I’m not saying you should do this. In fact, very probably, don’t do this. In discussing early retirement plans with my buddy Justin recently, however, I learned for the first time about penalty-free ways of accessing retirement accounts early. This post is in the spirit of learning about obscure financial planning tips relevant to one in a thousand people.1

One hitch for young folks attempting FIRE (Financial Independence, Retire Early) is that traditional 401(k) accounts do not let you withdraw retirement savings, without a 10% penalty, before age 59.5. If you diligently socked away money into a plump nest egg in a tax-advantaged account in your 20s, 30s, and 40s, how would you access this money for your early retirement?

Justin mentioned two techniques known to FIRE Movement adherents for accessing retirement account funds early, without penalty. One is known as the “72(t) exception.” The other is “building a 5-year Roth conversion ladder.” I’ll take them one at a time.

The 72(t) exemption allows a person under 59.5 (the ordinary non-penalty retirement age) to lock in a fixed annual withdrawal amount from their retirement accounts, as long as that amount continues without fail until age 59.5, and also for at least five years. The amount withdrawn may be determined by an IRS table of ‘expected remaining life.’ That’s the same table that gets used for typical ‘required minimum distributions’ from retirement accounts after age 70.5. Or it could be determined by two other allowable methods that fix an annual withdrawal rate, based on either ‘annuitizing’ or ‘amortizing’ your account balances in an even, formulaic way. You can find calculators online that will let you compare withdrawal amounts between all three methods.

The bummer of this technique is that it’s entirely inflexible. Once you start retirement account withdrawals under the 72(t) exemption, you may not stop until age 59.5, even if your life circumstances change. In addition, any account that goes into 72(t)-mode cannot be contributed to anymore. It’s locked. And your withdrawal amounts are locked in.

Ben Gurwitz, Certified Financial Planner and Principal of San Antonio-based Financial Life Advisors, a fee-only financial planning firm, likens the 72(t) choice to “a straightjacket.” He also says that both in his previous work with a CPA firm and in his current work, reviewing hundreds of clients’ finances, he has never once had a client choose the 72(t) option. Probably because it’s weirdly inflexible. As he says, “Once you turn this thing on, you can’t turn it off.” If you decide not to retire, or you realize you need more (or less) income in retirement, you can’t really shift the 72(t) withdrawals in mid-plan.

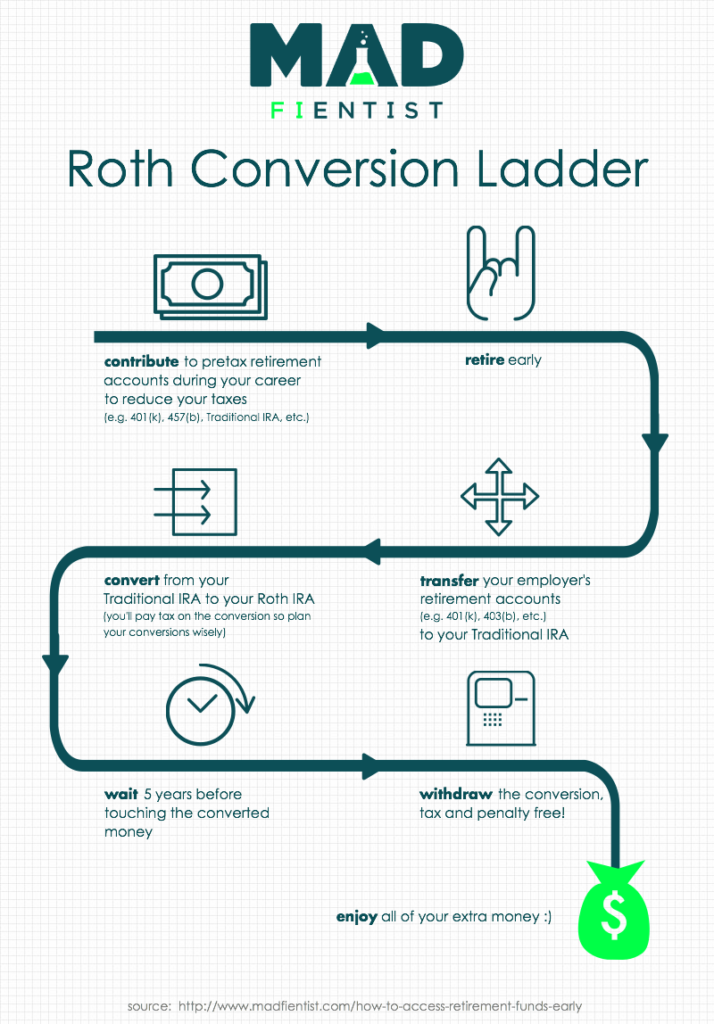

The second FIRE technique for accessing retirement account money early – The “5-year Roth conversion ladder” – is a lot more reasonable, and a lot more flexible.

As a reminder, Roth retirement account contributions are taxed upfront, but allow for tax-free withdrawals in retirement.

Because Roth money has been taxed once as income already, the rules are a bit more relaxed for how and when withdrawals can be made.

One semi-relaxed rule is that 5 years after converting funds from a traditional 401(k) to a Roth account, the Roth funds may be withdrawn penalty-free, even before age 59.5. You are required to pay taxes on 401(k) funds to make the conversion, but then the Roth money is available tax-free in the future. And because of larger annual contribution limits, it’s easier and more plausible to build up a sizeable nest egg in a 401(k) than in a Roth IRA.

Maybe an example would help. You’re 45 years old. You plan to retire at age 50. And you need to use the funds in your $250,000 401(k) to supplement your lifestyle costs, at least until you qualify, let’s say, for a combination of Social Security and a pension at age 59.5.

You begin to construct your “Roth conversion ladder” by converting $25,000 of your traditional 401(k) into a Roth IRA at age 45. You owe some income taxes on that conversion. You continue to do this conversion of $25,000 per year, every year, over the next 10 years, until the original traditional 401(k) is depleted. The goal is that by the time you hit age 50 – early retirement age – you can withdraw $25,000 from the Roth account without incurring any early-retirement penalty. By converting $25,000 each year starting at age 45, you should have $25,000 (or more, after investment gains) available to you as tax-free income each year beginning at age 50.

As long as your conversion was done at least 5 years prior, you can withdraw Roth converted amounts tax free and penalty free. That’s the basis for the “5-year Roth conversion ladder” strategy for early retirement folks.

Gurwitz concurs this is a more flexible approach to early-retirement planning, and a technique that in no way restricts future income or decisions. If one decides to not retire at age 50, besides having paid taxes, there’s no particular downside to having converted traditional 401(k) retirement funds into a Roth.

Gurwitz agrees with me, however, that the concept of FIRE itself may be the problem, in so far as people are eager to quit work. The “work is just a means to an end,” approach maybe misses the bigger picture about the value of work in our lives, he says. “They [FIRE adherents] are shooting at the wrong thing.”

Another problem he sees, partially reflecting what he does for a living, is people trying to do this entirely on their own. Planning for retirement, and especially early retirement, can be complicated. But the kind of person who passionately reads FIRE blogs is also precisely the kind of person uninterested in paying a financial planner.

So they probably wouldn’t walk in the door to ask for advice about the 72(t) or a “5-year Roth conversion ladder” in the first place. Gurwitz cautions against that do-it-yourself approach.

Says Gurwitz, “I would encourage people to seek the advice of a professional. If they can’t afford to see a professional, they probably can’t afford to be financially independent and retire early.”

I’m a do-it-yourselfer when it comes to my own personal finances. But I think I’m in Gurwitz’s camp when it comes to next-level FIRE strategies, which are kind of complex.

So, as Smokey the Bear might say, don’t play with matches kids, and seek professional help before you start your FIRE.

A version of this post ran in the San Antonio Express News and Houston Chronicle.

Please see related posts:

FIRE Part I – Taxonomy of the Different Retirement Styles of the Young and Independent

FIRE Part III – On the Importance of Being Frugal

Post read (732) times.

- “Per usual,” you mutter under your breath. Hey now! I heard that! ↩