The private $4.7 billion Industry Bancshares Inc. in rural Texas made the dramatic step in early November of asking for a meeting in December 2023 to solicit shareholder permission to issue additional ordinary shares and preferred shares. It’s unclear at this point whether they will get this permission or be able to raise additional capital. What is clear is that existing shareholders of Industry Bancshares are unlikely to end 2023 happy, no matter what happens next.

There’s a straight through-line narrative from the rapid interest-rate hikes by the Federal Reserve in 2022, to a number of large bank failures this Spring in New York and California, to Industry Bancshares recently seeking permission to raise more capital. Rate hikes have caused a slow-moving banking crisis nationwide throughout 2023. This crisis has now come home to rural, central Texas.

Other banks and bond portfolio losses

Plenty of other better-known banks have suffered this year from their bond portfolio losses, with the same root cause of aggressive Fed hikes in 2022.

Silicon Valley Bank, which in March 2023 suffered the third-largest bank failure in US history, had almost exactly the same problem as Industry Bancshares, but on a larger scale. Like Industry Bancshares, it owned many ultra-safe long-maturity US Treasury bonds which dropped in value when interest rates rose. The differences in customer profiles, however, could not be starker. Whereas Silicon Valley’s Twitter-networked high net-worth depositors yanked their money quickly and brought down the bank in the course of a week, Industry Bancshares customers appear to move at a different speed. The key difference – and this has been an advantage so far for the Texas bank – is the slow pace of deposit banking among its customers.

Bank of America, to name another well-known bank, has a huge bond portfolio-loss problem that has been a headache for national regulators ever since the beginning of 2023. In October 2023 Bank of America reported $131 billion in unrealized bond portfolio losses. Unlike Industry Bancshares, however, Bank of America has a highly positive net worth overall of $229 billion, on a traditional GAAP accounting basis, as of September 2023.

San Antonio-based USAA, the largest Texas-based bank, had a $10.4 billion loss on its bond portfolio in 2022 and reported its first negative earnings year in its 100-year history. USAA also had a substantial positive net worth at over $27 billion at the end of last year on a traditional GAAP accounting basis.

So Industry Bancshares has plenty of company among the misery of banks whose bond portfolios got hurt by the rapid rate hikes of 2022. It stands uniquely apart, however, in its dropping into negative net worth territory throughout all of 2023, a valuation place no financial institution wants to be.

Illiquidity versus insolvency

In the normal model of banks at risk, we worry about a run on a bank because of illiquidity. Illiquidity arises because banks generally only keep a fraction of their total assets in cash or highly liquid equivalents. This is usually fine because they generally assume customers will not all demand their cash back at the same time. If customers did suddenly withdraw their deposits – as you probably watched in the fictional small-town bank run depicted in the Christmas classic “It’s A Wonderful Life” – no bank generally holds sufficient cash on hand. In a traditional liquidity crisis we understand that the problem is one of timing. Meaning, if you give the bank enough time to sell off its assets to raise cash, everything will be fine. The bank ultimately holds plenty of valuable assets well above the money owed to depositors and lenders. It’s illiquid, but not insolvent. Every modern bank worries about illiquidity risk because it can happen to any bank. FDIC insurance is a great solution for illiquidity risk, because it eliminates the need for smaller depositors – anyone below $250 thousand at the bank – to demand their money back quickly out of fear of a bank run.

In the more extreme model of banks at risk, however, we worry about a bank run due to insolvency. That could happen if a bank has a negative net worth – owing more money than it actually owns in assets. This is rare. Normally insolvency could be due to unexpectedly high losses on a bank’s real estate or business loan portfolio. Or as happened this past year, it could be because of an extreme drop in the value of a bank’s bond portfolio. The problem and the solution is not a matter of needing more time to sell assets – it’s a matter of the bank literally doesn’t have enough valuable assets to cover its liabilities, and then depositors realizing the risk they face in that situation.

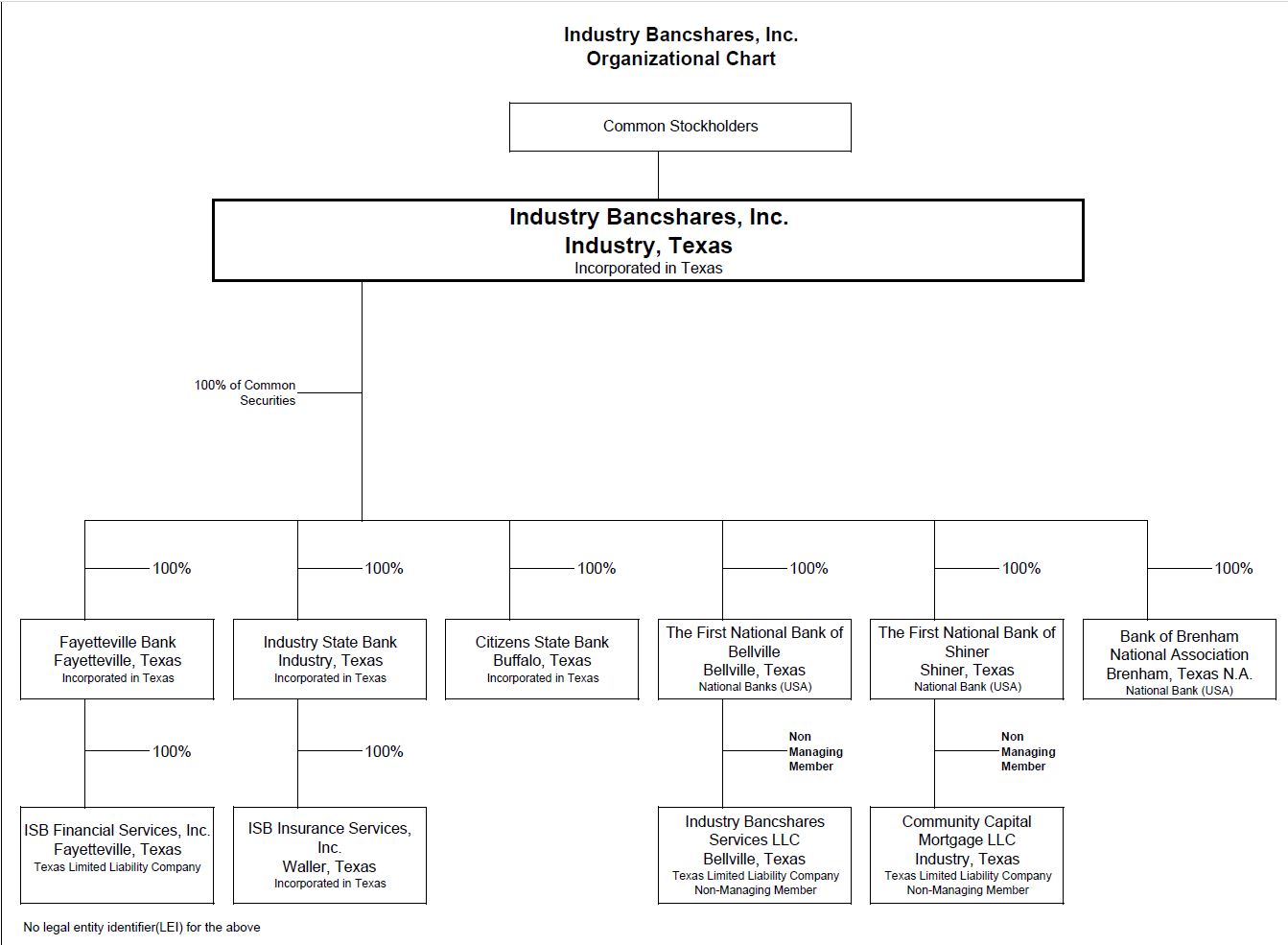

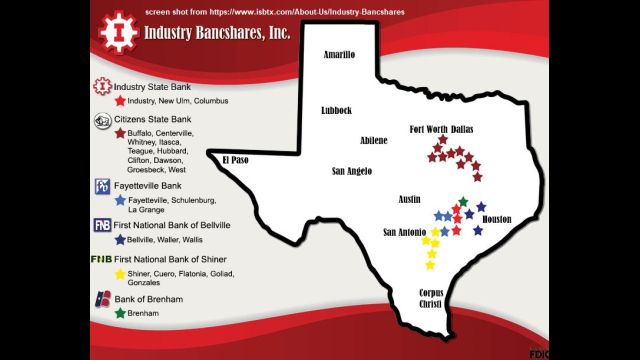

Weirdly, as I wrote about a few months ago, just 15 out of 4,697 banks in the United States reported a negative net worth mid-way through 2023, putting them at risk of insolvency if too many depositors and lenders decided to ask for their money back. Even more weirdly, 6 of those 15 negative net worth banks are actually part of the same bank, the bank holding company Industry Bancshares. This holding company is made up of 6 small Texas banks with 27 branches located in rural counties between Houston, San Antonio, and Austin: Citizens State Bank of Buffalo, Bank of Brenham National Association, Fayetteville Bank, First National Bank of Bellville, First National Bank of Shiner, and Industry State Bank.

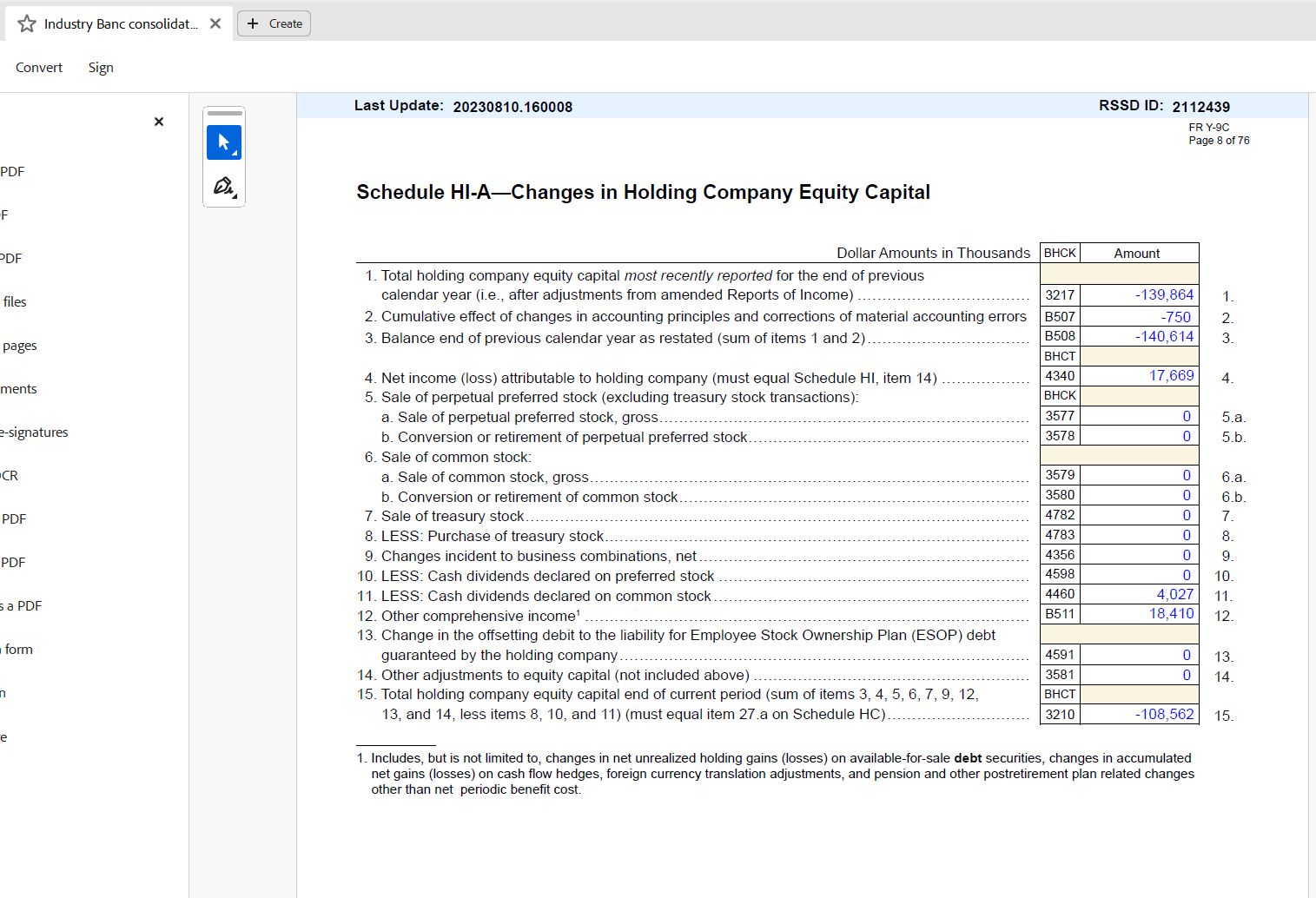

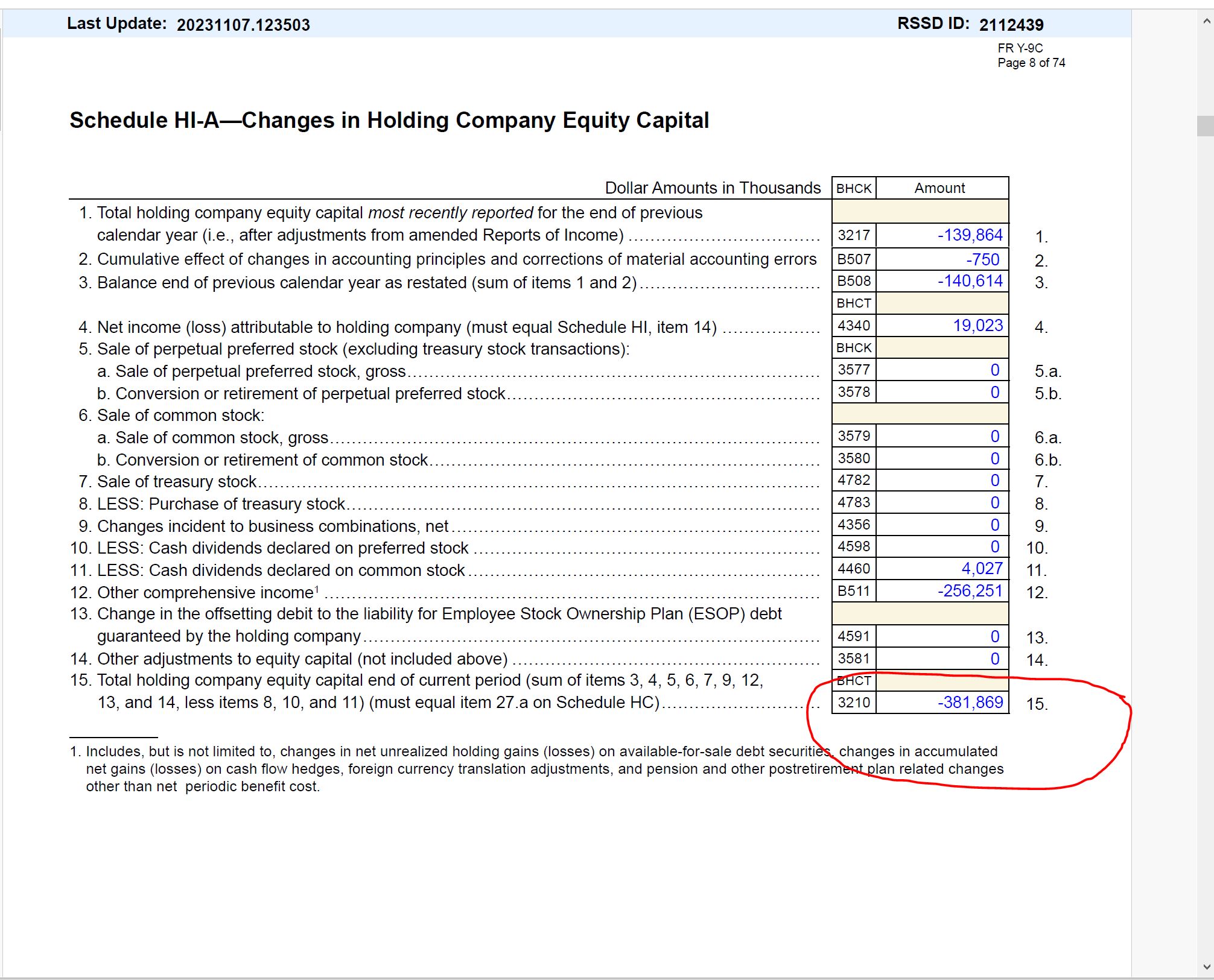

When I first wrote about the bank, each one of the six individual banks had a negative net worth. In total the six were collectively in the hole for $128 million, or $108 million at the bank holding company level. That value was based on public filings from the end of June 2023. Unfortunately, due to further interest rate rises and bond portfolio losses, each of the six individual banks now has a significantly larger, that is to say worse, negative net worth. Collectively that balance sheet hole ballooned to $401.4 million by September 30 2023, or $381.9 million at the bank holding company level.

The solutions

The last time I wrote about Industry Bancshares, I mentioned possible solutions management could pursue were to:

1. Try to sell to a larger, better-capitalized, bank

2. Raise new investor capital

3. Do nothing, and hope to earn their way over time out of their negative equity position, or

4. Do nothing, and hope for bond portfolio values to improve.

I don’t know if they are trying option 1. They reported to shareholders that they hired a financial advisor known as Hovde Group to seek strategic financial solutions. The December 2023 shareholder meeting is a necessary step in the direction of option 2. Option 3 is a longer-term strategy which requires patience on the part of regulators and depositors to overlook their negative net worth for a few years in the hopes that consistent profitability solves the problem. Industry Bancshares reported $19 million in net income through September 2023, so this is possible, but it would take a while. Option 4, which they elected to do by default, appears to have exacerbated the situation.

Interest rates jumped again in the 3rd quarter of 2023, and losses deepened. Option 4, doing nothing with the bond portfolio, has made their negative equity position 3 times larger than was previously reported, halfway through the year.

Bank Accounting v. GAAP Accounting

Because of a quirk in the way banks are regulated, banks can choose to have their portfolio losses on “available for sale” bonds ignored by regulators, when regulators look to see if a bank is solvent or has sufficient capital. Only when bonds are sold – and Industry Bancshares has not sold theirs – are the losses counted. And bonds don’t have to be sold, as long as depositors or other lenders do not request their money back. As a result, Industry Bancshares can state with a straight face that they meet regulatory standards for “well capitalized.” At the same time, in ordinary business terms and according to common sense, they have a deeply negative net worth.

An October letter to shareholders from management included this message:

“You may have seen an article or two about the Company that have not been very favorable and have been very misleading in many respects. The articles have painted our Company and the banks in an unnecessarily poor light due to an accounting concept that requires banks to report unrealized losses and gains on a certain portion of their securities portfolios.”

I would posit that my article in September was not “very misleading in many respects” at all, although readers can render their own judgment on that. Bankers – who literally evaluate corporate solvency and business valuations for a living – understand very well what the difference is between positive and negative net worth, despite what regulators permit them to report and claim.

Dividends, valuations, and at-risk people and groups

It is notable that the bank paid $4.027 million in dividends via two payments to shareholders in April 2023 and July 2023, even though the bank as a going concern was worth less than zero dollars in the ordinary sense of a business enterprise.

In January 2023, bank management communicated to shareholders that bank shares were worth an estimated $37.25 per share, down from approximately $44 per share in 2022. This despite a December 31 2022 equity capital position of negative $159.7 million across all six banks combined. Management has suggested that a new share offering after December 2023 would be in the range of $1.5 to $2.5 per share. Even before the issuance of new shares, existing shareholders are facing a 95% loss in value over the past year.

The owners of the more than $2 billion in more than 3,100 deposit accounts with balances above $250 thousand, employees who may have their net worth tied up in an Employee Stock Ownership Plan (ESOP), and ordinary shareholders should seek to more fully understand their situation at Industry Bancshares.

A version of this post ran in the San Antonio Express News and Houston Chronicle.

Please see related posts

USAA had a very bad, no good year in 2022

It’s A Wonderful Life, a failed banker origin story

Post read (1118) times.