If you face the high-quality problem of finishing your life with too much money, you’ve probably already figured out that three groups, and three groups only, get your surplus: The government, your family, and your preferred charities. Of these, we typically all agree about leaving the lowest legal amount to the government. Then we face tremendous stress about how to allocate our fortune between the other two.

If you face the high-quality problem of finishing your life with too much money, you’ve probably already figured out that three groups, and three groups only, get your surplus: The government, your family, and your preferred charities. Of these, we typically all agree about leaving the lowest legal amount to the government. Then we face tremendous stress about how to allocate our fortune between the other two.

This post not only nudges you toward door number three (your favorite charities!) but advocates a tax-efficient, low-cost way to do it, available to people of even modest means.

But first, the problem of children.

Many choose to prioritize their children or relatives first, which is fine, whatever, it’s your dollar. My own personal starting point about inheritance discussions is this: children do not deserve free money.

This partly explains why I like estate taxes more than other forms of taxation.

However, I realize we’re not going to all agree on that one, and I’m not (yet) in a position to vastly increase federal estate taxes.

Meanwhile, what do people facing a wealth surplus worry about? Merrill Lynch – in a 2015 report titled “How Much Should I Give To My Family? On the Risks and Rewards of Giving ” – found two problems when they surveyed their high net-worth clients. First, 42 percent of respondents plan to pass on their assets only AFTER their death, rather than while they’re alive. Second, more than 60 percent of high net-worth clients worried about the potential negative effects of inherited wealth on their children.

The problem, as Merrill Lynch and other financial advisors will likely agree, is that those findings bump up against two well-known estate-planning principles.

First, giving away money during your lifetime – rather than after your death – is the most efficient way to minimize taxes on transferring your wealth. And 42 percent of Merrill Lynch respondents weren’t planning that. So now all we need is a (tax-efficient, low-cost) way to give money away while you’re still alive. Keep reading.

Second, the key to lowering stress in estate planning is to put your personal values in the center of the plan. More than 60 percent are stressed about the tension between their values and their children’s values, which means they have not sufficiently figured out answers to the questions: What do you believe in? What do you stand for? What people or organizations or values represent the highest expressions of meaning in your life?

Second, the key to lowering stress in estate planning is to put your personal values in the center of the plan. More than 60 percent are stressed about the tension between their values and their children’s values, which means they have not sufficiently figured out answers to the questions: What do you believe in? What do you stand for? What people or organizations or values represent the highest expressions of meaning in your life?

If it’s all about your children, cool, give them the money. If you have other values you want to express as well, however, let’s talk about donor-advised funds for a moment.

Donor Advised Funds

What’s the best way to give away money during your lifetime? Although that’s too broad a question, I’m going to opine anyway. A very good way – surprisingly both affordable and flexible – seems to be donor-advised funds (DAF).

You should obviously be cautious when taking tax, legal, and financial advice from someone who writes a blog, but it seems to me a DAF offers tremendous advantages in a simpler – and therefore lower cost – way than a foundation or trust, especially if your estate will not require the Full Monty of intergenerational wealth planning.

Most of the major brokerage houses and investment firms offer donor-advised funds, which appear to a nice, low-cost way to accomplish an expression of your values in your lifetime – and beyond! – without setting up a potentially complicated and expensive legal structure, such as a foundation or trust.

Most of the major brokerage houses and investment firms offer donor-advised funds, which appear to a nice, low-cost way to accomplish an expression of your values in your lifetime – and beyond! – without setting up a potentially complicated and expensive legal structure, such as a foundation or trust.

Here are some basics when you contribute to a DAF:

- You can enjoy a charitable gift tax benefit in the year of your gift.

- Your assets continue to grow in value, tax free, over time.

- You don’t have to designate all of your charitable beneficiaries now, because your appointed trustees – such as you and your children – can designate gifts to charities over time.

- Giving involves a simple call or note to the brokerage firm, which then confirms the recipient charity is legit. After verifying that, the money for your donation goes out to the charity in just a few days’ time.

Mostly what the DAF gives you, as I view it, is time to enjoy giving while you are still alive. That’s time to make future decisions and hold conversations with your children or other designated trustees about your values. I also like the idea that you get a chance, during your lifetime, to observe and reflect on the effect of your gift. Is the charity actually fulfilling its mission? Is it fulfilling your mission? And then, why not actually get thanked in person, rather than the grimmer path of grateful recipients having to thank a plaque with your name on it?

I looked up three different well-known, name-brand brokerage companies to check out fees and account minimums on their DAFs.

I looked up three different well-known, name-brand brokerage companies to check out fees and account minimums on their DAFs.

All three charged 0.6% annual fees on DAFs, with reduced fees on accounts over $500,000.

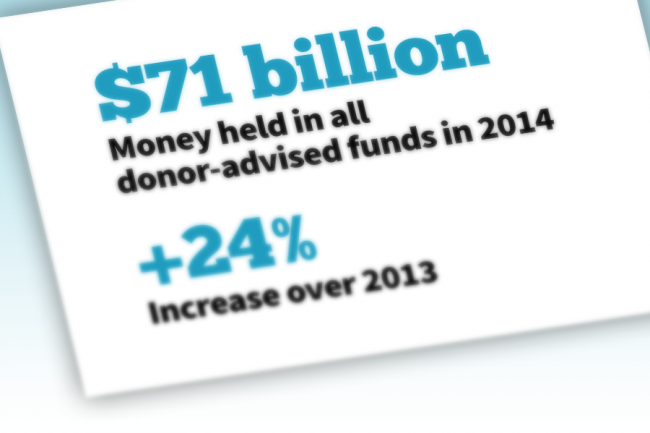

The National Philanthropic Trust reports the average DAF reached $296,701 in 2014. but clearly you can open up one of these funds for far less. Two of the three brokerage firms I looked at offer opening account minimums of $5,000, while a third required a $25,000 minimum.

What that says to me is that tax-advantaged, value-driven charitable giving of your wealth – both in your lifetime and beyond – isn’t something only available to the extremely wealthy. Instead, pretty sophisticated philanthropic vehicles are available to Main Street investors, who just happen to have a little surplus.

You can give your assets to the DAF this year, enjoying all available tax advantages of that gift now, and spend future years giving to worthy causes.

You can do this over time in consultation with your children or designated trustees, affording you the satisfaction of giving, as well as the pleasure of talking about and expressing your highest values.

That seems like a really nice legacy to pass on.

A version of this appeared in the San Antonio Express News and the Houston Chronicle.

Please see related posts:

Estate Tax Takedown – Levine v. Mankiw

Philanthropy Part I – Giving Money Away

Philanthropy Part II – Asking for Money

Post read (794) times.