Podcast: Play in new window | Download

In this interview, Julie – a college advisor, offers her perspective on the rising cost of college, which has become financially unfeasible for most middle class families in the last 25 years.

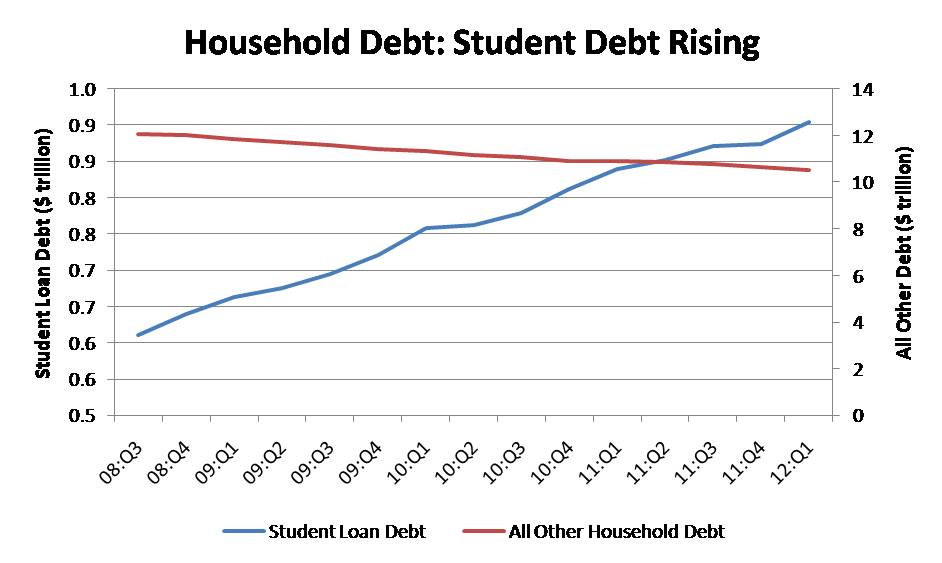

Please see related post on Compound Interest and College Savings

THE INTERVIEW:

Michael: Hi, my name is Mike and I used to be a hedge-fund manager.

Julie: I’m Julie. I am a college advisor for over 25 years.

Michael: I’m interested in the perspective of a private college school college guidance counselor. But understanding that for many or the majority of people, they are not in private school, so your financial picture will be a particular slice of American life. In your experience have parents typically prepared for the cost of college by the time the student is getting to their junior year, or are they taken by surprise?

Julie: Actually my parents are not particularly rich. We’re not in a very affluent area and so a lot of my students have financial aid at our school, even though we’re only a day school and don’t have a very high tuition.

Most parents, however, have not been able to prepare for college because if they are thinking in terms of a private college in the northeast where we live, the cost now is 55,000 dollars or as much as 60,000 dollars. It’s very hard to save that money, even if you start the day the child was born. That’s a very hard thing to prepare for.

CALCULATING BORROWING NEEDS FOR COLLEGE

Michael: I went to the College Board site that you pointed out to me, and inputted some of my information. Indeed, although we don’t feel like we have a lot left over at the end of any month or year, it’s a 49,000 dollar estimated obligation according to the College Board, for a typical four-year college. It’s kind of a scary experience to put in your numbers and think I’m not wealthy; I’m just kind of ordinary getting by here, and yet the institutions are basically saying “thanks for your numbers; you’re going to pay-“

Julie: 200,000 dollars at least for college. You’re the banker. How much would someone have to be saving every day, every year, from the day a child is born to have 200,000 dollars by the time the child was 18? Even if they got 8% return, which they’re not getting anymore, how much would they have to be saving every year?[1]

Basically I will mention to people you’ve got to run these numbers and that was junior year I brought it up. But they [the parents] don’t want to run them because they don’t want to know. So senior year rolls around and they may not have even run the numbers. Then I can’t give very good advice because if they have 200,000 in the bank or they have a very high income which means they could scrape up 50,000 a year, after taxes, that’s one thing. But that’s not the majority of people.

If they’re not going to get very much in financial aid, they really need to be thinking what is a lower cost college, what could I have instead. That’s going to have to be either a state university, possibly a Canadian university. Maybe they could go overseas, but they can’t go to a private college in the northeast.

Michael: Among the private school families then that you’re dealing with, what percentage of parents or kids or the combination are willing to forego the high cost, presumably higher status college to go for the lower-cost approach? What percentage of your 25-30 students are actually making that choice at the end of the senior year?

URGING AGAINST TOO MUCH DEBT

Julie: That’s a good question. Last year I had a lot of students who at my urging were trying to avoid high debt. The problem is that you can get into a college that costs 55,000. Your parents can maybe come up with some money, and then the college might even give you 15,000 or 20,000 but there could then be this gap between what you can squeeze out from the home income and the small amount of financial aid you’re eligible for. That gap can be easily filled by borrowing by the student. The colleges will help arrange for the kid to borrow 15,000 or 20,000 dollars. I don’t want them to do that.

Michael: To what extent are those families who are choosing to fill the gap with 25,000 dollars of a student-loan debt, in your opinion are they fully understanding the implications of the debt or are they saying there’s nothing more important than a college education for my child so I’m doing it, or do you think they’re closing their eyes and doing what we would in another context say it’s really irresponsible to run up 25,000 dollars of credit-card debt? Yet they’re doing it in another form through student-loan debt because student-loan debt is considered good debt. Are your families walking into this with their eyes open?

Julie: Recently, I think a lot of them have taken my advice, which is they don’t want to do that. They’ll choose the option that has the lowest debt. But that will still be at least 5,000 dollars for the student. If you can get into Harvard, maybe it’ll be less. Wellesley – that’s pretty good financial aid. There are a few places that are so rich they really give significantly better financial aid than every place else. But most students are facing at least, if the parents don’t have the full amount, at least $5,000 a year in debt.

Michael: Which is $20,000 at the end of four years.

Julie: Right, but most of the packages will be closer to $12,000 to $15,000 per year.

HISTORICAL COMPARISON

Michael: So you’re getting up to $45,000 dollars worth of debt or $60,000 dollars worth of debt for a 22-year old. What is the historical comparison? Have you been doing this for close to 30 years, what was it like 30 years ago?

Julie: The problem is my children went to college 20-30 years ago. It was expensive but it was manageable. But in the last 25 years, the rate of increase of the cost of college has been astronomically much higher than the regular cost of living increase. You have 2-3% cost of living increase and you’ve got 7-8% every year compounding in the cost of college. The numbers now simply don’t work. What was a sacrifice for people 20-30 years ago is now simply an impossibility without tremendous debt. Of course, the starting, average salary for a college graduate has actually in real dollars declined over the last 20 years. It’s a pretty scary situation.

IS THE COST OF COLLEGE A BUBBLE?

Michael: In financial terms there seems to be an analogy between, say, the housing bubble that we experienced from 1998 to 2008 in which that asset price – housing price – went up by 10-15% per year, year-over-year, and yet peoples’ incomes didn’t increase to that extent. If the nominal rate of inflation is 2%, and the price of college is going up 7% year-over-year for 10-15 years, it does seem to be an unsustainable sort of asset-price bubble, analogous to the housing market.

Julie: What you have are the most expensive, elite colleges, are heavily populated by very affluent people, even though a place like Harvard or Princeton will give tremendous financial aid; they still have 75% of their applicants, are pretty well off.

Michael: One of the thoughts I had in your discussion of the asset-price bubble of college tuition, if indeed that’s what it is, is the relationship between the cost of debt which got very low – the cost of mortgages, mortgage rates were very low while asset prices were going up. At the same time analogously the student loan debt is extremely cheap from an interest rate perspective, which kind of helps subsidize the extraordinary principal amounts of student-loan debt. If it’s at 3.5% you can carry 50,000 dollars, whereas if it was at 8% or 10%, where it might have been 30 years ago in the ’80s, you can’t really carry 50,000 dollars worth of debt as easily.

But it’ll be interesting, as it is real estate reacts very quickly to changes in interest rates, if interest rates go up, real estate prices typically drop quickly. It’ll be interesting and unpleasant presumably for universities, if interest rates go up and suddenly people can’t really carry 50,000 dollars of what was previously 3% debt, then becomes 7% debt. There has to be a reaction to that, although the government is heavily involved in the student-loan market, keeping it low.

Julie: There’s no question that if the government had not been subsidizing these loans and making them so easy to get, that we’d have a different situation. On the one hand, we’d have even more of a premium on being well off to be able to go to college. On the other hand, colleges might not have been able to increase their costs and prices as they have by 7% and 8%. Because where would the money have come from? A few elite schools are going to be able to price it at almost anything, but I don’t really see how all the small private schools that are not highly regarded are going to be able to keep up this situation.

COLLEGES GET PRETTY MERCENARY

Julie: I’ve had people come to my office who are representing the college, and they’re admissions officers out recruiting. I’ll say what about this student, would this be a likely fit for your college? Would she fit the profile for admission? If I mention the person is a full pay, they’ll say “Yeah yeah, full pay, I think they’ll probably get in.”

Michael: That’s pretty mercenary.

Julie: It’s pretty bad. But they’re just being truthful. That’s now almost your best bet for admission, not at the most competitive school, but at many, many, being a full pay is going to be very useful to you. And if you’re a full pay at any college other than the most elite, you’re likely to get a discount. For a college that charges $55,000 and you’re basically a full pay, they’ll discount it by $10,000 or even $15,000 because they’d rather get someone who’s paying $40,000 than have to subsidize someone who can only pay $10,000 or $20,000. That’s what the whole merit aid system is; it’s a subsidy for the people who are basically full pay but might come to your school, your college if they’ll discount the tuition. Outside the elite colleges, all schools are giving merit aid, discounting the price. The discount is bigger for students with high scores and good grades.

The sticker price is not true for a decent student but it’s still too high. You’ve read in the New York Times there are middle-class families whose children are going to community college for a year or two, and then if you have to borrow $15,000 or $20,000 a year for the last two years, that’s not so bad. That’s certainly a strategy I recommend.

Michael: Is there any good news? What kind of students get financial aid or merit aid or sport scholarships or international students? What do colleges actually pay for, anything happy?

Julie: Anything happy? They’re trying. The colleges aren’t trying to rip people off. But they have for some reason felt that their college needed to be spending money and raising their price by 7% or 8% when inflation wasn’t anywhere near there. That’s where I’m critical of the colleges. I’m critical of this huge change in how many teachers there are. There isn’t a huge change. But how many administrators there are, there’s a huge change. Why is that? What became so hard to manage?

Michael: The mean version would be the students need to have their coddled lives, but maybe I just sound like an old person resenting those college students having a good time.

Julie: I don’t think it’s probably related to the kids as much as bureaucracy tends to grow. That’s just the way it is. And if the money is there – or seemed to be there – because it was easy to borrow it, for the students, where would be the incentive for them to lower prices, never mind hold the line?

Please see related posts:

Interview with College Counselor Part II – Is the college financial model broken?

College Savings and Compound interest

College savings vs. Retirement savings

[1] I recommend readers turn to this post, in which I discuss the amount of money we might need to save to have enough. Also, I recommend inputting your own numbers into the College Board’s calculator, to figure out scenarios for you and your family.

Post read (6122) times.

2 Replies to “Interview Part I: Advisor on the Rising Cost of College”

The cost of tuition has become obsessively high. When students graduate with such a high student loan amount, they are delayed in progressing in life.

Agreed! We need to think before we leap into debt!