Last night completed Day 30 of the “Allowance Experiment,” in which I offered my eldest daughter a daily payment calculated as 10% of her allowance savings, compounding daily. On day 1, she began with an initial grub stake of $1. She received $0.10 on day 2 (10% of $1) and $0.11 on day 3 (10% of $1.10), and so on.

By Day 30, however, due to the magic of compounding, the daily payment grew to a substantial $1.44. At the end of 30 days, she had $15.86 in the money jar. That’s a pretty good sum for an 8 year old, because she can buy any ice cream her little heart desires, and $15.86 is also approximately 1/1000th of the way to obtaining an American Girl Doll.[1]

With this kind of experiment, one must stop after about a month. Otherwise – because compound interest turns money into kudzu crossed with HGH crossed with a mutant Godzilla[2] – by 6 months of this I would end up paying her $2.1 million per day, and she would have over $25 million in her jar. At which point obviously I’d be asking her for a daily allowance.

Plus with $25 million in the bank she could afford to purchase approximately 2 American Girl Dolls at the same time.[3]

Unexpected benefits

As I wrote before, one of the beneficial side effects of the allowance experiment – because I required her to do the daily interim calculations of 10%, plus adding up the totals in the jar – was appropriately difficult math for a 3rd grader. This is smart parenting.

If her math errors worked in my favor, well that’s just good banking practice

You know what else is smart parenting? When she messed up the calculations. For example, when the 10% number she calculated ended up larger than it should have been, I immediately pointed out her error and asked her to try again. I was not about to pay any more than I had to.

But what about when she messed up the calculations and it worked in my favor? What about when she asked me to pay less in compound interest than I should?

Well, let me just say that all’s fair in love, war, banking, and parenting. I mean, you can take the Dad out of Goldman Sachs, but you can’t expect to take Goldman Sachs out of the Dad, now can you?

Plus, as (my guide to all good parenting practices) Jack Handey points out, kids like to be tricked.[4]

The main point, accomplished

All jokes aside, the point of this experiment was not so much to induce savings or to teach basic math, but to viscerally illustrate the powerful force of compound interest.

I asked her if she understood the way in which money grew at an accelerating pace with regular 10% compounding. She responded with a wide-eyed, “Yes, it gets really big.”

[1] That last number is just a price estimate based on gut feeling. I haven’t looked it up.

[2] “Kudzu crossed with HGH crossed with a mutant Godzilla” is the name of my new favorite funk band. Also, I’m going to copyright it as a title for my book on compound interest, so don’t even think of copying it.

[4] From the parenting guru himself: ‘One thing kids like is to be tricked. For instance, I was going to take my little nephew to Disneyland, but instead I drove him to an old burned-out warehouse. “Oh, no,” I said. “Disneyland burned down.” He cried and cried, but I think that deep down, he though it was a pretty good joke. I started to drive over to the real Disneyland, but it was getting pretty late.’

In summary form, he advises paying ‘daily interest’ on a small nominal starting amount, over a period of 1 to 3 months, so that kids can viscerally feel the money-grows-money magic of compound interest.

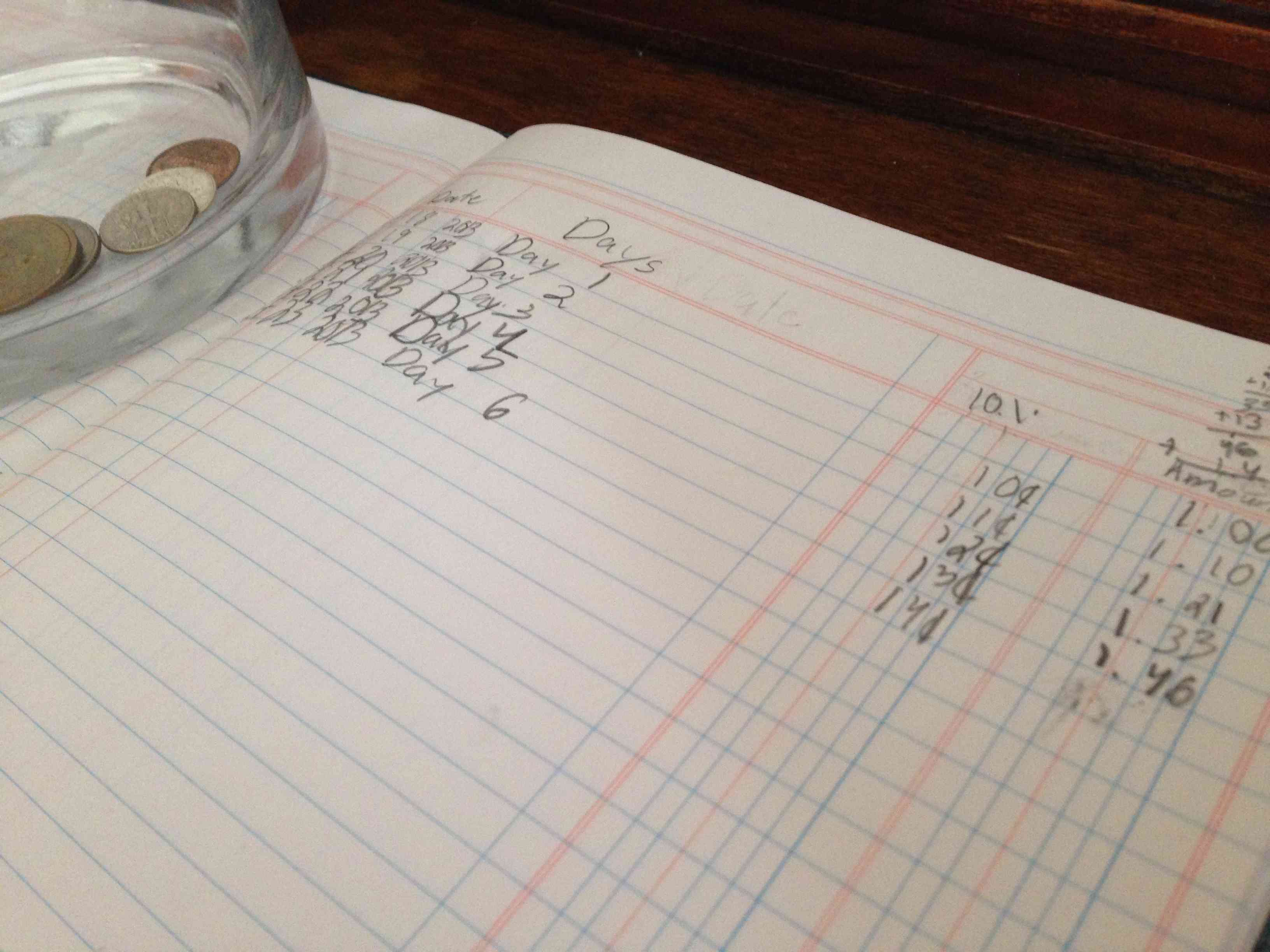

For my daughter I paid $1 into a glass jar on Day 1. Further, I have promised to pay her 10% in ‘daily interest’ on all money accumulated in the jar, over the course of 30 days.

For example,

Day 2 I paid 10 cents (10% of $1).

Day 3 I paid 11 cents (10% of $1.10)

Day 4 I paid 12 cents (10% of $1.21)

Day 5 I paid 13 cents (10% of $1.33)

Day 6 is today.

Your update on that project is as follows: This is even better than I expected, because of some unexpected consequences of my requirements.

I asked my daughter to document her 30 days of allowance in a lined journal.

One column shows the date, while the next column has the day number. The third column shows the daily 10%, while the final column lists the accumulated total in the jar.

I required her to calculate 10% of the total each day, as well as add up the totals on her own. If she wants to get paid, she needs to do the math. It’s a small step, but I’m so happy I required this.

A digression

I sometimes walk around my neighborhood wondering whether all of the world’s ills could be solved if people knew how to quickly and accurately calculate percents of things. Wouldn’t it all be better if we really understand discussions of percents of things?[2]

Am I the only one who thinks this? The Federal budget, poverty in America, tax policy, retirement savings, or properly tipping the bartender – I mean we’d all be better at all of these key problems if we could only calculate 5%, 10%, 15%, 20%, and intuitively understand what they mean.

When I see my daughter moving the decimal place over one numerical place to figure out 10% of her allowance jar savings, a little part of me jumps up and jauntily jigs with joy. Because this is a good life skill, and also SHE WILL BE THE NEXT FED CHAIRMAN TO SUCCEED JANET YELLEN.

The next math consequence– rounding numbers.

In addition to teaching compound interest, and teaching the calculation of percents, another math concept arose today. On day 6, she has $1.46 in the jar. Well, the contribution amount today isn’t 14 cents now is it?

My daughter is in third grade, and they’ve talked about rounding numbers, but this is probably the first time she’ll get to materially benefit from rounding up numbers. That’s right, 15 cents goes in the jar today. The numbers are starting to add up quickly.

I understand I derive an inordinate amount of pleasure from teaching my kid these math concepts. But is there anything more important right now?

[1] My managing editor (aka wife) had allowance requirements for my 8 year-old too, such as “pick your crap up off the stairs and put it back in your room where it belongs.” But you can see that kind of stuff further described in the Mommys-Anonymous.com blog.

[2] We can all agree that the world’s ills could be solved teaching the calculation of percents, plus empathy. But if I had to choose between teaching empathy and the calculation of percents, well, shoot, which do you think I should do? I kid, I kid. I’m an ex-banker. OBVIOUSLY ITS CALCULATING PERCENTS.

Parents will recognize the following as the “If You Give a Pig a Pancake” problem, referencing the ubiquitous children’s book about giving a pig the first thing (a pancake) which leads to the next thing (some syrup), which leads to the next thing (a napkin), and so on.

For those of you who have not been parents in the past twenty years and aren’t familiar with the pig-and-pancake problem, file this one under the “Department of Unintended Consequences” Tab.

Fast forward a few weeks to a conversation she had with my Managing Editor (aka wife) last night.

“Mommy.I need money.”

“Why?”

“There’s a book fair at school but Daddy took all of my money and put it in stocks.And stocks are not fun at all.”

“I’m sorry dear.”

“Can I have an allowance?”

“Let me talk to Daddy.”

Ugh.It is true that I took all of her money.And converted it into shares of Kellogg stock.

And it’s also true that the steady stream of loose teeth – her main source of revenue via the Tooth Fairy – has dried up lately.There’s just no telling when the next tooth will drop, and then the school book fair comes up. Girls who don’t lose teeth don’t get paid.And then she needs fairy princess dolls, then it’s just all like, bills, bills, bills for my eight year old right now.You understand what I’m saying.

I didn’t hear about this conversation at first, but I noticed my oldest daughter kept prompting my wife to bring up some particular unnamed topic last night.

My daughter was eager for the conversation, but my wife strongly preferred that she and I develop a common strategy with regard to allowances, without having to simultaneously negotiate with an eight year-old.

(Here’s where I ought to insert some analogy between negotiating with 8 year-olds and negotiating with terrorists.Or lately, negotiating with Congressmen overly responsive to hard-core constituencies, encouraged by a system gerrymandered for incumbency.But I digress.)

Also, my wife assumed I’d have some strong ideas about what to do when it comes to kids’ finances.You probably won’t believe this, but I have a lot of thoughts about allowances.

If you give a pig a pancake, pretty soon she’ll ask for some syrup

Allowances!

So now we have moved, like the proverbial pig and his pancake, from the “first stock investment” phase to the “allowance phase” of parenthood.At this point my wife and I haven’t fully decided what to do, although I’m about to explain to you my best ideas so far, at least for the first month of her allowance.[1]

This is one of the cleverest allowance ideas I’ve ever come across, so I thought I’d share before even rolling it out to my family.

In fact he lists three great ways of teaching the power of compound interest to kids through the mechanism of the allowance.Each one has its own special advantage.

Cookie Jar Experiments

The power of compound interest – The Cookie Jar Experiments

Tobias describes three versions of what he calls the Cookie Jar Experiment, which over a month or two can viscerally and intuitively teach the magic of compound interest to kids through the mechanism of an allowance.

Version One. Offer your kid $1 on Day 1, and put it in a cookie jar.[2] Offer to add 10% more each day, as ‘daily interest growth’ on that original $1.

So, for example, on Day 2: $1.10 would be in the jar,

Day 3: $1.21. And then on

Day 4: $1.33.

After a month there will be a total of $17.45 in the jar, which shows how powerful 10% compounding can be, even if you begin with just $1.

Tobias suggests you probably won’t continue the experiment to the end of Month 3 ($5,313) or Month 6 ($28 million) but really that’s up to you and your own resources.

In my opinion, the power of compound interest as a concept is really worth teaching, so some of you will want to consider going the full 6 months.It will only cost you $28 million in total.If you do decide to do everything it takes to teach little Johnny the power of compound interest, be sure to email me at Bankers Anonymous so that I can provide my bank account number for the minimal 2% fee I normally charge for this kind of life-changing advice.

Anyway, back to my regularly scheduled commentary.While ‘real life’ doesn’t let you compound at 10% on a daily basis,[3] the experiment lets you demonstrate the amazing power of compound growth to your kids in a concrete way.

The 1 month time period – by which $1 grows to $17.45 – is short enough that kids can see the growth and just how powerful it can be.

Version Two.

This next version of the Cookie Jar Experiments is best for two kids, and it can drive home the power of compounding early, plus delayed gratification.[4]

Between your two kids, you offer a similar deal to version one, but with a twist. If one of them is willing to skip the first three days of interest accrual, they can get something desirable like a chocolate bar.

After they finish fighting over the chocolate, you run the experiment for, say, two months.[5] The child who went without the chocolate has $304, while the ‘lucky’ child who got the chocolate only has $228 in the cookie jar at the end of 60 days.

The lesson: Start saving early because it’s the earliest accruing period that matters the most.

The child with $304 can now buy a whole bunch of delicious cookies and leave the greedy chocolate eater weeping.

Are we having fun yet, kids?

Kids?Please stop fighting, please.Thank you.

Version Three.

“If only he’d used his powers for Good, instead of Evil.”

Run the same experiment as in Version One, but use the interest rate associated with many credit cards.Let’s pick 20% because it’s a round number, even though many people’s effective credit card rates are even higher.

Start adding money to the $1 at a 20% growth rate and label this ‘Credit Card’ growth. On Day 19 the ‘credit card’ account has grown to $32, versus the $6 to which the original savings at 10% per day grew.

If you run the comparison all the way to Day 35, the difference is $590 for the credit card account versus $28 for the ordinary 10% growth account. The key to this version is pointing out that some people scrimp and save and achieve some growth on their savings, while others pay huge portions of their money to credit card companies.

Here’s a video version of this allowance experiment:

Again, of course, whether you fill up a cookie jar with $590 is up to you and your family’s means, but you can create an unforgettable demonstration for your kids of how small differences in compound interest rates make for giant differences in the medium and long run.

So what will we do about the allowance request?

So will we decide to run these experiments on our children when they request an allowance?

I’m going to push for at least Version One to kick off the new allowance phase for my eight year-old.

If she complains, I’ve got a Jack Handey quote ready:

“One thing kids like is to be tricked. For instance, I was going to take my little nephew to Disneyland, but instead I drove him to an old burned-out warehouse. “Oh, no,” I said. “Disneyland burned down.” He cried and cried, but I think that deep down, he thought it was a pretty good joke. I started to drive over to the real Disneyland, but it was getting pretty late.”— Jack Handey

That’s why I say, deep down inside, she’s knows stock investing is fun. And so are Daddy’s experiments with allowances.

[1]After that, we may revert to a more typical $2/week, conditional on a usually-left-undone chore – cleanup of the girls’ room – that drives my wife nearly to glue-huffing, out of frustration, on a weekly basis.

[2] Or, wherever.Do cookie jars even exist anymore?

Last night completed Day 30 of the “Allowance Experiment,” in which I offered my eldest daughter a daily payment calculated as 10% of her allowance savings, compounding daily. On day 1, she began with an initial grub stake of $1. She received $0.10 on day 2 (10% of $1) and $0.11 on day 3 (10% of $1.10), and so on.

Last night completed Day 30 of the “Allowance Experiment,” in which I offered my eldest daughter a daily payment calculated as 10% of her allowance savings, compounding daily. On day 1, she began with an initial grub stake of $1. She received $0.10 on day 2 (10% of $1) and $0.11 on day 3 (10% of $1.10), and so on.