My littlest one turned four years-old last weekend1, and my eight year-old is taking a Texas-Public-Schools-3rd-Grade-State-Mandated-High-Stakes-Standardized-Test this week2, so you can probably guess what’s on this ex-banker’s mind:

Time is quickly running out for me to save money for their college tuition.4

The only thing scarier than those scary scary clown head trash cans at my littlest daughter’s birthday party5 is the prospect of saving enough money for her college tuition.

For my eight year-old, I’ve got just 10 years to go before C-Day, so I thought I’d share my current ex-banker thoughts with others, in the hopes that we can experience this horrific fear together.

Also, “saving for college” allows me to discuss my favorite topic (compound interest!) so that’s always a good enough reason by itself for a Bankers Anonymous post.

I see three big questions about college savings, with the most interesting one being #2.

Question #1: What college savings account or investment vehicle, if any, should I use?

- Question #2: How much do I need to save, per month, to be totally set for college tuition payments when they arrive? (Compound interest calculations coming up! Yay!)

- Question #3: What kind of investments do I need in my college savings account?

I’ll take these in order.

Question #1: What savings account or investment vehicle, if any should I use?

Open up a 529 College Savings account.

Ok, that was easy.

But, why a 529? Also, which one?

The first “why” is because you may get an income tax advantage when you make a 529 account contribution, depending on the state you live in. When I lived in New York and paid New York state income tax, I enjoyed an income tax break on my contributions. Now that I live in Texas, I get no state income tax advantage from 529 account contributions.6 So that may, or may not, apply to you.

The second ‘why’ is that any capital gains or investment income – which might be triggered when I sold stocks or earned interest on my investments – remain protected from taxation in that year, assuming I do not make withdrawals from my 529 account. If I just held my college savings in a regular, taxable, brokerage account, I’d be required to pay taxes on capital gains or other income from my investments. The result of this 529 account tax protection is that I can grow my money much faster than in a regular, taxable, brokerage account.

Ok, so that sounds good, but which 529 account should you open? Probably you should start by investigating your own state’s offering7, precisely for that potential income tax break. But if you live, as I do, in a state without an income tax, then you can consider other advantages, having to do with

a) Contribution limits – Some states allow higher contributions than others

b) Flexibility of investment choices – some states offer restricted types of investments

c) Cost of available investment choices – some states offer higher-cost plans than others

d) Convenience

I opened a New York state account for my oldest daughter because we lived there, then. My youngest was born in Texas, but I opened a New York state account for her as well, purely for convenience sake. I prefer tracking both girls’ college savings information on a single website.

Question #2 – How much do I need to save, monthly, to have everything covered?

The College Board (The fun group that brought you the SAT, the PSAT the AP tests, and more!) has a couple of incredibly useful online calculators.

First, they can help you figure out how much of college’s cost you, as a parent, will likely have pay. To try the calculator, go here.

This calculator asks some specific questions about your family situation, plus your income and savings, and then tells you how much the financial aid department of a college will likely expect you to contribute for your child’s annual college expense.

Beware, because [**Spoiler Alert**]

This number will be much higher than you want it to be.

I don’t think of myself as wealthy, and generally we don’t have much left over at the end of the month. Which is why the expected contribution number from a typical financial aid department left my face feeling a bit tingly.

Is it getting warm in here, or is that just me? My editor-in-chief 8 thinks I’m either suffering from menopause or anaphylaxis based on these symptoms. We’ll just have to wait and see.

Next, the College Board has a great college savings calculator to tell you how far your current plan will go toward paying for college. Before you go there, I’d like to warn you – the result is scarier than scary, scary, clowns.

First, you input the current cost of college, an assumed rate of tuition inflation, how many years your child will attend, and how much you will likely have to pay, which you may have some idea about based on the first online College Board calculator above. Next, you input how much you’ve already saved, what you expect your annual investment returns will be, how many more years you have before your child goes to college, and how much you plan to contribute monthly, between now and then.

You input all of that, and then you have a heart attack immediately and die, because there’s Just. No. Way.

I personally can’t feel the whole left side of my face right now.

For example, let’s say I’ve managed to put aside $19,000 for my 4 year-old up until now.

Looking good, Billy Ray.

And let’s say I plan to invest $200 per month until she turns 18, and I can earn a 7% return on my investments, via my 529 account.

Feeling good, Lewis.

Also, assume a private 4 year college costs $50,000 per year today, the college cost inflation rate is 5%, and I plan to pay 90% of that from savings.

I have an estimated shortfall of $276,399.

Randolph, this isn’t Monopoly money we’re playing with.

Some of you clever readers may just be smirking because your little darling will likely either get a ton of scholarships or else attend a state college, no?

Well, the bad reality is that state college isn’t that affordable these days either.

The average 4-year in-state tuition cost, according to the College Board, will set you back $21,477 this year.

If I have zero savings for my 4 year old, but I manage to invest $200 per month, starting now, and she attends an average cost in-state college, I’m still $107,582 short, 14 years from now.

The answer to the question “how much should I be saving per month to be totally set for tuition” is provided by the College Board calculator, just under the shortfall number.

I’m sorry about this, but as you know: Compound interest is powerful.

After you recover from this shock, you’re ready to move on to question #3.

Question #3 – How should you invest your child’s 529 Account?

This one’s easy, and frequent Bankers Anonymous readers will not learn a single, damned, new thing from me here, because the answer is unchanged from previous, similar questions about how to invest for the long run.

Hopefully you noticed, from playing around with the college board’s calculator, that you need a fairly high rate of return on your investments from now until college to even have a chance of closing the gap between your current savings and how much you’ll owe for your child’s college, every year, for four years.

Now, since returns have to be high, you have precisely one choice for how to invest: 100% equities.

Let me further clarify, in a way that will again make me sound like a broken record for careful readers: You need to invest your long-term savings for college in a highly diversified low-cost (probably indexed) mutual fund, invested in stocks only.

Why 100% equities?

Why not bonds or other safe investments? Two reasons.

The first reason is low returns. For the vast majority of us, we can’t afford to invest in bonds over the medium to long run. An intermediate-term bond fund will return somewhere between 0.5% and 2.5% right now, and that’s just not going to cut it.

The second reason is that – on a probability-adjusted basis – you will get more from investing in equities.

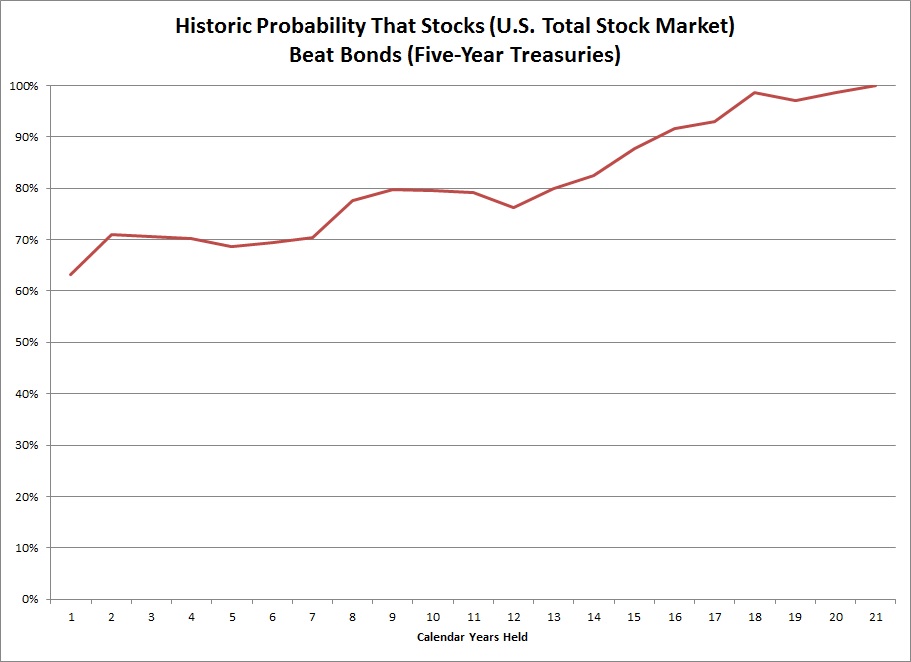

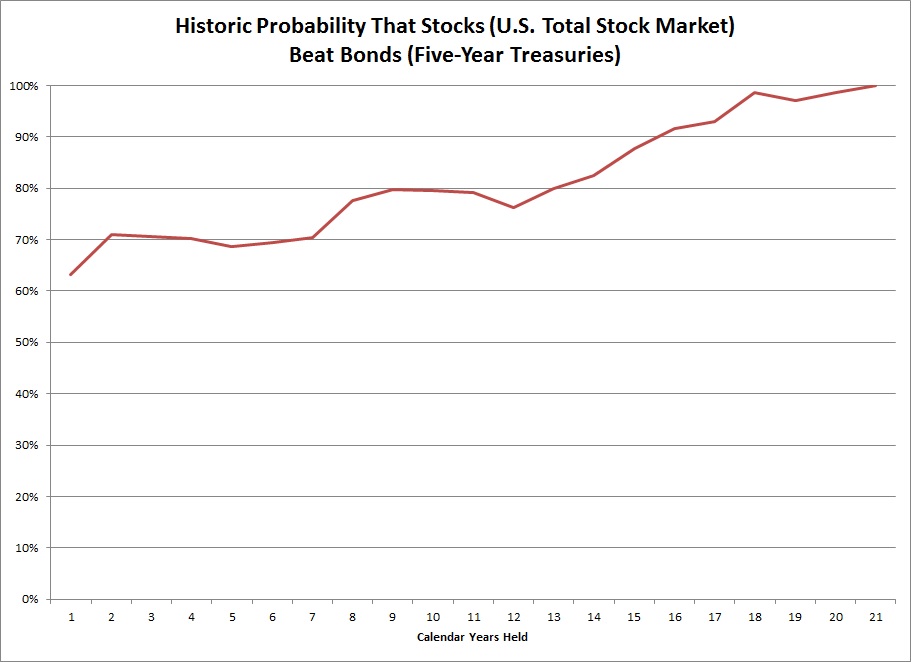

Here are the relevant facts to back up my assertion, as well as a cool graphic of these statements 9

{kind=link}

If you have a 5-year investment horizon, you will be better off entirely in stocks, rather than bonds, 70% of the time.

If you have a 10-year horizon – as I do – you will be better off entirely in stocks rather than bonds, 80% of the time.

If you have a 15-year horizon – as I do with my youngest daughter – a 100% stocks portfolio10 outperforms a 100% bonds portfolio 90+% percent of the time.

Is that guaranteed? Of course not

Probabilities are not the same as guarantees,11 so of course the bet you make on investing in 100% equities in your child’s 529 account could go wrong. But making the other choice – including bonds in your portfolio – is a low probability bet. By investing in bonds you are implicitly saying “Probabilities be damned! I don’t care about history! This time is different!”12

Look, I play poker with the neighborhood dads, so I know that low-probability bets sometimes work out. But I also know it’s kind of stupid to make low-probability bets. Trust me, because I’ve been losing $20 a week on a regular basis to these guys, testing this hypothesis, since I’m not a strong poker player.

You can decide to weigh down your kid’s college savings account with bonds, and you may be under the illusion that this is ‘prudent’ because they’re bonds and “bonds = safe.” But it’s not prudent, any more than it’s prudent to bet with jack seven off-suit.

Would I advocate investing in 100% equities if my kid is going to college next year?

Well, this gets trickier. Stocks still beat bonds in most years, so if you want to play the odds – and if you have some kind of cushion – you could reasonably keep the account in stocks. Most of the time – on a probabilistic basis – this would be a winning choice.

But I realize this seems a bit extreme, so with one year to go I’d probably take next years’ tuition (potentially only 1/4th of your position) and plunk it into a risk-free investment, like a money market fund13, and leave the rest exposed to stocks. Remember, 3/4ths of your account has more than one year to remain invested. Each additional year invested increases the probability that stocks beat bonds.14

Tick Tock Tick Tock

For my wife and me, that loud ticking we hear is not the biological clock anymore, but rather the college financial clock.

For anyone in our demographic15 who checked the College Board calculator,16 I’ll now sum up the only other good pieces of advice I can think of related to saving for college.

- Open up a 529 Account for each kid. Like, right now. Stop reading blogs and do this immediately. Really. Did you do it yet? How about now?

- Set up an automatic withdrawal from your bank account, so you don’t have to make a choice about contributing every month. Because if you have to make the choice every month, the money might not be there. Even $25 per month in automatic withdrawals is better than nothing. Increasing that $25 monthly contribution over time, once the account is open, will be much easier than you think.

Best of luck!

Please see related posts on:

Interview with College Advisor Part I – The insanely rising cost of college

Interview with College Advisor Part II – is the 4-year college financial model broken?

New York Times on funding your 401K Account vs. 529 Account

And related post: Stocks over Bonds – The Probabilistic View

And related post: Ask an Ex-Banker: Should I open an IRA?

Post read (12748) times.

- Kiddie Park, established in 1925! A Merry-Go-Round from 1925! Scary, scary, clowns! Oh my! ↩

- First, take the Pre-Test! Then the Practice Test! Then the Real Test! Oh my! ↩

- As Dora the Explorer would say. ↩

- My wife and I like to jokingly append “–should they choose that path,” whenever we discuss our daughters going off to college, but the fact is that’s our chosen path for them and they can deviate from it at their peril. I’d like to see you just try it, kiddo. ↩

- Everything you need to know about my view on little kid birthday parties was captured recently by Drew Magary at Deadspin.com. We have got to do something about the Big Birthday Industrial Complex. ↩

- In a news item that may or may not be directly related to this fact, my local urban school district boasts 7% college readiness among its graduates. I will now light myself on fire. ↩

- Here’s a nice website for getting starting comparison shopping for 529 accounts. ↩

- aka wife. Also, she’s an MD ↩

- Courtesy of David Hultstrom at Financial Architects LLC. ↩

- Hopefully the following is obvious, but just in case it’s not: When I say 100% stocks I mean a highly diversified mutual fund, not an individual stock or even a small group of stocks, or a single stock sector. When I say bonds I really mean a AAA-rated bond fund of, say, intermediate duration. Not junk bonds or emerging markets or anything else interesting and high-yielding. ↩

- As my close, personal friend, Nate Silver would say. (I wish.) ↩

- “This time is different” is one of those investing No-Nos as a justification for making an investment decision. “This time is different” is a fine gambling notion (for investing in individual tech stocks, for example, or buying into a venture capital fund) but is not a fine investing notion. ↩

- Why a money market fund and not a bond fund? Because a bond fund, with only one year to go, could actually lose money as well – in a rising interest rate environment – so only a money market fund guarantees you zero volatility of results. ↩

- Incidentally, investing today for your kids’ college next year is NOT the way to do this. Sorry if you are reading this with a 17 year-old breathing down your neck. 529 accounts have little to offer in this case, and compound interest can’t help you much either. ↩

- Meaning, you’re going to pay for some kid’s college some day. ↩

- And if you haven’t yet used the calculators, have a swig of whisky and then seriously you should go check them, it’s the right thing to do. ↩