My wife and I recently renewed our home equity line of credit 1 with our bank.

HELOCs are as good as Nutella

When the notary at my bank had us in the room for 30 minutes busily initialing and signing many dozens of pages per a minute – pausing approximately 0.7 seconds per page – my mind began to explore the absurdity of it all.

Am I supposed to have read each page? Does this signature here actually compel my compliance with everything on the page? Really?

Hidden in the fine print of these documents, the bank probably slipped “And, henceforth I, Michael Taylor, by my signature below, do solemnly agree to wear a rubber ducky costume to work every day. Also I agree that my banker is the super-duper coolest person ever” and there’s no way I would have caught that in the fine print.

And yet, I signed. My cursive name must mean I agreed to it all. Yes, I agreed to whatever they wrote down there!

I’ve worked on many sides of the mortgage business for many years now, so I understand the point of this paperwork. To wit, the papers have zero to do with serving borrowers and 100 percent to do with creating a CYA paper trail – a paper trail that serves the lender, not me, if things go badly.

I get that.

I wish I didn’t have to participate in this charade of me ‘agreeing’ to something which I am unwilling to read thoroughly, that the bank knows I am not reading, and yet the bank also knows they can take me to court and win by arguing successfully that I agreed to all their terms, if I fail to comply with said terms.

We’ve all had that experience of mindlessly signing and initialing page after page of unread documents.

What do all those initials and signatures, the unreadable documentation, plus all of the regulatory morass that underpins it all, stand in the place of? Human judgment.

Written rules substitute for our ability, or the bank’s ability, to make individual decisions specific to a situation.

But here’s the weird thing that I returned to in the midst of signing my name dozens of times in front of my notary: this dehumanization of the decision process is a good thing. This automated decision-making process works to our advantage.

We think we want our bankers to be able to use their judgment. But we really don’t.

We think we would all be better off if we had a banker, like George Bailey from It’s a Wonderful Life, who could look us in the eye and say: “Here’s a loan, Taylors, I trust you. Don’t worry about all that boring paperwork, your handshake is enough.”

We’d skip out of the bank buoyed by Banker Bailey’s great judgment and trust in our solid character.

To the extent that George Bailey’s world ever existed (it may have, or it may not have) I don’t think that was a better world for borrowers for at least for one important reason: Borrowing costs.

All the impersonal unreadable language assists in making mortgage loans like my HELOC (Home Equity Line of Credit, but you know that) one of the cheapest ways to borrow on this planet.

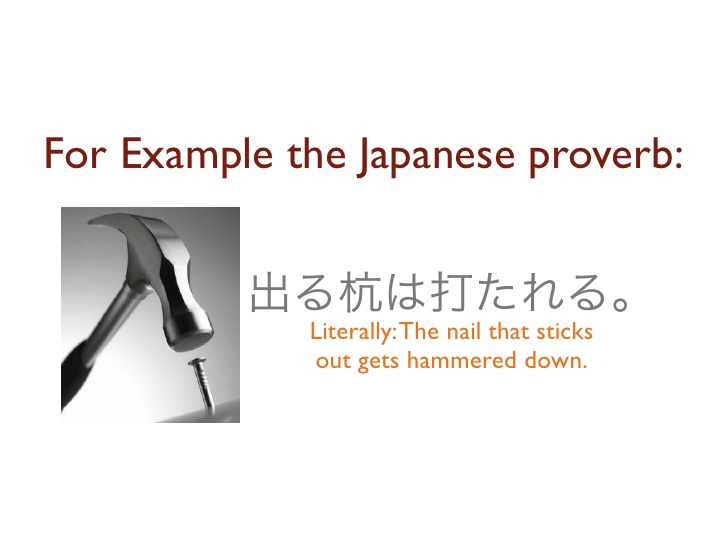

Banks do not really underwrite mortgage loans anymore. Instead, they originate mortgages for a fee, and then feed the mortgage bond investor system with similarly situated mortgage loans. To feed that system, every single mortgage or HELOC must conform precisely to the standards of bond investors.

The mortgage bond market attracts a billion of dollars of investment capital on a daily basis 2 to fund home ownership. That money invested in mortgages gets offered at rock bottom interest rates precisely because of the uniformity enforced inside a mortgage bond.

Any non-conformity in the mortgage underwriting process makes the loan ineligible for inclusion in a mortgage bond structure. “The nail that sticks out must be hammered down,” as the Japanese cliche goes.

With a signature missing here or an initial missing there, the bond structuring companies would kick our loan out, and the bank would get stuck with an inefficient product on their books, which is the last thing they want.

I’ve never worked in the Wal-Mart supply chain, but I’ve read about the incredibly strict standards by which suppliers must meet packaging specifications to get their stuff into Wal-Mart stores. Those inflexible standards help produce the rock-bottom Wal-Mart prices. Human judgment or flexibility with the rules would raise prices in Wal-Mart, just as it would for my HELOC.

All things must be automated

When my wife and I signed our HELOC recently, we were the product being packaged for sale into the mortgage bond market. We got a great interest rate, and it only required an assembly-line approach to signing everything.

By the way, home equity lines of credit are the bomb. Tangential to the following discussion, I believe home equity lines of credit – despite causing widespread financial destruction in 2008 – are the best invention since Nutella on toast. But that’s a discussion for another time and place. ↩

How do I get that number, you ask? Great question. The US mortgage bond market added up to $8.7 Trillion in mortgage bonds at the end of 2014. At a weighted average coupon of 4.5% (I made that up but it feels average-y at this point) that would generate about a billion dollars in interest per day. Factoring in principal repayments the US mortgage bond market has to attract more than a billion dollars every day just to stay the same size. ↩

I mean, don’t get me wrong, home ownership is awesome for some – even for many – but I don’t think we talk enough about whether it’s such an unimpeachable good thing that it deserves quite so many subsidies.

We traditionally have subsidized home ownership in myriad ways.

A quasi-government guaranty (followed by a $800 Billion assumption of liabilities in 2008) of mortgage guarantors Fannie Mae and Freddie Mac.

Federal FHA/VA loan programs for first-time home buyers and veterans to encourage home-purchasing with as little as a 3% down payment.

Mortgage-interest tax deduction ($200 Billion in foregone tax revenue).

And yet, the benefits and effects of such subsidies are questionable

We do not have an appreciably higher percentage of home-owners in the US vs. other countries that lack such subsidies

3% to 10% down-payment mortgages default more frequently (50% more frequently) than 20% down-payment mortgages, serving both home-buyer and bank poorly.

Americans tend to react to the mortgage interest subsidy by buying bigger homes, rather than saving the money.

The mortgage interest tax deduction is regressive, in the sense that it primarily benefits folks with incomes higher than $100,000, and a household with a larger home and mortgage benefits more than a household with a more modest home and mortgage.

Houses, which often constitute a high portion of household net worth, are a very illiquid investment.

Housing, as a sector, tends to add volatility to the economic cycle – making booms more manic and busts more depressive.

Surowiecki summarizes nicely: Given the extraordinary subsidies aimed at the sector – compared to other worthy areas of subsidy – is it all worth it?

I’m not going to jump up and down and declare that this latest negotiated relaxation of federal mortgage standards means we’re back to the pre-Crisis madness.

On the other hand, it appears that all the tough policy talk – about shoring up lending standards, winding down Fannie and Freddie, requiring strict 20% down payments for new mortgages, and requiring mortgage securitization banks to retain at least 5% of the bonds they make to have ‘skin in the game’ – just went flying out the window yesterday.

As I mentioned recently, HUD is very focused on increasing lending, even if it means pushing banks back into the subprime space. One problem that HUD and the Federal Housing Finance Agency face is that mortgage standards appear high and tight for anyone with less than perfect credit or the traditional hefty 20% down payments.

In addition, mortgage originator and aggregator banks are scared to death of any misstep in the underwriting process, because that allows Fannie and Freddie to kick the mortgage back onto the mortgage bank’s balance sheet. Mis-steps, even tiny ones, also expose banks to the kinds of government lawsuits for which they’ve paid many billions of dollars in recent years, in what I basically believe to be “settle and quickly move on” situations for banks, rather than outright winnable cases for the government (but that’s another long story.)

1. A relaxation of the 20% down payment requirement for conforming loans, to as low as 3% down for certain qualifying buyers. Details to follow in coming weeks.

2. A new set of easier requirements that make it less likely Fannie or Freddie will kick back non-underwriting compliant loans to underwriting banks.

Separately, the FHFA indicated that banks will not have to carry 5% of the risk of mortgage bonds, if borrowers did not provide a 20% down payments. Banks hated that rule, and they got their wish.

These steps will clearly please both mortgage banks and borrowers in the short run.

In the medium to long run, we’ve definitely taken a giant leap toward riskier mortgage lending.

John Carney at the WSJ says

The rule [regarding banks holding 5% of mortgage securities themselves] isn’t just a small step back for mortgages, it is a giant leap backward for the entire financial system.

I can’t remember any speech Mayor Julian Castro ever made to which I paid much attention.

Shouldn’t be pushing Subprime Mortgages

Decade of Downtown?

Meh. I had just moved to San Antonio’s downtown and I didn’t have any context. Democratic National Convention?

I missed it because I was recovering that day from a blowout wedding in the Yucatan.

But last Tuesday’s speech introducing his priorities at HUD?

Did somebody say mortgage and housing policy?

Now you’re in my wheelhouse, Secretary Castro. As a former mortgage bond salesman, I’ve got some strong opinions about federal mortgage and housing policy.

First, the bad:

HUD Secretary Castro named increasing access to mortgages for borrowers with low credit scores a top priority of HUD.

I cringed.

Home Ownership Rate Comparison, 2011

Do you know another name for increasing access to mortgages for borrowers with low credit scores?

That’s called sub-prime mortgage lending.

Restricting mortgage loans from people with bad credit scores is not housing discrimination or lending discrimination.

Rather, restricting mortgage loans from people with bad credit is prudent practice for both borrowers and lenders.

People with low credit scores are people who have not previously paid their bills on time. That’s just the definition of bad credit.

People can fix their bad credit over time, and government can play a positive role in encouraging financial education, for example, or by regulating credit reporting and consumer protections.

But most importantly, people with bad credit are people who should probably wait a bit longer before taking on the largest loan generally available to them – a home mortgage.

Encouraging more people with low credit scores to take out mortgages is a bit like breaking out the champagne at the AA meeting to celebrate a month of sobriety. Bad things can and will follow.

Look, I get it, when you’re a hammer, everything looks like a nail. And when you’re HUD Secretary, more home ownership is always better.

I guess my larger problem with Castro’s stated HUD priority is that home ownership isn’t always better.

It’s fine with me if banks or private lenders want to take extraordinary risks and lend to people who won’t pay them back in the future, but I really don’t think the federal government should be encouraging more of that activity.

Back in the pre 2008-Crisis days, mortgage giant Fannie Mae used to run constant radio advertisements proudly proclaiming “We’re In The American Dream Business!” and at the time, who could argue with them?

Home ownership traditionally fell somewhere between Motherhood,

Baseball, and Apple Pie on the spectrum of unimpeachable good things.

Well, since 2008 we’ve gotten wiser:

Apple pie causes obesity.

Baseball is full of PED cheaters.

And Mothers are the direct catalyst for about 50 percent of all of the adults who seek psychotherapy. (Since you’re curious, scientific studies show that Fathers are responsible for the next 25 percent of all therapy-seekers, and scary, scary clowns make up the final 25 percent. In my case, it was the clowns.)

Housing as an investment tool

And home ownership? Well, it’s both an incredibly powerful tool for building middle class wealth, as well as the cause of the worst financial crisis since the Great Depression.

While I would advocate home ownership for many people, pushing home ownership to excess – like Apple Pie, Baseball, and Motherhood – also leads to terrible outcomes.

We don’t need more subprime lending, and we don’t need government agencies encouraging more subprime lending.

Speaking of Fannie Mae and the American Dream Business, I really liked a different part of Castro’s speech.

The bill would set broad guidelines for mortgage lending and securitization in the future. Most importantly – from my perspective – the bill would kill former mortgage monstrosities Fannie Mae and Freddie Mac, which themselves currently languish indefinitely in conservatorship purgatory.

Why were they monstrosities?

To me, the definition of a monstrosity is a company that enriches private investors and its executives, all the while enjoying a government guaranty, and therefore represents a massive public subsidy of private enrichment.

And yes, I understand that all of Wall Street briefly earned monstrosity status by that definition in 2008.

But the difference between Wall Street and the mortgage monstrosities Fannie Mae and Freddie Mac is that the latter companies always had this monstrosity status, from their very inception.

Technically, they were described as “Government-sponsored entities” and government officials occasionally tried to point out that their debt was not explicitly guaranteed by the Federal government.

In practice, Fannie and Freddie bond investors always assumed that when push came to shove Fannie and Freddie would be bailed out by the Federal government. Of course, push did come to shove in 2008, and bond investors were proved right.

I don’t know. That just seems like a lot of money to be paid to run a government sponsored (and guaranteed) entity. There’s no flies on that pair of Dickensian-named CEOs, Raines and Mudd, despite SEC investigations of both of them for securities and accounting fraud, and a paltry settlement with Raines.

The Senate bill supported by Castro would not eliminate federal government subsidies for the housing and mortgage markets, but it would greatly reduce the future taxpayer subsidies for the enrichment of quasi-private monstrosity entities like Fannie Mae and Freddie Mac, and their investors and executives.

The bill would replace them with a much more narrowly-functioning government entity – modeled on the banking deposit insurance agency FDIC – to provide mortgage insurance and a taxpayer-protection fund against mortgage losses.

That would lead to much less private enrichment with a public subsidy.

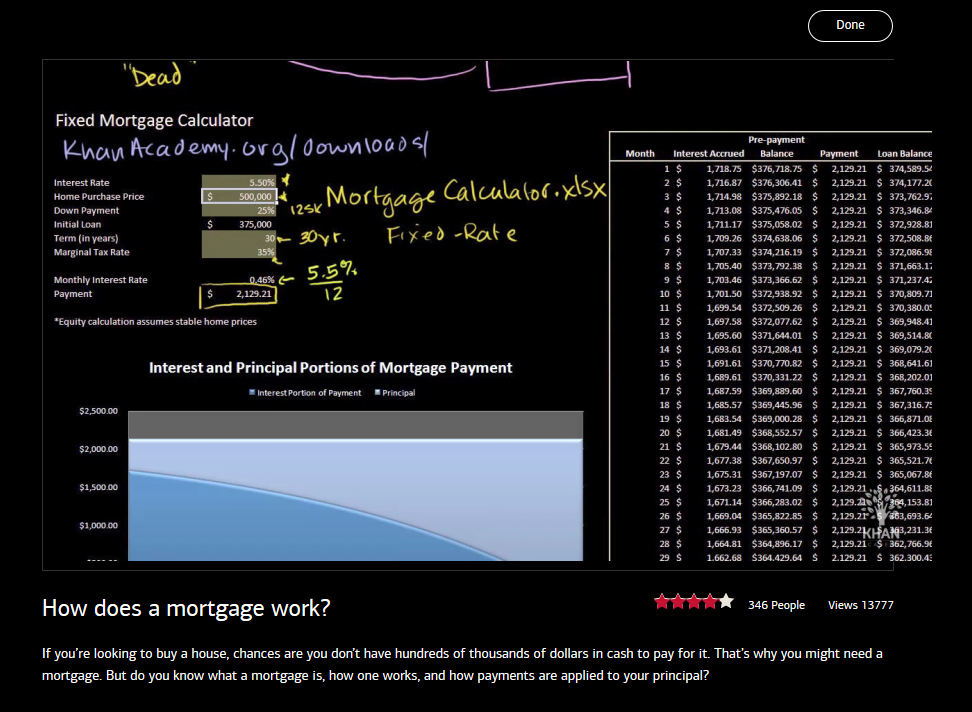

I was scouring the interwebs lately for a financial education project I’m doing and I came across Sal Khan’s joint educational venture with Bank of America called www.bettermoneyhabits.com

There’s some very good stuff there, but I was drawn in particular to his “How does a mortgage work” video.

I happen to have this weird belief that everybody who takes out a mortgage (or car loan, or business loan, whatever) should be required – as a pre-condition of their borrowing the money – to build their own ‘loan spreadsheet,’ in order to learn the nuts and bolts of how it works. If you’ve programmed it into a spreadsheet, and calculated how the principal and interest gets paid every month, and how it amortizes, you gain insight into interest rates and cash flows that you can’t get any other way.

Anyway, I know this weird belief will not be implemented by any lender anytime soon, so the next best thing is to introduce people to pre-made spreadsheets on mortgages, and to walk them through the component parts. As a master teacher, Sal Khan is suited to do this very well. There are a ton of pre-made mortgage spreadsheet available online, but Khan Academy’s is as good as any.

Khan Academy makes available a pre-made spreadsheet under the “Fixed Mortgage Calculator” link here, that lets you input amounts, and fixed interest rates and even tax rates to calculate interest savings.

Also, I had no idea that Mortgage comes from Old French meaning Dead-Contract, since presumably the contract or title to the real estate gets killed off over time, eventually releasing the borrower from the lien. Fun!

Ok friends, are you ready? I’m about to piss you off.

Contrary to the dominant journalistic narrative of the 2008 Crisis – that greedy bankers and their Wall Street enablers tricked the poor and gullible into predatory loans on their homes which led to foreclosures and economic misery – I think borrowers mostly caused the mortgage crisis.

Underwater house. Who is to blame?

Obviously this is a deeply unpopular thing to say, and cuts against the grain of “little guy = good” and “big bank = bad,” and it appears at first blush that I’m blaming the victim. I sympathize with homeowners who lost their jobs and then possibly their homes and clearly many were victims of forces beyond their control. But I’m still gonna piss you off.

Borrower as “innocent victim” myth

I really just mean to point out that a whole lot of borrowers were not innocent victims, but rather perpetrators of mortgage fraud. Many of these folks were investors, speculators, flippers, and just Hail-Mary passers hoping short-term real estate inflation could cover their terrible financial positions.

I mean to call out the people who knew they didn’t really have a chance at paying back their loans under ordinary circumstances, except maybe extraordinary price appreciation. I mean people who got “no income, no asset” loans knowing that income and asset disclosure would tank their chance to borrow a lot of money. I mean people who, with almost no money down, bought an option to ride the upside of real estate appreciation but who risked no real equity when the market went sideways and then south.

I don’t believe I’m an extremist in this view, I am a realist.

Bankers getting stoopid

Yes, mortgage underwriting standards slipped from “loose” to “stoopid” somewhere between 2004 and 2007, with ARMS, sub-prime loans, interest-only loans, and liar-loans expanding from niche products for niche situations to dominant products crowding out sensible mortgage loans, eventually clogging up the sewage pipelines of global finance. One of my earliest podcast interviews for this site was with a mortgage underwriter who got out of the business just as the ridiculousness started to take over.

But despite this, and contrary to the dominant journalistic narrative, banks do not make money when they lend money to people who will not, or cannot, pay them back. Lending to a borrower who cannot pay back the loan is not a profitable strategy. I’ve never met a banker who wanted to take back someone’s home. It’s a ticket straight to financial destruction for the bank.[1]

Yes, bankers are profit-oriented, and yes they got briefly stoopid, but banks generally get only a few years to make these kinds of terrible underwriting and financial modeling decisions, after which, the inexorable gravity of finance pulls them down, punishes them, and makes them pay.[2]

Borrowers too acted from a combination of greed and stupidity, taking out loans they should never have taken.

Homeownership is not a fundamental right of citizenship. It’s a choice that’s right for some people, but financially catastrophic for others, because home ownership is risky. A mortgage contract confers opportunity, but also demands responsibility.

And yes, I get it, it’s harder to blame the individual borrower who lost her job, her credit and then her home, than it is to blame the overpaid financiers and their banking institutions. Obviously the underwater and foreclosed borrower is a far more sympathetic character than the slick mortgage bond investor or the bank. But just because we feel for the little guy or gal doesn’t mean we should misunderstand shared responsibility for the mortgage crisis of 2008.

I understand better than most the terrible mistakes and greed of Wall Street. I was there, and I’ve written about some of it here. I’ll be the first to say I think the ongoing coddling of Wall Street and unsolved TBTF problem remains a black mark on the Obama administration. But if we don’t acknowledge the shared responsibility of predatory borrowers then we don’t learn the right lessons from the mortgage crisis.

Although I disagree with much of his politics, Edward Conard in his Unintended Consequences debunks – better than anything else I’ve read – the flawed journalistic narrative on the mortgage crisis of 2008.

I know I’m going to piss people off when I write this, because it’s impolite to lay responsibility on the individual homeowner who had the most to lose.

Selling mortgages from bank to bank

What about the fact that mortgages get sold and reassigned to banks that didn’t even underwrite the loans?

Recently a neighbor told me a story – with a straight face – that an acquaintance of hers received notice from a bank of imminent foreclosure on her house. The acquaintance claimed to have made all of her mortgage payments, but the mortgage had been sold to another bank, which hadn’t received her monthly payments. My neighbor was shocked about the mortgage having been sold to another bank, and wholly believed her friend would lose her home.

I remained outwardly sympathetic and pleasant, but let me tell you what I was really thinking.

To dispose of the last point first, the fact that the mortgage was sold to another bank is irrelevant. You know why? Because practically every single mortgage in this country is sold from one bank to another.

Unless you got a mortgage from one of four banks – Wells Fargo, Bank of America, Citibank, or JP Morgan Chase – you can be absolutely certain your mortgage will either be sold or serviced by a different bank.[3] Look at your mortgage statements. Is that the bank that gave you your mortgage? Probably not.

But but but – I hear the objections to the original point – what about all those mortgage bank robo-signers in the foreclosure mills? What about foreclosure mistakes, in which people lose their homes due to bank error?

Ah, yes, the myth of foreclosure mistakes.

The myth of mistaken foreclosure

I just do not believe in the myth of mistaken foreclosure.

I say this with confidence for a couple of reasons.

Through my business I’ve invested in many mortgages myself, a great number of which became delinquent.[4]

It takes between 6 months and a few years to enforce unpaid debts. Thousands of dollars in attorney fees are followed by months of notices, certified mail, and disclosures to homeowners in arrears. Unlike a Hobbesian life, mortgage foreclosure is nasty, brutish, and long. If the lender pressing foreclosure misses any steps along the way, you pass directly to Go, do not collect $200, and the foreclosure process can be held up indefinitely.

Look, we live in an extremely litigious society. There are thousands of consumer rights’ lawyers ready to take on a big juicy target like a bank for mistakenly foreclosing on a homeowner who has faithfully made mortgage payments but who lost his home due to bank error. Any homeowner who got mistakenly foreclosed upon by a bank is not a homeless loser but holds a golden ticket to financial paradise.

Borrowers mistakenly foreclosed upon hold a Golden Ticket

A mistaken foreclosure is a Golden Ticket for the homeowner?

Has this ex-banker forgotten his meds?

No.

If Bankers-Anonymous readers can refer me to a homeowner tricked out of her home, or mistakenly foreclosed upon who remained current on her mortgage,[5] I will find a lawyer who will win millions of dollars for that homeowner from the bank. If you can find me more than one instance nationwide – let’s just say a few dozen – we will all retire just on the referral fees to the class action lawyers alone.

How much can we make the banks pay? $100 million? $200 million? Maybe more. Some percentage of that would be fine by me.

But it’s never going to happen, because it’s a big fat myth.

Mortgage settlements with big banks

But wait, what about the hundreds of millions of dollars in penalties Wall Street banks have paid in the past 5 years to attorneys general for mortgage underwriting errors or fraud? Doesn’t that prove Wall Street and the mortgage banks were cheating and predatory?

No. It proves only that securities firms cannot afford to get crossways with securities regulators. Not a single mortgage case filed by the government against the big banks in the past 5 years has ever gone to trial.

The banks’ attorneys immediately ask for a settlement, put aside a big chunk of money, and try to move on.

Being sued by the government for securities fraud is such a business-quashing situation that no bank can remain there for long. Their lawyers just reach for the corporate wallet and ask the regulators what it’s going to take, and then they move on.

Conclusion

I’m not trying to be the mean jerk here by blaming the borrowers. Clearly homeowners suffered, and they suffered individually more than the bankers. But we need a clearer-headed analysis of the cause of the mortgage crisis – or at least a more balanced view of where to place the blame.[6]

I think we’ve bought into an imbalanced journalistic narrative, and we draw the wrong lessons for the future as a result.

Postscript to the Conclusion

On this same issue of ‘who to blame?’ the mortgage crisis strongly resembles the internet crash of 2000 and then-Attorney General Spitzer’s campaign to blame internet analysts. As always, Michael Lewis said it best, in this classic New York Times Magazine article. If you choose the politically convenient target – mean, nasty, banks and their forked-tongue research analysts – rather than the fact that investors are greedy, working with imperfect information, and should be held responsible for their own investment decisions, then you learn the wrong lessons. And you end up with a bullying hypocrite for a New York Governor, among other consequences.[7]

In the case of the mortgage crisis, exclusively blaming the banks for loose lending standards leads to, among other things:

Tightened credit restrictions, especially for the poor

Absolving homeowners and borrowers for the consequences of their own financial decisions

Punishing individuals who actually stayed current on their underwater mortgages instead of walking away

So let’s consider the whole picture of responsibility, however unpalatable it may seem.

[1] When they don’t get paid back, banks have to start a foreclosure process, which is long, costly, and uncertain. Then when they do obtain the property, more often than not the bank sells it for a loss. It’s a terrible situation. Banks don’t like to own properties. They want Tuppence.

[2] And then they call up daddy Paulson, and say ‘Daddy, start writing checks!’ Yes, I realize banks got unfairly bailed out. That too drives me nuts. But I’m talking right now about the causes of the crisis, not the consequences.

[4] In a related piece of news, I’m no longer a hedge fund manager. Rather, I’m stacking mad chips as a blogger.

[5] “Remained current on her mortgage” is the key clause of this whole thing. I define a foreclosure mistake as a situation in which the homeowner who actually paid the mortgage, but lost the home. Yes, lots of people lost their home after not paying on the mortgage, and that’s tragic all around. But that’s not the bank taking advantage of people, that’s the bank following through on its signed, written contract, which contract has been thrown into default for non-payment.

[6] On this same issue of ‘who to blame?’ the mortgage crisis strongly resembles the internet crash of 2000 and then-Attorney General Spitzer’s campaign to blame internet analysts. As always, Michael Lewis said it best, in this classic New York Times Magazine article. If you choose the politically convenient target – mean banks and their forked tongue research analysts – rather than the fact that investors are greedy and working with imperfect information and should be held responsible for their own investment decisions, then you learn the wrong lessons. And you end up with a bullying hypocrite for a New York Governor, among other consequences.

[7] And then after he’s exposed for what he is, you get him back, as Comptroller of New York City.

Written rules substitute for our ability, or the bank’s ability, to make individual decisions specific to a situation.

Written rules substitute for our ability, or the bank’s ability, to make individual decisions specific to a situation.