Like everyone with a home mortgage, I have homeowner’s insurance that covers most catastrophes, although the list of covered catastrophes specifically does not include flooding.

Occasionally I worry because my house backs right up to the San Antonio River. Fortunately, my yard and house are outside the boundaries considered to have a 1 percent chance of flooding per year, the so-called “100-year flood plain.” So up until now I’ve never had flood insurance, nor have I been required to have it by my bank.

There was a bit of weather recently in Texas you may have heard about, which got me thinking again about flood insurance, and also about how reliable our current risk-assessment methods are.

As a financial rule, I’m usually in the “don’t buy too much insurance” camp, urging people to self-insure whenever possible. Or as the French might say, I adopt an “après moi, le deluge” approach to many insurable risks.

Flood insurance, however, might be in the special category of things for which self-insuring doesn’t work as well. Meaning, even though my house sits outside of the 100-year flood plain, I really cannot afford the unexpected but catastrophic loss of my house due to flooding.

I called up my insurance provider this past week to get a quote on flood insurance for my house. I learned a few things.

I received an annual premium quote of $499 for up to $250,000 in damage to my house, plus an additional $100,000 for personal belongings, subject to a $1,250 deductible in each loss category.

In fact, everyone has to go through a private insurance company to get this federal flood insurance. Almost nobody gets private flood insurance.

I mean, there’s also a private market solution, but barely. I went to one provider online and entered all my data to match the quote I got from my regular insurance provider. The annual premium would be $3,219. So, more than 6 times as expensive as the FEMA quote. With that difference, you can sort of see why the federal government dominates the market.

Matthew Hartwig, a spokesperson for insurance provider USAA, told me that their flood insurance call volumes rose up to 9 times their regular rates before, during, and after the landfall of Hurricane Harvey. Customer inquiries even now continue at a higher than normal rate.

Unfortunately, none of those flood insurance sales in late August and early September can help Hurricane Harvey victims, because of a 30-day wait rule, before recently-purchased flood insurance becomes effective. Buying now only helps for the next flood.

Interestingly, engineering and flood risk specialists are in the process of re-evaluating how we deal with flood risk these days.

The old way of risk assessment is to simply map out whether a property is, or is not, in a 100-year flood plain.

Patrice Melançon, Watershed Engineering Manager for the San Antonio River Authority, described to me at least a few engineering discussions underway in the wake of Harvey.

She cited her counterparts in Houston who are actively discussing whether the right level of “risky” should be to look closely at properties previously considered to be in a so-called “500-year flood plain,” or areas that have only a 0.2 percent chance of flooding per year.

Of course, a common-sense reaction to that news is to wonder whether things have changed, possibly due to climate change, such that previous rainfall data informing the 100-year flood plain is no longer accurate in 2017.

While FEMA still relies on maps that show the 100-year flood plain, they are developing – in conjunction with local partners like SARA – a more sophisticated set of maps that show the likelihood of flooding within 30 years, as well as the probabilistic severity of flooding inside and outside the 100-year flood plain, The new maps are “informational” and “consultative” rather than being used for regulatory purposes like the 100-year flood plain maps, but nevertheless represent the next level of risk-analysis.

I’ll be checking out those new maps. Even now, about 25 percent of flood claims occur on houses located outside of a flood zone. That’s on houses that are deemed safely outside the flood plain, like mine.

Finally, Melançon mentioned to me that SARA expects to receive, in another 3 or 4 weeks, updated computer modeling and analysis of what would occur if Harvey-level rainfall dumped on the city of San Antonio. I’m pretty interested in those results too.

Personally, I don’t want to pay $500 to protect against a thing that’s never going to happen.

On the other hand, a “thing that’s never going to happen” just happened all over the city of Houston and in towns up and down the Texas coast. And four different Category 4 and 5 hurricanes were never going to make landfall within four weeks of each other until Hurricanes Harvey, Irma, Jose and Maria actually smashed all normal expectations of weather patterns.

Not covered in your homeowners insurance policy

So, yeah, we’re buying flood insurance.

As a scary epilogue to this story, you know what else is not covered by regular homeowner’s insurance? Property damage due to nuclear war. And I know that’s never going to happen either, right? Anyway, enjoy your morning coffee with breakfast, everybody.

I’m a big fan of niche financial markets as well as learning about how NOT to invest. This leads me this week to the “life settlements” industry, and a subset of that business known as “viaticals.”

Living owners of life insurance policies sometimes seek to sell their policies on the secondary market to receive a lump sum of money as well as to relieve themselves of the obligation to keep up expensive life insurance premiums. Life settlement investors pay that lump sum, maintain the policy premiums, and then collect the death benefit when the original policy owner dies.

The purchasers of secondary life insurance policies, investment funds seeking an above-market return, usually take over policies of elderly or terminally-ill patients who no longer can afford, or who no longer wish to afford, the life insurance premiums on the policy. For the investor, ideally, the insured person dies quickly, before the premium costs eat up returns.

While regulated and considered legal transactions in 42 states, there’s an obvious ick-factor to life settlements, as investors essentially bet on, and benefit from, the early death of policy sellers. The faster the death, the greater the profits. Which when you think about it, you know, ugh. A life insurance policy for someone who beats the odds and lives a long time will end up costing investor the money, who pays too much in premiums, for too long, to ever make a profit.

Viaticals, a subset of life settlements, refers specifically to investing in policies of terminally ill patients, with less than two years to live, or the chronically ill, unable to perform two “activities of daily living” like eating or dressing oneself. For the policy purchaser, you can see how a life insurance policy of a terminally ill person on death’s door is worth a lot more than the life insurance policy of a healthy person.

The legitimate financial cases for buying a secondary life insurance policy are twofold. First, terminally-ill or elderly folks may need access to their cash today for end-of-life care. The industry first grew up as a response to the crisis of terminally-ill and relatively young men with AIDS in the late 1980s. They needed money right away and worried less about heirs or estate-planning.

Those earliest pools of viaticals, dedicated to purchasing AIDS policies, blew up catastrophically for investors in the mid 90s, when a miracle cocktail combining protease inhibitors and two other drugs transformed HIV from a death sentence to a chronic illness. The insured survived, and investors lost everything.

The second major category of sellers today are often older high net-worth folks who purchased life insurance as an estate-planning tool, but who later find their estate-planning needs have changed, and they no longer want to maintain their policy.

The “ick factor” associated with viaticals is not the main reason why I’d urge you to avoid this business opportunity, should it ever come your way. Rather, I’d avoid life settlements because the industry seems to attract both fraud and financial blowups like a jelly donut on my counter attracts ants.

The fraud probably happens because life settlements and viaticals are just niche-y and opaque enough to attract a certain type of scheme-promoter, who knows how to appeal to a risk-taking investor. That risk-taking investor in turn usually thinks they’ve found a relatively hidden, low-risk, high-return way to invest.

Fraud in the industry has been perpetuated in a variety of clever ways.

My friend Michael Stern, a successful industry veteran of the life settlements industry over a dozen years, described to me a few of the classic scams.

In Texas, one of the industry’s most notorious operators, Life Partners Inc, filed for bankruptcy in 2015 following $46.9 million in court-imposed fines against the company and its main executives for fraud and insider trading. The Wall Street Journal reports that Life Partners depended upon a physician – working on commission – who assigned shortened life-expectancies to policies where independent estimates would have been much longer. Those short-life estimates juiced the price at which the operators could sell life insurance policies to relatively unsophisticated investors.

Following that, maintaining the policies sometimes got too expensive for those investors, so the Life Partners executives repurchased policies from their customers to the financial benefit of insiders, leading to insider trading fines. The executives seem to have avoided jail time, and the business exited bankruptcy in December 2016, to be liquidated for the benefit of investors.

Stern explained to me that because policies are expensive for existing investors to maintain, some operators have fallen into the illegal practice of paying off old investors with new incoming investors, the classic definition of a Ponzi scheme.

USVI suffered some problematic pension investments

Stern also mentioned that his industry now has learned to blacklist or avoid purchasing policies from certain zip codes with a preponderance of fraudulent medical reports, where a medical examiner is likely boosting the value of policies by diagnoses which exaggerate the risk of imminent death.

In the US Virgin Islands last year, a viatical investment gone awry blew a $50 million hole in the territory’s government pension plan, a plan that was already in distress. The 2016 auditor’s report reads like a “what the heck just happened?” story.

Although the life settlements industry remains a relatively small few billion dollars in policies per year, compared to the maybe $20 trillion in face value outstanding of the traditional life insurance business, large and sophisticated sponsors do participate, such as Apollo Global Management (APO) and American International Group Inc (AIG).

As a side note, I decided long ago that when I write my first novel – a financial thriller obviously – the main plotline will involve a hedge fund dedicated to viaticals. Could a certain unscrupulous hedge fund manager, maybe, put a thumb on the scale to speed along the process of death? Nothing too obvious, you know, just some prudent risk management and juicing of returns on the margins. The patients were already pretty sick, you understand, so it’s a mercy, really. Think Robin Cook’s Coma meets Michael Lewis’ The Big Short.

While viaticals make a brilliant premise for a creepy novel, my financial advice is to leave this investment opportunity entirely to the professionals, partly for the ick factor, and partly because they are best equipped to navigate the fraud and blowups that seem to follow this industry niche.

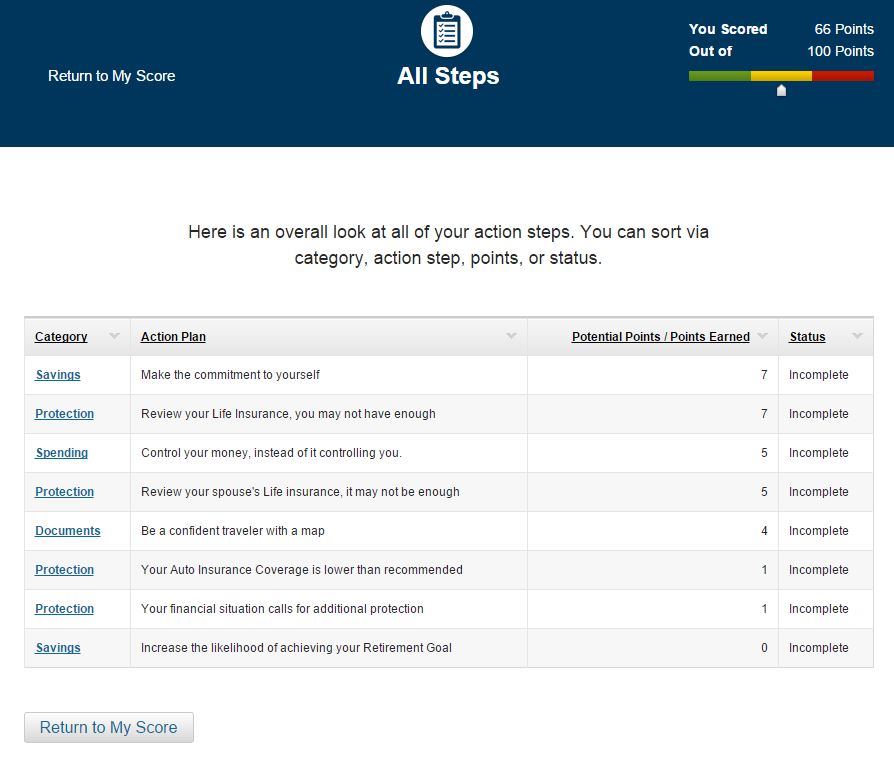

My personal bank – which also offers insurance and investments – recently invited me to discover my ‘Financial Readiness’ score, available in five minutes by taking a quick online survey.

Now, I am a competitive person who likes to win. For example, I know my SAT scores from high school, as well as my fastest one-mile and marathon racing times, by heart.

As a finance guy, I knew I would rock the Financial Readiness score. Bring. It. On.

The online survey asked me about my type of work, personal annual income, plus household income. Not bad, I thought, not bad.

Next, I answered questions on whether I rented or owned a home, the size of my monthly housing payment, and whether or not I budgeted. Home ownership, yes, budgeting, not so much. I hate budgeting.

Further questions prompted me to discuss my insurance against disability or loss of life, my dependents, and my retirement savings and investments. Well, I like to think I don’t over-insure, but I do have some retirement accounts.

Finally, the survey asked about whether I have documented my will, and whether I have named a health-care proxy. Yes. Totally. Nailed it.

My score

At the end of the survey my pulse quickened in anticipation of a huge pat-on-the-back for my incredible financial readiness.

I got a 66. Out of 100.

What?! Me? There must be some mistake.

A 66?

I’ve never gotten a 66 on anything in my life. Even worse, a 66 on my finances?!

I have three thoughts about my Financial Readiness Score.

A 66?!

My first thought I already told you, which is: “What?!”

That thought represents “Denial” and “Anger” steps in my five stages of grief.

Second Thought

My second thought – (possibly part of “Bargaining and “Depression”?) – came from a closer review of the Financial Readiness plan which my bank provided, following my score.

My Financial Readiness Report showed areas where I could improve my score, by reviewing and changing my approach to savings, planning, and financial protection.

The report suggested setting budgetary goals. That’s probably not happening. It also prompted me to consider upping my insurance coverage. Not surprisingly, my bank is also involved in savings accounts and insurance, so you can see a bit where they’re coming from.

I’m not saying their wrong. I’m just saying they have an agenda.

I have strong feelings about some of these things, and I think on at least a few topics, reasonable people could disagree.

In exploring these areas for boosting my score, I noticed robust prompts to action. In modelling out my retirement planning, for example, I got a chance to see how my intended retirement age, as well as my appetite for risk, would affect the probability of meeting my retirement goals. It was pretty cool, actually.

Third Thought

My third thought about my Financial Readiness score, as I move toward “Acceptance,” is that these simple but potentially catalytic surveys – paired with calls to action – might be quite useful. Let me expand on that thought for a moment.

Most of us need financial guidance. A fundamental theme of my financial writing is that almost nobody feels confident that they have all their finances figured out, yet few know where to turn to a trustworthy source.

We don’t like banks. We don’t trust our financial advisor. Insurance confuses us. The last thing we want to do as adults is spend precious free time with a lawyer to talk about what happens to all our stuff when we die. In all that confusion and natural aversion, we tend to not even know where to begin. So, like everybody else, we punt decision-making until some medium-distant future, maybe months from now, maybe when a crisis happens, or maybe until never.

Possibly, a five-minute internet-style quiz from my bank becomes the on-ramp to better planning and decisions?

I mean, not in my case, since the quiz is obviously flawed and they got my score wrong. But, you know, maybe for others.

In my favorite movie of all time, Rob Reiner recalls the two-word alliterative review of Spinal Tap’s unsuccessful second album “Shark Sandwich,” as simply “Shit Sandwich.’

The band members react to this shocking review with resentment, but also with a sense for what newspapers are allowed to actually say.

David St. Hubbins: “Where’d they print that?”

Nigel Tufnel: “That’s not real!”

Derek Smalls: “You can’t print that!”

Which bring me to my two-word review of an extremely popular ‘investment’ product known as the variable annuity. For variable annuities, I’ve got the same two-word review: “Shit Sandwich.”

Variable annuities deserve the same two word review: “Shit Sandwich”

They Can’t Print That

As I wrote this, I knew the newspaper I write a column for wouldn’t carry my real review of variable annuities.1

Of course they won’t let me print a traditional four-letter word. But, for the record, I really don’t think scatology is why most media “can’t print that’ when it comes to my review.

No, they really ‘can’t print that’ because insurance companies are really important media advertisers and variable annuities are really profitable for insurance companies. Hence, you will rarely see an honest review of variable annuities in traditional media.

I’ve been a faithful reader of the Wall Street Journal for nearly twenty years. They are the best daily newspaper when it comes to finance. Just about every three months or so the ‘Retirement’ or ‘Investments’ section of the Journal has a special on annuities, including ‘variable annuities.’ Alongside these sections of course are a slew of brokerage and insurance company advertisements. (If you didn’t already know, that’s the point of these special sections. This is the nature of the Financial Infotainment Industrial Complex.)

That’s where the fun begins. The writers of the Wall Street Journal are smart, and they are also commercially sensible, by which I mean they know where their bread is buttered. So they do this funny tortured-writer’s dance when describing variable annuities. “New annuity guarantees raise questions,” mumbles one ambiguous headline, or “They’re changing our annuity!” writes another, in which, buried in the heart of the article, we learn of many things that can go wrong with these things, without the writer coming out and saying the one thing he or she clearly knows, which is “stay away from variable annuities if you plan on having enough money in retirement.”

Up until this point I haven’t really explained: What is a variable annuity? Also: why should you care?

I’ll start with the second question first. You should care because an overwhelmingly large number of people who don’t know any better have followed their investment advisor/insurance broker/retirement specialist’s advice and bought this shit sandwich, to the tune of approximately $660 Billion. And this overwhelmingly large number of people plan to use it as a main vehicle for their retirement. Don’t know if you have one? Check your retirement plan. Do you use an insurance company for your investments? If yes, chances are, sadly, you bought one of these.

But back to the first question:

What is a variable annuity?

The insurance companies claim that a variable annuity is an investment product that offers both things that every investor wants, namely ‘safety’ plus ‘good returns.’ The variable annuity appears to offer ‘safety’ via a guaranteed income in retirement. The variable annuity also appears to offer ‘good returns’ by adjusting the guaranteed income upward if stock markets do well during the investment period of the variable annuity.

Ok, so…safety and good returns sounds pretty nice…What’s the problem? The biggest problem is extraordinary fees. Like, probably, all-in fees of 3.5 percent per year on your portfolio, which is a serious drag on your money (but great for the insurance company!)

All appearances to the contrary, insurance companies are really not magical wand-wavers that offer the mythical unique combination of safety and good returns. They pretty much just invest your money in stock and bond markets (plus real estate and some derivatives I guess) just like you can directly, except instead of offering you the actual returns of the blended portfolio you bought, they offer you the returns of a blended portfolio minus decades of huge fees. A really dumb combination of stocks and bonds invested over decades will beat a similarly-invested variable annuity every single time. Because of the fees.

Other problems

There are some other problems with variable annuities which I’ll list here for completeness’-sake.

Once in a while, but more often than we’d like, insurance companies totally miscalculate variable annuity payouts and throw themselves into receivership (a kind of bankruptcy for insurance companies.)

State insurance regulators know this, so they really like to see heavy fees to accompany these products, to keep up the capital base of insurance companies, to avoid receivership. That’s not good for you.

The other way insurance companies avoid receivership is to change the rules governing payouts after you’ve already bought in to the variable annuity. Yes, they do this, and that’s not good for you either.

States typically charge a special tax on payouts from variable annuities, possibly to compensate states for that future receivership problem. Also not good.

You owe ordinary income tax (meaning, top tax rates) on variable annuity income. Regular investments in taxable accounts, held for over a year, offer better tax treatment than this.

Variable annuities are roach-motel investments. You can get in easily, but it’s hard to get out, typically unless you pay hefty “surrender charges” if you try to get out within a 5 or 10 year “surrender period.” This is, basically, unconscionable. My advice: Just make like the French army,2 take the pain, and move on to a better investment.

Variable annuities come to you accompanied by unreadable documentation, incalculable payouts, and small-print ‘disclosures.’ Nobody buying into these things can actually explain to themselves how they work.3

That lack of understanding includes your insurance broker. Ask him some time to explain, in plain language, why this is a better deal than a simple blended portfolio of stocks and bonds. Whatever his moving lips appear to say, the real answer is “my fat commission,” which runs about 5 percent of the amount you invested.

As I’ve written here before, I don’t sell any investment product for a living, and no investment company or insurance company is paying me, so I don’t benefit whether you follow my advice or not.

Variable annuities are good for the insurance company because they make excessive fees from them. They are good for your insurance broker/retirement specialist because of the commission.

Good for the insurance company and great for your broker. Not good for you. But hey…

They are not good for you. But hey, as Meatloaf sang, “Two out of three ain’t bad.”

Newspapers of the world: I challenge you to print honest reviews of variable annuities.

But as Derek Smalls said, “They can’t print that.”

A version of this post, without the scatological reference, and with a toned-down version of my critique of how the Financial Infotainment Industrial Complex really operates, ran in the San Antonio Express News.

I’m not so much concerned with the vulgarity. (Although my editor was!) After all, let’s talk truth for a moment: you can’t read the national or international news section of any ‘respectable’ daily paper without worrying that your curious ten year-old will glance over your shoulder and ask you for definitions of ‘beheadings,’ or ‘pedophile,’ or ‘systematic rape.’ I mean, we’ve got worse problems than a little scatology. ↩

Except apparently this guy at www.annuityreview.com who offers, for an initial $150 fee, (and who knows after that, maybe more?) to analyze your variable annuity and give you a ten page report on all of its features, pluses and minuses. I don’t have any ties to the service myself, I only saw it referred to in the WSJ, but it strikes me as a good idea for people already stuck with these roach motels. Also, note the fact that if you need a ten-page report to describe your investment product then that investment has violated the “Keep It Simple, Smarty” rule of investing. ↩

The Fourth Law of Thermodynamics in my household states: “Physical objects that appear to be broken, will remain broken through time and space.”

I carry my un-handyness with me through life, including matters having to do with cars. When I came up with a flat rear left tire a few weeks ago on the way to drop off the girls, I rolled into the national-chain tire store a block away from their school. We walked from there.

Tire guy called me a half-hour later. (I will now paraphrase our conversation.)

“Your tire is unfixable, we’d recommend replacing that. We also noticed your two fronts are about three years old, have seen some wear-and-tear, and we are coming up to the fourth-year factory-recommended replacement time. So you should probably have us put new ones on there as well.”

“Ok, how much will that be?”

Now, as I mentioned, I am not handy. This places me at a specific disadvantage when it comes to having people diagnose and fix physical things for me, like my car’s tires. Tire Guy could have used some Walter Mitty-speak (“Uh, sir, we’re noticing the bifurcated invertabrator is missing three hamnails, and we’d recommend slotting in a T-bolt in the five-square”) and I’d probably agree to get those things fixed as well. I mean, how could I argue with him? It sounds legit.

A crucial error

But then Tire Guy made a crucial error. He quoted me the price for new tires. It was roughly $90 for one tire, including – he wanted me to know – a very good deal on a warranty, or $270 for three tires, again including a great deal on the warranty, plus labor. That put me all-in around $330.

Ok, that’s a lot, and I don’t know anything, and I knew I’d probably have to agree to that price.

But I do know one big rule of personal finance, which I will now pass on to all of you, and which constitutes the entire purpose of this long-winded tire story:

Warranties, generally speaking, are bad.

“So ok, $330, that sounds like a lot,” I tentatively began, “how much would it be without the warranties?”

“Oh well, you see, that was a really good deal on the warranties,” he began to reply.

“Ok, I get it, but let’s say I want to skip the warranty?

“Let me recalculate here. Um, yeah, it looks like about $385 without the warranty. You see it’s all part of the package deal.” (Please note: $55 bucks more without the warranty)

“No. I don’t see. That’s not right. You can’t offer me something supposedly valuable, like a warranty, and then charge me more when I remove the warranty. Excuse my language, but that’s…”

…And…you’ll have to imagine the classy and stylish way in which I expressed displeasure to emphasize my point.

“Well, let me see here, ok, I suppose I could replace the three tires – without the warranty – for about $315.” (or about $5 less per tire without the warranty.)

More tire warranty details

Now, my finance-guy curiosity took over. I wanted to know more details about this supposedly good-deal warranty.

“If my new tire needs replacement while I’m still under warranty, would it be free?”

“Not free, but it will only cost you only $20 to replace.”

“If I have a warranty with you guys, can I get the tire replaced anywhere else?”

“No, we’d be the only ones to honor the warranty.”

“Ah, I get it, so you want me to pay part of the cost today of the next tire needing replacement, and I have to do the work at your shop, rather than anywhere else where I happen to get a flat or have a problem. So really the point of the warranty is to get me to come back only to your shop?”

“Well, not exactly, but see they do want us to sell these warranties…”

“Forget it. Don’t do three tires. Just replace the one tire, no warranty.” And then I told him the problem of misleading customers – especially gullible and unhandy ones like me – is that customers who lose trust in their service-provider generally don’t come back. That’s a separate issue from a warranty, of course, and a fundamental rule of business, but an important point nevertheless. I will do my darndest to avoid going back there.

Rewinding for a moment, however, to review the personal finance issue of warranties: For most electronic devices and most household durables, most people most of the time would do better to forgo paying for a warranty. It’s a kind of excess insurance-policy that you should avoid, unless special circumstances apply.

Another warranty story

What even is this thing?

I remember purchasing in the early ‘00s a totally awesome stereo-component: A 100-CD changer (roughly the size of an overseas shipping/railcar container, if memory serves me correctly). The Best Buy salesman really, really, really wanted me to get that warranty. I found it odd that he focused on the high likelihood of my totally awesome 100-CD changer breaking within the next year, as I had not even left the store yet. I declined. I’m happy about that choice, even though of course it broke within three years, because by then Apple had begun to render moot all legacy music devices, with the iPod.

Michael: Hi, my name is Michael and I used to be a banker.

Wendy: Hi, Michael. Wendy Kowalik, I founded Predico Partners. We’re a financial consulting firm. I started my career with an insurance company and sold insurance for the same 17 years that we managed money.

You came from a firm that did quite a bit of insurance. As we’ve spoken in the past, that’s not always how insurance is sold. Probably the majority of the time it is some kind of weird blend between a supposed investment in addition to a risk transfer. You’ve done it. I haven’t sold insurance or been involved in that, but what do you think about my ideas?

Wendy: “It depends,” is the worst answer, but globally you’re on the right track. You’re exactly right. And what I’ll tell you is if someone is walking through the door saying you should use it as an investment vehicle, you’re probably on the wrong track.

Interview with Wendy Kowalik of Predico Partners

Very seldom will you find that working well. The insurance industry’s argument on that side of it is it’s disciplined savings. It grows tax deferred. Well, so does your 401(k). Make sure you’re making that out first. That’s the first place you need to be saving, on that side.

The other argument is you can go in and take a loan out tax-free. Very true statement except for the fact that if the policy doesn’t last for the long term, then you pay taxes on every dollar you took out. That’s where it’s all the details within the insurance that many times make them not work as they were originally sold.

Yes, for globally, I would tell everybody that there’s only two reasons to purchase insurance.

To protect an income source if you’ve got a spouse that’s working and you need their income to make your monthly budget. You need to protect that.

The second side of the table is if you have estate taxes. You can use insurance to basically pay a lower dollar amount for you estate taxes. Outside of those two pieces of the puzzle, I don’t really see a huge need for life insurance.

Michael: The second part, the estate taxes, is going to be much more of a high net-worth problem than an ordinary investor problem. We’re talking up at the top 5%, 1% or .01%. It gets more plausible that they’re going to be able to have a tax savings and estate planning through insurance, right?

Wendy: Right, sitting here today, an estate over 10-million dollars for a married couple and an estate over 5-million dollars for a single individual.

Michael: What I tell people, and most of my ordinary acquaintances are not in that category, I just say “You need to focus on self-insuring” through trying to invest your money so that when it comes time where you can no longer work, or you choose to not work, you’re not worried about an income stream, and you’ve self-insured though actual investments, rather than this expensive version, which is paying an insurance company to be this mix of asset protection, asset building, and income replacement.

Wendy: That’s exactly right. You should have two different pieces of the puzzle. You should have term insurance if you’re protecting an income stream for a period of time. And use your savings separate from that.

Michael: Right. I just don’t trust that most insurance sales people in the industry is parsing that out for people to say “If you’re got a risk of loss of income, you need term for the period of time in which you’re worried about that, and then use the savings to put that in the market.”

This is what I always tell people — without knowing — having not worked in the insurance industry that just seems to be the right thing.

Wendy: Right.

Michael: For most people, with obvious exceptions. If you’ve got a ten-million-dollar estate it’s a whole different situation and you probably need different set of advice, which I’m not qualified to give. We’ve got term insurance in my family related to how old my kids are, when they are going to be no longer under my protection, and can fend for themselves in a sense. But it’s super-duper cheap to get that, for a certain number of years, and a certain amount of money, not a huge amount, but sufficient to not leave them in a lurch.

Wendy: That’s the biggest struggle on the insurance side, is figuring out what that number is.

Michael: Tight.Certainly back to your two reasons to have insurance. One is replacing income stream, and the second is estate planning and possible tax reduction. The folks for whom that second part is relevant, estate planning — the first part seems to me to be totally irrelevant. You’re either in one or the other. You’re probably not in both because if you have ten million somewhere in assets, you don’t really need to ensure further a loss of income stream. You’re probably going to be able to feed and clothe yourself now. Or am I not thinking about that right?

Wendy: Yes, no you’re right. Could they self-insure? Absolutely. What you’ll find a lot of times, though, is you’ve got people in that situation that have purchased property or they’ve got a family-owned business that makes that up. Then it becomes a liquidity event. Do I really want to unload Pepsi to pay the estate taxes? Or do I want to have to sell at that point or do I want to buy some time? It still may not be this massive convoluted structure, but I may be that I want to purchase an amount to give me time to figure out what I want to do with the asset.

On Budgeting, and Getting Rich Slow

Michael: So, any other topics you think we should get onto the podcast?

Wendy: The other thing you put on there was budgeting. How do people come up with a budget.

Michael: Oh yeah, let’s talk about that.

Wendy: I do think that is a big piece of the puzzle. The number-one side we run through is no matter how much money you have, you’ve got to understand how much you spend that’s fixed expenses and will not change, no matter what you do right now, unless you actually make radical lifestyle changes, such as selling your home, changing your cars, that type of thing. Or is it just discretionary, and to me that is such a big piece of the puzzle, is understanding exactly what you’ve got that’s fixed, what you’ve got that’s discretionary, because that’s the only way you can determine can I really cut back and make some changes, and start saving more, because we don’t need to eat out as much or go do this as much. Or is it that we’ve extended beyond what we can truly afford either in a home, or cars, or things such as that, and we need to change lifestyles more dramatically than just not going out to eat on Friday nights.

Michael: I’ve taken to saying to people, my friends, or peers, or people that ask my advice that nobody has any extra money at the end of the month. Whether you make 350,000 bucks a year or you make 35,000 bucks a year. There’s no extra money. Your lifestyle builds to whatever you’ve gotten comfortable with, and I tell people you basically have to trick yourself into creating little streams of savings and investments. This isn’t true for everybody and to bring up my nine-year-old daughter, she’s basically a hoarder. Her babysitter basically said early on she’s going to be on the hoarder TV show. She never throws anything away, so if you give her some money — there’s a few people like that, who save all their pennies, nuts, and squirrel them away.

But for most people there is no money. There’s no salary that’s enough to make sure you have extra money. If you move up from the Honda to the Audi, then you have to get the Jaguar. You’re still just buying a car, but somehow if you make 350,000 dollars. It’s not hard to go bankrupt on 400,000 dollars a year. Mike Tyson went bankrupt after earning 300-million dollars in his life. There isn’t any real money…[that’s sufficient.] You have to figure out tricks and ways to get the excesses.

Then you have these weird stories of the person who never made more than 40,000 dollars in their life, and they have huge investment accounts, relatively speaking, at the end of their life. They were able to do it.

Wendy: My favorite was we had a client referred to us in my former firm. That was exactly it. He had been a civil service employee, never made over 40,000 dollars for many years, and finally topped out at 65,000 dollars. She was in her early 80s, late 70s, and her investment account was worth 15 million dollars. She purchased with every extra few dollars, at the end of the month, she’d say this is what we’re going to set aside for savings. He would purchase bank stocks because he decided that it paid a little bit in dividends, and that was what he followed. He did financial stocks and he purchased six stocks, followed them. He never once sold a dollar of them. He never cashed them in for anything, and just added to those same six. That’s what it grew to. It was absolutely incredible.

Stocks for the long run

Michael: That is incredible. If you have 60 years of doing that, there’s the compound returns of equity exposure to a couple of good stocks or six different bank stocks over a certain period of time. That’s incredible, yet mathematically very plausible when you look at it, how much you could put away, and if you let it ride for 40 to 60 years. It’s totally doable. It doesn’t feel like that until holy cow, 30 years later suddenly it’s grown.

Wendy: Right.

Michael: I feel like that message doesn’t get out to enough people or it gets out when you turn 62 and you’re like huh, so I should have been starting 40 years ago? Now you tell me?

Wendy: That’s right. And I think it’s hard to withstand, and I think what many people strive for is they keep trying to find a better way to get to the investment returns. They’re looking for that — there’s some trick to get there. A lot of it is just hard work and discipline.

Michael: It’s hard to make the affirmative choice to do it, but if just sneakily happens by default you can build up wealth, I think.

Wendy: I completely agree. We tell everybody if you take it and send it to a brokerage account that’s not in your bank, leave it in cash for 90 days, that way you know can you really make it without that money, without having to go back and take it back. You normally won’t call the brokerage account and ask them to send you a check. You really do need it if you’re doing that. So then at the end of 90 days put it to work. See if you can increase it and put away more in the next pay period.

Michael: I think that method works. GET RICH SLOW. It’s hard to get rich quick.

Wendy: Very true.

Michael: Thank you for discussing all these things. I think there’s lots of interesting ideas here that people should be paying attention to.

Occasionally I worry because my house backs right up to the San Antonio River. Fortunately, my yard and house are outside the boundaries considered to have a 1 percent chance of flooding per year, the so-called “100-year flood plain.” So up until now I’ve never had flood insurance, nor have I been required to have it by my bank.

Occasionally I worry because my house backs right up to the San Antonio River. Fortunately, my yard and house are outside the boundaries considered to have a 1 percent chance of flooding per year, the so-called “100-year flood plain.” So up until now I’ve never had flood insurance, nor have I been required to have it by my bank. Of course, a common-sense reaction to that news is to wonder whether things have changed, possibly due to climate change, such that previous rainfall data informing the 100-year flood plain is no longer accurate in 2017.

Of course, a common-sense reaction to that news is to wonder whether things have changed, possibly due to climate change, such that previous rainfall data informing the 100-year flood plain is no longer accurate in 2017.