I went online recently to explore certain hard-core taboo subjects. I looked up words we don’t talk about in polite company. Certainly not in front of the children. Words like Trust Fund. Inheritance. Aristocracy.

I’m interested in the fact that when it comes to these concepts we don’t openly agree on what kind of society we want.

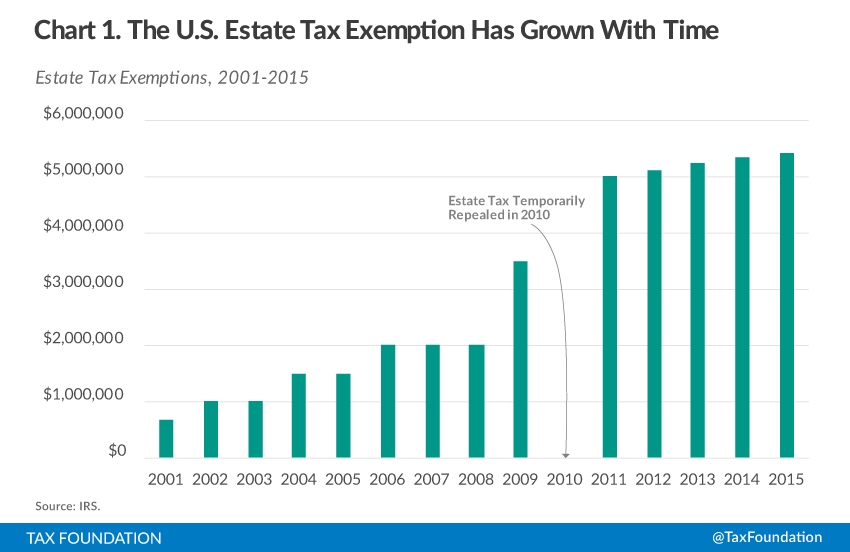

For example, it’s clear to me from the major tax reform of December 2017 – which raised the estate tax exemption for a married couple to $22.36 million from the previous $11.18 million exemption – that we as a society want more trust fund kids. Trust fund kids are great. Surely, despite our political differences, that’s something we can all come together around as a nation?

Trust Fund

Speaking of which, in the past year I agreed to be a trustee for some family members. I received copies of their “Last Will and Testament” documents. I’m really a “backup” trustee, in the sense that I’m a trustee only in the unlikely circumstance that my relatives die young, while their children are quite young themselves.

Clearly my relatives did well picking a good trustee. But what is the right age of inheritance?

A main point of the written will on which I am named trustee is to ensure that if my relatives die early their two children do not receives big piles of money at too early an age. They stand to receive one-third of the inheritance upon reaching their 30thbirthdays, and the remaining two-thirds of their inheritance upon their 35thbirthdays. If their parents live a long and full life, the children will inherit money significantly older than that, there will be no restriction on their inheritance, and my own role becomes unnecessary, as we all hope it will be.

The idea here, according to my relative who asked me to be the trustee, is to delay as long possible the pile of money that her girls could inherit. I asked my relative how and why she chose those ages of inheritance. Why not 25? Or 45? Why not give it all to them?

Says the mother of the girls, “I just came up with those ages based on my own experience and my reading that most young people who inherit money lose it before long. We ran them past the attorney and he seemed to agree, so we went with it.” So not a lot of science, just recognizable common sense.

I hope you realize I was being sarcastic above about trust fund kids. My relatives – like most thoughtful people – don’t want to create trust fund babies either. They want their children to become hard-working adults whose professional lives are already in full swing – their mid-30s – before they get money that could demotivate them or encourage bad habits.

When you jump down the rabbit-hole of the trust fund sub-genre of personal finance literature you’ll find interesting articles like “Confessions of A Trust Fund Baby.”

I’ll summarize for you a few of my findings based on this reading:

Coke, booze, Ecstasy, and clubbing really is more plentiful among the trust fund set.

It’s a lot easier to take certain poorly paid jobs, in certain expensive cities, if you have a trust fund.

Money is a delightful safety net, but cannot confer meaning.

As a reader of Anthony Trollope and Jane Austen novels, I suppose I’ve long had this interest in trust fund kids. None of the main characters in these 19thCentury romances actually works for a living. The only question is how much annual income they may each depend on without working, and what suitable romantic matches may be made to help or hinder their continuing in the style to which they’ve become accustomed. This was all discussed in the 19thCentury without shame and without a sense that being a trust fund kid implied you were a wastrel. In fact, not working for a living was the key sign that you were a worthy person, a gentleman or a gentlewoman.

In the 20thand 21stCentury by contrast – and in contrast to my sarcastic comments above – we mostly carry a combination of worry about and contempt for trust fund kids. That’s not necessarily fair to the kids – they didn’t choose to inherit the money. But I think it’s interesting that our collective attitude is at odds with the direction of estate tax legislation.

Estate Tax Changes

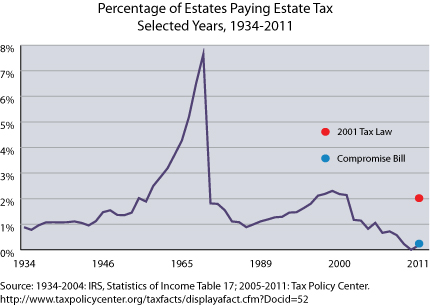

The tax-free inheritance number has climbed dramatically since 2000. When President George W. Bush came into office, children of wealthy parents could inherit up to $1.35 million tax free. The estate tax – the tax imposed on amounts above that exclusion – stood at 55 percent.

Under Bush, the exemption number began to climb steadily year by year to $4 million, while the tax rate fell to 45 percent. During the Obama era, the tax exemption jumped further and then climbed annually to $10.86 million. Meanwhile, the tax rate dropped to 40 percent. Now with the 2017 reform, lucky heirs can inherit from their parents up to $22.36 million, tax free.

Our tax system is increasingly designed to return us to the 19thCentury, even if the way we think about wealth concentration and inheritance remains rooted in the 20thCentury. As a country it feels like we have this weirdly bipolar and contradictory attitude toward trust fund kids.

I think we should just admit we prefer an aristocracy. The plain fact is we’ve steadily reformed our tax laws throughout the 21stCentury so that we can have more of it.

I’m a huge fan of Bloomberg’s Matt Levine,1 who is basically smarter and funnier than anyone writing about finance.

Anyway, I was annoyed to read yesterday’s Op-Ed by Gregory Mankiw (whose textbook of course we all had to have in College) Mankiw’s a Harvard professor with all the respect that comes with that, and he’s attacking a tax position I hold dearly. My view is that the Estate Tax is the best of all taxes, and Mankiw’s view in the Op-Ed is that it’s unfair, because of the different level of taxation that will hit a theoretical household of frugals vs. spendthrifts.

Mankiw’s view is that two households that generate, say, $20 million in wealth will be hit by unequal taxes, depending on how they spend, or don’t spend, their money. To complete the thought, a spendy household will end up avoiding the estate tax – currently 40% of an estate’s value above $5.45 million. Meanwhile, a thrifty household will pay those hefty taxes, when the couple dies. Humph. That did sound unfair when I read it yesterday.

Thankfully, Levine rescues my views, with an important distinction. The taxpayer is actually their heir, not the wealth-generator. The wealth-generator is dead. And when you think about what is “fair” to heirs, the calculus changes. Take it away, Matt:

Here is a curious argument from N. Gregory Mankiw that the estate tax is bad “because it violates a principle that economists call horizontal equity. The basic idea is that similar people should face similar tax burdens.” So if two couples — the Frugals and the Profligates — each start businesses, work hard, and earn the same amount of money, they should each pay the same amount of taxes, even if the Frugals save all their money and the Profligates spend theirs. They do. But Mankiw thinks they don’t:

[Levine now quoting Mankiw:] Under an income tax, the couples would pay the same, because they earned the same income. Under a consumption tax, Mr. and Mrs. Profligate would pay more because of their lavish living (though the Frugals’ descendants would also pay when they spend their inheritance). But under our current system, which combines an income tax and an estate tax, the Frugal family has the higher tax burden. To me, this does not seem right.

Ah, see, the problem here is thinking that the senior Frugals pay the estate tax. They don’t. They are dead when the estate tax is assessed. The two great inevitabilities are death and taxes, but death is in an important sense logically prior. When you pay taxes, you still (usually) prefer not to be dead. Once you are dead, you have no preferences about taxes. We could fund the government with a lovely, efficient, non-distortionary system of taxing only the dead, except — and this is another key point — the dead don’t have any money. The incidence of the estate tax can’t be on dead people. Once the Frugals die, their heirs have the money, and the estate tax taxes them. If the Frugals’ children make $30,000 a year as art gallery assistants and also inherit $20 million, and Mr. and Mrs. Justnotrich’s children make $30,000 a year as Wal-Mart employees and inherit nothing, it seems odd to say that they should pay the same taxes as a matter of horizontal equity.

So anyway, I think Levine the finance blogger wins that round against Mankiw the professor. Also, it fits my worldview, so…

And you should subscribe to his daily email. No wait, don’t, because then you’ll realize how often I’m trying to ape his style. Forget I mentinoed it. ↩

One of Piketty’s main goals is to understand the conditions under which concentrated wealth can emerge, persist, vanish, and perhaps reappear.

Piketty’s unique offering, I think, it that he (along with colleagues) built the most complete, historical, transnational data-set on wealth distribution. Specifically, he allows us to compare three centuries of wealth data in France and the UK. He also built the most complete data sets on wealth in Germany, Italy, Scandinavian countries, Japan, and the United States.

Through that longitudinal data we get to see what has changed over the centuries, and where we stand today, compared to the past. We also get to see how the United States stacks up against other wealthy countries.

I’m late to the party in reviewing Piketty’s book – published in 2014 – but I think it doesn’t matter. He’s got centuries of data behind him and the book has a long shelf-life ahead of it.

All inequality discussions are political

Even engaging in a discussion about inequality involves political and normative choices. What we choose to measure, for example, has a great effect on what conclusions we draw.

Readers of Piketty’s work, naturally, come armed to the fight with political agendas. I know I do, and you do too. I happen to think inequality is a defining problem of our time. Others may not agree. ‘How much does inequality matter’ is a deeply political question in and of itself.

Piketty offers a great example of this, when he cites governmental measures of inequality. Traditionally, OECD governments present the ratio between the 90th (top) percentile of income and the 10th (bottom) percentile of income as a proxy for income inequality. Problematically, Piketty points out, this so-called P90/P10 ratio completely ignores the vast concentration of wealth within the top 1% of many countries. The bottom 9% portion of the top 10% in the United States, for example, look like pikers compared to the top 1%, a fact that the P90/P10 ratio tends to hide.

Additionally, the ratio will not indicate what portion of national income the top 10% earns, whether it’s 20% as in the case of Scandinavian Europe in the 1980s, 50% as in the case of the contemporary United States, or 90% in the Belle Epoque era of Britain and France preceding World War I. By choosing to present the P90/P10 ratio, governments choose the ‘chaste veil of official publications,’ a set of data that obscures as much as it enlightens.

War as Equalizer

The devastating wars of the 20th Century destroyed so much concentrated wealth in Britain and France (in addition to Germany and Japan, obviously) that they literally upended the social order. Piketty’s data shows how wealth concentration with the Top 10% and 1% in these countries plummeted in the first half of the 20th Century.

Wealth inequality stayed relatively tame in the decades following World War II, before ticking upward in the 1980s and beyond. An easy explanation for renewed wealth concentration may be changing tax rates, especially following the Reagan & Thatcher revolutions in the Anglo American countries.

Austen & Trollope & an Economist’s style

I have long looked to Jane Austen and Anthony Trollope as sources of information on the meaning and use of wealth, so I was pleased to see Piketty do the same.[2]

Jane Austen

Outside of these 19th Century literary references, Piketty does not rely on metaphors, popular writing, or anecdote. He’s an economist, primarily focused on his data and formulas to explain wealth creation. Like a serious economist, he takes great pains to explain his data collection methods and to circumscribe his conclusions. This makes for drier writing, but high credibility.

The Piketty thesis, in a thumbnail sketch

Piketty has a math-based worldview on how wealth becomes concentrated, and how it may inevitably lead to inequality in the future. I’ll attempt to concisely describe it here, so that you may mention it casually and sophisticatedly at your next cocktail party to impress your friends. You are welcome.

In the first section of the book, he builds the case that the proportion of national income that goes to ‘labor’ (what people get paid to do in exchange for the application of their time and talents) versus what goes to ‘capital’ (financial returns that accrue to an accumulated stock of wealth) is a key set of numbers to study in a national economy.

A key number for measuring this is what he calls the national “capital/income ratio” – which measures the stock of accumulated wealth of a country compared to the flow of total national income in any given year.

Typically we might see that the national wealth in a developed country is five or six times greater than the country’s income.

This ratio allows Piketty to measure – over time and across countries – the amount of money that ‘capital’ earns each year versus what ‘labor’ earns each year.

A household analogy for the capital/income ratio

To break that down into household terms and in numbers that our brains can handle, we might say that the capital income ratio of my household could be five if, for example, I boasted of a personal net worth of $500,000 and an annual income of $100,000. I mention the household analogy to illustrate the capital/income ratio as just a way of comparing the fixed accumulated store of wealth with a flow of annual income. Piketty focuses on measuring this number for countries over time, counting the entire national ‘store of wealth’ and the entire national ‘income.’

Second number: % annual return on capital

The reason why the national capital/income ratio matters is that it allows Piketty, and us, to see how much of national income is earned by ‘labor’ versus how much is earned by ‘capital.’ To do this, we need to know what the overall annual ‘rate of return’ on capital is in any national economy. This rate of return is just like how it sounds: If I invest $100,000 for example, do I make 2% on my money, or 6%, or 15%? An individual’s return on investment will depend on the particular investment of course – a bank CD vs. a bond vs. a stock vs. a rental property vs. an angel investment in a startup – to cite a few well-known possible investments. That aggregate national ‘return on investment’ will be the average of all these investments across millions of households and firms.

We might find, and Piketty does, that the average national return on capital often fluctuates in the 4 to 5% range over time.

Certainly Austen and Trollope generally assumed a 5% return on capital. A gentleman landowner who could count on 5,000 pounds per year in income might have been able to value his holdings – although voluntary land-sales were all but forbidden back then – at around 100,000 pounds.

Putting them together – income from capital

A fundamental math formula underpinning Piketty’s book is that the capital income ratio, multiplied by the return on capital, tells us what the overall proportion of income derived from capital is in a national economy. Money either comes from working (labor) or from investing (capital) and it helps us to be able to calculate what portion comes from capital.

Piketty, and we, care about this because it’s the beginning for understanding how wealth grows on wealth and how, possibly, an increasing rate of wealth inequality may in certain circumstances acquire a sort of mathematical inevitability.[3]

To return to a household analogy for a moment – which may help explain what Piketty measures at the national level – we could say again that I have a capital/income ratio of five. That’s based on my presumed $500,000 household net worth and $100,000 annual income (and $500K/$100K is five).

We could then assume that my return on capital (picture my $500K invested in ‘capital stock’ although in reality it might be entirely tied up in my house, but whatever) as 5%. When we multiply 5 fives 5% we get 25%, which represents the ‘annual income derived from capital’ of my household for example.

That annual income derived from capital – at the national level – is what Piketty takes great pains to build historical data around, and to track through time and across countries. We can see from the first math formula that the capital/income ratio determines to a great extent how much of national income will go to holders of capital (in simpler terms, holders of wealth. In simplest terms, how much goes to capitalists rather than workers.)

Piketty tracks the decline in ‘annual income derived from capital’ from the early Twentieth century through World Wars One and Two, but then the steady increase in the annual income derived from capital since the 1950s, as a way to understand changes throughout the last century.

A second math formula

Upon this foundation, Piketty introduces a second math formula. The capital/income ratio will tend to converge toward, over the long run, the ratio of the national savings rate divided by the growth rate of the economy.

A country with a high savings rate will tend, over time, to have a higher capital/income ratio. A country with a low growth rate (because the growth-rate number is in the denominator of the formula) will tend to also have a high capital/income ratio. Both of these situations we might expect will tend to exasperate inequality, as more of a nation’s wealth goes to capital, rather than labor.

By contrast, we would expect high growth rates in the economy over time to lower the capital/income ratio, and over time to lower the percent of income that goes to capital, rather than labor. That might correlate over time with lower inequality.

In either case, small changes in the economic growth rate can have great effects on the capital/income ratio over the long run. This second formula’s predictive capacity, Piketty clarifies, only works over the long run, possibly over decades. Nevertheless, he argues that its effects are constant and unavoidable.

Viewing the future

From a predictive perspective, Piketty would point to the savings rate, the economic growth rate, and the return on capital as the key measures of whether inequality will tend to increase or decrease in a national economy over time. Lower savings rates should lead to higher equality of wealth. Lower returns on capital should also leader to higher equality. But perhaps the biggest determinant of future equality is the growth rate of the economy.

And to simplify 600 pages of complex economic thought: Looking forward the slower secular growth in the economy of developed countries may inevitably doom these economies to increasing rates of wealth inequality.

A further summary of his data: The United States and Britain and France continue to move in a trend – begun in earnest in the 1980s – toward wealth concentration that will resemble the Belle Epoque of 19th Century Britain and France.

When we see the trends, it’s not hard to become alarmed about increasing concentration of wealth forming a sort of permanent aristocracy over our nominal democracies. Piketty urges us to note the data, note the trends, and try to understand the dangers to capitalism and democracy in the long run.

Policy Recommendations

Merely studying inequality is a political and moral choice, but making policy recommendations is obviously even more so. Here is where Piketty’s critics have mostly directed their fire.

Although I love his data and analysis, I am less certain that I will adopt Piketty’s prescriptive worldview on policies.

Piketty favors a progressive annual tax on large fortunes, as a way to combat the inevitability of wealth concentration. To the extent that would involve an estate tax, I am on board. The annual tax on wealth is obviously a further step altogether, since it would occur once a year. I can easily imagine the steps wealthy households would immediately take to avoid this tax, but Piketty nevertheless makes the case.

He also proposes a kind of global tax on capital, which as Piketty readily admits, is hard to imagine becoming a reality right now, both mechanically and politically. Banking coordination and reporting would be a crucial first step. This seems a long way off.

Piketty also favors an increased marginal income tax rate – possibly as high as 80% – on the highest earners in the United States. Although tax revenue from such a high rate on a small number of earners would be minimal, Piketty makes the case that the step would go some way toward reducing the concentration of income-capture by a small cohort of super managers, probably by voluntary compensation policy changes by large firms.

In each of these tax proposals Piketty seeks not to generate much revenue or replace existing tax regimes, but rather to regulate capitalism itself. If capitalism tends toward oligarchic concentrations of wealth – as the first ¾ of the book argues – his goal is to preserve the good of capitalism (efficient allocation of resources, high productivity gains) while mitigating the effects of the bad.

Capital isn’t the last word on these issues, but a key starting point for a discussion on the state of things.

Please see related posts:

[1] My summary of Kennedy: First, great powers become great based on their economic strengths. Second, great powers subsequently take on imperial obligations, which require increasingly larger military expenditures. Third, great powers sink under the cost of their military obligations. Like clockwork! And it doesn’t bode well for the current hegemon, with a military budget bigger than the next seven biggest militaries, combined.

[2] He also references the novels of Honore de Balzac, who I have not yet read. But I will someday.

[3] Unless counteracted by policies – like taxes – or exogenous events – like wars. Describing these counterbalancing forces take up a significant portion of the book.

Some readers became angry about my view of this tax break and took umbrage at my lack of sympathy for ‘job creators’ like hedge fund owners.

Among other complaints, readers wondered why I didn’t write about tax atrocities like the ‘death tax,’ known in other circles as the estate tax.

Inspired by that critique, I will offer my thoughts on other taxes that I pay and tax breaks that I enjoy, both from an objective standpoint – taking into account ‘what’s fair for society’ – and from a subjective standpoint – taking into account my own personal situation and ‘what’s fair to me.’

For this post: The Estate Tax.

Fair to Society

Honestly, estate taxes are my favorite ‘fair to society’ tax. When I am declared ‘Lord Of All Catan’ over this entire country I will quickly and happily raise the estate tax rate and lower the exemption for estate taxation. Estate taxes are fair to society because:

Very few pay this tax, which makes it ‘fair’ in my view

2. All taxes distort the efficiency of markets, but estate taxes distort consumption and other economic activity less than other taxes. That minimized distortion makes it more efficient than other taxes.

3. Estate taxes contribute in some (small) way toward ‘churning’ the stratified wealth levels of society, something that is fair in a society that values socio-economic mobility.

4. Estate taxes encourage the creation of philanthropic avenues such as endowments and foundations to avoid estate taxation. In that way the wealthy dedicate funds according to their specific moral choices (education, health, fitness, parks, art, scientific research, whatever) rather than trusting to the government to make those choices for them. A diverse range of non-governmental philanthropic funding streams strengthens civil society. Absence of Data

While I don’t have the economic statistics to back up statements two through four above – I instinctively feel they apply to any tax on inheritance. Maybe you totally disagree. I’m ok with that. Maybe you’d like to agree, but you’d also like to see some data to back up my statements.

For readers who prefer actual data over pontificating, I offer in reply one of my favorite sayings from former San Antonio Express News writer and faux-philosopher Jack Handey:

“Instead of having ‘answers’ on a math test, they should just call them ‘impressions,’ and if you got a different ‘impression,’ so what, can’t we all be brothers?”

Fair to Me

Since I don’t expect to inherit much from my parents, and I don’t expect to pass on much to my own children, I find the estate tax extremely ‘fair to me.’

I say, bring it on!

So that was easy. But now let me try a thought experiment.

How would my mind alter under different circumstances?

A mental test

What if I had a ten million dollar estate coming my way, and the federal estate tax would take 40% of all the money I was set to inherit over my $5 million estate tax exemption? Would I find it so ‘fair to me’ then? 1

I would like to think that I would be wise and grateful enough not to begrudge the federal government the $2 million estate tax (40% of the $5 million over the $5 million exemption amount) because I would get to keep $8 million in inheritance.

Ah, a cool $8 million for me, that I didn’t have to work for.

“I’m just lucky to be born into a family with $10 million to pass on,” I would think to myself as I inhaled from my Rosemary-Lime scented calming soap I order in bulk from Gwyneth Paltrow’s website.

Frankly, that’s not a bad deal that would leave me impoverished. I’m pretty sure I could just squeak by on a mere $8 million. In that scenario I do think the estate tax would still be ‘fair to me.’

The real test

Ok, but what if I stood to inherit a $100 million estate from my parents? And the federal government could tax 40% of my $95 million, (remember: we all get to keep the first inherited $5 million tax-free!) leaving me with just $62 million?

How do I like that estate tax now?

Well, if you put it that way, now I’m angry.

Because that is totally not fair to me!

Most importantly, how is guy like me supposed to get by on just $62 million? I have rights you know, based on the family I was born into.

The federal government probably just squandered the $38 million death tax it extracted from my deceased hard-working parents and me and gave it away to welfare queens and immigrants!

Gah!

Did you guys just call me a ‘piker’

Somebody get the Koch brothers on the line right now and let’s fix this unfair system together!

What?

The Koch brothers said they don’t want to talk to me ‘and my measly $62 million?’

Technically, I would be taxed on 40% of all amounts over $5.34 million – the current exemption for estate taxes – but please humor me, I’m trying to stick to round numbers to keep the numbers from distracting us. ↩

Like most of you, I am busy today updating my will, following the birth of the Prince of Cambridge. I, too, want to ensure that he grows up in the world wanting in nothing.

Naturally it is only just and right that I designate a portion of my entail to His Royal Highness.

That got me thinking about whether I had any advice for the bourgeoisie regarding estate planning.

If you can afford it, please don’t take estate planning advice from a blogger

If you will have sufficient funds at your death to require sophisticated estate planning, you will serve yourself well by hiring a specialized attorney who can advise you on up-to-date, optimal strategies for leaving money in a way that matches your values.

But if you can’t afford it, read on…

If you do not now have – or do not yet have – sufficient funds to pursue sophisticated advice on estate planning, here’s some basic principles to keep in mind.

Make a Will

Even if you are too young to have ever felt death’s breath upon your neck, everything can change in an instant. Writing down your wishes, having a witness, signing it, storing it safely, and notifying family members of its existence is an act of kindness for all who love you.

Retirement Accounts

You should know that when you open your IRA and 401K accounts, you designate a beneficiary (or beneficiaries) upon your death, and that furthermore, that choice trumps anything written in your will.

Which is why smart estate planners advise you to check your IRA and 401K beneficiaries periodically to be sure they reflect your current wishes.

So, you may have named the cute barista at your favorite coffee shop as a beneficiary to your 401K as a joke when you were 23 and unemployed, but if you don’t change that 70 years later, you may be giving money away on your death to a total stranger, albeit one who made amazing cappuccino foam hearts once upon a time.

A more likely scenario, and hence more worrisome: the 100% IRA beneficiary designation you gave to your first child – because you thought “one and done” – no longer reflects your larger brood of seven additional children and their 43 grandchildren when you die.

Pro tip: Do not create 50 enemies within your own family, cursing you in the grave because you forgot to update your IRA beneficiaries.

Tax Planning

The only thing I want to say here is that my old rule on taxes still applies: If you are going through extraordinary legal and financial hoops to avoid paying taxes, you may be missing the big picture.

Keep it simple – or as simple as you can – and be wary of complicated tax avoidance plans. The more effective they are, the more likely it is that the IRS will declare them void in the future. At which point, you’ll owe a lot of money and need to pay more fees to undo the plan.

The more intricate the tax avoidance plan, the more likely it is you’ll create headaches to be undone in the future, albeit with additional expensive fees – of course – for lawyers and advisors.

If it seems too good to be true, like all investments, it probably is.

Letting heirs know your plans

The more I study estate planning, the more I understand that the biggest mistake people make is to keep their plans to themselves.

If your worthy children will not get anything from your estate – which is fine with me because the expectation of inheritance can be a cruel corruptor – then it makes sense to let your heirs know ahead of time.

If your unworthy, rascally, children will not get anything from your estate – which is fine with me if that reflects your values and they’re jerks anyway – then they should know that before you die.

If some children will get more than other children – for whatever valid reason which trumps equal treatment – for goodness sake give everyone a warning and a reason for your choice.

Receiving less than a sibling from a deceased parent, without so much as a warning and a reason, is enough to guarantee inter-generational family strife for your kids’ remaining lives. Be empathetic, and tell them what’s in the will.

His Royal Highness the Prince of Cambridge

In the meantime, God bless the little heir. In the event of my untimely death, I hope he enjoys all of my hand-painted Dungeons and Dragons figurines as much as I did.

Two things you can count on with a casino entrepreneur like Sheldon Adelson: he knows the odds better than you do, and the house always wins.

In a recent Wall Street Journal interview, Sands Casinoowner Adelson shares his left-of-center political beliefs, including support for abortion rights and stem-cell research, the DREAM act, and socialized medicine. So why would he pour a reported $150 million[1] in 2012 into losing Republican candidates in the last election? And why would he vow to double that amount in the next go around?

The answer clearly lies in his odds-based analysis of tax policy, and his views of expected value.

I’m going to assume some simple numbers for Adelson’s net worth and annual income, and go through a quick analysis of the kind of odds Adelson works with in his head that leads him to be so generous to GOP candidates.

Let’s assume Forbes Magazine’s estimated $20 Billion net worth for Adelson, and my estimate of $2 Billion for Adelson in annual income.[2] To begin by stating the obvious, when you make $2 Billion a year[3], tax policy matters quite a bit.

Throughout the Presidential election, I’m going to assume Adelson knew the odds of a Romney victory were always around 40%.[4] I’m going to further assume a 25% chance that a Republican Presidential victory can lead to lower taxes.[5]

These seem like reasonable assumptions about the odds of influencing different tax rates, but of course you’re free to disagree and propose your own.[6]

Ordinary Income Tax

Adelson pays himself $1 to 2 million a year to run his Sands Casino empire. [7]

If I assume a GOP victory influences the highest marginal income tax rate by 5%, the expected value to Adelson of a GOP victory becomes his highest marginal income (I’m going to use $1,000,000 for easy math again) multiplied by the change in tax rate, multiplied by the odds of a GOP victory, multiplied by the odds of successfully influencing the tax rate. In other words:

$1,000,000 x 5% x 40% x 25% = $5,000

So…When Obama talks about raising income taxes on people earning more than $250,000 a year, Adelson really couldn’t give a flying whoop about the marginal tax rate on ordinary income. You might care, but believe me, Adelson doesn’t care. Retaining an extra $5,000 a year is not why Adelson gives to the GOP.

Dividend Tax

The qualified dividends tax rate currently stands at 15%, but will jump to 39.6% without a new provision to favor this type of income by January 2013. As I wrote earlier, wealthy folks care more about dividends and capital gains taxes than taxes on salaries. A GOP victory could have as much as a 20% effect on the marginal tax rate.

To avoid that, and in a move that should be surprising to precisely nobody, Adelson just announced a special dividend of $2.75 per share to be paid on December 18, 2012. With 431.5 million shares of Sands, Adelson will be sending himself a nice $1,186,625,000 holiday present.[8] This dividend supplements the typical 25 cents per share per quarter that Sands pays, or $431,500,000 per year that Adelson earns in ordinary dividends even before this special dividend.

If Adelson plans to make himself an estimated $1,500,000,000 qualified dividend payment annually, his expected value of a GOP victory is:

$1,500,000,000 x 20% x 40% x 25% = $30,000,000

Now that is something worth trying to influence through political donations. Heck, he could have made his money back in 6 months if Newt Gingrich had gone all the way to the White House.

Long Term Capital Gains Tax

Adelson, like the rest of us, pays 15% on his long term capital gains, from harvesting gains in securities that appreciate in value. With no deal before January 2013, that rate jumps to 20%, still comfortably better than the kind of suckers-rate of 35% that high salary earners pay for working for a living.[9]

I assume Adelson’s got about $100,000,000 in long term securities gains he can harvest, and a GOP victory could influence that rate by 5%, leading to an expected value of:

$100,000,000 x 5% x 40% x 25% = $1,000,000

Corporate Tax

Corporations the size of Sands Casino pay a 35% rate on corporate profits. For a number of non-crazy reasons either a Democratic or Republican tax regime might lower this, but let’s assume the GOP’s ability to lower this top rate by 5%. Just for kicks, to reflect the fact that corporations can greatly influence the amount of ‘profit’ they declare domestically in any given year, and to come up with round numbers, I’m going to assume a scenario in which Adelson’s proportionate share of Sands’ corporate profit is $399,000,000 annually.[10] His potential tax savings from a GOP victory therefore are:

$399,000,000 x 5% x 40% x 25% = $1,995,000.

Corporate profits may be voluntarily reduced or heavily managed through off-shoring earnings,[11] offsetting earnings against previous year tax losses, or by incurring new, costly expansions to eat up profits in the current year.

It’s obviously nice to lower corporate taxes, but nothing is as nice as being able to influence the estate tax.

Estate Tax

Now it gets REALLY interesting for Adelson. Bush-Cheney managed to eliminate the Estate Tax for one year in 2010,[12] but that kind of success is like flopping a low st when the other guy thinks he’s sitting pretty and ready to go in on pocket Aces…in other words, it happens rarely and it’s the greatest feeling in the world.[13] Realistically, a 10% change in the estate tax rate would fully satisfy Adelson. Because if he dies with a $20,000,000,000 estate, those numbers still multiply out for the following expected value:

$20,000,000,000 x 10% x 40% x 25% = $200,000,000

An expected value of a $200,000,000 million one-time payout upon his death certainly justifies a large investment in GOP candidates!

Of course, unlike the other taxes above, Adelson would only reap those rewards once, from the other side of the grave.

On the positive side, however, all of the other expected values for income, dividend, capital gains, and corporate taxes are annual expected values. Meaning, to make this as perfectly clear as a royal straight flush, Adelson wins the expected value every single year that he can influence tax rates to go lower through a GOP victory.[14]

When I add up the annual expected value of changes in tax rates due to a GOP victory, I get to $33,000,000 per year, plus a one-time $200,000,000 estate tax win. And for that kind of payout, you only need to invest $150 million every four years. At that point, you’re playing blackjack after the gorilla has crossed his arms to signal the count is right.[15] Or more plainly, those are some good odds.

In sum, Adelson should be investing even more in GOP candidates, as he’s getting back more in expected value than he’s giving. Which, as a casino guy, he knows perfectly well. Hence, the plan to double down next year.

[1] Included an estimated $100 million to help nominee Mitt Romney, a man he tried very hard to defeat during the primary by propping up Newt Gingrich’s chewing gum and paper bag campaign in the Spring of 2012.

[2] Adelson may very well average better than a 10% annual return on his assets, but I’m just going to estimate with round numbers to make my life and the math easier.

[3] I’m not at this point literally speaking from experience. But like all Americans, I believe the fact that I am not yet earning $2 Billion per year is just a quirk of timing. As John Steinbeck reportedly said: “Socialism never took root in America because the poor see themselves not as an exploited proletariat but as temporarily embarrassed millionaires.”

[4] I’m picking a single ‘average’ again to make my math easy. This number is based on the Iowa political market’s implied rates. I’m a big fan and participant in the online political trading markets supported by the Iowa Business School. Between July 2011 and just a few days before the election, the implied odds of the Republican presidential candidate of winning fluctuated between 35-50%, with just a month above that range in the Fall of 2011, and a few weeks below that in September 2012, before the first televised debate.

[5] This may be too low. The Bush-Cheney Administration, in gambling terms, managed to ‘run-the-table’ on lowering tax rates that mattered to people like Adelson. (I.e. dividends, capital gains, and estate taxes) Other Republicans, especially in the face of today’s hefty deficits, would have a harder time reproducing their success.

[6] Heck, this being the interwebs and all, you’re free to put on your troll hat and call me either a socialist drone or a capitalist dupe depending on where your own views took root. It’s a free country. Or at least “it used to be a free country before those [fill in the blanks: Communist/Socialist/Corporatist/Fascist] jack-booted SWAT teams of the [fill in the blank: Bush/Obama] Administration started clandestinely snuffing our last remaining freedoms. Uh, also, pass me the Cheetos.”

[7] Pffffhht, nothing more than enough to occasionally play the penny slots.

[9] For more on how tax policy encourages or discourages work, see my post here. To sum up: Your government would like you to earn a living through 1. Receive gifts and inheritance (0% taxes for the first $5 million) 2. Make money with your money pile (0% on Triple Tax Free bonds up to 15% taxes on capital gains and dividends) and 3. Earn a salary (up to 35% tax on ordinary income).

[10] I just picked this because that way I can say Adelson earns an even total of $2 Billion per year, which sounds about right.

[12] New York Yankee’s irascible owner George Steinbrenner famously benefitted his family to the tune of hundreds of millions of dollars by dying in 2010, the best of all estate tax years to die. Is it ok to mention here, apropos of nothing, that I hate A-Rod? I’m going to answer my own question: “Yes. A-Rod sucks.”

[13] Except for that part about your dead relative who left you money in the estate. That part is still sad.

[14] I haven’t even got into State level taxes. But in a discussion with my uncle about the value of paying for GOP candidate victories, he rightly pointed out the risk/reward for political investment and tax savings is probably even more attractive at the state and local level. He said it best: “You think paying for a US Congressman is good value? You should see how cheap it is to buy a state or city official!”

[15] Please remind me to do a Bankers Anonymous review of Bringing Down the House, which would make this analogy explicable if it doesn’t already make sense.

I’m interested in the fact that when it comes to these concepts we don’t openly agree on what kind of society we want.

I’m interested in the fact that when it comes to these concepts we don’t openly agree on what kind of society we want. I hope you realize I was being sarcastic above about trust fund kids. My relatives – like most thoughtful people – don’t want to create trust fund babies either. They want their children to become hard-working adults whose professional lives are already in full swing – their mid-30s – before they get money that could demotivate them or encourage bad habits.

I hope you realize I was being sarcastic above about trust fund kids. My relatives – like most thoughtful people – don’t want to create trust fund babies either. They want their children to become hard-working adults whose professional lives are already in full swing – their mid-30s – before they get money that could demotivate them or encourage bad habits. As a reader of Anthony Trollope and Jane Austen novels, I suppose I’ve long had this interest in trust fund kids. None of the main characters in these 19thCentury romances actually works for a living. The only question is how much annual income they may each depend on without working, and what suitable romantic matches may be made to help or hinder their continuing in the style to which they’ve become accustomed. This was all discussed in the 19thCentury without shame and without a sense that being a trust fund kid implied you were a wastrel. In fact, not working for a living was the key sign that you were a worthy person, a gentleman or a gentlewoman.

As a reader of Anthony Trollope and Jane Austen novels, I suppose I’ve long had this interest in trust fund kids. None of the main characters in these 19thCentury romances actually works for a living. The only question is how much annual income they may each depend on without working, and what suitable romantic matches may be made to help or hinder their continuing in the style to which they’ve become accustomed. This was all discussed in the 19thCentury without shame and without a sense that being a trust fund kid implied you were a wastrel. In fact, not working for a living was the key sign that you were a worthy person, a gentleman or a gentlewoman. Under Bush, the exemption number began to climb steadily year by year to $4 million, while the tax rate fell to 45 percent. During the Obama era, the tax exemption jumped further and then climbed annually to $10.86 million. Meanwhile, the tax rate dropped to 40 percent. Now with the 2017 reform, lucky heirs can inherit from their parents up to $22.36 million, tax free.

Under Bush, the exemption number began to climb steadily year by year to $4 million, while the tax rate fell to 45 percent. During the Obama era, the tax exemption jumped further and then climbed annually to $10.86 million. Meanwhile, the tax rate dropped to 40 percent. Now with the 2017 reform, lucky heirs can inherit from their parents up to $22.36 million, tax free.