Parents will recognize the following as the “If You Give a Pig a Pancake” problem, referencing the ubiquitous children’s book about giving a pig the first thing (a pancake) which leads to the next thing (some syrup), which leads to the next thing (a napkin), and so on.

For those of you who have not been parents in the past twenty years and aren’t familiar with the pig-and-pancake problem, file this one under the “Department of Unintended Consequences” Tab.

Fast forward a few weeks to a conversation she had with my Managing Editor (aka wife) last night.

“Mommy.I need money.”

“Why?”

“There’s a book fair at school but Daddy took all of my money and put it in stocks.And stocks are not fun at all.”

“I’m sorry dear.”

“Can I have an allowance?”

“Let me talk to Daddy.”

Ugh.It is true that I took all of her money.And converted it into shares of Kellogg stock.

And it’s also true that the steady stream of loose teeth – her main source of revenue via the Tooth Fairy – has dried up lately.There’s just no telling when the next tooth will drop, and then the school book fair comes up. Girls who don’t lose teeth don’t get paid.And then she needs fairy princess dolls, then it’s just all like, bills, bills, bills for my eight year old right now.You understand what I’m saying.

I didn’t hear about this conversation at first, but I noticed my oldest daughter kept prompting my wife to bring up some particular unnamed topic last night.

My daughter was eager for the conversation, but my wife strongly preferred that she and I develop a common strategy with regard to allowances, without having to simultaneously negotiate with an eight year-old.

(Here’s where I ought to insert some analogy between negotiating with 8 year-olds and negotiating with terrorists.Or lately, negotiating with Congressmen overly responsive to hard-core constituencies, encouraged by a system gerrymandered for incumbency.But I digress.)

Also, my wife assumed I’d have some strong ideas about what to do when it comes to kids’ finances.You probably won’t believe this, but I have a lot of thoughts about allowances.

If you give a pig a pancake, pretty soon she’ll ask for some syrup

Allowances!

So now we have moved, like the proverbial pig and his pancake, from the “first stock investment” phase to the “allowance phase” of parenthood.At this point my wife and I haven’t fully decided what to do, although I’m about to explain to you my best ideas so far, at least for the first month of her allowance.[1]

This is one of the cleverest allowance ideas I’ve ever come across, so I thought I’d share before even rolling it out to my family.

In fact he lists three great ways of teaching the power of compound interest to kids through the mechanism of the allowance.Each one has its own special advantage.

Cookie Jar Experiments

The power of compound interest – The Cookie Jar Experiments

Tobias describes three versions of what he calls the Cookie Jar Experiment, which over a month or two can viscerally and intuitively teach the magic of compound interest to kids through the mechanism of an allowance.

Version One. Offer your kid $1 on Day 1, and put it in a cookie jar.[2] Offer to add 10% more each day, as ‘daily interest growth’ on that original $1.

So, for example, on Day 2: $1.10 would be in the jar,

Day 3: $1.21. And then on

Day 4: $1.33.

After a month there will be a total of $17.45 in the jar, which shows how powerful 10% compounding can be, even if you begin with just $1.

Tobias suggests you probably won’t continue the experiment to the end of Month 3 ($5,313) or Month 6 ($28 million) but really that’s up to you and your own resources.

In my opinion, the power of compound interest as a concept is really worth teaching, so some of you will want to consider going the full 6 months.It will only cost you $28 million in total.If you do decide to do everything it takes to teach little Johnny the power of compound interest, be sure to email me at Bankers Anonymous so that I can provide my bank account number for the minimal 2% fee I normally charge for this kind of life-changing advice.

Anyway, back to my regularly scheduled commentary.While ‘real life’ doesn’t let you compound at 10% on a daily basis,[3] the experiment lets you demonstrate the amazing power of compound growth to your kids in a concrete way.

The 1 month time period – by which $1 grows to $17.45 – is short enough that kids can see the growth and just how powerful it can be.

Version Two.

This next version of the Cookie Jar Experiments is best for two kids, and it can drive home the power of compounding early, plus delayed gratification.[4]

Between your two kids, you offer a similar deal to version one, but with a twist. If one of them is willing to skip the first three days of interest accrual, they can get something desirable like a chocolate bar.

After they finish fighting over the chocolate, you run the experiment for, say, two months.[5] The child who went without the chocolate has $304, while the ‘lucky’ child who got the chocolate only has $228 in the cookie jar at the end of 60 days.

The lesson: Start saving early because it’s the earliest accruing period that matters the most.

The child with $304 can now buy a whole bunch of delicious cookies and leave the greedy chocolate eater weeping.

Are we having fun yet, kids?

Kids?Please stop fighting, please.Thank you.

Version Three.

“If only he’d used his powers for Good, instead of Evil.”

Run the same experiment as in Version One, but use the interest rate associated with many credit cards.Let’s pick 20% because it’s a round number, even though many people’s effective credit card rates are even higher.

Start adding money to the $1 at a 20% growth rate and label this ‘Credit Card’ growth. On Day 19 the ‘credit card’ account has grown to $32, versus the $6 to which the original savings at 10% per day grew.

If you run the comparison all the way to Day 35, the difference is $590 for the credit card account versus $28 for the ordinary 10% growth account. The key to this version is pointing out that some people scrimp and save and achieve some growth on their savings, while others pay huge portions of their money to credit card companies.

Here’s a video version of this allowance experiment:

Again, of course, whether you fill up a cookie jar with $590 is up to you and your family’s means, but you can create an unforgettable demonstration for your kids of how small differences in compound interest rates make for giant differences in the medium and long run.

So what will we do about the allowance request?

So will we decide to run these experiments on our children when they request an allowance?

I’m going to push for at least Version One to kick off the new allowance phase for my eight year-old.

If she complains, I’ve got a Jack Handey quote ready:

“One thing kids like is to be tricked. For instance, I was going to take my little nephew to Disneyland, but instead I drove him to an old burned-out warehouse. “Oh, no,” I said. “Disneyland burned down.” He cried and cried, but I think that deep down, he thought it was a pretty good joke. I started to drive over to the real Disneyland, but it was getting pretty late.”— Jack Handey

That’s why I say, deep down inside, she’s knows stock investing is fun. And so are Daddy’s experiments with allowances.

[1]After that, we may revert to a more typical $2/week, conditional on a usually-left-undone chore – cleanup of the girls’ room – that drives my wife nearly to glue-huffing, out of frustration, on a weekly basis.

[2] Or, wherever.Do cookie jars even exist anymore?

A friend recently asked me to speak to her company at an informal ‘Lunch and Learn,’ about a common financial problem many of us face, namely “How Can I Save Money?”

My initial thought – and some version of this is same thought occurs many times somebody asks me to help with anything[1] – is that I’m not the right person to lead that discussion.But I’ll get to that point later.As Suze Orman was apparently unavailable that day, I put together my thoughts, and this is what I came up with.

Beyond Rational Thought

Saving money, losing weight, or kicking addiction all exist in that realm of adult behavior change which are immune to rational solutions.

I can enumerate four good factual, rational, reasons to not eat cupcakes, but that rarely stops you from ordering the red velvet with icing and a cherry on top.

I can list 10 techniques for cutting out non-essentials from your daily expenses but you’re still probably going to blow $30/week on the Venti Iced Pumpkin Spice Caramel Double Shot Frappuccino, aren’t you?

(Incidentally, I don’t think it will work, but if you do want a list of at least 51 great ways to save money,the best chapter I’ve ever read on the topic is Chapter Two of Andrew Tobias’ excellent The Only Investment Guide You’ll Ever Need, which is entitled “A Penny Saved Is Two Pennies Earned.” I reviewed Tobias’ book here.)

Purchasing non-essentials doesn’t make any financial sense, and it certainly doesn’t help your diet when it involves things like cronuts, but we’re in the realm of deep subconscious decision-making here.You can’t rationalize your way into good decisions in this realm.

Can this Jedi help you save money?

Trick the Mind

In short, you need a Jedi.

My advice for someone struggling with saving money on a monthly basis is to realize that rational thought is helpless in the face of subconscious desires, and that only by tricking our rational mind do we have a chance.

Consequently, I’ve got three Jedi mind tricks to offer:

1. Hawthorne effect (aka, “Observer effect”)

Scientists – ranging from quantum physicists to weight-loss investigators – struggle with the “Hawthorne Effect” the idea that in the act of observing something we inevitably alter the thing we study.How does this relate to saving money?You can be your own frustrated scientist by studying your household budget, as I wrote in an earlier post.

You could decide to buy budgeting software like Quicken, or use an online service like Mint.com, or YNAB.com or just save your money and create your own Excel Spreadsheet.You’d need to record every single monthly expense, then categorize it into essential, useful, and non-essential.

As you dig into where your money goes and start observing closely, you will gather data. And that data can be helpful in its own right, but does not actually constitute the Jedi mind trick I’m talking about.

What I am talking about is that you will probably begin to skew the data in a positive direction by the mind trick of the Hawthorne effect.The longer and more closely you begin to observe your spending patterns, the more likely you are to shift your spending patterns toward a more positive direction.That skew that frustrates scientists will nudge you to better choices.

2. Radical Transparency and Positive Peer Pressure

As sober alcoholics know, most of us need a group.We need to be able to tell our story.

Having trouble saving money is hard enough, but it’s especially hard because it typically happens in secret.Our shame and personal struggle to save money is in our heads, and we console ourselves with the fact that at least other people don’t realize we have growing credit card debt.

And when we go out with our friends, we’ll happily pick up the tab because, shit, I don’t want anybody to suspect I’m broke.

Obviously, this is part of the problem.

As a result we’ve got to trick our minds.

Something that seems to work for saving money is radical transparency – oversharing with others who will cheer you on, pick you up when you fall, and ideally join you in the journey.

The first step on the journey would be to pick the peer group, and often including a partner or spouse would be an important first step.

Maybe they’ll come from your regular Wednesday 6am Yoga class.Maybe they can come from a subset of regulars at your favorite Magic: The Gathering game store.More likely, these days, you will draw your social network of radically transparent money savers from Reddit, or Facebook, or Twitter.

It doesn’t matter so much how you form the group. What matters is that you feel responsible to others and you don’t try to save money alone.

Each person in your group who commits to saving money further commits to transparently share their struggle, methods, successes, and failure in saving money each month.When you get tired of posting that you’re broke, or watching your friends do the same, you move that tendency to radical transparency in a positive direction and get people to help you form an action plan.

The reader profiles on a site like Free Money Finance are an attempt at this kind of radical transparency.

Forcibly trick your mind away from keeping your spending patterns secret, and instead tap into the pride and peer accolades you will get at making the difficult money-saving choice.

3. Out of sight, out of mind

I typically don’t use either of the two savings plans above, but I absolutely use this one.Money you don’t see is the best way to save.

If we don’t have money in our hand, or if in fact we never even see it in our bank, it’s much easier to forget that we ever had it in the first place.Which, naturally, means we’re more likely to save rather than spend.

Automatic payroll deduction is by far the most important Jedi money-saving trick available.

This one works, and it’s particularly awesome when saving for long-term problems like retirement or college tuition. If you’ve got an employee-sponsored 401K plan or 403b plan, there is simply no better way to create saving than to have your paycheck automatically deducted.

Automatic bank transfers, if you don’t have access to a 401K/403b plan, work next best.Most banks and most investment programs will happily set up automatic transfers between your accounts.Slipping a few hundred dollars per month out of your checking account into a savings account, or College saving 529 account, or a mutual fund account may be the only way for most of us to actually accumulate savings over time.

Most of us badly need this Jedi mind trick.

The least financially efficient – but still frequently used – version of this is the IRS tax withholding/refund trick which many of us use.We love it when the IRS sends us a few hundred or a few thousand dollars refund after we file our taxes.

Unlike automatic payroll deductions or automatic bank transfers, the tax refund trick is inefficient, as you end up giving the federal government a 0% loan until you get your refund.But it also constitutes a major part of many people’s savings plan.

But because ‘out of sight, out of mind’ works so well, we end up using tax refunds as a kind of savings plan as well.

When you feel artificially poorer you adjust your lifestyle and spending accordingly.

Concluding thought

Messing with yourself with Jedi mind tricks like ascience project, radically exposing your finances to others, and tricking yourself into feeling more poor than you really are – each of these techniques are irrational.Each of these operates on the subconscious in a way that doesn’t make perfect sense.

But because that’s often where the problem lies in savings money, that’s where the solution will come from as well.

Post-script: Incidentally, who is best qualified in your life to help you learn to save money?

It’s not me.

My guess is that the best person to help you figure out how to save money is somebody who has suffered from living beyond their means in the past, and who has developed effective strategies for overcoming this problem.

I’d rather ask a formerly-chubby-now-turned-Cross-Fit-stud for weight loss advice than I would the naturally skinny person who has never struggled with extra pounds.

Just like a recovering banker turned blogger has something to offer a society trying to recover from the particular affliction of banking, you need hard-won experience to understand and change certain behaviors.

Having told you why you shouldn’t take my advice, I went ahead and offered it to you anyway.Which is kind of irrational.I hope it works.

[1]I don’t think my instinctual “I’m not the right person” comes from pure laziness or avoidance of helping others.

However, I am reminded of this great piece of advice from Jack Handey:

“To me, it’s always a good idea to always carry two sacks of something when you walk around.

That way, if anybody says, ‘Hey, can you give me a hand?’ you can say, ‘Sorry, got these sacks.’”

Silver’s big idea is for us to move away from “I have the explanation and I know what’s going to happen,” to a different way of understanding the world characterized by “I can articulate a range of outcomes and attach meaningful probabilities to the possible outcomes.”

Bayesian probability

Bayes’ theory, Silver explains, helps us come up with the most accurate probability of some event occurring. Fortunately, it’s not too complicated.

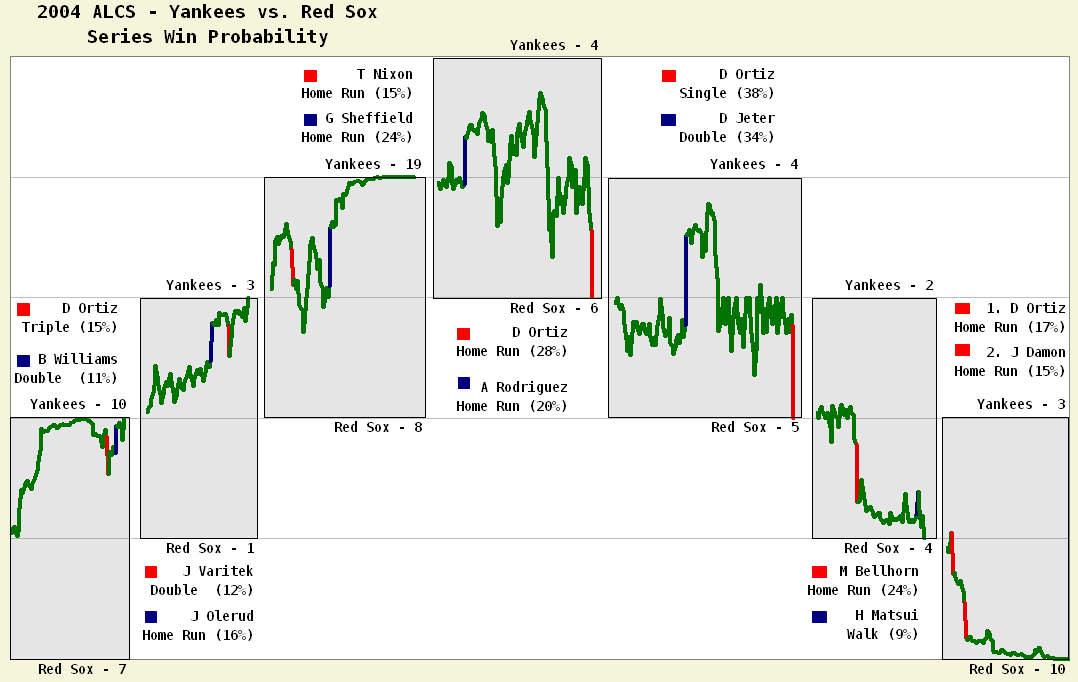

The Red Sox, of course, defy all probabilities

As we approach the MLB playoffs I’m fully aware of the irony of applying rational Bayesian probability to something as totally irrational, magical, and unlikely as Red Sox playoff outcomes.

My childhood and young adulthood consisted of them repeatedly snatching defeat from the jaws of victory. Both the Game Six World Series loss in 1986 to the Mets and the 2003 ALCS loss to the Yankees[1] defied all semblance of probability – we didn’t need a mathematical theorem to tell us that.

At the time, all we knew was that God personally intervened in baseball outcomes and that she enjoyed torturing us. And we hoped that God had plans for our redemption, some day.

We know now that, like the biblical story of Job, Red Sox Nation suffered for a reason. We now own the Greatest Sports Victory of All Time, coming back impossibly from devastating losses in the first 3 ALCS games in 2004 to vanquish the Yankees and sweep the Cardinals.[2] No sports victory has ever been as sweet as that. It was all so improbable. No math could ever explain that magic.

Greatest Sports Moments Ever, reduced to probabilities

And yet, I insist we try to learn Bayesian Probability today

Fine then.

To use it, we need to define three known (or assumed) variables, in order to come up with a fourth, unknown variable, which is the thing we want to know, the probability of an event.

The known or assumed variables will be:

X = an initial estimate of the likelihood of an event. This is called a ‘prior’ since it’s our best guess of some probability prior to further investigation. Before the playoffs even begin, how likely are the Red Sox to become World Series Champions?

Y = The probability that if some condition is met, the event will happen. In other words, how probable is it that a team that won the World Series had originally won their first game of the playoffs?

Z = The probability that if that same condition is met, the event will not happen. For a team that did not win the World Series, how probable is it that they won their first game of the playoffs?

The unknown variable, what we’re trying to determine, is our closest approximation of the probability of the event happening.

4. I’ll call that unknown variable V. What is the probability of the Red Sox winning the World Series, if they win their first game on Friday?

The math formula of Bayes’ theorem, using these four variables, is:

V = (X*Y)/(X*Y + Z(1-X))

I understand that formula makes no sense in the abstract, so that’s why we’ll illustrate it with the Red Sox.

We need an example using numbers, please

Since it’s that time of year, I’ll ask the key question on everyone’s mind right now:

If they win on Friday, October 4th – their first game of the playoffs, will the Boston Red Sox go all the way on to win the World Series?

We can now define variables and assign probabilites

The variable V (This is the unknown what we’re trying to solve for)

V is the probability that the Red Sox win the World Series this year, if they win their first game of the playoffs.

Variable X, our prior

I will make our prior –the initial estimate for the Red Sox winning the World Series – 15%. If all 8 playoff teams had an equal chance of winning the World Series my prior would be 12.5%, the percent equivalent of 1 divided by 8. But given that the Sox had the best record in baseball this year – and they have studs like Big Papi and Pedroia – I have to boost their prior to 15%.

Variable Y, the conditional probability that the hypothesis is true

One of the requirements for using Bayesian probability theory is that we insert a conditional probability. We can simply express this hypothesis as “If this happens, this other thing is made more likely.”

In our example I’ll make the non-crazy hypothesis that there is some positive causal relationship between teams winning their first game of the playoffs and teams that eventually win the entire World Series.

Let’s assume we know, from historical data,[3] that teams that won the World Series had previously won their first game of the playoffs 58% of the time. That’s our variable Y.

Variable Z, the false hypothesis variable

The false hypothesis variable in this example would be made from the 7 of 8 teams that historically begin the playoffs but do not go on to win the World Series. Of these non-champions, what is the probability they won their first game? I’ll estimate this at 45%[4]

Putting it all together

Using Bayes Theorem, we can now revise our estimate of the Red Sox winning the World Series, after the first playoff game has been played.

If the Red Sox win on October 4th, we can plug in variables X, Y and Z to determine the new probability of a glorious Red Sox World Series victory, variable V.

Remember: V = X*Y / (X*Y + Z*(1-X))

Plugging in our known and assumed probabilities, we get the

Summed up, if the Red Sox win their first game Friday[5], we would revise our probability of them winning the World Series up to 18.5% from 15%.

Intuitively, this makes some sense. There should be only a modest increase in the probability of a World Series championship after one game.

There’s a small positive correlation between winning the first game in the playoffs and eventually winning the World Series.

But even if it’s a blowout one way or another, let’s not get carried away. The chances of them going all the way is only up to 18.5%.

Martyrdom & bloody sacrifice go beyond rational thought

Anchoring effect of priors

We should note, and Silver emphasizes, that the anchoring effect of priors greatly influences our updated probabilities. In plainer English, our starting point for how we think the Red Sox are likely to do limits our ending point.

If we start with a prior that the Red Sox only have a 5% chance of winning the World Series, then their chances of winning the championship only jump to 6.3% after taking the first game, using my same assumed inputs.

Again using the same assumptions, if the Red Sox were 75% favorites to win it all, then a first game victory pushes them up to 79.5% favorites using the Bayesian Theorem.

Next Steps

If we want to follow the rest of the Red Sox playoff outcomes probabilistically, we’d take our revised prior – let’s say 18.5% after Game One – and come up with updated probabilities for variables Y and Z for Game Two. To use new Y and Z variables effectively we would need new historical data to determine the conditional probability of a World Series victory based on Game Two results.

Continued iteration

Nate Silver would advocate applying this constant iteration, revising our probabilities and priors as new information arrives, for a wide range of complex phenomenon that defy prediction. Will Mike Napoli’s beard change weather patterns inside Fenway? Is it not Nate Silver, but rather Big Papi who is the witch? Will super-agent Scott Boras release a karma-bomb press release on another client like he did with A-Rod during the 2007 World Series, effectively marking the beginning of the end for A-Rod? The probabilities change as the events unfurl.

Or not

Or conversely, we could just ignore all math, attach ourselves to one big idea, and never let go.

Because unrevised big beliefs, like sports fandom, do have their attractions.

[2] Incidentally, that 53 minute 30-for30 video of “the Greatest Sports Victory of All Time” I linked to on Youtube is totally awesome. Gives me the chils.

[3] I’m not a baseball stats geek with easy access to this kind of data, so I’m just making up numbers for the sake of illustration.

[4] Again, a stats geek could come up with the correct historical data to suggest a more accurate probability for the false hypothesis, but just work with me here a little bit on my completely made up numbers.

[5] And of course if my numbers were based on real data, rather than just picked out of the clear blue sky.

I took a mandatory course in high school[1] called “Theory of Knowledge,” meant to help us consider ‘How do we know things?”

“How do we know things?” turns out to be one of those big philosophical questions – dating from the time of Plato & Aristotle – irritating all of us for the last few millenia.

What Nate Silver addresses more than anything in The Signal and The Noise: Why So Many Prediction Fail – But Some Don’tis how we know things – in particular how we use and misuse information to understand and make predictions about complex phenomena such as baseball performance, political outcomes, the weather, earthquakes, terrorist attacks, chess, Texas Hold ‘em poker, climate change, the spread of infectious diseases, and financial markets.

Silver argues effectively that we frequently go wrong in many areas when we adopt a single model or approach to a problem, when an evolving, flexible, multiple-input, probabilistic approach would serve us better.

The problem of political pundits

Silver repeatedly returns in The Signal and the Noise to criticize political pundits on a TV show called The McLaughlin Group, on which commentators from the left and the right appear to make bold political predictions. Silver – among the most widely admired public forecasters of political outcomes – eviscerates this type of ‘prediction,’ citing data that shows these commentators make accurate predictions no more often than would a random coin toss.

But television rewards ‘bold stances’ and ‘big ideas’ of the type The McLaughlin Group traffics in, while largely ignoring more thoughtful approaches.

Silver labels and criticizes the “Big Idea” mindset that passes for political commentary on television in favor of a more modest, probabilistic, and empirical “Small Idea” mindset. Small ideas, nuanced, uncertain, and modest, however, make for poor television ratings.

But Silver does have a Big Idea himself

For complex, hard to predict phenomena[3], Silver explains his preferred method, based on a probability theorem attributed to an 18th Century English minister Thomas Bayes.

No doubt Silver thinks many more of us should become familiar with this branch of probability and statistics math. [4]

Beyond the Bayesian theory, however, Silver encourages us to adopt a probabilistic world-view. His big idea is for us to move away from “I have the explanation and I know what’s going to happen,” to a different way of understanding the world characterized by “I can articulate a range of outcomes and attach meaningful probabilities to the possible outcomes.”

Over time, as we refine our data gathering and multifaceted models, we can move our small ideas forward and become ‘less wrong’ about the world.

In the investment world the former style of traders – the one’s with big ideas and certainty – may have a good run of success, but generally get flushed out when markets turn. The best traders I’ve ever worked with think and speak in the latter way, considering new possibilities as markets evolve.

Some parts of this remind me of Nassim Taleb

The habits of mind Silver’s book encourages are not dissimilar to Nassim Taleb’s empirical skepticism, although they differ greatly in style and in points of emphasis. Taleb tends to be aggressively critical of everybody else’s models, whereas Silver more generously praises other theorists’ models and critiques his own.

Both Taleb and Silver share, however, a restless dissatisfaction with the inputs into our understanding right now. Both would say we do not know enough. We have not considered enough factors to explain whatever phenomenon we purport to explain. Our models need improvement and perpetual skepticism. The best we can do is to think probabilistically about future events.

Both encourage a learned humility about what we can know or patterns we think we observe in the world.

How does this relate to investing?

I’d estimate only about ten percent of Silver’s book explicitly addresses investing. As I mentioned, The Signal And The Noise is really a “Theory of Knowledge” book rather than in investing book.

But because Silver thinks like the best financial traders, uses probabilistic math effectively, and writes more clearly than almost anyone, his ideas are worth applying to investing.

1. Attribution of success

Among people who invest their own or other people’s money, 99.5%[5] of us attribute successful outcomes to personal investing acumen, while attributing unsuccessful outcomes to circumstances beyond our control.

The noise surrounding our own success – misinterpreting a generally rising market as stock-picking skill for example – leads us to overestimate our ability to influence investment returns. As a result, too many of us engage in security selection, or too many of us pay others to achieve superior investment results, despite the evidence that we’re overpaying.

2. Responsibility for failure

Conversely, our abdication of personal responsibility for losses – it must have been ‘the bad markets’ after all! – leads us to underestimate our own errors of judgment.

In both cases – success or failure – we’re prone to adopt an uncritical approach to the right level of responsibility for outcomes.

3. Efficient market hypothesis as an illustration of the Bayesian approach

Although Silver gives numerous examples of his Bayesian probabilistic approach to problems with numbers, one of his best examples is purely textual, on the efficient market hypothesis. He lists seven increasingly accurate, yet also qualified and probabilistic statements, on what we know about efficient markets.

The series of increasingly accurate, yet ‘less bold,’ statements are not only a great illustration of his big idea but also the right lesson for us on investing, so I reproduce it in full here:

b) No investor can beat the stock market over the long run.[7]

c) No investor can beat the stock market over the long run relative to his level of risk.[8]

d) No investor can beat the stock market over the long run relative to his level of risk and accounting for transaction costs.[9]

e) No investor can beat the stock market over the long run relative to his level of risk and accounting for his transaction costs, unless he has inside information[10]

f) Few investors can beat the stock market over the long run relative to their level of risk and accounting for their transaction costs, unless they have inside information[11]

g) It is hard to tell how many investors beat the stock market over the long run, because the data is very noisy, but we know that most cannot relative to their level of risk, since trading produces no net excess return but entails transaction costs, so unless you have inside information, you are probably better off investing in an index fund.[12]

The first approximation – the unqualified statement that no investor can beat the stock market – seems to be extremely powerful. By the time we get to the last one, which is full of expressions of uncertainty, we have nothing that would fit on a bumper sticker. But it is also a more complete description of the objective world.

If you want a 21st Century theory of knowledge, teaching you ‘how to think’ about the major world problems of global warming, financial crashes, avian flu, and terrorism, as well as ephemera like poker, chess, sports betting and baseball, start with The Signal and The Noise: Why So Many Prediction Fail – But Some Don’t by Nate Silver.

[1] Readers who study at an International Baccalaureate (IB) high school will be familiar with the “Theory of Knowledge” course. It’s a really great idea for a course, but I have yet to meet anyone who thought the experience of the course lived up to the idea that inspired it.

[3] Each chapter separately tackles baseball, political forecasting, weather, earthquakes, economic growth, infectious disease growth, sports betting, chess, poker, climate change, and terrorism – each in their own way posing a challenge of seeing into the future.

[4] The mathematics of Bayesian probability is relatively straightforward so I think I’ll try in a subsequent post to do it justice.

[5] I rounded down to be conservative, because that’s just good science.

[6] The original, powerful, efficient market thesis

[7] Because, clearly, some people sometimes do, for some period of time

[8] You can take some crazy stock-market risks and WAY outperform boring stodgy stocks much of the time. We have to match up comparable investment risk levels.

[9] A theoretical ‘market-beating’ high volume trading strategy often looks less market-beating when you take into account the frictions of trading.

[10] Inside information sure is helpful, when trying to beat the market

[11] Maybe some can do it, like Warren Buffett, but it’s super rare. Probably you can’t do it.

[12] So carefully hedged! So qualified and full of doubts! So true!