economist would call “The Paradox of Choice” but which we could also understand more simply as “The Deer in the Headlights” response. For some, their 403(b) plan contributions stay stuck in a money market account earning no return. For others, they use the random dartboard approach to investing. The third option, by design, is that school district employees invest according to the plan of that nice insurance salesman offering free pizza in the teacher’s lounge. All of these are bad results in their own way.

At least two-thirds of approved 403(b) vendors in Texas are insurance companies or have insurance affiliates. Do you want to guess the result of having insurance companies as the dominant providers for 403(b) plans?

A study by independent consultancy Aon Hewitt estimated in 2016 only 24 percent of 403(b) investments are in mutual funds (the preferable products), compared to 43 percent in fixed annuities (the inappropriate product) and 33 percent in variable annuities (the abominably high-cost product.) Those last two products are specifically insurance-company products, whereas mutual funds are typical brokerage company products.

The result of these asset allocation choices, AON Hewitt estimated, is $10 billion in extra costs paid by 403(b) participant investors, as compared to a comparable 401(k) style investment platform available to private sector workers and products. This is a multi-billion dollar fiduciary failure involving many responsible parties.

One way to understand the asset allocation problem is to understand the effect of compounding different returns over a long career. A school employee who managed to put away $50,000 in her 403(b) by age 30 faces a vastly different retirement depending on what she chooses as her primary investment vehicle. A 4% return on that investment would become worth $240,000, as compared to an 8% return becoming worth $1.08 million by age 70. Differences in returns, when compounded over 40 years, lead to massive divergences in results. Costs and investment products matter tremendously.

Before 1974, only insurance companies could provide investment products to 403(b) plans, giving them a head start with these types of plans. But 45 years later, the relative absence of mutual fund providers stands out as a shocking result. After so many years that result must be considered a feature, not a bug, of 403(b) plan design. It suits the insurance industry to keep this territory for itself, at the great expense of public school employees.

Can reasonable people disagree reasonably?

Now, I haven’t yet explained yet why insurance products are particularly pernicious in Texas 403(b) plan platforms. Many nice people, including especially insurance company employees, believe these to be fine products.

They are not.

I am not anti-Insurance. I buy insurance. It has an important role to play in all of our financial lives. Fixed and variable annuities are not good products, however, for a retirement plan. They are specifically inappropriate within a Texas public school employee’s retirement account. But they account for 75% of the products!

I don’t work for any finance or brokerage company. This is precisely why, even if you don’t understand my point straight away, you should at least believe that I don’t have an ax to grind, except to state the truth as I understand it.

I would go so far as to say that any independent fiduciary for a teacher’s retirement plan – and by independent again I mean someone not paid by any finance company – would agree that these are not the best products for public school district 403(b) plan participants.

And yet, they are the dominant products. Why is that?

In subsequent posts I will lay out the plausible explanation for this result, which is a perfectly legal – but ought to be illegal – crime hidden in plain site.

I’m not the right age for reverse mortgages1 but a reader asked me for my help. Some deep-down part of me will always be a mortgage guy, so I decided to learn more about these things.2

The reader, named Jesse, aged 73, called to relay his experience trying to get a reverse mortgage on his house, and to ask for my advice.

For Jesse, his idea was to use the money he could pull out of his house to help pay for taxes and insurance in the coming years.

Although I had never paid much attention to reverse mortgages, I previously had a vaguely negative feeling about them. I’ll describe those and sure, there are reasons to be cautious.

In the course of following up on Jesse’s inquiry, I also earned a bunch of unique and kind of awesome features of reverse mortgages which I had never seen in any other loan product. My overall thought is that under the right circumstances, these could be very useful mortgages.

No Payments, Ever

The first weird thing is that a borrower can decide to never make any principal and interest payments on the loan. For life! The debt accrues interest of course but the borrower can choose to never pay on that interest or principal. The lender gets paid back eventually, when the house is either sold or the owner dies, but in the meantime the loan doesn’t require any payments. Ever. I’ve never seen that on a loan structure before.

Second, as long as the homeowner complies with the mortgage agreement – which means staying current on taxes and insurance – neither the homeowner nor the homeowner’s spouse can be evicted from the house. Ever. It’s a bank loan backed by collateral, but the bank can’t take the collateral for the life of the borrowers. This is also something I’ve never seen before.

As it turned out, Jesse couldn’t move forward with the reverse mortgage, however, because his husband Ralph is only 51, and Texas requires both spouses to be over age 62.4

Other states have more lenient spousal rules, but Texas has its own way of doing things, as you may have heard.

I’ll describe my three previous issues with reverse mortgages, as well as my evolving views.

Complexity is the Enemy of the Good

An important worry is that as a relatively unusual loan product, consumers could be more likely to make bad choices about a thing they don’t understand very well. Even a traditional home mortgage can seem complex but it resembles other products we’re familiar with, like an automobile loan or a personal loan.

A reverse mortgage, by contrast, acts a bit like a retirement account or annuity, in that you can take money out over time as you get older. It’s also a bit like a credit card or home equity line of credit, in that it “revolves,” meaning you can take money out but also pay it back as often as you like. But it’s also different than a credit card or home equity loan, because you don’t have to pay it back with regular or even any payments (until you die). One of my guiding principles of finance is simplicity. Reverse mortgages may be a complicated form of debt for some people, and complicated is the enemy of the good.

Somewhat reducing my fear, however, is that every prospective reverse mortgage borrower must take a financial counseling course by phone, mandated by the Federal Housing Authority (FHA), which regulates reverse mortgages. Guy Stidham, owner of Mortgage of Texas and Financial LLC, a San Antonio-based mortgage broker who offers both traditional and reverse mortgages, says these courses cost about $150 and take a few weeks to schedule, which serves as a kind of “cooling off” function for prospective borrowers.5

Borrowing capacity

One of the more complicated topics of a reverse mortgage is how much you can borrow. Big picture, you should know two things: First, you can generally borrow much less initially with a reverse mortgage than with a traditional mortgage. Second, the amount you can borrow against your house trends upward over time, at the same rate as your mortgage’s interest rate. Let me fill in a few details on this issue.

Your initial borrowing amount is calculated according to an FHA formula by taking into account three things: The value of your house, your interest rate, and your age.

The FHA says that the younger you are, the less you can borrow against your house. This makes sense since time will eat away at your home equity, and you are not required to make payments on a reverse mortgage. The FHA also says that the higher the interest rate, the less you can borrow. This also makes sense because a higher interest rate, compounding over time with no payments, will also eat away at your home equity.

With an online calculator you can see how much of your home value you are allowed to borrow against. If you test out the calculator, you’ll see a 70 year-old charged 4.5 percent can borrow less than 50 percent against their house. The typical range of borrowing is between 40 and 65 percent of home value, substantially less than the 80 percent standard with a traditional mortgage.

Here’s a weird quirk of reverse mortgages, however, The amount you can borrow against your house increases over time, precisely in line with the interest rate you are charged. If you’re charged 5 percent interest, your available borrowing limit increases by 5 percent per year. For reverse mortgage borrowers using this as a home equity line of credit, the annually increased borrowing capacity will seem like a cool feature. For people concerned with reverse mortgages eating up your home equity, this increased borrowing capacity may seem pernicious.

I won’t rule either way, except to say that debt in all forms is always a drug, which may be used for good or evil. The increasing borrowing limit just ups your dosage of the drug over time.

Are these high cost mortgages?

My second big worry was that reverse mortgage would be high cost products for borrowers. This fear turns out to be somewhat true, although there’s some nuance to the cost issue.

The biggest cost of a reverse mortgage is mandatory mortgage insurance. Reverse mortgage borrowers are charged by the Federal Housing Authority (FHA) 2 percent of the appraised home value. For a $500,000 appraised home, the FHA would charge $10,000, which would be rolled into your loan balance at the time of origination. The FHA also charges 0.5 percent annually on the balance, as further insurance against losses. I think this is the biggest contributor to reverse mortgage costing more than traditional mortgages.

Next, what kind of interest rate should we expect on a reverse mortgage?

Most reverse mortgages charge a variable interest rate. According to Greg Groh, a reverse mortgage originator with All Reverse Mortgage, last week the starting variable interest rate was 4.32 percent which, added to the insurance cost, would mean a borrower’s cost of 4.82 percent.

What do I think of those rates? They’re slightly higher than a traditional mortgage, but also less than the rate I’m currently charged for my home equity line of credit, on which I pay 5.49 percent, and happily so. So, the floating interest rate isn’t a big knock on reverse mortgages.

Joe DeMarkey, Strategic Business Development Leader of Reverse Mortgage Funding estimated fixed rates now between 4.375 and 5.125 percent, in the same ballpark as a traditional 30-year mortgage. So, again, the cost of a reverse mortgage isn’t particularly from an above-market interest rate.

DeMarkey points out that 80 percent of reverse mortgages have floating interest rates rather than fixed rates. With floating rate loans, the initial interest rate often starts out reasonably low but there’s always a risk that future higher interest rates make that same debt more expensive later.

Broker commissions and origination fees

Stidham allows that a broker like him can be compensated more by the lender to sell a reverse mortgage in part because they are a less competitive product. His fee for brokering a reverse mortgage could be up to 3 times higher than with a traditional mortgage.

Finally, there’s the issue of origination fees. The maximum origination fee is capped at $6,000, and would actually be smaller for smaller loans.

Closing costs like attorney fees, title insurance, and bank appraisals are all basically the same as a traditional mortgage. Groh reports that a reverse mortgage bank appraisal cost might run slightly higher, but on the order of $550 for a reverse mortgage appraisal rather than $450 for a traditional mortgage. Not a big deal there. The main big cost difference, as I said earlier, is the FHA-charged insurance, which is pretty hefty.

Servicing Details

The servicing component of reverse mortgages is slightly different than for a traditional mortgage. Since borrowers must live in their house, does that force a sale if an elderly person moves out to a nursing facility? Yes, and no.

Borrowers may live outside of the home up to 12 continuous months, meaning even an extended hospital stay or stint in a nursing home does not trigger any change with the mortgage.

Each year a lender sends an “occupancy certificate” letter to the home which must be signed and returned, according to Cliff Auerswald of All Reverse Mortgage. If the borrower does not return that certificate, then the servicer may send someone over to do a drive-by inspection of the property.

If the borrower decided to leave the home for more than 12 months, then in fact the loan would become due. For that reason, any borrower who doesn’t plan to stay in their home “for life,” should probably look for another product rather than a reverse mortgage.

Hollowing out Equity

My third big problem with reverse mortgages was that they clashed with my traditional view of the incredible wealth building potential of home ownership– a way to automatically build up a store of wealth by making affordable monthly principal and interest payments on your house over a few decades. Because reverse mortgages drain that value over time, they made me want shout “Wait…But that’s…that’s not how it’s supposed to work!”

Look, my strongest advice would be to fully pay down your home mortgage over 15 to 30 years, don’t borrow against your house, and depend solely on accumulated retirement savings plus social security to support you in your old age. There’s nothing wrong with that advice except for the fact that it sounds a bit like: “My strongest advice to you is to be rich in your old age.”

And, you know, that’s not very actionable advice by the time you actually retire.

If you can’t be rich, my second strongest recommendation would be to take out a home equity line of credit, since these are revolving lines, they allow you to flexibly borrow as needed, and act like a low-interest emergency credit card. They are awesome and we used one to renovate our kitchen and paint our house. I love my HELOC. A reverse mortgage therefore is really a third-best option, but it seems to me a pretty fine choice under many scenarios.

As my wife reminded me recently, one of my other long-standing theories of personal finance is that kids shouldn’t inherit stuff. Since we don’t intend to bequeath our house to our girls, I shouldn’t be opposed to draining the house of our home equity once we hit our 70s or 80s. At that age, the goal shouldn’t be to continuously build up assets (For what? For whom?) but rather to spend money to make our lives better.

If we planned to stay in our house, my wife and I recently agreed we’d be open to a reverse mortgage in our 70s.

This post is a combination of a couple of columns I wrote for the newspaper, combined into one long post. ↩

A reverse mortgage, sometimes called a home equity conversion mortgage (aka HECM), is targeted to 62 year olds and up. Home equity, I should clarify, is the difference between the value of a house and the amount of debt on the house. That means a $300,000 house with a $100,000 mortgage has $200,000 in home equity. A reverse mortgage is a kind of home equity loan, specifically to borrow in old age without having to make payments, if you don’t want to. ↩

As an aside, Jesse wondered if discrimination from the bank was at play because he’s gay. I told him he should hope for that, as a class-action attorney could solve all his financial needs and he wouldn’t need the mortgage any more. Alas, Texas law says your spouse can’t be younger than 62 to take a reverse mortgage, whereas in other states your spouse can be younger than 62. It’s age discrimination, not LGBT discrimination. No big discrimination win for Jesse. ↩

Disclosure: I have done consulting projects for Stidham in the past. ↩