Hill employs the patter of a carnival barker throughout his book, which should probably be the first clue. But Novak did the research on the man Napoleon Hill himself.

As it turns out, his life was a complete lie. His original claim to have learned the secrets of business from Andrew Carnegie: false. His business biography: A cover-up of his scam-artist background.

One lesson of Novak’s piece: If it seems like the guy is selling snake-oil, he’s probably selling snake oil. We’re in a new era, in which the ability to spot a scam artist is particularly important. One of my rules has always been, if he’s willing to lie and cheat about some things, he’s probably willing to do it about anything.

Passing bad checks, lying about the ‘source’ of his business knowledge, running from the law…You have to consider the messenger when evaluating the message. Anyway, if you’ve been tricked into reading this kind of book, or worse, going to ‘real estate seminars‘ with the same approach, you’ll be sure to enjoy Novak’s piece on Napoleon Hill.

Please see related posts

When I write all these things, I want to clarify these are not predictions, but rather my frightened projections forward of what I see Trump has indicated he will do. I will get no pleasure in being “right.” I sincerely hope Trump’s supporters and allies have the last laugh at me. As an American citizen, I hope he turns out to be just a call-it-like-he-sees-it competent businessman thumbing his nose at the elite establishment.[1]

What would allow me to sleep better? For starters, I wish there was real opposition in government right now. With the Democratic Party stripped from the top levers of federal power, that opposition has to come from within the Republican Party. That’s the real bottom line right now.

The two things I want most for Christmas this year are an assertive free press and aggressive enforcers of the separation of powers and the Bill of Rights. If I’m really laying out all my wants, somebody who can keep us from foreign wars and fiscal suicide would be nice as well.

My policy agenda

If you’ve read this far into my posts on the Trump administration, can I let you in on a little (sort of unintended) joke about my Trump fears and my policy advocacy?

I didn’t really intend this when I started writing about Trump, but the things I’m advocating here are all traditional conservative Republican values. That’s not usually where I land. I don’t know Bill Kristol’s inner dialogue deeply, but I’d like to think he and I would agree on all of this stuff.

I’m talking about enforcing strict constitutional values, like individual freedom, not collective rights. I’m talking about protections against encroaching government interventions like surveillance and registrations – the kinds of things conservative Republicans usually advocate. I’m talking about limiting our responses to foreign provocations. I’m talking about balancing our budget and paying our debts. I’m talking about maintaining national strength through an independent central bank and monetary policy. I’m talking about expanding free trade, not getting into a protectionist crouch to coddle certain favored industries. Shit, this would put me on the same page as a conservative icon like Ronald Reagan. That’s all I ask for right now.

The way I figure it, this is not the time to be pushing my more narrow progressive agenda, or any wish for the arc of history to bend my way. This is a time to keep the focus on surviving First Order threats to the Republic.

It’s a lot to ask, I know. These are the kind of existential threats we haven’t really worried about at the start of a Presidency since the four inaugurations of Franklin Delano Roosevelt during the Great Depression and World War Two.

Because if you take President-elect Donald Trump at his literal word during the campaign, all of these threats are suddenly back on the table. This is why I’m not sleeping.

Help us, Ted Cruz!

Calling all patriotic leaders of the Republican Party: The time will come, probably very soon, for you to take brave, even historic, stands. This is your time to show America’s greatness.

I feel like Princess Leia here, stuffing a message into my laptop just before the Empire arrives, whispering earnestly into my MacBook Pro: “Help us, Ted Cruz, you’re our only hope.”

Here is my short-list of Republican patriots I am counting on.

Senator Ted Cruz – You believe deeply in the US Constitution and even taught Constitutional law at the University of Texas. Your senior thesis at Princeton was on the separation of powers. Before becoming my Senator from Texas you argued and won five cases in front of the Supreme Court. You have shown an eagerness to be a completely maniacal obstructionist in the Senate on principles you believe in. You nearly took down our government during The Fiscal Cliff near-default of 2013.

This is a great start! You even deeply dislike Trump! We could all use a guy like you right now.

I figure you also understand the #Calexit impulse of Californians wanting to secede from the union, since that’s an old idea from the Right in Texas. You believe in protecting states from the encroachment of the federal government. You need to be a bulwark of support for these Californians who are newly frightened of the federal government! You’ve got this!

Senator John McCain – Nobody understands the grave damage torturing enemy combatants does to our security and reputation – in addition to what we might poetically call our nation’s soul – more than you. You suffered for years at the hands of torturers in Vietnam.

President-elect Trump has threatened he will torture enemies with “waterboarding and much worse.” Senator McCain, you have called waterboarding a War Crime. You have singular credibility and a duty to stand up on this issue. I’m guessing Trump – after he said of you he likes “people who weren’t captured,” is not a close ally of yours. You did make a good start when you declared that you would take the Trump administration to court if they attempt to torture people. Please continue to speak out.

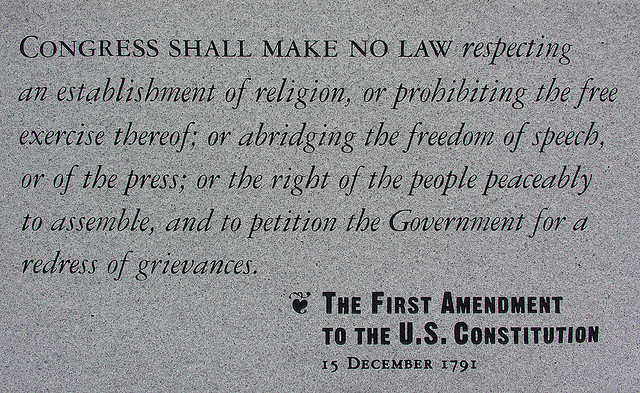

Chief Justice John Roberts – Our individual, inalienable, rights may be trampled by the instincts of Donald Trump, with the appointment of people who seem to want to take these away. If they are appointed to cabinet positions, will the Supreme Court stand up to advocates for increased domestic spying, or terrible ideas like advocacy for special registration for American Muslims? Religious freedom and freedom from warrantless searches underpin our system. Justice Roberts, please guide the Supreme Court toward striking down laws or executive orders that contradict our First and Fourth Amendment rights to religious freedom and privacy.

Senator Rand Paul – Your whole career – and that of your father Congressman Ron Paul – is a fight for principles you believe in, particularly strongly on both First Amendment rights and on the idea we should not involve ourselves in foreign military adventures. We all need you to be a zealot on both of these issues right now. Our incoming Commander-in-Chief Trump exudes an appetite for vengeance and violence, with little impulse control.

Sen. Rand Paul, R-Ky., speaks during an event at the University of Chicago’s Ida Noyes Hall in Chicago on Tuesday, April 22, 2014. (AP Photo/Andrew A. Nelles) ORG XMIT: ILAN114

On First Amendment rights of free speech and a free press, Trump said he was “running against the crooked media,” calling them “dishonest” “disgusting,” and “scum.” He threatened newspapers like the Washington Post with “such problems” once he has been elected.

As for foreign wars, we will certainly be threatened by other countries and terrorists in the next few years, but that does not mean we should go to war because some tinpot dictator tweeted about Trump’s tiny fingers. Senator Paul, please continue to make the principled case for keeping us out of Trumped-up wars.

“[I]s Donald Trump a serious candidate? The reason I ask this is, if you’re going to close the internet, realize, America, what that entails. That entails getting rid of the First Amendment, ok? It’s no small feat. If you are going to kill the families of terrorists, realize that there’s something called the Geneva Convention we’re going to have to pull out of. It would defy every norm that is America. So when you ask yourself, whoever you are, that think you’re going to support Donald Trump, think, do you believe in the Constitution? Are you going to change the Constitution?”

House Speaker Paul Ryan – You made your reputation within the Republican Party as an economic policy wonk and fiscal conservative. That means spending only what we can afford, and responsibly paying our bills. You know in your head, within your heart, and on your spreadsheets that our country – with a 100 percent debt to GDP ratio already right now – cannot afford a massive tax cut and a trillion dollar infrastructure spending plan, as called for by President-Elect Trump. And certainly, not both at the same time. I know you know this, because you understand budgets.

The US Constitution’s Article 1, Section 7 mandates:

“All bills for raising revenue shall originate in the House of Representatives.”

That’s you! C’mon Speaker Ryan, you got this. Stand up for what’s right. The US Bond markets turn their lonely eyes to you.

America – you need leadership in your corner, at least until 2018 mid-term elections. I present to you the principled leadership of Cruz, McCain, Roberts, Paul, and Ryan. Let’s hope they are enough.

I’m sorry, folks. I’ll probably never sleep again.

[1] With the self-control, empathy, honesty, and class of an 8 year-old spoiled man-child, but still.

Trump does not respect the freedom of religion when he says Muslims resident in the country may need to sign up with a specific registry. He undermines both the rule of law and the separation of powers when he attacks the court investigating his Trump University fraud – because of a specific judge’s ancestry.

Even short of Constitutional threats, he’s already ripped up traditions and best practices that are often as important as codified law. The fact that he repeatedly lied about not releasing his tax returns because of an IRS audit – thus flouting modern tradition about financial disclosure from Presidential candidates – shows he will push the limits on unwritten norms, when it suits him.

This limit-pushing instinct, combined with a disregard for Constitutional checks on power, make Trump a danger to the Republic. At every turn he attempts the immoral, illegal, or unconstitutional choice. It’s going to take alert and brave members of government and society at all levels to keep the US Constitutional issues front and center, and viable.

As Matt Levine pointedly reminded us the day after Trump’s election, the Constitution and other laws are only as good as the people who are willing to enforce them. Otherwise laws just become silly pieces of paper, worthy of little notice, or the kind of things to knowingly flout like speed limits that few heed on a highway. That’s why it’s a little extra frightening right now that the opposition party in Washington is so weak. Are there Republican leaders who can stand up to Trump? I really hope so.

It should be obvious by now – even before he takes office – that, as President, Trump will attempt to violate many of our most important constitutional protections and best practices in his first few years in office. The question will be whether and how people respond. Chavez, Putin, and Hitler all managed to eliminate checks and balances to their power in their early years in office.

Do our leaders roll over and allow him to get away with it?

This is a long post about how Trump has specifically threatened to cause an economic or financial crises through either a trade war or through undermining the US monetary system and credit.

Similar to a security crisis, I can’t sleep because I worry Trump may inadvertently cause an economic crisis, which he may then uses as a pretext for further authoritarian moves.

Look, this can’t be a prediction about “what’s going to happen” with the economy under Trump. Most of the time when we talk about markets responding to a presidency, we are finding false signals in noise or we’re predicting things that are really unknowable.

I do worry, however, about two specific economic problems that Trump has promised to cause: Trade wars, and interference with US financial strength through the bond markets and Federal Reserve. The long-term problem with an economic crisis – besides the obvious pain and suffering – is a societal desperation that allows an authoritarian to make bold moves otherwise unavailable to him.

Let’s start with trade.

In the arena of international trade, Trump’s “plans” – such as they are – could and would cause a worldwide trade-war and global recession. He launched his presidential campaign pledging massive 35% tariffs on our major trading partner Mexico. He reiterated his plans many times on the campaign trail to retaliate both against Mexico, and against companies like Ford Motor that may move manufacturing jobs to Mexico. By the way, 16% of our national exports go to Mexico.

Trump pledged to withdraw not only from the recently-negotiated Trans-Pacific Partnership but also to renegotiate or withdraw from 1994’s North American Free Trade Agreement with major trading partners Canada and Mexico. By the way, 19% percent of all U.S. exports go to Canada.

Trump’s promises mark a very big shift in US policy and leadership.

The problem with unilateral trade sanctions like this is:

They don’t stay unilateral. Countries affected will obviously retaliate against us with their own trade sanctions, and;

The United States would probably be in violation of international trade systems like the WTO.

The globalization of trade since the end of World War II – and in particular since the end of the Cold War – has greatly favored the United States, even if the effects of trade hurt particular industries or geographies. A reversal of that trade situation – championed by Trump as he champions those most hurt by globalization – will make us all poorer.

At the same time, high tariffs are unlikely to bring back manufacturing jobs. The bad news[1] is that we pay people too much in this country and we enforce too many worker protections to make many manufacturing jobs viable here.

Trump has promised a trade war, but without a chance that it could possibly “work” in the sense of bringing back many jobs for those most affected by globalization.

Now, maybe Trump is just kidding about his trade war plans. Maybe its just a goof, indicating his direction of thought, but he won’t enact anything as crazy as what he’s promised?

Commerce Secretary Wilbur Ross

His selection of billionaire investor Wilbur Ross for Commerce Secretary, however, indicates Trump’s seriousness about protective tariffs. Ross made his career as an extraordinarily successful vulture investor in beaten-down industries such as steel and coal, domestic industries buffeted in part by regulations and high worker-costs, but also by international trade.

In 2002 and 2003, Ross bought up bankrupt steel-producers LTV Corporation, Acme Metals and Bethlehem Steel.

A well-timed 30% tariff on imported steel in 2002 enacted during the George W. Bush Administration helped raise the value of Ross’ steel holdings, which he eventually sold to Indian-owned Mittal Corp in 2005.

Incoming Commerce Secretary Wilbur Ross likes steel tariffs

Ross has indicated his support for both Trump and the idea of protective tariffs, and he clearly has the business experience to know that trade protection can enrich the owners of certain industries.

While higher steel prices help steel workers and owners, however, they hurt other industrial companies – like the auto or construction industries – that need to buy steel at the lowest price possible.

Trade wars can benefit some select sectors and people even while most of us end up poorer through higher costs. International trade has been a major generator of wealth since the end of World War II, with the United States as its biggest cheerleader. I’m afraid Trump intends to kill the golden goose, with severe economic consequences.

Undermining financial strength

The second economic crisis threatened by Trump is his promise to weaken the Federal Reserve. It will take some wise financial counseling to explain to Trump why his threats do not really help the United States. He has not shown evidence, however, that he can take that kind of advice, or learn from it.

I worry that over the next two years Trump will have the ability to reshape the Federal Reserve in ways that undermine one of the central bank’s key strengths – its independence from politics.

Janet Yellen, Chair of Federal Reserve

The Fed is the quasi-public, semi-mysterious, massively-powerful, independent central bank for the United States. It’s an “independent” regulator, meaning it technically doesn’t report to Congress or the U.S. president. Given its mystery and importance, critics on the Left and Right often seek to curb the power of the Fed. Anything that powerful must be part of some kind of conspiracy, right?

President-Elect Trump — who served as human fly-paper for the bad economic ideas of fringy cranks throughout his campaign — caught this wave too. He accused the Fed of being in the tank for the Obama administration. Like the Republican Party, the Democratic Party, the FBI, the Electoral College, and the media to name a few — the Fed — Trump complained, was part of an unfair conspiracy against him.

But then Trump went further down an even darker path in attacking the Fed. In “Donald Trump’s Argument For America,” released in the days before the election, he linked images of Fed Chair Janet Yellen to the well-known faces of financiers George Soros and Goldman Sachs CEO Lloyd Blankfein, as part of a “global elite” conspiring against ordinary Americans. All three are Jewish, of course, and the ad recalled anti-Semitic conspiracy theories that follow the vile and fictional “Protocols of the Elders of Zion.” Whether Trump claims that Yellen is in the tank for his opponents, or whether he winks knowingly at anti-Semites about a global Jewish conspiracy, he has set the stage to justify curbing the Fed’s independence.

This video:

This should trouble us tremendously. The U.S. is a country that — despite the confounding popularity of the Kardashians — retains an outsized role in the global economy. One of America’s greatest strengths as a financial power is the belief that its central bank is not unduly subject to political control from any particular party or faction.

Usually when we talk about policies from the Fed, we don’t focus on Democrats and Republicans or Liberals and Conservatives, but rather “Hawks” and “Doves.”

In simplest terms, a “hawk” tends to worry about inflation more than unemployment, and pushes the board to raise interest rates quickly enough to avoid unexpected inflation. A “dove,” conversely, worries more about unemployment than inflation, and would tend to want to keep interest rates low as long as possible, to juice economic activity even if it spurs a little bit of inflation. I’m simplifying here, but these are the broad strokes.

A key point, though, is that a Fed governor — whether hawk or dove — is supposed act independently from politics. Almost as important is the idea that a Fed governor seems to act independently from politics. We count on the appearance of independence as much as the reality.

The first guarantee of independence is that the seven board members, known as governors, serve 14-year terms, thus guaranteed to outlast any U.S. President. A bit like justices appointed to the Supreme Court for life, Fed governors therefore should not owe their ongoing positions to any particular political faction. The next guarantee of central bank independence is that the Fed Chair is nominated by the President from among the governors and gets appointed to a four-year term that does not coincide with a President’s four-year term. Janet Yellen, the current Fed Chair, plans to stay in office at least through her term in 2018.

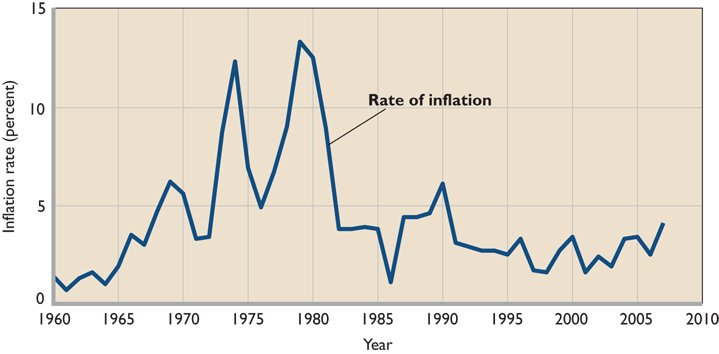

Inflation spikes correspond with political interference with the Fed

The specter of political interference in Fed policy has darkened our political scene before. Economist and former Minneapolis Fed President Narayana Kocherlakota recently wrote about historical problems when the executive branch interferes with the US Fed. During and following World War II, the Fed kept long-term rates artificially low to allow the government to borrow cheaply. Inflation soared to nearly 10 percent by the time the Korean War began in 1950. Later, Narayana reports, Presidents Johnson and Nixon pressured the Fed to stimulate the economy, leading in part to astronomical inflation of the ’60s and ’70s that peaked at 14 percent in 1980.

With President Trump able to appoint a new Fed chair and vice-chair in 2018, plus the chance to fill two more currently open spots on the Board of Governors, a real point of pressure exists. By 2018, he will have appointed four of seven Fed governors. Would Trump show restraint, or would he pressure the Fed to support his agenda?

Authoritarians, as a rule, cannot stand independent central banks. They don’t like the idea that some entity independent of them can wield vast power over both the real economy and banking institutions.

The U.S. enjoys a massive financial subsidy because, up until now, the wealthy of the world trust that our currency will not be suddenly inflated away to worthlessness. An independent Fed assures the world that authoritarians cannot bend monetary policy to their will. But authoritarian regimes, the kind that curb central bank independence, never get trusted with this kind of financial status, as a place where global holders of capital want to park their surpluses.

There are many areas where Trump’s actions might undermine our strengths as a country. Attacking the independence of the Fed is one of the most important ones to watch out for.

Threatening bond markets

Last but certainly not least, it takes a long time (dating back to Alexander Hamilton!) to build up the kind of credit the United States gets for political independence in monetary policy, as well as the kind of trust that attracts global capital to fund our government. It probably only takes one aggressive authoritarian to make that capital flee. And if it flees quickly, that alone can cause a financial crisis.

During the campaign last Summer, Trump argued that if the US borrowed too much, he would simply re-negotiate our debts.

“I’ve borrowed knowing that you can pay back with discounts. [As President,] I would borrow knowing that if the economy crashed, you could make a deal.”

Um. Wut.

Holy fucking shit. Gah. That’s not how it works with the US bond market. You don’t default (that’s what “making a deal” means) on the US bond market. Or at least, you don’t get to do it more than once. Because suddenly you’re Argentina, or Ecuador, or Ukraine when it comes to your ability to borrow.

He’s talking about treating our country like one of his Atlantic City casinos, walking away and stiffing our lenders. If bond investors took him seriously and literally (like I do) we’d have an immediate financial panic. Personally I think Trump’s attitude towards US sovereign debt is the scariest thing he’s ever said, in terms of a threat to the continuation of the United States of America as we know it.

And that’s saying a lot, considering what’s come out of his mouth or Twitter account.

Who will be to blame?

If an economic or financial crisis occurs under a Trump administration, I don’t see the events as something that would cause Trump to reflect on his actions or take responsibility for his errors. I think he will see the crisis he caused as an opportunity to blame his enemies.

An economic crisis – like a security crisis – can make people desperate for action, any action (however rash) to make it better. People who are angry or fearful about losing their jobs or financial status or fortunes are more likely to turn a blind eye to constitutional encroachments.

Those constitutional encroachments are in the end what I’m most worried about, and are what I will write about next.

My littlest one turned four years-old last weekend1, and my eight year-old is taking a Texas-Public-Schools-3rd-Grade-State-Mandated-High-Stakes-Standardized-Test this week2, so you can probably guess what’s on this ex-banker’s mind:

Time is quickly running out for me to save money for their college tuition.4

The only thing scarier than those scary scary clown head trash cans at my littlest daughter’s birthday party5 is the prospect of saving enough money for her college tuition.

For my eight year-old, I’ve got just 10 years to go before C-Day, so I thought I’d share my current ex-banker thoughts with others, in the hopes that we can experience this horrific fear together.

Also, “saving for college” allows me to discuss my favorite topic (compound interest!) so that’s always a good enough reason by itself for a Bankers Anonymous post.

I see three big questions about college savings, with the most interesting one being #2.

Question #1: What college savings account or investment vehicle, if any, should I use?

Question #2: How much do I need to save, per month, to be totally set for college tuition payments when they arrive? (Compound interest calculations coming up! Yay!)

Question #3: What kind of investments do I need in my college savings account?

I’ll take these in order.

Question #1: What savings account or investment vehicle, if any should I use?

Open up a 529 College Savings account.

Ok, that was easy.

But, why a 529? Also, which one?

The first “why” is because you may get an income tax advantage when you make a 529 account contribution, depending on the state you live in. When I lived in New York and paid New York state income tax, I enjoyed an income tax break on my contributions. Now that I live in Texas, I get no state income tax advantage from 529 account contributions.6 So that may, or may not, apply to you.

The second ‘why’ is that any capital gains or investment income – which might be triggered when I sold stocks or earned interest on my investments – remain protected from taxation in that year, assuming I do not make withdrawals from my 529 account. If I just held my college savings in a regular, taxable, brokerage account, I’d be required to pay taxes on capital gains or other income from my investments. The result of this 529 account tax protection is that I can grow my money much faster than in a regular, taxable, brokerage account.

Ok, so that sounds good, but which 529 account should you open? Probably you should start by investigating your own state’s offering7, precisely for that potential income tax break. But if you live, as I do, in a state without an income tax, then you can consider other advantages, having to do with

a) Contribution limits – Some states allow higher contributions than others

b) Flexibility of investment choices – some states offer restricted types of investments

c) Cost of available investment choices – some states offer higher-cost plans than others

d) Convenience

I opened a New York state account for my oldest daughter because we lived there, then. My youngest was born in Texas, but I opened a New York state account for her as well, purely for convenience sake. I prefer tracking both girls’ college savings information on a single website.

Question #2 – How much do I need to save, monthly, to have everything covered?

The College Board (The fun group that brought you the SAT, the PSAT the AP tests, and more!) has a couple of incredibly useful online calculators.

First, they can help you figure out how much of college’s cost you, as a parent, will likely have pay. To try the calculator, go here.

This calculator asks some specific questions about your family situation, plus your income and savings, and then tells you how much the financial aid department of a college will likely expect you to contribute for your child’s annual college expense.

Beware, because [**Spoiler Alert**]

This number will be much higher than you want it to be.

I don’t think of myself as wealthy, and generally we don’t have much left over at the end of the month. Which is why the expected contribution number from a typical financial aid department left my face feeling a bit tingly.

Is it getting warm in here, or is that just me? My editor-in-chief 8 thinks I’m either suffering from menopause or anaphylaxis based on these symptoms. We’ll just have to wait and see.

Next, the College Board has a great college savings calculator to tell you how far your current plan will go toward paying for college. Before you go there, I’d like to warn you – the result is scarier than scary, scary, clowns.

First, you input the current cost of college, an assumed rate of tuition inflation, how many years your child will attend, and how much you will likely have to pay, which you may have some idea about based on the first online College Board calculator above. Next, you input how much you’ve already saved, what you expect your annual investment returns will be, how many more years you have before your child goes to college, and how much you plan to contribute monthly, between now and then.

You input all of that, and then you have a heart attack immediately and die, because there’s Just. No. Way.

I personally can’t feel the whole left side of my face right now.

For example, let’s say I’ve managed to put aside $19,000 for my 4 year-old up until now.

Looking good, Billy Ray.

And let’s say I plan to invest $200 per month until she turns 18, and I can earn a 7% return on my investments, via my 529 account.

Feeling good, Lewis.

Also, assume a private 4 year college costs $50,000 per year today, the college cost inflation rate is 5%, and I plan to pay 90% of that from savings.

I have an estimated shortfall of $276,399.

Randolph, this isn’t Monopoly money we’re playing with.

Some of you clever readers may just be smirking because your little darling will likely either get a ton of scholarships or else attend a state college, no?

Well, the bad reality is that state college isn’t that affordable these days either.

The average 4-year in-state tuition cost, according to the College Board, will set you back $21,477 this year.

If I have zero savings for my 4 year old, but I manage to invest $200 per month, starting now, and she attends an average cost in-state college, I’m still $107,582 short, 14 years from now.

The answer to the question “how much should I be saving per month to be totally set for tuition” is provided by the College Board calculator, just under the shortfall number.

After you recover from this shock, you’re ready to move on to question #3.

Question #3 – How should you invest your child’s 529 Account?

This one’s easy, and frequent Bankers Anonymous readers will not learn a single, damned, new thing from me here, because the answer is unchanged from previous, similar questions about how to invest for the long run.

Hopefully you noticed, from playing around with the college board’s calculator, that you need a fairly high rate of return on your investments from now until college to even have a chance of closing the gap between your current savings and how much you’ll owe for your child’s college, every year, for four years.

Now, since returns have to be high, you have precisely one choice for how to invest: 100% equities.

Let me further clarify, in a way that will again make me sound like a broken record for careful readers: You need to invest your long-term savings for college in a highly diversified low-cost (probably indexed) mutual fund, invested in stocks only.

Why 100% equities?

Why not bonds or other safe investments? Two reasons.

The first reason is low returns. For the vast majority of us, we can’t afford to invest in bonds over the medium to long run. An intermediate-term bond fund will return somewhere between 0.5% and 2.5% right now, and that’s just not going to cut it.

The second reason is that – on a probability-adjusted basis – you will get more from investing in equities.

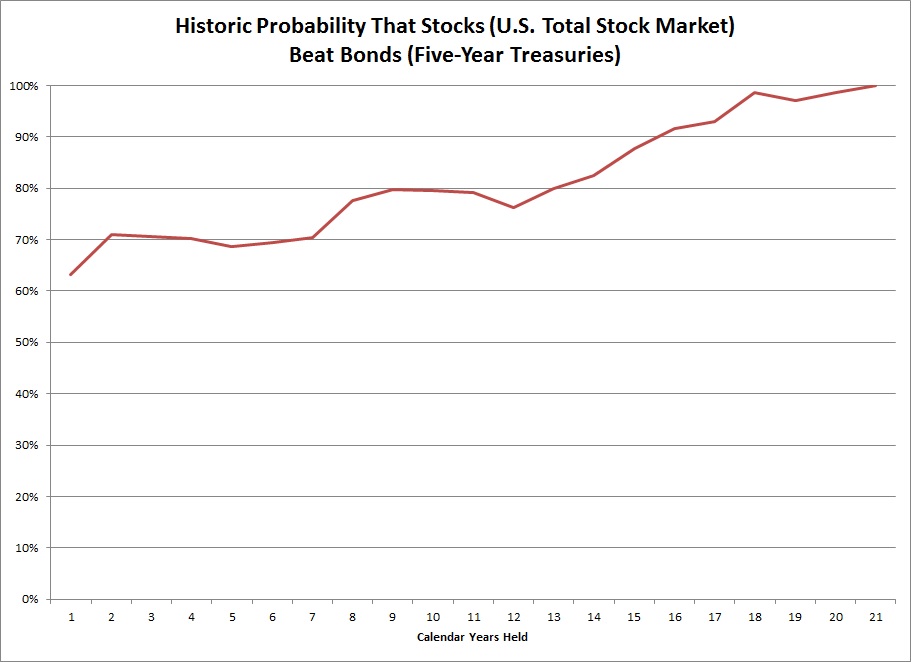

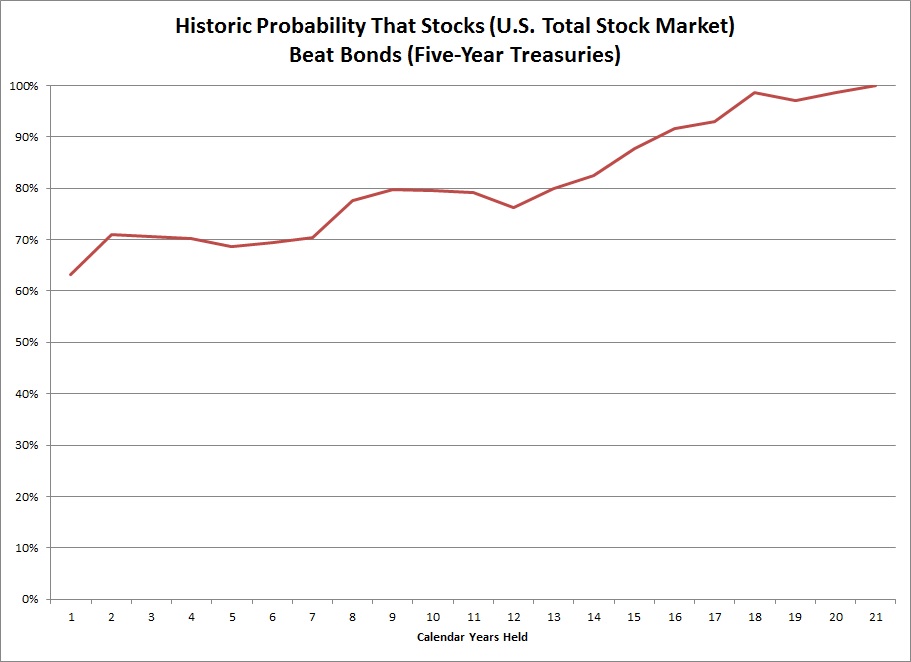

If you have a 5-year investment horizon, you will be better off entirely in stocks, rather than bonds, 70% of the time.

If you have a 10-year horizon – as I do – you will be better off entirely in stocks rather than bonds, 80% of the time.

If you have a 15-year horizon – as I do with my youngest daughter – a 100% stocks portfolio10 outperforms a 100% bonds portfolio 90+% percent of the time.

Is that guaranteed? Of course not

Probabilities are not the same as guarantees,11 so of course the bet you make on investing in 100% equities in your child’s 529 account could go wrong. But making the other choice – including bonds in your portfolio – is a low probability bet. By investing in bonds you are implicitly saying “Probabilities be damned! I don’t care about history! This time is different!”12

Look, I play poker with the neighborhood dads, so I know that low-probability bets sometimes work out. But I also know it’s kind of stupid to make low-probability bets. Trust me, because I’ve been losing $20 a week on a regular basis to these guys, testing this hypothesis, since I’m not a strong poker player.

You can decide to weigh down your kid’s college savings account with bonds, and you may be under the illusion that this is ‘prudent’ because they’re bonds and “bonds = safe.” But it’s not prudent, any more than it’s prudent to bet with jack seven off-suit.

Low probability bet

Would I advocate investing in 100% equities if my kid is going to college next year?

Well, this gets trickier. Stocks still beat bonds in most years, so if you want to play the odds – and if you have some kind of cushion – you could reasonably keep the account in stocks. Most of the time – on a probabilistic basis – this would be a winning choice.

But I realize this seems a bit extreme, so with one year to go I’d probably take next years’ tuition (potentially only 1/4th of your position) and plunk it into a risk-free investment, like a money market fund13, and leave the rest exposed to stocks. Remember, 3/4ths of your account has more than one year to remain invested. Each additional year invested increases the probability that stocks beat bonds.14

Tick Tock Tick Tock

For my wife and me, that loud ticking we hear is not the biological clock anymore, but rather the college financial clock.

For anyone in our demographic15 who checked the College Board calculator,16 I’ll now sum up the only other good pieces of advice I can think of related to saving for college.

Open up a 529 Account for each kid. Like, right now. Stop reading blogs and do this immediately. Really. Did you do it yet? How about now?

Set up an automatic withdrawal from your bank account, so you don’t have to make a choice about contributing every month. Because if you have to make the choice every month, the money might not be there. Even $25 per month in automatic withdrawals is better than nothing. Increasing that $25 monthly contribution over time, once the account is open, will be much easier than you think.

My wife and I like to jokingly append “–should they choose that path,” whenever we discuss our daughters going off to college, but the fact is that’s our chosen path for them and they can deviate from it at their peril. I’d like to see you just try it, kiddo. ↩

In a news item that may or may not be directly related to this fact, my local urban school district boasts 7% college readiness among its graduates. I will now light myself on fire. ↩

Hopefully the following is obvious, but just in case it’s not: When I say 100% stocks I mean a highly diversified mutual fund, not an individual stock or even a small group of stocks, or a single stock sector. When I say bonds I really mean a AAA-rated bond fund of, say, intermediate duration. Not junk bonds or emerging markets or anything else interesting and high-yielding. ↩

“This time is different” is one of those investing No-Nos as a justification for making an investment decision. “This time is different” is a fine gambling notion (for investing in individual tech stocks, for example, or buying into a venture capital fund) but is not a fine investing notion. ↩

Why a money market fund and not a bond fund? Because a bond fund, with only one year to go, could actually lose money as well – in a rising interest rate environment – so only a money market fund guarantees you zero volatility of results. ↩

Incidentally, investing today for your kids’ college next year is NOT the way to do this. Sorry if you are reading this with a 17 year-old breathing down your neck. 529 accounts have little to offer in this case, and compound interest can’t help you much either. ↩

Meaning, you’re going to pay for some kid’s college some day. ↩

And if you haven’t yet used the calculators, have a swig of whisky and then seriously you should go check them, it’s the right thing to do. ↩

I read with great interest this long piece by Matt Novak on the back-story of Napoleon Hill, a man who gets credit as the father of the self-help genre. When I started doing financial book reviews, a number of people (and lists) recommended Hill’s 1937 classic, Think and Grow Rich. I reviewed his book, and while much of it was cheesy, I tried to keep an open mind.

I read with great interest this long piece by Matt Novak on the back-story of Napoleon Hill, a man who gets credit as the father of the self-help genre. When I started doing financial book reviews, a number of people (and lists) recommended Hill’s 1937 classic, Think and Grow Rich. I reviewed his book, and while much of it was cheesy, I tried to keep an open mind.

{kind=link}