Follow the money!

It’s not just “those corrupt folks” over there, it’s often “these corrupt folks” over here as well.

Post read (6826) times.

Follow the money!

It’s not just “those corrupt folks” over there, it’s often “these corrupt folks” over here as well.

Post read (6826) times.

Is mortgage debt good debt? A dangerous drug? Or both?

All debt acts like a drug.

Debt artificially changes your personal financial metabolism, accelerating personal consumption, and exaggerating investment losses and gains.

Like any pharmaceutical, debt can be life-saving. Without debt, you might have to wait an additional 10 years before you’ve saved up enough to own your home. Without debt, you might not be able to eat, between now and better employment, 3 months from now. Without debt, your further education plans never happen. Without debt, you’d be stuck. Debt can be awesome.

Like any pharmaceutical, debt can also be life-destroying.

A mortgage, because it’s the largest debt most of us can qualify for, is the ultimate drug. Just because a mortgage can make the dream of home-ownership a reality, provide investment leverage, offer tax advantages and a hedge against inflation doesn’t make it any less dangerous for certain parts of the population.

Mortgages are powerful drugs and in any given group of people some of us will abuse the pharmaceutical.

Please see related Mortgage posts:

Part I – I refinanced my mortgage and today I’m a Golden God

Part II – Should I pay my mortgage early?

Part III – Why are 15-year mortgages cheaper than 30-year mortgages?

Part IV – What are Mortgage Points? Are they good, bad or indifferent?

Part VI – What happens at the Wall Street level to my mortgage?

Part VII – Introduction to Mortgage Derivatives

Part VIII – The Cause of the 2008 Crisis

Post read (9574) times.

Mortgage banks will quote you a mortgage interest rate, with the option to pay more money upfront, in the form of ‘points,’ for a lower interest rate over the life of the loan.

Mortgage banks will quote you a mortgage interest rate, with the option to pay more money upfront, in the form of ‘points,’ for a lower interest rate over the life of the loan.

The quick answer to “good, bad or indifferent?“

Mostly bad, for most people.

It’s possibly good or indifferent under very specific scenarios.

One ‘point’ on a mortgage means precisely 1% of the loan principal amount. If you plan to take out a $200,000 mortgage, for example, and you pay 1 point upfront, you will pay exactly $2,000 additional at the mortgage closing, ie the time you take out the loan.

The effect on your interest rate of paying 1 point varies, but might be in the order of 1/4 of 1%.[1] At today’s rates, you might lower your 15 year mortgage interest rate from 3.75% down to 3.5%, which could lower your monthly payment on a $200,000 15 year loan by about $25.

Let’s do 30-year mortgages now.[2]

The effect of paying 1 point on a 30-year mortgage, or $2,000, could also be in the order of 1/4 of 1%, and you could lower your 30-year mortgage interest rate from 4.75% to 4.5%, providing approximately $25 in monthly savings. This is similar to the effect of points on a 15 year, except that a 30-year mortgage provides more time for monthly savings through the lowered interest rate.

The effect of paying 3 points on a 30-year mortgage, or $6,000, could be in the order of 5/8 of 1%, lowering your interest rate from 4.75% to 4.125%, providing approximately $75 in savings per month.

Does it make sense to pay points?

Not for most people.

The important thing to note, if you want to understand ‘points’ is that the monthly savings by paying points is a fraction of the upfront cost.

In the quotes above, after paying 1 point on a 15-year or 30-year mortgage, or 3 points on the 30-year mortgage, it will take 80 months to ‘break even.’ That’s $2000 upfront, divided by $25/month savings, or $6000 divided by $75/month savings.

Nearly 7 years to ‘break even’ on the optional points seeks like a long time to me. I don’t think of myself as particularly prone to refinancing or moving, but as I review my own 15 year history of real estate home ownership & mortgages, I realize I’ve taken out 5 different mortgages. No mortgage has lasted more than 4 years. Granted, this is during a period of falling interest rates[3] and I’m young enough to have moved a few times in that period, but still, I think most people can’t know for sure that they’ll be in the same place, in the same mortgage, for the life of a mortgage.

Points make even less sense on a 15-year mortgage than they do for a 30-year, since there’s less opportunity to ride out the life of loan, past the 7.7 year break-even point.

Receiving, rather than paying, points

My mortgage lender[4] also offers the option to receive points, essentially payment toward closing costs, in exchange for a higher mortgage interest rate. This process works the same way, except that you get $2,000 applied to lower your upfront costs but might agree for example to pay an additional 1/4 of 1%, raising the rate from 4.5% to 4.75%.

The breakeven calculation for ‘receiving points’ now would work the other way, in that you’re worse off the longer you stay in the same mortgage. In the specific situation that you knew you only wanted to stay in a house for 3 years, it might make sense to lower your closing costs through receiving points.

The larger issue, however, is that if you knew you would stay in a house for only 3 years you probably should think twice about buying, since home ownership is risky and you could end up losing money in the short run.

In sum, on mortgage points: Don’t do it. That’s all.

Tax deductibility of mortgage points

Ok, not quite all. One additional factor about paying mortgage points is that they are tax deductible in the year you signed the loan. Mortgage points are considered ‘pre-paid interest,’ which allows you to itemize them on your income taxes, just like other mortgage interest. Now, that is all.

Please see related Mortgage posts:

Part I – I refinanced my mortgage and today I’m a Golden God

Part II – Should I pay my mortgage early?

Part III – Why are 15-year mortgages cheaper than 30-year mortgages?

Part V – Is mortgage debt ‘good debt’ A dangerous drug? Or Both?

Part VI – What happens at the Wall Street level to my mortgage?

[1] There is not a precise formula for knowing in advance what effect paying points will have on the mortgage interest rate you’re quoted by a bank. These examples are real, taken from mortgage quotes I’ve asked for at today’s rates, but you can expect they’ll vary somewhat within a range. My goal here is to give a sense for likely ranges.

[2] I started with 15-year mortgage rates because, did I mention I refinanced into a 15-year mortgage?

[3] And that trend might have permanently reversed itself last month!

Post read (13399) times.

Why are 15 year mortgages cheaper than 30 year mortgages?

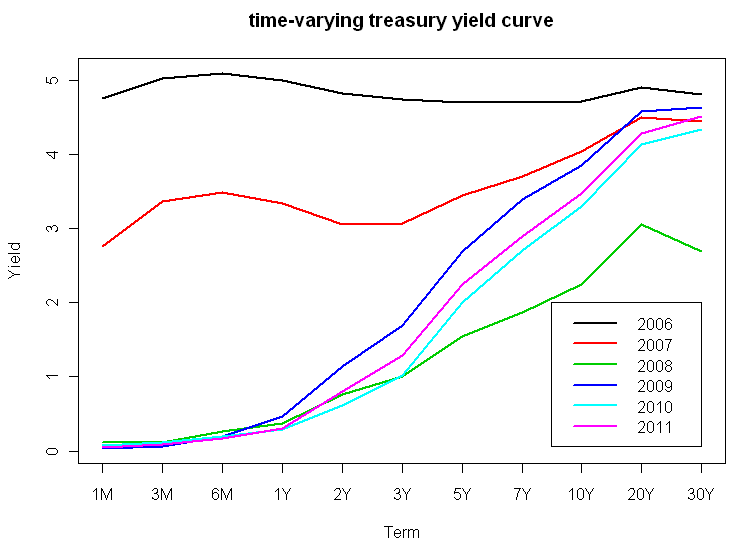

The answer has to do with the interest-rate curve. Contrary to what some may believe, the economy does not have one interest rate, but rather an infinite number of market-based rates, and dozens of important benchmark rates that determine the cost of money to different groups of borrowers.

Mortgage interest rates respond to market-based interest rates, which may be seen as an upward-sloping curve on a graph, showing a Y-axis of % interest rates and an X-axis of different loan “terms” that represent the cost of money for time periods from 1 day, to 3 months to 30 years.

Generally, 15-year mortgage interest rates trade somewhat below 30-year rates, as lenders charge less to lend money for 15 years than 30 years.

For that matter, generally 3, 5, and 7 year mortgage rates are lower than 15-year or 30-year rates, which is where the ‘teaser’ rates for adjustable-rate mortgages (ARMs) come from, before those interest rates float upwards at the end of a their 3, 5, and 7-year fixed period.

Mortgage borrowers historically refinanced after the fixed period, making it statistically reasonable – in pre-2008 crisis times – to charge lower rates for 3, 5, and 7-year interest rates. The fact that ARMs got combined in a toxic manner with sub-prime lending temporarily gave ARMs a bad name, although I think they’re great products, and I got a 5-year ARM in 2001 and a later a 3-year ARM in 2006.

Please see related Mortgage posts:

Part I – I refinanced my mortgage and today I’m a Golden God

Part II – Should I pay my mortgage early?

Part IV – What are Mortgage Points? Are they good, bad or indifferent?

Part V – Is mortgage debt ‘good debt’ A dangerous drug? Or Both?

Part VI – What happens at the Wall Street level to my mortgage?

Part VII – Introduction to Mortgage Derivatives

Part VIII – The Cause of the 2008 Crisis

Post read (11961) times.

Let me dispense with the major flaw in the book first.

The authors conducted a study in the 1990s of close to 350 millionaires, with an average net worth of $3.7 million, surveying them on their behaviors, spending patterns, lifestyle choices, and attitudes. From that review Stanley and Danko describe a composite “average millionaire” and explain the lifestyle factors correlated with US millionaires.

The real point of the book, the only reason to purchase it, is to learn how we, the readers, can replicate their success.

Yet the caustic financial critic Nassim Nicholas Taleb blasted their book in his own Fooled by Randomness for a statistical flaw. As Taleb points out, simply interviewing 350 millionaire ‘winners’ does not take into account the possibly thousands or millions of people who might have behaved in ways similar to the 350 but who did not end up millionaires. The study underlying The Millionaire Next Door suffers from “survivorship bias.”

This same “survivorship bias” leads to our thinking that all hedge fund managers in 2013 are rich – and have good investment track records – because we only look at surviving hedge fund managers, not the tens of thousands who have disappeared from the investment scene or gone out of business.2

Having pointed out the logical scientific flaw in their method, however, I would argue that Stanley and Danko are still worth reading. Even if their research does not rise to the level of a randomized placebo-controlled double-blind study that you’d require for true science, their correlations seem useful and right.

So what do Stanley and Danko say about millionaires?

They live below their means.

They allocate their time, energy and money efficiently, in ways conducive to building wealth.

They believe that financial independence is more important than displaying high social status

Their parents did not provide economic outpatient care

Their adult children are economically self-sufficient

They are proficient in targeting market opportunities

They chose the right occupation.

An enduring image from the book, introduced in Chapter 1, is the ‘big hat, no cattle’ phrase referring to people who appear wealthy, but really have little actual wealth. They spend money on showy things but finance their purchases with debt. (Now that I live in Texas, I enjoy hat and cattle references more.)

They state this point, re-state it, and then argue it some more, that the appearance of wealth – a fancy car, expensive trips, a three-story house in the right zip code – are not wealth itself but in fact – in many ways – the opposite of wealth. To the extent these raise the cost of people’s lifestyle, wealth is harder to achieve for those with expensive needs rather than ordinary needs.

One of the great things about Stanley and Danko’s “steps to being the millionaire next door” – in fact the key attraction of their best-seller – is the applicability to everyone’s life. “Live within your means,” as a step 1, works for anyone, with either $999,000 saved – or just starting out.

Please see related post The Millionaire Mind, by Thomas Stanley

Please see related post: All Bankers Anonymous Book Reviews in one place.

Post read (12190) times.

In the past year I subscribed to the newsletter of an investment adviser about whom I know very little. Pretty much every month he comes out with something awesome, and today’s newsletter was no exception. As I’m not a client of his I can’t vouch for him as an adviser but I like the way his mind works. I’ve excerpted the beginning of this month’s newsletter below:

In the past year I subscribed to the newsletter of an investment adviser about whom I know very little. Pretty much every month he comes out with something awesome, and today’s newsletter was no exception. As I’m not a client of his I can’t vouch for him as an adviser but I like the way his mind works. I’ve excerpted the beginning of this month’s newsletter below:

“You may have noticed that I rarely comment on the market or economy in this monthly newsletter and this month I thought I would explain why and also explain what we do focus on.

There are three reasons why I don’t talk or write much about what the market or economy might do in the near future:

First, no one – including me – generally knows. (See The Signal and the Noise by Nate Silver, Expert Political Judgement by Phil Tetlock, and The Fortune Sellers by William Sherden for example.) Known information is already priced into the market. It is only profitable to invest based on things you know that everyone else doesn’t! That type of knowledge is generally either a delusion (we really don’t know) or insider trading (which is illegal).

Second, there is so much other commentary in the media on the state of markets and the economy that I doubt I could add much of value to the babble. Indeed, I think the best thing we all could probably do is stop listening to most of it.

Third, the important thing is whether you can reach your long-term financial goals such as a comfortable retirement, a quality education for your progeny, or leaving a lasting legacy. What is expected to happen to the unemployment rate or what might happen to the Dow Jones Industrial Average in the immediate future has very little to do with accomplishing those goals. If I spent more time prognosticating it might give the misleading impression that the short term market gyrations are important.”

He’s also the author of something I think is the best summary 4 pages on investing I’ve ever found, which is on his site, but which I’ve uploaded to my scribd.com page as well.

He encourages folks to subscribe to his newsletter through his website. So I’ll encourage you to do the same, on his Ruminations Page.

Post read (4962) times.