I downloaded a fin-tech app called Acorns a few weeks ago. I recommend you drop this blog post now, text your favorite twenty-something, and make sure they’ve downloaded this thing already. I am now an evangelizing convert.

Here’s a short list of problems many people have in getting started investing and building wealth.

- No money (duh, obviously)

- No time to figure out investing

- No interest in following stock and bond markets

- No confidence navigating investment choices

- No plan for ongoing automation of investments

- No experience avoiding high-cost service providers

Each of these problems afflicts twenty-somethings even more than the rest of us.

And yet, as any fifty year-old who wakes up from a few decades working and paying down debts learns (when they finally make that appointment with an investment advisor) even small amounts of money socked away decades ago would have made the problem of retirement and wealth-building so much easier.

But how does anyone even begin? As I’ve mentioned before, beginning is perhaps the hardest part of investing. Enter Acorns.

Endorsing a product

Now, I really hate to endorse a specific product or company when I write about finance topics, because part of my whole “ex-banker in recovery” identity is to form opinions without the reality – or even appearance of – “selling a product.”

Having said that, I’m almost annoyed with myself to say: this is an awesome product and every investment beginner should be using it. The crazy thing about Acorns is that they’ve addressed all six of the problems I listed above.

No money?

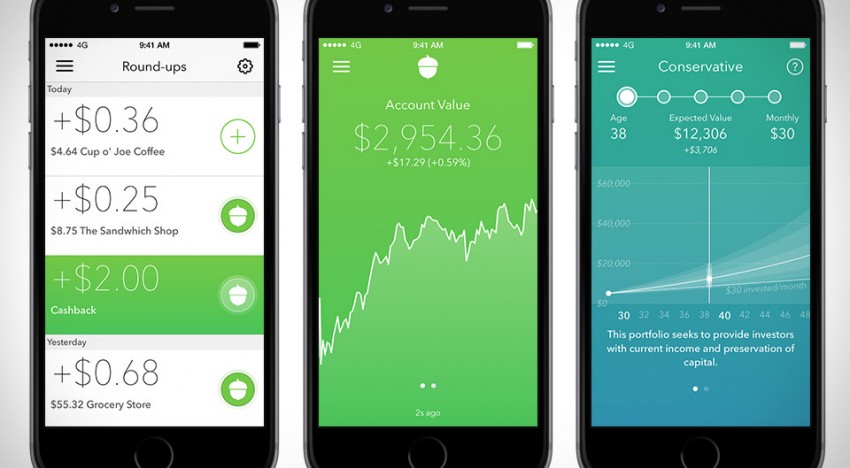

The app invites you to begin with an initial $5 bank transfer. The app’s opening pitch is that it will invest your “spare change.” They use a technique Bank of America pioneered about 10 years ago, which was to “round up” little transactional odd-lots – the equivalent of pocket change you’d throw into a coin jar at the end of the day – and invest it for you. Acorns tracks these spare change amounts from all accounts you choose to link – such as a debt, credit, or checking account – and automatically transfers it into an investment account. Pretty clever.

No time?

The app took about 5mins to get started, and another 3 minutes that first day entering a bit of personal data and linking bank accounts. I never spoke to a live human, which is great. I never set aside time to do it. I set it up on my phone, in between my kids talking to me about their day.

“No, sweety, I didn’t really listen to your story about the turtle. Can’t you see Daddy’s moving money around with his phone? This is 2 minutes of sacred Daddy-time.” (I’m a really good parent.)

No interest?

After about 2 minutes of entering personal information, the app suggests one of five portfolios on a risk spectrum from “Conservative” to “Aggressive.” Each of these is built from a blend of Exchange Traded Funds (ETFs) to get you exposed to bonds and stocks, but without having to know anything about these things. While I personally find markets fascinating, I think the ultra-simplification makes sense for everyone who finds stock and bond markets utterly dull.

No confidence?

With no investment choice to make beyond one of five portfolios on a risk spectrum, app users don’t get stuck by the deadly indecision-problem – what behavioral economists call “the paradox of choice” – in which we avoid something entirely because we can’t face the problem of choosing between too many options.

Based on my age, income and wealth, the app suggested the merely “Moderately Aggressive” portfolio for me.

“Are you calling me old?” I hissed angrily into my phone. I chose the “Aggressive” portfolio instead, like the middle-aged man who rents the black Camaro convertible because #YOLO.

No plan for automation?

This, right here, is the most powerful part of the Acorns app, since automation is the key to moderate-income people getting wealthy. The app continuously pestered me to commit to an automatic investing program, either daily, weekly, or monthly, and in any amount, from as little as $1 per transfer. It prompted me so many times that I finally agree to do it weekly, in an amount affordable to me.

By the way, nobody’s accumulating much money based on the “spare change” gimmick I described above, but this automated-invested feature is what will make a twenty-something a millionaire in the long run, with hardly any suffering along the way.

Cost avoidance?

Acorns charges $1/month until you get $5,000 with them, after which they charge 0.25 percent per year on your portfolio. This is the kind of rock-bottom robo-advisor fee that has the investment advisory business a little freaked out right now. I like it.

Acorns’ limitations

Can I come up with some criticisms of this thing? Of course I can.

- I personally wouldn’t choose a blend that includes even the 10 percent corporate and government bonds I got – despite the fact that I chose “Aggressive” as my allocation. Fortunately my “Aggressive” Acorns allocation is 90 percent risky, the way I like it.

- A person confident and informed about investments could do all of what Acorns does without paying the Acorns fees, obviously. Their fees are low, but yes you could do this yourself, fee-less.

- The simplicity of the app does not allow for a complete suite of investment activities. I happen to think simplicity almost always works better than complexity when it comes to our personal investments, but of course the entire money management industry is built on the opposite idea – the conceit that complex tools help us “beat the market.” Not only can you not execute butterfly call spreads or hedge foreign-exchange exposure with Acorns, but you can’t even buy individual stocks. Again, that’s a feature not a bug from my perspective, but shockingly not everyone sees things my way. (Not yet they don’t.)

- If you already have some wealth, and your system works for you without too much cost, Acorns seems mostly unnecessary. It’s definitely geared toward the “just getting started” crowd.

On the other hand, I’m not even the right demographic for Acorns, and I’m a total convert.

So…basically…like, download this thing right now.

A version of this post ran in the San Antonio Express News.

Please see related posts:

Getting rich slow through automation and small regular contributions

Getting started is the hardest part of investing

Automation may be the most important feature of your investment program

Post read (1985) times.

One Reply to “Check Out This Acorns Thing”

However Acorns provides zero support. No phone number or chat is provided. Your only option is email which will get you a promise to reply in 1-2 business days.