Hello Professor!

This is your former student, one year post personal finance class, and I am in need of advice.

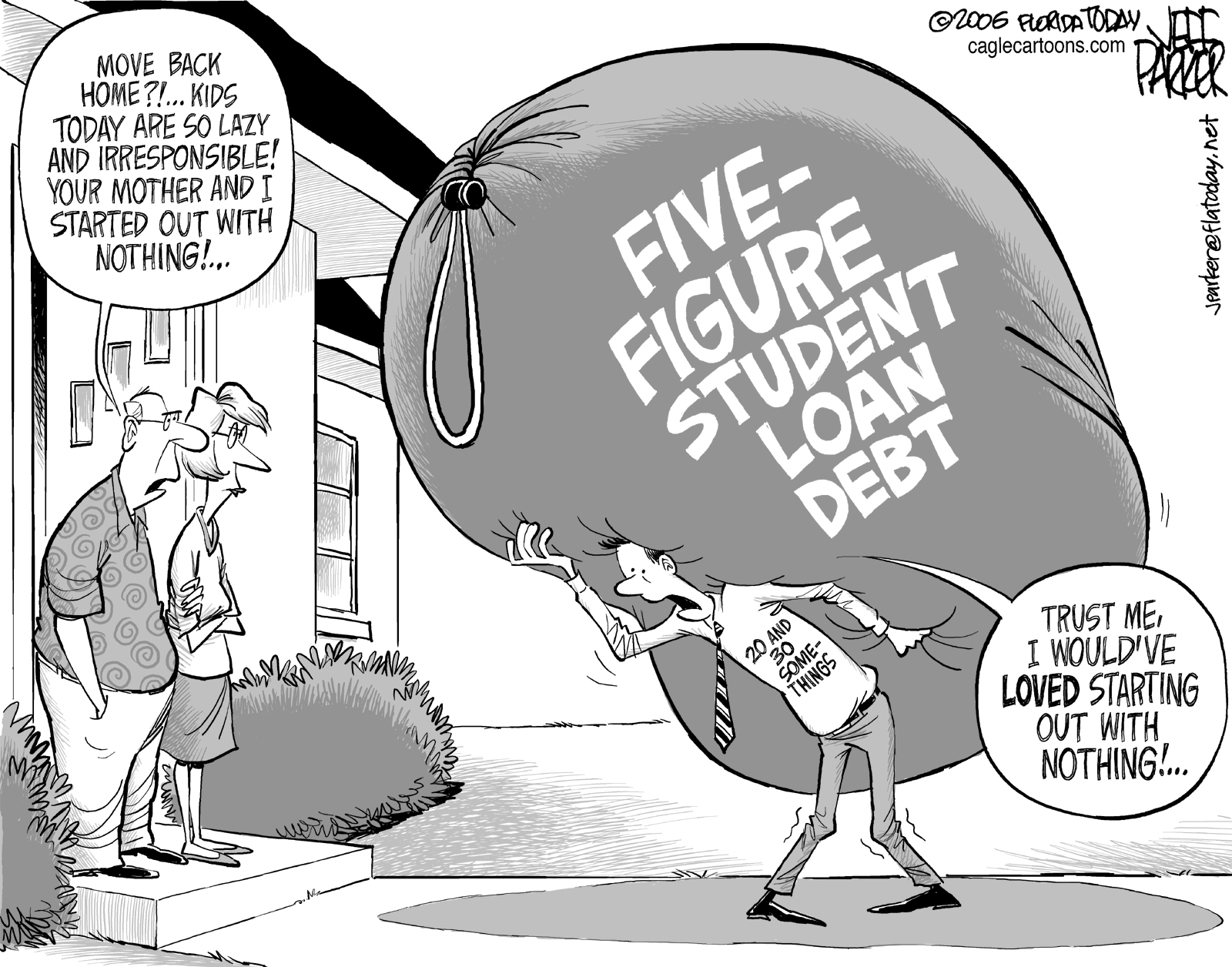

Here’s the backstory. After spending one year in the IT Consulting world, making 70K and being equally stressed to the detriment of my health, I jumped ship (per the advice of my employer, they noticed I wasn’t sleeping). I left on good terms and with a fair severance pay. At this point of life re-evaluation I like the idea of taking however much time is necessary to ensure that misery is not a part of my daily routine at my next gig.

I have about 30K in student loans not paid off, interest rates ranging from 3.4% to 5%. The actual breakdown:

- Loan A, minimum monthly payment $130/mo for 120 months: [12K @ 5%];

- Loan B, total 18K, minimum monthly payment for all of Loan B $150/mo for 120 months [10K @ 3.4%, 5K @ 4%, and 3K @ 4.5%]).

My monthly expenses run between 1K to 1.5K and I have around 15K in savings (not including emergency funds, which is 3K and then 4K in a HSA account which can only be used for health expenses, I’m wanting to use all of that 15K towards paying off loans).

What advice do you have for planning my budget? I want to remove as much principal from my loans now to lower my interest payments. I may be able to defer paying monthly payments with no interest accruing for both my loans citing unemployment as the reason, another case might involve interest accruing as normal but monthly payment not required.

Any and all advice would be appreciated, thank you! Let me know if any of this info needs clarifying.

Sincerely,

AF in Houston

——————

Dear AF,

Thanks for reaching out, I’m glad to hear you’re continuing to track a lot of the things we discussed in the Personal Finance course last year.

Congrats on building that cash cushion – that’s admirable and rare for anyone one year out of college. It sounds like unemployment is not as scary to you as being stressed out – so the cash cushion allows you to take some time to figure out the next step, which is really great.

The way I read your note, you mentioned three financial factors you’re trying to optimize, and then a few more unmentioned financial factors that I think you should include in the mix for decision-making.

Your mentioned factors:

1. Cash burn of $1,500 cost/month (aka unemployment)

2. $30K student loans

3. $15K savings

Your unmentioned factors:

1. Maxing out your Individual IRA when at you’re age 23

2. Finding work that covers your lifestyle costs and doesn’t leave you stressed out and unhealthy.

So…as far as important financial decisions in the next year, the most important is probably solving the issue of cash burn. You’ve got ten months, at your reported run rate, to solve that one (That’s $15K divided by 1.5K per month).

Ideally, you combine employment with the unmentioned factor #2, namely getting work that pays and keeps you healthy. Until you solve that one, I wouldn’t get aggressive about paying down your students loans.

Why do I say that?

If you decide to use your $15K cushion to pay down student loan debt, you shorten the time you have to get good, healthy work. Finding good work can take time. You don’t necessarily want to take another job that doesn’t suit you, and leaves you stressed out again, if you’re forced into the next job by the problem of running out of cash.

In addition, it’s very admirable to want to pay down your student loan debts with your savings, but in this particular situation I wouldn’t advocate that. Your student loan debt is low-interest debt, meaning it is compatible with good long-term financial decisions. (If you told me you had $30K in high-interest credit card debt, or any amount of credit card debt for that matter, I’d be strongly advocating paying that down as quickly as possible, as priority #1)

Then there’s another – in my opinion better – use for your savings if you’re trying to maximize your financial situation with your cash.

You didn’t mention contributing toward your $5,500 limit in an individual IRA. Hopefully you remember our discussion in class on the compounding effect of growing that money over the next 50 years. (Undoubtedly you can still do the math that shows your $5,500 becoming $101,311 fifty years from now at a reasonable 6% compound growth rate. Right? Please tell me yes.) Combine that with the 25% income tax relief you’d get on making a $5,500 contribution this year (so, up to $1,375 that you keep, not the federal government) and I think a strong case could be made for prioritizing your IRA contribution over student loan principal repayment.

Obviously you have to stay current on your student loans, but I don’t think its a bad idea to pay the minimal required amount, at least until you figure our your employment situation.

An implied part of my calculation here is that, given your education and past earning power, you’re capable of getting a high-paying job in the next year. The trickier part – in the long run – is finding a high-paying job that doesn’t leave you stressed and unhealthy.

My summary thoughts would advocate either of the following to routes:

The cautious approach – Hoard your cash long enough to get a good job, pay the minimum on your student loans, but don’t pay down principal on that debt until you’ve figured out how much your new job pays.

The more aggressive wealth-building approach – contribute generously to your Individual IRA (up to $5,500) and keep the rest in cash. That leaves you more like only 6 months to solve the cash burn problem (aka unemployment), but hopefully that’s enough time for a smart guy like you.

Feel free to write back and ask for more clarifications or even to challenge my assumptions.

Best of luck and keep me informed!

Michael

Post read (1051) times.