I went to my happy place this past week, which faithful readers (both of you!) will understand means I got to build myself a really neat-o spreadsheet.

I went to my happy place this past week, which faithful readers (both of you!) will understand means I got to build myself a really neat-o spreadsheet.

I built it so that I could see “under the hood” of Social Security benefits calculations. This isn’t something I’d necessarily recommend to people who grew up in a loving household and who know how to relate to real live humans. But everybody has his or her hobbies. Don’t judge.

Generally, if you want to know what you should know about Social Security, I strongly recommend creating a My Social Security Account and I also strongly recommend going online to your Social Security benefits estimator. These online sources are easy to use, full of insights personalized to your own situation, and they could save you the hassle of a phone or in-person visit with a Social Security office.

But for the small percentage of you who’d like to talk nerdy with me, I thought I’d add a few more insights into what I found as a result of my custom-built spreadsheet and by pulling my own reports.

These insights include the effect of low earnings, the effect of entrepreneurship, and a benefit of working deep into one’s retirement years.

My Own Report

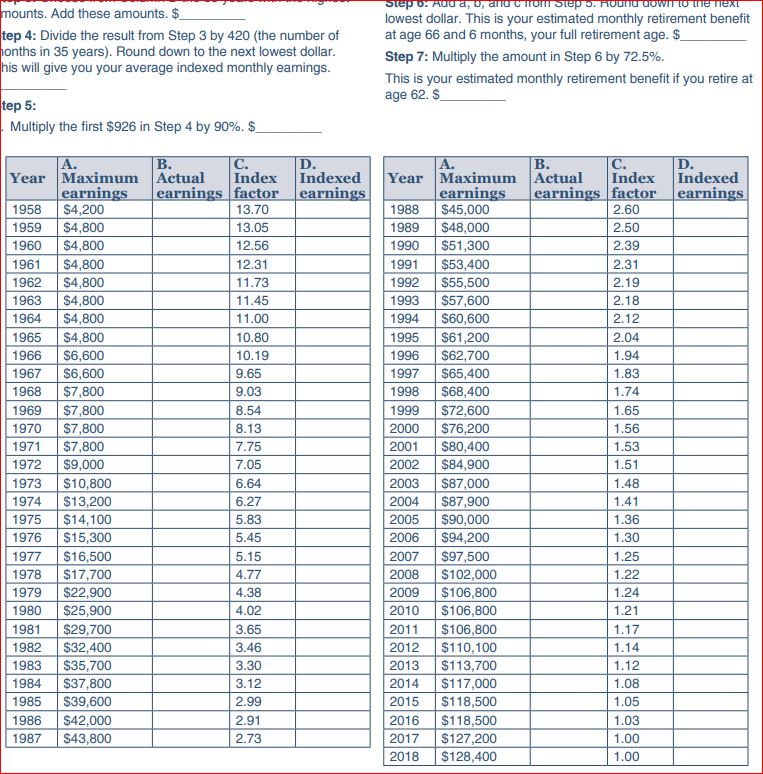

In the example of my own Social Security report, since I graduated from college, between 1996 and 2017 I have twenty-two years in which I have reported taxes. (2018 taxes, obviously, are not yet filed.) Of those twenty two, eight years represent high earnings. Three years represent virtually no income (I’ll explain that a little later on). In the other eleven years my income was “meh.”

I mentioned in the last post on Social Security that having a high income for a short amount of time is not as valuable – for the purpose of maximizing Social Security benefits – as having a moderate income for a long period of time. That’s because every year out of 35 years of earning income and paying taxes matters. Miss out on one year of earnings, and your benefits go down, at least a little bit.

As a soon-to-be forty-seven year-old, I have twenty more years in which to earn income, pay Social Security taxes, and therefore maximize my benefits. “Full retirement” age for me, by the time I get there, is scheduled to be 67 years old.

Incidentally, for current Social Security retirees today, the “full retirement” age is 66 and a half, but that age keeps creeping upward. And it ought to creep upward because we live way longer on average than people used to, so it only makes sense for the solvency of the Social Security program to increase the retirement age. But that’s a controversial topic for another day.

The point is that I’ve got a mere twenty more years to maximize my eventual benefits. And yes, one way to increase benefits is to delay starting your monthly payments. But that’s a well-known fact, and also not the topic for today. The topic today is getting the best thirty-five years of earnings possible.

Racking up thirty-five steady years can be difficult, for example, if you start or run your own business.

Entrepreneurial income varies tremendously year to year, which will have an effect on your final Social Security Benefits. I noticed from my own Social Security report that in the first three years of founding my investment business in the mid-2000s that I earned essentially zero income. The losses incurred in my startup years zeroed out my taxes – which was delightful at the time – but it also meant I did not pay into the Social Security system. Since all thirty-five years of earnings count toward building up Social Security benefits, entrepreneurs with volatile earnings may accrue far fewer benefits over a lifetime than will long-time employees with steady earnings. Even very successful businesses have years of losses, at least from the owner’s tax perspective, so that could lower Social Security contributions and therefore eventually benefits.

Entrepreneurial income varies tremendously year to year, which will have an effect on your final Social Security Benefits. I noticed from my own Social Security report that in the first three years of founding my investment business in the mid-2000s that I earned essentially zero income. The losses incurred in my startup years zeroed out my taxes – which was delightful at the time – but it also meant I did not pay into the Social Security system. Since all thirty-five years of earnings count toward building up Social Security benefits, entrepreneurs with volatile earnings may accrue far fewer benefits over a lifetime than will long-time employees with steady earnings. Even very successful businesses have years of losses, at least from the owner’s tax perspective, so that could lower Social Security contributions and therefore eventually benefits.

Work Past Retirement Age

So how does somebody improve his or her benefits, even with some low-earning years?

My mother, age 76, presents an interesting data point on Social Security benefits, which she has been collecting for the last six years. After raising us kids, she racked up some low-paying years during her career as a private school teacher. She continues to work as a consultant now, however, making decent income well past her full retirement age. Because Social Security benefits depend on calculating your highest 35 working years, her recent income years – in her mid-70s – have been slowly replacing lower earning years from her 40s. As a result, her monthly Social Security check has adjusted upward by a little bit each year.

Katrina Bledsoe, Management Analyst at the Dallas region Public Affairs Office of Social Security, confirms that this upward adjustment should happen automatically every year, if you continue working. If you don’t see the automatic adjustment, Bledsoe says beneficiaries may contact their Social Security office. Don’t do so until the 2nd quarter of the year, however, because Social Security will need to see your official IRS tax data to recalculate benefits, and that generally doesn’t happen before April 15th.

Two final Social Security thoughts. Monthly benefits generally are not enough to live on, comfortably, in retirement. Social Security payments should be thought of as a living supplement, not a sufficiency.

Two final Social Security thoughts. Monthly benefits generally are not enough to live on, comfortably, in retirement. Social Security payments should be thought of as a living supplement, not a sufficiency.

On the other hand, as much as 40 percent of American households do not have appreciable retirement savings. The median net worth of Americans between ages 65 and 74 is $224,000. With that statistic, we can see that Social Security constitutes the single most important source of funds retirees have to live on.

To do some simple math 1 for which I don’t even need my cool spreadsheet, I would divide annual benefits by 5% to get a rough value of Social Security for an individual, as if it were the equivalent of a lump sum in the bank. That would make $2,500 in monthly Social Security benefits worth $600,000. That rough estimate shows us that Social Security is the largest safety net that a majority of Americans have.

Please see related post:

Social Security Nerdy Spreadsheet Part I – The Rabbit and the Hare

Post read (767) times.

- And please don’t @ me to quibble about this last math assumption. Chill. I’m creating a quick and rough estimate for comparisons’ sake. Thank you. ↩