My wife and I recently renewed our home equity line of credit 1 with our bank.

HELOCs are as good as Nutella

When the notary at my bank had us in the room for 30 minutes busily initialing and signing many dozens of pages per a minute – pausing approximately 0.7 seconds per page – my mind began to explore the absurdity of it all.

Am I supposed to have read each page? Does this signature here actually compel my compliance with everything on the page? Really?

Hidden in the fine print of these documents, the bank probably slipped “And, henceforth I, Michael Taylor, by my signature below, do solemnly agree to wear a rubber ducky costume to work every day. Also I agree that my banker is the super-duper coolest person ever” and there’s no way I would have caught that in the fine print.

And yet, I signed. My cursive name must mean I agreed to it all. Yes, I agreed to whatever they wrote down there!

I’ve worked on many sides of the mortgage business for many years now, so I understand the point of this paperwork. To wit, the papers have zero to do with serving borrowers and 100 percent to do with creating a CYA paper trail – a paper trail that serves the lender, not me, if things go badly.

I get that.

I wish I didn’t have to participate in this charade of me ‘agreeing’ to something which I am unwilling to read thoroughly, that the bank knows I am not reading, and yet the bank also knows they can take me to court and win by arguing successfully that I agreed to all their terms, if I fail to comply with said terms.

We’ve all had that experience of mindlessly signing and initialing page after page of unread documents.

What do all those initials and signatures, the unreadable documentation, plus all of the regulatory morass that underpins it all, stand in the place of? Human judgment.

Written rules substitute for our ability, or the bank’s ability, to make individual decisions specific to a situation.

But here’s the weird thing that I returned to in the midst of signing my name dozens of times in front of my notary: this dehumanization of the decision process is a good thing. This automated decision-making process works to our advantage.

We think we want our bankers to be able to use their judgment. But we really don’t.

We think we would all be better off if we had a banker, like George Bailey from It’s a Wonderful Life, who could look us in the eye and say: “Here’s a loan, Taylors, I trust you. Don’t worry about all that boring paperwork, your handshake is enough.”

We’d skip out of the bank buoyed by Banker Bailey’s great judgment and trust in our solid character.

To the extent that George Bailey’s world ever existed (it may have, or it may not have) I don’t think that was a better world for borrowers for at least for one important reason: Borrowing costs.

All the impersonal unreadable language assists in making mortgage loans like my HELOC (Home Equity Line of Credit, but you know that) one of the cheapest ways to borrow on this planet.

Banks do not really underwrite mortgage loans anymore. Instead, they originate mortgages for a fee, and then feed the mortgage bond investor system with similarly situated mortgage loans. To feed that system, every single mortgage or HELOC must conform precisely to the standards of bond investors.

The mortgage bond market attracts a billion of dollars of investment capital on a daily basis 2 to fund home ownership. That money invested in mortgages gets offered at rock bottom interest rates precisely because of the uniformity enforced inside a mortgage bond.

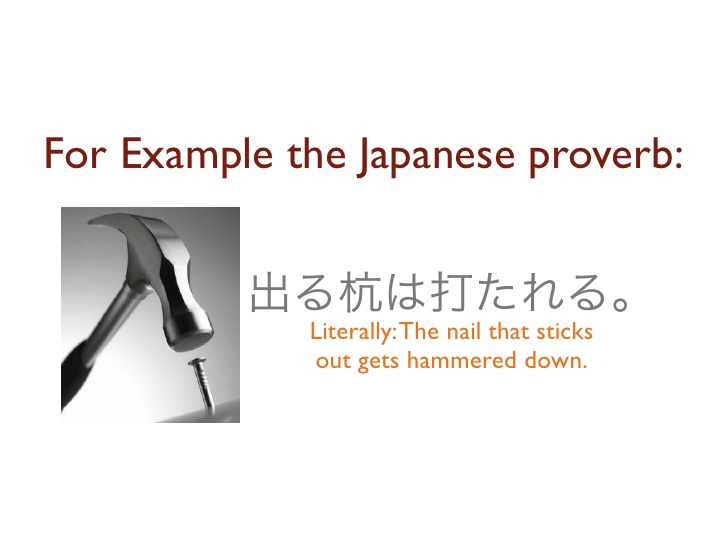

Any non-conformity in the mortgage underwriting process makes the loan ineligible for inclusion in a mortgage bond structure. “The nail that sticks out must be hammered down,” as the Japanese cliche goes.

With a signature missing here or an initial missing there, the bond structuring companies would kick our loan out, and the bank would get stuck with an inefficient product on their books, which is the last thing they want.

I’ve never worked in the Wal-Mart supply chain, but I’ve read about the incredibly strict standards by which suppliers must meet packaging specifications to get their stuff into Wal-Mart stores. Those inflexible standards help produce the rock-bottom Wal-Mart prices. Human judgment or flexibility with the rules would raise prices in Wal-Mart, just as it would for my HELOC.

All things must be automated

When my wife and I signed our HELOC recently, we were the product being packaged for sale into the mortgage bond market. We got a great interest rate, and it only required an assembly-line approach to signing everything.

By the way, home equity lines of credit are the bomb. Tangential to the following discussion, I believe home equity lines of credit – despite causing widespread financial destruction in 2008 – are the best invention since Nutella on toast. But that’s a discussion for another time and place. ↩

How do I get that number, you ask? Great question. The US mortgage bond market added up to $8.7 Trillion in mortgage bonds at the end of 2014. At a weighted average coupon of 4.5% (I made that up but it feels average-y at this point) that would generate about a billion dollars in interest per day. Factoring in principal repayments the US mortgage bond market has to attract more than a billion dollars every day just to stay the same size. ↩

As before, I don’t think it’s enough to say ‘I hate taxes,’ because taxes are a necessary evil. I don’t know about you, but I want to have adequately funded schools, parks, and public safety services.

If I have to pay taxes, however, I want to feel that everybody pays their fair share. The key to making peace with the evil of taxes is fairness. As before, I want to discuss real estate taxes in terms of what is ‘fair to me,’ and what is ‘fair to society.’

Fair to me

I recently toured (for the purposes of buying) a small fraction of a piece of undeveloped land in Southeastern Bexar County. The entire parcel of approximately 95 acres is located (for locals who care) inside the 1604 Loop, between Highways 281 and 37.

(I only looked to buy a fraction of the entire parcel, not the whole thing.)

The entire 95 acres might be worth, I don’t know, $500,000? Maybe more?

Would anyone like to guess what the 2014 taxes were for the 95 acres? Take a moment to guess.

Would you believe $170?

When I picked my jaw up off the floor I phoned the Bexar County Assessor’s office.

The 95 acres I toured are designated as a 1-D-1 ‘Agricultural Use’ – either cattle or timber. As a result Bexar County only taxes theoretical ‘agricultural income’ from that property, rather than the full ‘market value’ of the parcel.

The ‘market value’ of these 95 acres might be $500,000, but the actual ‘assessed value’ of the 95 acres is $6,780 – the estimated annual ‘agricultural value’ of the parcel.

As a prospective purchaser of a small fraction of this land, this tax code seemed very ‘fair to me.’

Fair to Society

But fair to society?

Holy cow, this is one of the least fair property tax rules I’ve ever come across.

If you own a house or any other non-agricultural property in San Antonio, you pay taxes as a percent of estimated value, typically around 2.7% of market value.

If I owned a big house in Bexar County worth say, $500,000, I should expect to pay 2.7% in taxes to the county, or $13,500 per year. Which, I don’t know about you, but seems like a lot me.

If I owned a big “1-D-1” parcel for 95 acres in Bexar County worth that same $500,000, however, I should expect to pay 2.7% of $6,780, or less than $200 in taxes per year. Which seems like very little to me.

Here’s where the unfairness hits: The “1-D-1” designations in Bexar County shift the burden of property taxes away from large landowners (like developers) and onto individual home owners.

I learned that a residential ‘market value’ property owner should expect to pay something like one hundred times more taxes than an ‘agricultural value’ property owner per year, according to Bexar County Deputy Chief Appraiser Mary Kieke.

Not about agriculture

I’m not saying I want poor farmers and poor ranchers to pay a lot more in taxes.

Mamas, don’t let your babies grow up to claim 1-D-1 Ag exemptions on their taxes

I can see why the State of Texas, as a whole, has decided to reward legitimate agricultural activity with favorable taxation, as a nod to its rural roots and a preservation of a certain way of life.

I don’t want to mess with that heritage. It’s not my personal gig, but I can understand the point of view.

What I am saying is that this 95-acre parcel I looked at isn’t agricultural in any real conceivable sense of the word. I mean, maybe they’ve run a couple of cows over it whenever a tax assessor is coming by? Maybe some people have cut down a few trees on the property there and reported a ‘timber use?’ I guess?

It’s land banking

Bexar County is mostly comprised of the City of San Antonio, and for the most part San Antonio has ceased to be an agricultural producer. That’s not preventing people from taking advantage of the tax code to land bank cheaply, however.

For the present owners, this parcel – as the small lots around it show – acts as a very low cost land-bank for future housing developments, either in 1-acre lots, or larger tracts.

When I expressed amazement to Appraiser Kieke, she agreed with me that “there are legitimate agricultural uses, of course, but, by and large, this [1-D-1 designation] has become a way for developers to hold land with very low taxes.”

In Bexar County

So how big is the effect in Bexar County? About $63 million per year in lost taxes.

The total difference in value between ‘agricultural’ and ‘market value’ property in Bexar County is $2,348,327,452, according to Kieke, and 2.7% of that amounts to approximately $63 million per year.

If you’re a homeowner in Bexar County you are subsidizing landowners with 1-D-1 exemptions to the tune of $63 million per year, money the county needs that has to come from your much higher homeowner appraisals.

The point here isn’t to increase tax collection by an additional $63 million. But homeowners have a very unfair deal compared to many land-banking owners with 1-D-1 exemptions in Bexar County.

Editor’s Note: A version of this appeared in the San Antonio Express News. Dignowity Hill is a historic neighborhood in San Antonio balanced precariously – for the moment – on the cusp of hipsterism, about to fall into the ‘gentrified’ category. For anyone who has strongly held opinions about gentrification, let me assure you this post has nothing to do with Dignowity Hill, or gentrification. Thank you.

My friend recently asked me what I thought about his idea of buying a small plot of land he saw for sale in Dignowity Hill, as a short-term investment. Less than $10,000.

“The East Side is getting ready to boom,” he tells me. Agreed.

“Dignowity Hill has so much charm and a ton of new investment activity nearby, with the Hays Street Bridge and Brewery, and prices will be going up.” Yup, probably.

“I like the idea of investing for a couple of years, then cashing out.” Ok, now I knew he was on the wrong track, and I told him so.

Markets are more efficient than you think

What I believe my friend did not take into account is the idea that he has hundreds – actually make that probably thousands – of competitors for that single parcel on Dignowity Hill. Those competitors mean he will not likely get a bargain.

Most middle class people, certainly most homeowners, understand the basics of real estate investing. That means hundreds of thousands of people – in San Antonio alone – have the knowledge necessary to buy that parcel, and certainly tens of thousands of people in the city have available cash to pick up a plot of land at less than $10,000.

Of those tens of thousands, I’d estimate many hundreds to a few thousand San Antonio residents actively look for real estate opportunities. I don’t think it’s unreasonable to expect that hundreds of San Antonians have seen this exact parcel, and up until now, have not made a bona fide offer to purchase it, at, or very near, the listed price.

This is not to say definitively that the parcel is a bad investment. Frankly I have no idea. I never looked at it. But I do know that markets with hundreds of potential buyers are pretty efficient at price discovery, and the parcel will not be a screaming bargain for my friend.

Will the East Side boom? Sure. Is Dignowity Hill totally cool? Yeah. Could prices double in a few years? I wouldn’t be surprised.

But the current offering price of the parcel will take into account all of these factors. Any reasonably efficient market aggregates opinions and is forward-looking – meaning my friend would have to pay now for the likely boom, the coolness, and the chance of doubling.

My entire point with this anecdote is this: although we may not see the competition in front of us, many markets are extremely efficient at reflecting all the unseen competition for investments. Real estate is less efficient than some markets, but it’s really not so inefficient that a part-time speculator like my friend will grab a great bargain.

Before concluding, I want to point out two other reasons my friend should be cautious.

Short-term time horizons

If you need to sell any investment within five years, then I don’t call that an investment, that’s something like a speculation. There’s nothing inherently wrong with speculating, only that it tends to work up until the point when it doesn’t any more, and then it ends up looking a lot like gambling in retrospect.

Real estate inefficiency

Real estate – as a speculation or as an investment – is terribly inefficient to buy and sell. Most real estate transactions require you to get an appraisal, do a title search, pay a realtor, and possibly an attorney, all of which add up quickly.

To invest $10,000 in the stock market, for example, will cost you less than $20 to do the transaction at an online discount broker. To invest $10,000 in real estate – unless you have distinct professional discounts or built-in advantages – might run you 1,000 in fees, easily.

I’m not saying I don’t love real estate as a long-term investment. I love real estate. Most of my non-retirement net worth comes from real estate ownership, of my home. But for small, short-term investments, I would rarely recommend real estate, much less real estate speculation.

Garza was kind enough to respond last week, and I appreciate that he took the time.

He corrected a significant error I made on the price at which he sold one of his properties, although the outcome of a lawsuit with respect to a fire at the property, and his sale, should still remain in the public eye.

My goal with Bankers Anonymous is to make finance and financial transactions more accessible to the public.This matters particularly when it comes to evaluating public officials’ actions in the public and private business sphere.

Garza reached out to me last week shortly after I posted a review of his real estate transactions.

Most importantly, he corrected a sale price I reported for 139 North Street, which burned in the Spring of 2011.Based on a public records search, I reported a sale price of $156,250, an implausibly high sale price for a burned structure.

Garza has since showed me a ‘Settlement Statement’ on the sale to Nuvista LLC, which shows a more reasonable $43,000 purchase price.Since an unusual feature of the 139 North Street situation – in addition to the unusual fire, the unusual buyer, and the unusual loan – was the sale price this is an important correction.

The buyer, Nuvista LLC – newly formed in November 2012 by a recently bankrupt gentleman from Arizona – did obtain a $125,000 loan from private individuals in Allen, TX at the time of the purchase.

Ed Garza also responded to other aspects of my real estate review, and I have included commentary and portions of our interview below.

We covered a range of topics, including

A) The fire at 139 North Street

B) The sale price of 1919 Magnolia

C) The appraisal of 2006 Magnolia

In a subsequent post, I’ve included a portion of the interview in which we discussed his other business dealings, including contracting with VIA.

I noted in my piece that a fire in the empty property seemed unusual, and I was curious what the fire inspection showed.Garza responded that

1. The Fire department’s report was ‘inconclusive,’

2. The bank’s insurance company initiated litigation against the contractors on the issue 1.5 years ago,

3. Garza’s firm joined the litigation alongside the insurance company, and

4. Depositions have not yet begun as of June 2013.

The portion of the interview about the fire is below.[I have edited out a few comments tangential to the discussion of the fire at 139 North Street.]

Michael: I’m interested in the story that was reported in the Express News about 139 North Street, and that there’d been a fire there. Can you tell me what happened? I can only see what I can see from that story, but what happened?

Ed:It was a home that was being restored. Probably 80% into the project, the fire occurred. When it’s 80% of the project, that’s after putting in, and investing into a renovation budget of probably close to $100,000 over a period of at least a year, and trying to bring that house, which had been vacant to a number of years prior to the purchase. It was devastating to have something that you spent not just obviously money to invest, but also the time and effort and sweat equity to bring something back to life, in a neighborhood that I’ve lived in all my life was quite devastating. It was the last house that we renovated either individually or as an entity just because of the financial hit we took because of the fire.

Michael:Who was the contractor?

Ed:The contractor was a local contractor that we used, Fieldgate Remodeling was the name of the firm. We used them in the house prior on some work. They were not a general contractor but they had performed services in some of the renovation on the house prior. I was impressed with their work. I was quite busy at the time and my business partner at the time was also busy.

With this next house that we had in inventory, we wanted to get somebody to do the day-to-day, which we’d never done before. We asked them if they would be the general contractor for the project to oversee the day-to-day work.

Michael:Fieldgate Remodeling was the general contractor?

Ed:Correct.

Michael:What happened? Did they have insurance?

Ed:They have insurance. After the fire, the city did their inspection and it was — I guess the best way to say it was there wasn’t a conclusion, it was kind of undetermined.

Michael:When you say the city, who does the inspection for the city?

Ed:The fire department.

Michael:The fire department did an inspection?

Ed:Correct.

Michael:You described that as an inconclusive report?

Ed:Right. They said the property was secure, there was no forced entry into the property. But that they asked what had been done the night before, and what we were told by the contractor, the night before they were sanding the floors. Again this is getting into the final stages of the renovation. The arson investigator that the bank – or the insurance company for the bank – concluded for their report that they believe the fire was started through the combustion of the wood particles the night before, of the sanding of the floors with chemicals from — on a rag from what was used in the kitchen on the tile work.

The chemical and dust particle started the fire in a bucket near the front, literally in the front window of the house. If you’re standing there from the street, you would be able to see somebody. That’s where the bucket had been left, and that’s where the fire started. It burnt through the floor, went under the floor, through the walls, up to the attic and that’s what collapsed in the house was a big attic.

Michael:Do you know who the fire department person was who did the inspection?

Ed:Not offhand, I’m sure I can find his card.

Michael:Do you remember who the insurance company was?

Ed:That’s the same thing, I can get you that information. Are you talking about the insurance company for them or for the bank?

Michael:For the bank.

Ed:I can get you that information. It was also devastating the day of the fire that I learned my business partner allowed the insurance on the property to lapse. That was a shock. Fortunately, I found out through that week that the bank of course by law has to have the house insured, so they had a forced insurance on the property. But was not one that we carried as the property owners.

Since that time, the insurance company filed suit against Fieldgate. We joined that suit. I forgot the legal term that’s used, but we joined that suit for damages caused by that fire. We haven’t been deposed yet.

Michael:Your business partner let the insurance lapse?

Ed:Correct, for the entity. I’m not going to just blame him, but yeah, the business entity did not renew the fire-insurance policy on the house.

Michael:You were personally uninsured but the bank was insured. Do you remember the insurance company’s name?

Ed:No.

Michael:Did the bank’s insurance pay the bank off for the mortgage?

Ed:Yes.

Michael:When did they pay?

Ed:It was probably a few months after the fire.

Michael:At that time, the bank had insurance; you didn’t.

Ed:Correct.

Michael:Then the bank’s mortgage —

Ed:We weren’t going to collect on anything from the insurance but the bank, because of the forced insurance policy, was covered.

Michael:You’re understanding is the insurance did pay out to the bank?

Ed:Yes, so the note was paid later that year, the note was paid off. We held the property free and clear, but of course it’s a fire-damaged property.[1]

Michael:Sure.

Ed:We were out of the investment made for the renovation. No real way to recoup that, and renovating it was going to be — we did get an estimate to rebuild as-is, in terms of same materials, same quality the house was built. It was a little over $200,000.

Michael:It would have cost you $200,000 to rebuild.

Ed:Right, to rebuild as-is, same materials, same quality lumber, every detail was estimated and it was going to be quite an investment.

Michael:The timeline for the mortgage being satisfied by insurance on North Street is really the end of 2011?

Ed:Correct.

Michael:You’ve not been on the hook for that one since the end of 2011.

Ed:Correct, not on the hook in terms of the mortgage, but still in the litigation of the property.

Michael:Is that ongoing still?

Ed:Correct, we’ve not even been deposed yet. We joined that suit with the insurance company that sued the contractor, based on their investigation.

Michael:Are you claiming damages as well?

Ed:Yes.

Michael:As the entity that owned 139 North Street, trying to get reimbursed.

It’s not terribly relevant to the review of Garza’s real estate transactions, but he wanted me to note that in fact he purchased 1919 Magnolia at a better (ie. lower) price than I had obtained from my public records search.I had reported, based on records available to me, that he acquired the property for $114,220.40, which he 7 months later flipped for $250K.He clarifies that he purchased it for $90,400, and sold it for $234,000.

I expressed surprise in my review of this transaction that the buyer could obtain a 1% down-payment mortgage, at a price significantly above nearby comparables, in the tough real estate and lending environment of 2010.

Garza responded, in essence, that

1. The buyer must have had good credit [I think this is necessary, but not sufficient.]

2. The Austin-based bank appraiser must have seen something in the renovation that allowed him to use higher-end Monte Vista comparables rather than the dozens of Monticello Park comparables to come up with an appraisal.

[I have edited this section to take out non-germane comments]

Michael:That reminds me of this other property we haven’t talked about, the 2006 West Magnolia. What’s interesting about that for me is that this buyer was able to get such an attractive financing package. Did you know this buyer?

Ed:I did meet the buyer. They had a realtor.

Michael:Did you list it with somebody?

Ed:Yeah, the same lady that listed 1919 [Magnolia] listed 2006 [Magnolia] with Keller Williams.

Michael:Josette Gonzales?

Ed:Correct. I think that one took — that was already in the bust of the real-estate market and she was more cautious again because the values had gone down, appraisers were even more unpredictable in terms of how they would look at properties. But she still came back and said we can sell this one for $234,000. Keep in mind every house that we did set a new per-square-foot record in Monticello Park. I only focused in Monticello Park. That’s my neighborhood.

I wasn’t interested in buying properties to flip or just doing any house. Being employed at the time with a big company, I didn’t have the time to be doing this as a flipper would. This was more about bringing value back into the neighborhood that I’ve invested in, my wife’s invested in. It really became a passion.

So 2006, again being parishioners at St. Anne’s and the man was a deacon at the church. He passed away and his siblings, his daughter approached me about purchasing that house. We bought it for $120,000. Every house that I bought from Magnolia, both Magnolias, to the Mistletoe, to Fir, I always tracked the BCAD [Bexar County Appraisal District Online Property Search] and I would never offer anything more than the BCAD. That was just a general rule.

This one was right at the BCAD price when we purchased it, and probably sat on it for at least six to eight months before we started the project.

Michael:Just on the 2006 Magnolia, you got an amazing sale off, and what I thought was interesting and highlighted is the buyer — you said you knew the buyer somewhat?

Ed:No. The buyer was represented by a broker, and the buyer is the owner of Candlelight Coffeehouse. They’re the actual owners, what was represented to us, and they were not going to have a problem with applying for the note.

Michael:The note is extraordinary, a 1% down mortgage.

Ed:Right. It must be because of their credit. I would imagine that’s how they were able to get those terms, especially at that period of time. That house we probably had on the market for a month but for us that was a long time.Magnolia was a bit longer, being in 2010, and the market the way it was, but we were still able to sell it within that first couple of weeks.

Michael:I’ve been doing property for a long time and I find just getting a 20% down payment mortgage takes about two months itself, never mind a 1% down payment mortgage within a month, and never mind at a price that really these are outliers if you compare to other tax-assessed value or Zillow value in your neighborhood. They’re really big.

Ed:Even the appraisers, the one for 2006 Magnolia was an Austin appraiser, and every house was a different appraiser. You never know which way they’re going to lean, but the one from Austin came in and said this is an impressive house, every detail of this house has been renovated from the minute you walk up the sidewalk, to the new lawn, new driveway, every little detail of the house.

He said, “You don’t see these kinds of renovations. Usually we see flips, which mainly are in the interior, they may be more cosmetic. They don’t get to foundation or rewiring, and definitely don’t get to the landscaping.” Even an Austin appraiser didn’t know anything about the neighborhood, and they came with that Austin perspective. He appraised it a bit above what we were under contract for. They were using a lot of comps because many of these appraisers couldn’t find comps in Monticello, but they were using comps from Monte Vista.

Michael:I got a mortgage in 2010 and my bank came in about 15% less than what I was paying. I’m amazed that in 2010 you could get a 1% down mortgage and a bank to come in at really 30% higher than anything else in the neighborhood. It’s impressive.

Ed:We did a house on Fir also, 222 Fir, and that one set a per-square-foot record. That was the first one I did with Mr. Wayne. That was a 2-bedroom/1-bath and I think we had it sold for 211,000. The price per square foot it was $180-190 range, which again was unheard of in Monticello Park.

Written rules substitute for our ability, or the bank’s ability, to make individual decisions specific to a situation.

Written rules substitute for our ability, or the bank’s ability, to make individual decisions specific to a situation.