If you face the high-quality problem of finishing your life with too much money, you’ve probably already figured out that three groups, and three groups only, get your surplus: The government, your family, and your preferred charities. Of these, we typically all agree about leaving the lowest legal amount to the government. Then we face tremendous stress about how to allocate our fortune between the other two.

This post not only nudges you toward door number three (your favorite charities!) but advocates a tax-efficient, low-cost way to do it, available to people of even modest means.

But first, the problem of children.

Many choose to prioritize their children or relatives first, which is fine, whatever, it’s your dollar. My own personal starting point about inheritance discussions is this: children do not deserve free money.

However, I realize we’re not going to all agree on that one, and I’m not (yet) in a position to vastly increase federal estate taxes.

Meanwhile, what do people facing a wealth surplus worry about? Merrill Lynch – in a 2015 report titled “How Much Should I Give To My Family? On the Risks and Rewards of Giving ” – found two problems when they surveyed their high net-worth clients. First, 42 percent of respondents plan to pass on their assets only AFTER their death, rather than while they’re alive. Second, more than 60 percent of high net-worth clients worried about the potential negative effects of inherited wealth on their children.

The problem, as Merrill Lynch and other financial advisors will likely agree, is that those findings bump up against two well-known estate-planning principles.

First, giving away money during your lifetime – rather than after your death – is the most efficient way to minimize taxes on transferring your wealth. And 42 percent of Merrill Lynch respondents weren’t planning that. So now all we need is a (tax-efficient, low-cost) way to give money away while you’re still alive. Keep reading.

Second, the key to lowering stress in estate planning is to put your personal values in the center of the plan. More than 60 percent are stressed about the tension between their values and their children’s values, which means they have not sufficiently figured out answers to the questions: What do you believe in? What do you stand for? What people or organizations or values represent the highest expressions of meaning in your life?

If it’s all about your children, cool, give them the money. If you have other values you want to express as well, however, let’s talk about donor-advised funds for a moment.

Donor Advised Funds

What’s the best way to give away money during your lifetime? Although that’s too broad a question, I’m going to opine anyway. A very good way – surprisingly both affordable and flexible – seems to be donor-advised funds (DAF).

You should obviously be cautious when taking tax, legal, and financial advice from someone who writes a blog, but it seems to me a DAF offers tremendous advantages in a simpler – and therefore lower cost – way than a foundation or trust, especially if your estate will not require the Full Monty of intergenerational wealth planning.

Most of the major brokerage houses and investment firms offer donor-advised funds, which appear to a nice, low-cost way to accomplish an expression of your values in your lifetime – and beyond! – without setting up a potentially complicated and expensive legal structure, such as a foundation or trust.

Here are some basics when you contribute to a DAF:

You can enjoy a charitable gift tax benefit in the year of your gift.

Your assets continue to grow in value, tax free, over time.

You don’t have to designate all of your charitable beneficiaries now, because your appointed trustees – such as you and your children – can designate gifts to charities over time.

Giving involves a simple call or note to the brokerage firm, which then confirms the recipient charity is legit. After verifying that, the money for your donation goes out to the charity in just a few days’ time.

Mostly what the DAF gives you, as I view it, is time to enjoy giving while you are still alive. That’s time to make future decisions and hold conversations with your children or other designated trustees about your values. I also like the idea that you get a chance, during your lifetime, to observe and reflect on the effect of your gift. Is the charity actually fulfilling its mission? Is it fulfilling your mission? And then, why not actually get thanked in person, rather than the grimmer path of grateful recipients having to thank a plaque with your name on it?

I looked up three different well-known, name-brand brokerage companies to check out fees and account minimums on their DAFs.

All three charged 0.6% annual fees on DAFs, with reduced fees on accounts over $500,000.

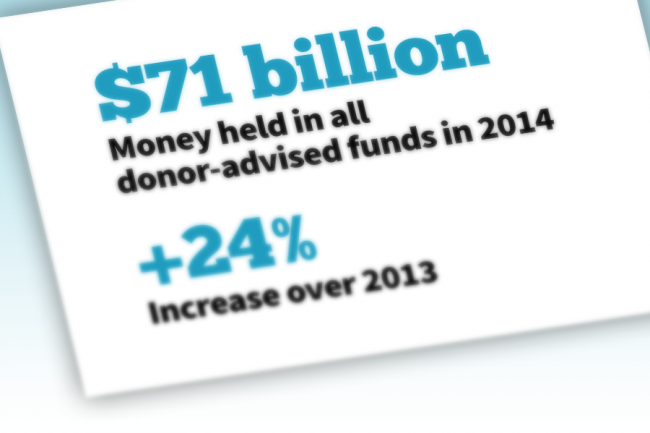

The National Philanthropic Trust reports the average DAF reached $296,701 in 2014. but clearly you can open up one of these funds for far less. Two of the three brokerage firms I looked at offer opening account minimums of $5,000, while a third required a $25,000 minimum.

What that says to me is that tax-advantaged, value-driven charitable giving of your wealth – both in your lifetime and beyond – isn’t something only available to the extremely wealthy. Instead, pretty sophisticated philanthropic vehicles are available to Main Street investors, who just happen to have a little surplus.

You can give your assets to the DAF this year, enjoying all available tax advantages of that gift now, and spend future years giving to worthy causes.

You can do this over time in consultation with your children or designated trustees, affording you the satisfaction of giving, as well as the pleasure of talking about and expressing your highest values.

I feel like there are lessons about philanthropy in John Paulson’s $400 million gift to Harvard that I haven’t seen explained yet.

I don’t know John Paulson (maybe that’s already obvious?) but I feel like I know a little bit about how he thinks, having worked with, for, and as a mortgage bond professional, and with, for, and as a hedge fund investor.

John Paulson is most famous for making $4 Billion in 2008 via the The Greatest Trade Ever, shorting sub-prime mortgage bonds through his eponymous hedge fund. Last week he shot back into the public eye for his philanthropy and the subsequent negative reactions to his gift, spearheaded by smart guys like Malcolm Gladwell and other pundits.

In reviewing reactions to his $400 million gift to Harvard’s School of Engineering and Applied Sciences, I’m struck that I haven’t heard an accurate description of Paulson’s reasoning, based on what we know about him. The overwhelming reaction of the smart guys is to complain that Harvard is one of the least deserving ‘charities’ around. Further, the conventional-wisdom smart guys complain, couldn’t he have found a charity to address poverty, or something more worthy, rather than make an already elite institution more elite?

Having worked with guys like Paulson, and understanding a bit about his professional background and track record, I know the following four things:

1. He’s focused on value. He would prefer to die rather than overpay for something.

What I mean by that is that when Paulson pays $400 million to Harvard for naming rights and also to get credit for the largest gift ever to a University, he’s not being careless about the amount. If he could get that kind of value for $375 million, he would have paid $375 million, not $400 million. Whatever the ultimate purpose of the gift (and I don’t pretend to know that, any more than I really know the inner thoughts of Paulson) he didn’t come up with $400 million by accident. And whatever his reasoning, and no matter how large the headline number, he was not overpaying.

2. He wants the #1 best thing. Not tenth best, not seventh best, not second best. Just the number one best thing. This next statement may sound flippant, and it may sound like I’m being Harvard-proud, and I really don’t mean to be. But if Paulson felt like he could have gotten what he wanted by donating to Dartmouth he would have done it. He chose Harvard because it struck him as the best.

Giving to ‘the best,’ obviously, is a different mind-set than giving to the ‘most worthy.’

Paulson’s critics feel he should have found a worthier cause than Harvard. Maybe so. But is that theoretical preferable charity the absolute best in the world at what they do? I suspect that criteria mattered to Paulson, as it does to many people who think like Paulson.

3. Risks matter tremendously. If he’s going to pay good money, the risks should be minimized. I think this point is probably key to why he didn’t give $400 million to a program to combat poverty, or end malaria, or whatever it is that Gladwell would have preferred he do. By giving to Harvard, Paulson can be certain that the institution will continue to thrive and be a steward of his funds 50 years from now. Did Paulson analyze the existing anti-poverty charities and find them too risky? I wouldn’t be shocked if he did.

Short of giving to the Bill and Melinda Gates Foundation1, I’m not sure how one gives huge sums of money to an anti-poverty charity at that scale while still minimizing one’s risks.

I’m not trying to argue that anti-poverty charities (or whatever Gladwell wants him to give to) are inherently risky. I actually have no idea. What I mean is that Paulson – by trade and by training as a hedge fund guy – has to be incredibly focused on risk management. You can’t succeed the way he has without applying the same eye for risk to one’s philanthropy. The one thing Harvard has over almost any other ‘charity’ is its image as a prudent low-risk investment.

Why would anyone like Paulson give to a ‘charity’ that already has a $36 billion endowment? Its a safe bet, that’s why.

4. The “smart guys” like Gladwell who represent conventional wisdom? Paulson does not give a fuck.

Just to expand for a moment on this fourth point, and to boil it down further with mathematical precision: Paulson gives precisely zero fucks what Malcolm Gladwell writes on Twitter.

Paulson’s “career trade” was made by understanding which way the entire mortgage bond market was positioned in 2008, and then he made the exact opposite bet, at extraordinary risk to himself and to his investors. In hindsight, he was a genius, but that move was incredibly difficult to make at the time, when every other short-seller of the mortgage bond market up until that point had gotten their ass handed to them.

Paulson’s smart enough to understand how the rest of the world thinks, but iconoclastic enough to lay that aside to determine what he alone thinks.

Most of us have a hard time going that strongly against the grain of public thought. Paulson’s entire career success is based on extreme contrarianism.

Lessons of Paulson’s gift

At the risk of trying to tie this all up with a neat bow, I think philanthropies can learn from the lessons of Paulson’s gift.

To appeal to a certain type of giver like Paulson, the point shouldn’t be to try to be the ‘worthiest’ cause in the universe, but rather to offer good value for the money. People who have made a lot of money in their lifetime tend to respond to value arguments – how will their gift have a bigger impact with you, rather than with someone else?

Further, are you the absolute best in your category? Forget neediness or worthiness. I suspect neediness is in fact a major turnoff for big donors. But excellence and being #1? Are you the Harvard of your category? I bet that’s very attractive to Paulson.

Next, are you a low risk? People who manage money for a living and who have a large fortune to steward want to see their money managed wisely, even after it’s given. Especially after it’s given.

Finally, does your donor give in order to be part of the in-crowd? Or to be an iconoclastic contrarian? We know by reputation that Paulson’s going to do whatever he thinks, not what the rest of the people think. That’s probably rare, but in the case of Harvard as a recipient, to their ultimate benefit.

I bet most people are social givers, eager to become or remain as a member of a social group, and philanthropic efforts to keep them appreciated as part of an inner circle probably matter a lot. Contrarians are rarer, but in Paulson’s case, can turn out quite nicely too.

[Fake full-disclosure/non-disclosure: I have given precisely zero dollars to my alma mater Harvard in the twenty years since I graduated from there, and I also give precisely zero fucks about Harvard’s philanthropic needs.]

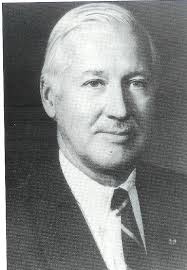

If you haven’t heard of Shelby M.C. Davis – and relatively few people have because he’s a very private person – you’re missing the story of one of the world’s great investing families, as well as one of the world’s most generous philanthropists. He’s an all-timer.

The most important wealth-creating decision Davis Sr. ever made – mirrored later by his son Shelby M.C. Davis – was to found his own business.

Davis Sr. trained as a New York insurance regulator, making a respectable but limited salary from the State. At age thirty-eight he quit his job, borrowed $50,000 from his wife’s family, and set himself up in business as a stockbroker, with a seat on the New York Stock Exchange, specializing in insurance stocks.

Shelby M. C. Davis, his son, made an equally fateful decision in 1968 when he left his job as an analyst at the Bank of New York to join a few partners to found the mutual fund company which eventually became Davis Selected Advisors.

Now, founding a own company does not guarantee wealth, because most new businesses fail, and because lots of people end up earning less working for themselves than they did working for others.[1]

On the other hand, equity ownership is the only way to create significant wealth. Every single large personal fortune – on the Forbes 400 list for example – results from business ownership, usually highly risky and undiversified to start. It might not have worked out – and undoubtedly even the Davises felt the risk of failure in the beginning – but owning their own businesses was the key first step.

Specialized knowledge

Davis Sr. – sitting in his insurance-regulator seat – gained deep insight into the insurance business at a particularly propitious moment. In the post-World War II era, insurance companies traded at extraordinarily cheap valuations.

Davis also happened to combine two great insights. First, he understood value investing before the world had even heard of Warren Buffett. Davis was the president of value-investor Benjamin Graham’s stock analysts’ organization in 1947. Second, Davis dug deeply into the investment portfolios and business practices of insurance companies.

Shelby Collum Davis

The result of Davis combining these two specialized insights closely resembled Warren Buffett’s path to wealth. Davis’ built his $50,000 initial investment stake into a personal fortune worth close to $900 million by the time he passed away in 1994. As the book reports, most of those gains came from purchasing insurance company shares, just as Buffett’s fortune grew from post-World War II insurance company ownership as well.

Shelby M.C. Davis, his son, invested in a wider variety of US and multinational companies, but his methods sprang from his father’s focus on specialized knowledge. Most importantly, Davis developed the art and science of deep dives into the quarterly reports of public companies as well as thorough independent research to discover attractive companies – classic value-investor practice.

Borrowing to the gills – leverage

Shelby Davis Sr. began his insurance brokerage with limited funds – $50,000 in 1948 – but took advantage of his ability to borrow money as a broker-dealer. Because of consumer protection laws, individuals who purchase stocks “on margin” through their broker can only borrow 50% of the value of their investment. A broker-dealer on the other hand, is allowed to borrow far more, limited mostly by what others are willing to lend them.

Davis Sr. purchased beaten-down insurance stocks for a living, and that alone might have made him a small fortune over his lifetime. Using borrowed funds as a broker-dealer, however, made him a huge fortune. The difference was that he magnified his returns by borrowing huge sums of money for decades.

Of course leverage can giveth, and leverage can taketh away. Sometimes borrowing huge amounts of money leads to a massive blowup of wealth. In Davis’ case, leverage enhanced rather than destroyed his fortune.

In a sense, all fortunes require leverage. Sometimes this is achieved by borrowing huge sums of money as Davis did, or as many real-estate investors do. Sometimes the leverage is actually ‘operating leverage,’ as in the example of the top equity owner of a law firm who employs many junior attorneys to do the work for him while he reaps the benefits at the top of the pyramid.

More recently, social media firms like Facebook and Twitter achieve a different kind of leverage through massive network-effects. The programming and administration work required to support an online network of 10,000 people, for example, becomes much more interesting as a business proposition when extended to the currently estimated 1.3 billion users of Facebook. That’s another kind of leverage.

In any case, you need leverage to create huge wealth.

The $1,000 hot dog – tightwad behavior

Davis family lore tells of Shelby Davis, Sr. taking a walk with his grandson, Chris Davis, in Manhattan. Chris asked granddad whether he would buy him a $1 hot dog. Davis Sr. pounced on his grandson with an object lesson in thrift and compound interest.

Did grandson Chris realize that $1, invested wisely, would double in value in five years? Furthermore, did he realize that this $1, compounded over 50 years, when Chris would be his grandfather’s age, would become worth over $1,000?[2]

Grandfather Davis asked: “Are you so hungry you need to eat a $1,000 hot dog?”

And that, ladies and gentlemen, is how wealthy people get, and stay, wealthy. It’s also an elegant lesson summarizing the key points of pretty much any book on building long-term wealth.[3]

Luck

Let’s face it: Nobody builds a great fortune without a tremendous amount of luck. While it may be true that “the harder I work, the luckier I get,” many hard-working brilliant people who combine business ownership with specialized knowledge and leverage do not achieve the fortunes they seek.

In Davis Sr.’s case, two pieces of luck stand out.

First, he began making leveraged investments in insurance stocks just at the beginning of a period of extraordinary growth. While he had the discipline to never sell, his leveraged investment at the time of a profound equity market downturn could have led to a forced a sale. Luckily for him, his fortune did not suffer that fate.

Second, as author Rothchild describes, Davis Sr. took a pause from investing his fortune between 1968 and 1975, when he served as US ambassador to Switzerland. During that period a bear market in stocks crushed his then-personal fortune of $50 million down to $20 million.

While historical counter-factuals are difficult, Rothchild wonders what would have happened had Davis been more actively involved in investing during those years. His distance from the investing world in precisely those years may have been a piece of extraordinary financial luck.

Later, between 1975, when Davis Sr. returned to managing his money, and his death in 1994, his fortune soared with markets to nearly $900 million.

Giving it all away

Interestingly, Davis Sr. set an amazing precedent with his fortune. He was determined that his heirs should not be handed a large fortune to inherit, so he dedicated the vast bulk of his money to political causes he believed in.

Shelby MC Davis

His son, Shelby, who established his own mutual fund business independently of his father, earned his own fortune. Although Shelby Jr.’s sons have taken over management of that business, he has made it clear to them that they will not inherit his wealth either.

In fact, I met Shelby Davis because he is in the process of giving away his fortune, as fast as he can, to support higher education for students from all over the world.

Another reason I’m interested in this book, and the Davis family

Shelby M.C. Davis, the son, happens to be a personal hero of mine.

Around the time he turned 60, Davis deeply embraced his father’s model that children should not inherit money. Children should be taught important lessons about building wealth, but ultimately they need to stand on their own and earn their own way.

The Davis family mantra is “Learn, Earn, Return” – describing the 3 phases of a good life. After studying at Princeton and working for Bank of New York in his first thirty years of Learning, and then building a successful mutual fund company over the next 30 years of Earning, Shelby decided to Return the bulk of his wealth to a cause he believed in, just as his father had.

In the late 1990s he worried that American students were overly parochial in their understanding of the world beyond our borders. The future, he believes, belongs to people who can think and act internationally.

Davis discovered the United World College of The American West – a two-year International Baccalaureate high school with 220 students from 70+ countries, dedicated to leadership training, fostering an international social conscience, and bettering the human condition.

UWC Davis Scholars at Brown University

Over time, Davis realized that not just the US students, but also the students arriving from abroad, had the power to transform US higher education for the better by internationalizing US university campuses.

He invested – with little fanfare or even recognition – close to $100 million of his wealth in supporting this institution and its sister schools, the other 13 United World Colleges around the world.

Shelby, his wife, mother, and UWC Davis Scholars at Wellesley

On top of that extraordinary commitment, Davis currently supports 2,400 United World College graduates at 90 US universities studying for their undergraduate degrees, through the Davis United World Scholars Program. He’s spending tens of millions of dollars per year of his fortune on this program to simultaneously transform individuals’ lives and to internationalize US higher education.

He funds this commitment year after year, sending tens of millions of dollars out of his future estate, both to help the students and to ‘save his sons’ from the burden of inheritance.

Basically, it’s ridiculous. Shelby Davis is amazing.

I recommend reading The Davis Discipline because it shows how some people accumulate extraordinary wealth.

[2] Clever users of the compound interest or discounted cash flow formula will easily calculate that grandfather Davis was assuming an approximate 15% annual compound return. An aggressive assumption for sure, but he managed to earn better than that during his investing career.

In the spirit of my earlier posts on Philanthropy, I enjoyed this presentation, with its thought-provoking questions.

Question #1: Can I make a difference?

He offers this site as an innovative way to think about philanthropic giving, even on a modest salary: www.givingwhatwecan.org

Question #2: Do I have to give up my career?

He argues that banking and finance, for example, can allow you to earn a lot of money, in order to give away a lot of money.

Question #3: Isn’t charity bureaucratic and ineffective?Some are more effective than others.We can look at returns on charitable investment at a site like www.givewell.com

Question #4: Isn’t it a burden to give up so much?

On asking for money, in a simple three step process.

Warning: Metaphor in use.

Step 1. Find a donor.

Step 2. “Oh, hi, it’s you. Listen, can I ask you a favor? Can you hold my baby for a minute?”

Step 3. In a few moments, donor not only cuddles baby – but ends up nose-to-nose whispering nonsense noises – and then “I love you.”

If you’re trying to raise money for your organization, repeat steps 1 through 3.

Asking for money is no more difficult than “I love you.” If you can say that, and inspire someone else to say that, you can raise all the money you’ll ever need for your worthy cause.

I’ve been the Annual Fund Co-Chair of my high school[1] for the past three years. I’ve overcome squeamishness about asking for money by focusing on the shared love. I love the school, and I’m usually soliciting money from people who also already love the school. It’s the easiest thing in the world.

It shouldn’t be awkward

You’ve always assumed that asking for money is scary and awkward. So was dating in junior high – which typically does not involve ‘love’ in the most effective way.

But if you love your cause, and if you’re helping your donor fall in love with the cause and the people around it, you’re winning. You just need to say ‘I love you’ to your worthy cause and to help your donor say ‘I love you’ to you and your cause. And that’s it.

The asking part follows naturally for people who fall in love with a cause.

Is it hard to ask the other parent of your infant child to warm up a bottle in the middle of the night? No, it’s the easiest and most natural thing in the world.

But what about data?

You’ve read that the world of philanthropy is different now – in particular now that metrics and data have taken over the process. You’ve learned that your non-profit must be business-like and show a ‘return on investment.’

Yes and No.

Best business practices like data-collection, efficiency, and metrics help you do your job better, so should be adopted by your organization for their own sake. But if you’re collecting data just to have something to show current and prospective donors, you’re not making good use of anyone’s time, or making good use of the data itself.

Track numbers that matter and improve your non-profit practice all for their own sake, and that’s all the ‘metrics’ you’ll ever really need.

Irrational love

At the moment of giving, donors must have an irrational love for what your organization does better than anyone else.

All the data in the world cannot make a donor fall deeply, madly, irrationally in love with you and your cause. Data doesn’t lead to love, only to a rational comparison between your group and someone else’s worthy cause. Which rational comparison mindset is a place you don’t want to be if you’re trying to raise a lot of money.

When you think about it, the act of giving away money is totally irrational, so the more you engage a donor’s rational thought process, the further you are from success.

Donors give because they love the people in the organization – or because they love some tender feeling that your group inspired.

Of course data helps you do your job, but only love inspires donors.

So stay focused on the love.

If you raise money for an organization, remember this most important step:

I’ve written before that the key to being wealthy involves work, and in particular, work doing something you would do regardless of whether it pays or not.

But giving money away is also a cause and effect of feeling wealthy.

We know we have enough money when we begin to give it away to others.The act of giving it away – philanthropically – signals to ourselves that we have a surplus.When we give philanthropically, however small and however temporarily, our life feels abundant.

We feel our own surplus most fully when our cup runneth over to fill someone else’s cup.If our goal is wealth, then we have to think about philanthropy.

Give of yourself, not just money

Sometimes we give money as a defensive mechanism, a kind of polite “go away” signal.

The homeless man, smelling of last month’s produce, received a little bit of money out of your pocket this week.But really your message was “Please don’t come any nearer.”I don’t think of this as philanthropy.

Similarly, but on a larger scale, I often hear of people giving much larger sums to causes they do not particularly believe in.But because they could not think of a polite way to say no to a friend, or they could not come up with a more effective way to fill a void in their life, they gave a significant amount of money.This isn’t philanthropy either.

Neither the homeless donation – nor the larger check – makes us feel wealthy in the way philanthropy can and should.

Philanthropy starts with the heart and may not involve the exchange of money for a long time.

If you are relatively young, or relatively light in the wallet, you can still start your philanthropic life.

Giving of your time and your expertise to a non-profit cause provides all of the benefits of giving money.You will capture the essence of philanthropy – that feeling of abundance, that feeling of working without expectation of compensation – long before you’re writing big checks to your favorite organization.

Lead with love, money will follow

The personal benefits of philanthropy – in terms of feeling wealthy and feeling the abundance of life – follow from the attitude and actions of you, the donor, rather than from your fortune.

Do you love the cause you support?Do you love the people in the organization?Are you offering something unique that you can give the organization?

Personally, I’m not a ladle-the-soup kind of guy.I have never felt my unique contribution to an organization would be serving food at the soup kitchen.

I know my way around a spreadsheet, however, so I have been fortunate enough to offer a set of financial eyes to my favorite non-profit, my high school for students from around the world.[1]

I love and believe in the school as one of the best hopes for a better world.I have built and sustained deep relationships with people there, both when I attended as a student and now as an adult advisor.It represents for me a source of love as well as a way to access my more generous self.

In my Wall Street and investing days, the fact that I gave time and money to my school helped me feel part of something larger and better.My financial day job – first as a bond salesman and later a distressed debt investor – did not fill this need. Despite the spiritual impoverishment of my Wall Street career, giving time, money, and love to my school made me wealthy.

[1] The best high school in the country, by the way, and I’m serious about that.It’s called the Armand Hammer United World College – USA. I know you’ve never heard of it, and that kills me because it’s the Best. School. Ever. And you know what? You’re in luck. We’re wrapping up the Annual Fund drive this month. Feeling wealthy is just a click away for you!

If you face the high-quality problem of finishing your life with too much money, you’ve probably already figured out that three groups, and three groups only, get your surplus: The government, your family, and your preferred charities. Of these, we typically all agree about leaving the lowest legal amount to the government. Then we face tremendous stress about how to allocate our fortune between the other two.

If you face the high-quality problem of finishing your life with too much money, you’ve probably already figured out that three groups, and three groups only, get your surplus: The government, your family, and your preferred charities. Of these, we typically all agree about leaving the lowest legal amount to the government. Then we face tremendous stress about how to allocate our fortune between the other two. Second, the key to lowering stress in estate planning is to put your personal values in the center of the plan. More than 60 percent are stressed about the tension between their values and their children’s values, which means they have not sufficiently figured out answers to the questions: What do you believe in? What do you stand for? What people or organizations or values represent the highest expressions of meaning in your life?

Second, the key to lowering stress in estate planning is to put your personal values in the center of the plan. More than 60 percent are stressed about the tension between their values and their children’s values, which means they have not sufficiently figured out answers to the questions: What do you believe in? What do you stand for? What people or organizations or values represent the highest expressions of meaning in your life? Most of the major brokerage houses and investment firms offer donor-advised funds, which appear to a nice, low-cost way to accomplish an expression of your values in your lifetime – and beyond! – without setting up a potentially complicated and expensive legal structure, such as a foundation or trust.

Most of the major brokerage houses and investment firms offer donor-advised funds, which appear to a nice, low-cost way to accomplish an expression of your values in your lifetime – and beyond! – without setting up a potentially complicated and expensive legal structure, such as a foundation or trust. I looked up three different well-known, name-brand brokerage companies to check out fees and account minimums on their DAFs.

I looked up three different well-known, name-brand brokerage companies to check out fees and account minimums on their DAFs.