Editor’s Note: A version of this post appeared in the San Antonio Express News.

In Praise of Susan Combs

As we elect a new crop of public officials in Texas this week let’s take a moment to appreciate an outgoing official, Susan Combs, Texas Comptroller of Public Accounts.

As we elect a new crop of public officials in Texas this week let’s take a moment to appreciate an outgoing official, Susan Combs, Texas Comptroller of Public Accounts.

As Comptroller, Combs served as a combination tax collector, check writer, and fiscal scold for the state.

Praising an elected official for a job well done is a deeply unfashionable activity, especially for someone like me who’s in the habit of writing critically.

I typically perceive our leaders as flawed vessels powered by ambition and ideology, and that my job is to expose them as such. But I need to praise Susan Combs.

A friend of mine knowledgeable about State politics burst my Combs bubble a little bit last week, arguing that Combs too was fueled by ambition and ideology during her tenure in office.

So be it. She is human.

But I love what she did as Comptroller!

In my personal political theology, every time one department of government lights up the financial darkness of another part of government, an angel earns its wings.[1]

Let me give you some specific examples of how Combs worked for the angels.

Things I love about Susan Combs

Combs made state, county, city, and school financial data available and searchable in a way that I don’t recall seeing from any other state.

Combs’ signature move during her time in the Comptroller’s office was to open up information on public expenditure in Texas to the disinfecting light of day.

As her website biography boasts, she put all of her agency’s expenditures on the web in her fourth day of office.

See, that’s what I’m talking about! Normally by the fourth day at a job I’d still be fiddling with the stupid espresso maker, trying not to spill coffee grinds all over the counter again. But Combs posted all of her office expenses online for the world to see.

I love, specifically, her office’s www.TexasTransparency.org website, with databases and special reports on public debt and public taxes.

For the site, Combs’ office requested, compiled, organized and made searchable a myriad of financial data points on Texas finances.

I highlight two of my favorite databases below.

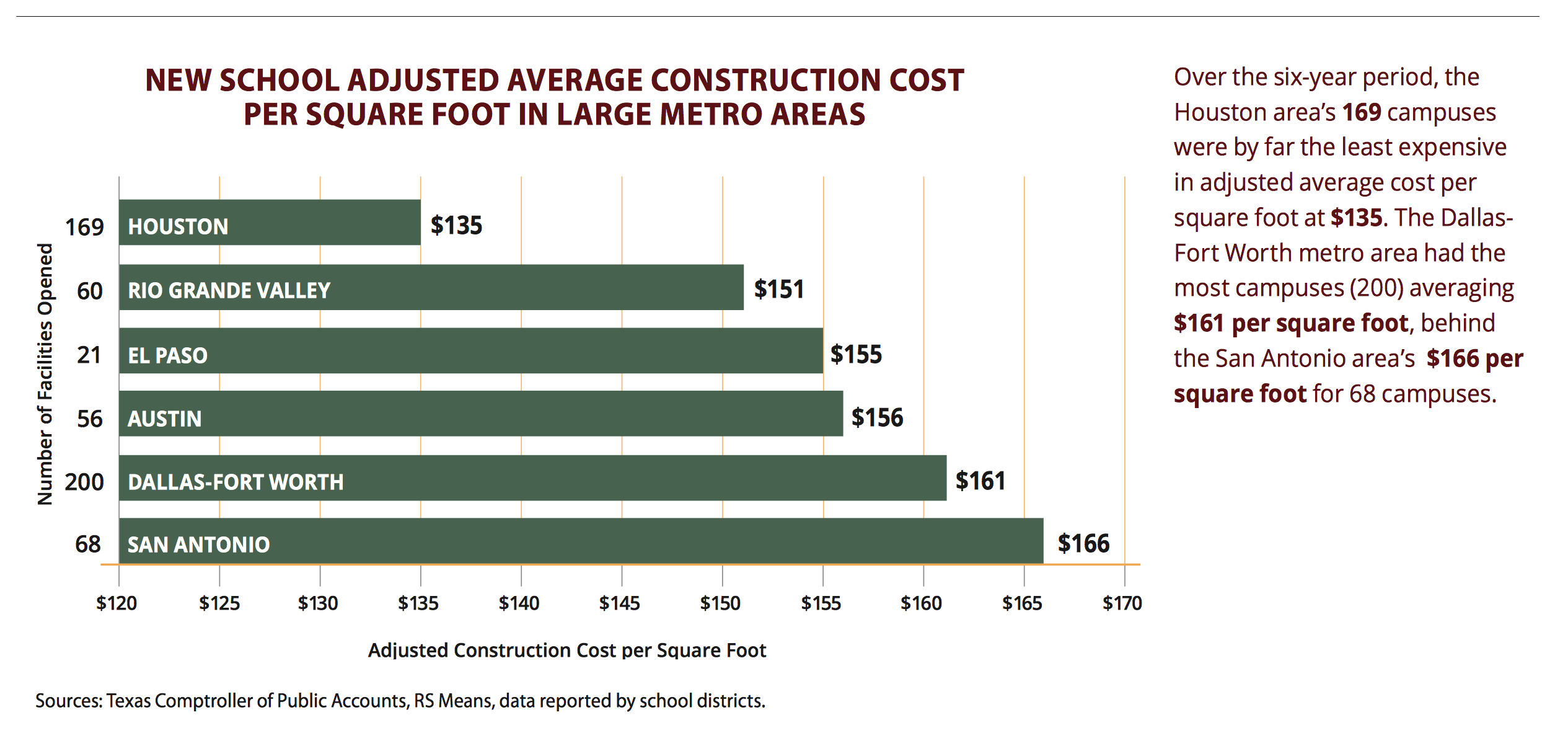

The cost of public school building construction

More than an ordinary citizen-taxpayer interest, I have a personal interest in the management of public schools in San Antonio, as my oldest daughter attends 4th Grade in San Antonio ISD.

We’ve loved her teachers for the past five years. We like her school community.

But let’s just say I have my doubts about SAISD leadership. I feel that there’s too much emphasis on real estate opportunities among some parts of SAISD’s leadership. Which makes me wonder about the following question:

Are school building costs high in San Antonio?

As private citizens, we have practically no chance of putting together enough comparative data from all over the state to study the cost of building in public schools

But Susan Combs’ office has the power to demand that data and make it available on the Texas Transparency website.

Uh-oh San Antonio – You’re paying too much

Taxpayers of San Antonio may be interested to know that the cost of school construction is higher here (per square foot) than any other large metropolitan area in the state – higher than Houston, Dallas, Austin, the Rio Grande Valley and El Paso.

I find those statistics particularly troubling, given that real estate and labor costs are generally lower in San Antonio than many of those areas, such as Houston, Dallas, and Austin.

I’d love to hear a plausible explanation for why we’re paying more to build schools here compared with other cities.

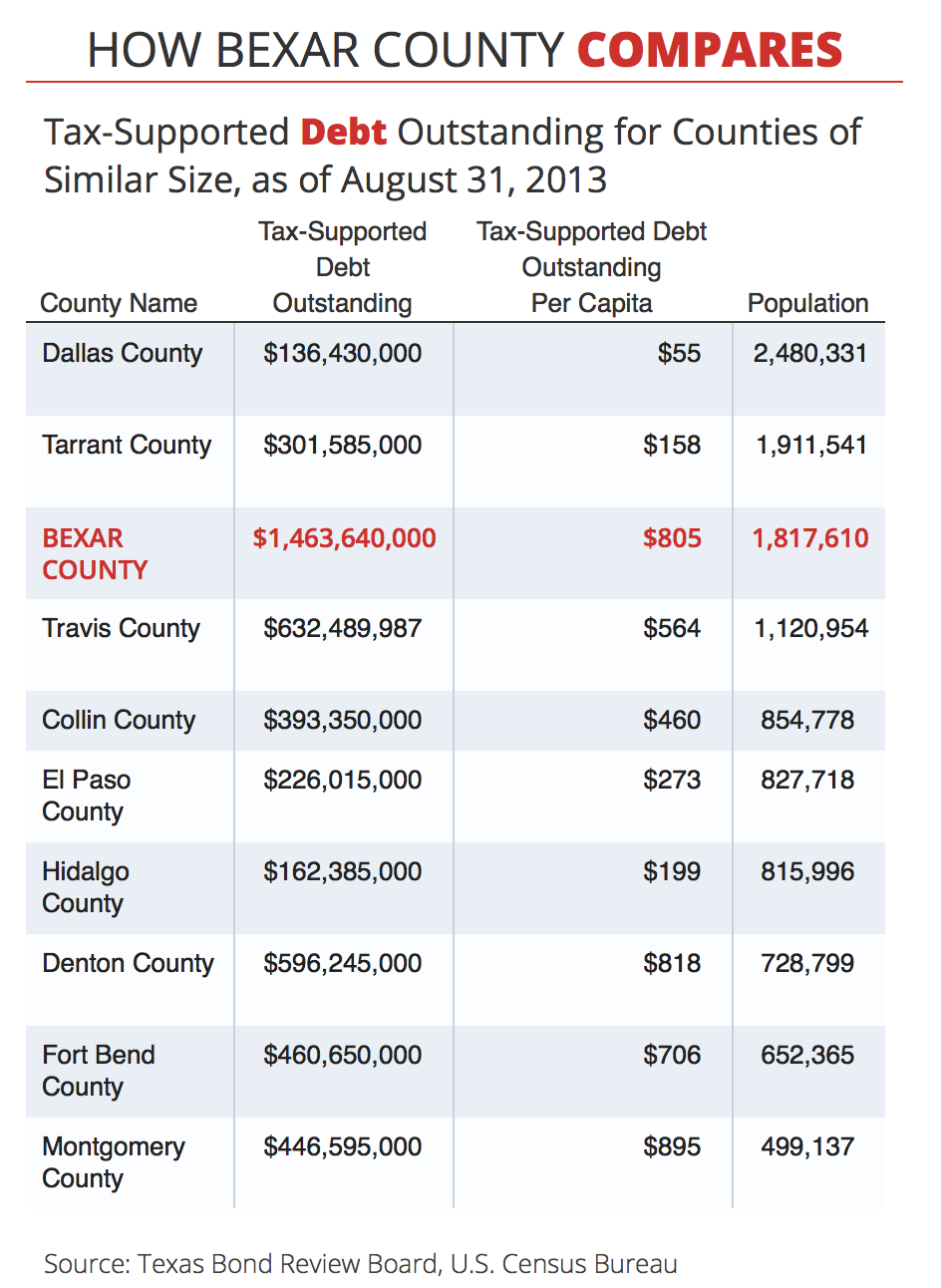

County Indebtedness

What other kinds of information does Combs’ data provide?

Would you like to be able to compare the debt-per-person that counties have incurred?

Yup, that’s in a searchable database compiled by Comptroller Combs as well.

Uh-oh, Bexar County – You owe more

You may be interested to learn that the debt per person in Bexar County sticks out like a sore thumb. Our tax-supported debt per person is way higher than the next 5 closest counties in size: Harris County (Houston), Dallas County (Dallas), Tarrant County (Fort Worth), Travis County (Austin), and Collin County (Plano).

Why are we more heavily indebted per person in Bexar County than anywhere else?

By, like, a lot?

I don’t know. Let’s ask our elected officials.

In the meantime, please join me this week in a slow clap for Combs’ career in Austin. I’m impressed.

Please see related posts:

A review of SAISD President Ed Garza’s real estate deals

Ed Garza responds on contracting with VIA

Ed Garza responds on real estate

On SAISD Superintendent candidate Manuel Isquierdo – Do You Believe in Coincidences?

[1] I’ve often praised the yoeman’s work of Neil Barofsky, the original watchdog for TARP money, known by the Norse God – sounding acronym SIGTARP. He did an incredible job of shining light on the darkness of the 2008 mortgage crisis bank bailouts, all while employed as a special Congressionally-mandated investigator under the Treasury department, thereby somewhat restoring my faith in our government’s ability to self-criticize and improve in the future.

Post read (1397) times.