The New York Times has a great Op-Ed today about the Expected Family Contribution (EFC) calculation, which I recently encouraged all parents with college-bound kids to check out.

The New York Times has a great Op-Ed today about the Expected Family Contribution (EFC) calculation, which I recently encouraged all parents with college-bound kids to check out.

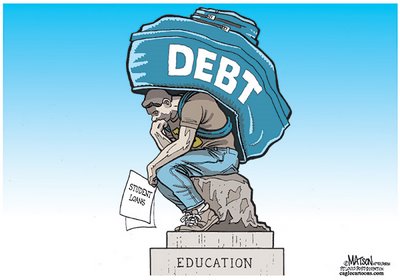

My main take-away from looking at my own family’s EFC estimate on the College Board site was jaw-dropping because there is Just.No.Way.

Where would an ordinary (non-wealthy) family be able to come up with that kind of cash to pay for college? Every year? For just one kid?

The answer, of course, is that very few families can come up with that kind of money, so students and their families take out extraordinarily large student loans.

The New York Times Op-Ed explains the pernicious effect of the federal government-calculated EFC. When all families receive a ‘government number’ it sets an artificially high floor for college tuition prices.

The Op-Ed also explains why some high-priced private universities may offer cheaper educational access to students than public universities, via the private universities’ generous financial aid packages.

The article also helpfully reviews some of the not-applicable, and not-generous, federal grant money available to families.

Finally, the Op-Ed recommends that Congress drastically cut the EFC by 75%, to reflect the fact that tuition cost hikes since 1980 have drastically outstripped inflation.

This proposal will not go over well in higher education circles, to say the least. Fortunately for colleges and universities, according to the article, they have spent a half-billion dollars lobbying Congress in the past 5 years, the eighth-highest special interest category.

Please see related posts:

College Savings and compound interest

Interview with College Advisor Part I – The insanely rising cost of college

Interview with College Advisor Part II – is the 4-year college financial model broken?

One source of college costs: administrators!

New York Times on funding your 401K Account vs. 529 Account

And another NYTimes follow-up on the confusing issue of FAFSA – determining the expected cost of college.

Post read (8102) times.