It’s January, the month named for Janus the two-faced Roman God who looked both backward to the past and forward to the future.

It’s January, the month named for Janus the two-faced Roman God who looked both backward to the past and forward to the future.

Looking back over 2016, I realized that I learned about three types of investment accounts, each of which – depending on your phase of life – might make for a nice New Year’s Financial Resolution.

Maybe best of all, all three investment accounts work well even if you start with small dollar amounts. And they each scale up to larger amounts, if you have the means.

Contemplating the start of a new year prompted me to divide these investment account ideas into three categories, past, present, and future. Or you could categorize them as investment accounts for the young, the middle-aged, and the old. I’ll start with the young.

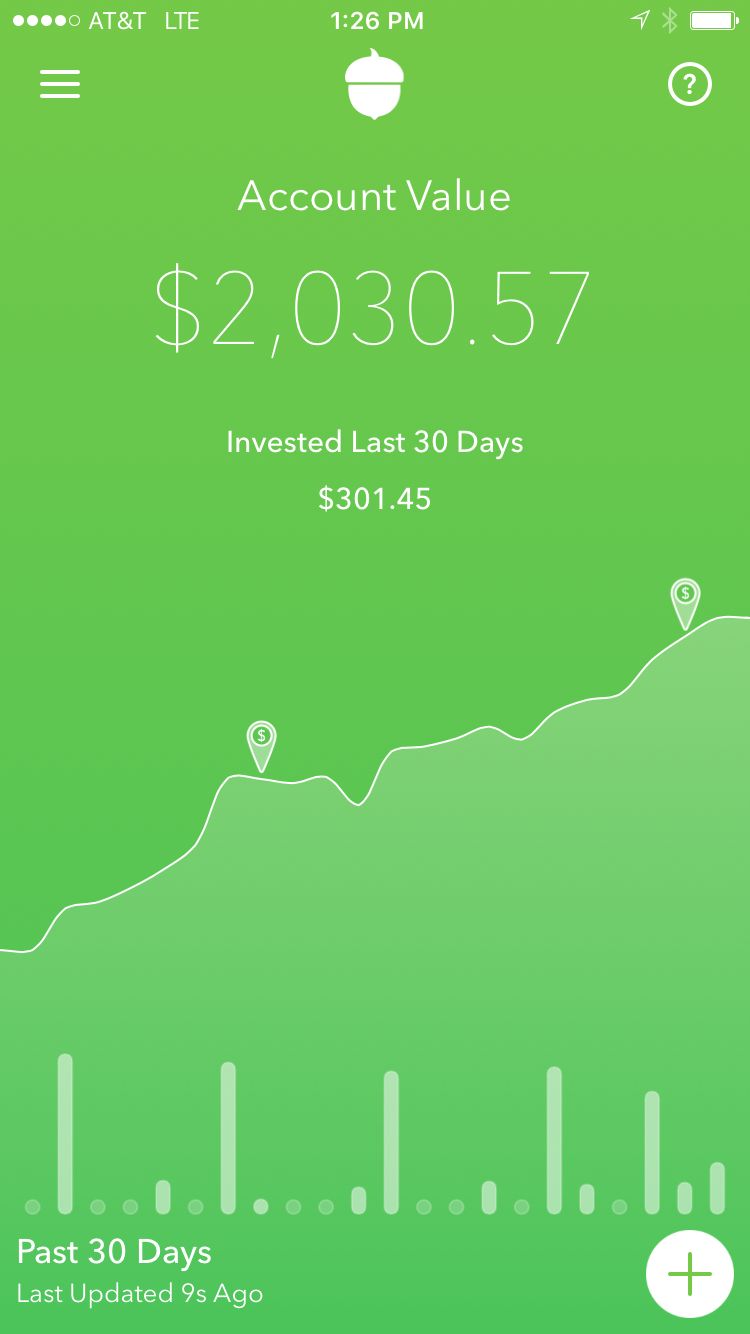

Millennials – Automatic Deductions – Acorns

People in your twenties: This one’s for you. The number one key to investment success is starting early in life, yet we often don’t for a variety of perfectly good reasons. The Acorns app addresses many of these barriers, through automatic regular deductions into a super-simple, low-cost, diversified portfolio. The app takes about five minutes and just $5 to get started. It’s mobile-friendly and has an intuitive interface. Acorns gives you a picture of your investment value now, but interestingly also shows you graphs of how your investing activity – when you stick with it month after month and year after year – will grow your account over the coming decades. I’m a big fan of anything that shows the awesome power of compound interest.

Automatic deductions from your checking account into an investment account is not just A WAY to invest. It’s really THE ONLY WAY to invest for most people of modest means. In my experience, nobody has a surplus at the end of the month unless we’ve devised a trick to whisk our money out of our account before own greedy little hands spend it. The Acorns App is the latest, best, trick to do that automatic whisking. I set up a $50/week automatic program in May 2016, just before I wrote my blog post on it. This week I have more than $2,000 in my account, and I barely noticed how it got there. This is painless investing, made super simple.

If you are 20-something and wondering how to begin investing, here’s the solution to your New Year’s Resolution. If you have a 20-something in your life, send them an Acorns invitation link.[1]

Parents – College Savings – 529 Accounts are for grandparents

Parents: This resolution is for you if you’re in my demographic. Two kids. Big college bills ahead (should they choose that path.) The more I’ve learned about 529 college savings accounts, the more I’d always recommend parents avoid them and build up tax-advantaged retirement accounts instead of 529s.

And yet, Sir Mix-A-Lot, let me add to that statement a big BUT:

And yet, Sir Mix-A-Lot, let me add to that statement a big BUT:

529 accounts make a lot of sense for grandparents who have a surplus. Grandparents who have solved their retirement needs already can use 529s to help the younger generation. Grandparent 529s do not count against financial aid calculations. Also, unlike IRAs and 401(k)s, there’s no age or income limit on making contributions. Finally, 529s are even helpful for estate planning purposes. All of these factors make 529s a better deal for grandparents than parents.

So here’s my New Year’s resolution advice to parents: You might not prioritize 529s yourself (compared to a retirement account) but work to open up an account so that you can invite YOUR parents to contribute toward their grandchild’s college fund. Do it. It’s the right way to approach 529 accounts.

Older generation – Passing on Values – Donor-Advised Funds

I am not yet part of the older generation – at least in my own mind – but opening a Donor Advised Fund (DAF) in 2017 is actually my own personal New Year’s Resolution.

The idea of a DAF is that you can make a charitable contribution this year – reaping an income tax benefit now – while parceling out charitable gifts over a longer period of time, even decades. Investments in the DAF can grow in a tax-advantaged way, while you take your own sweet time to decide who should receive your philanthropic dollars in the coming years.

If you already have an investment advisor or brokerage firm, you could ask them about the availability and terms for opening up a DAF with them. If they don’t offer DAFs or you don’t like their terms, you should know that a few of the online supermarket brokerages have account minimums as little as $5,000, and charge a reasonable 0.6 percent annual fee. The point is you don’t need $25 million to open up your own private foundation. A DAF makes tax-advantaged philanthropic-giving available to the masses.

If you already have an investment advisor or brokerage firm, you could ask them about the availability and terms for opening up a DAF with them. If they don’t offer DAFs or you don’t like their terms, you should know that a few of the online supermarket brokerages have account minimums as little as $5,000, and charge a reasonable 0.6 percent annual fee. The point is you don’t need $25 million to open up your own private foundation. A DAF makes tax-advantaged philanthropic-giving available to the masses.

But what is the real reason for a DAF, in my mind? And why is this my own New Years’ Resolution, and maybe could be yours too?

Just this: The DAF allows you to appoint trustees, who then share in the decision-making for future charitable gifts. I have in mind appointing my 6 year-old and 11 year-old as fellow trustees of my $5,000 DAF endowment. Could we three generate maybe $250 in investment income every year – a 5 percent annual return – that we then plan together to give away each year? That renewable $250 in annual giving – driven by conversations with my kids – is the real point of the DAF. What I’m really getting for my $5,000 contribution is something of immense value: a conversation-starter.

I know I can’t move the dial of any particular charity with just $250 per year, or even a one-time $5,000, but I can create a vehicle to talk about values with my kids. We can engage in a forward-looking conversation about the uses, and meaning, of wealth.

If you’re in the older generation, with an even bigger surplus, maybe that’s a useful New Years’ resolution for you too.

I wish you peace and prosperity in 2017, and welcome your input into what financial topics you would like to read about in the coming year.

A version of this post ran in the San Antonio Express News and Houston Chronicle.

See related posts:

College 529 Accounts are for Grandparents

DAFs help you create a pretty cool legacy

[1] And if you sign up using this particular link (rather than the generic one I inserted above in the main section), I get a $5 referral fee and you get a $5 starter fee, because those Acorns people are clever and give out $5 referrals to both inviter and invitee. But I’m seriously not whoring myself and my blog for the $5. This app is good.

Post read (244) times.

2 Replies to “Look Back Look Forward – New Years Resolutions”

The 529 advice is quite incorrect. 529 from grandparents will count as student income on the following year FAFSA and thus impact financial eligibility such as grant and scholarship monies. A way to avoid this is for the grandparents to fund the child’s senior year when following year FAFSA is a non-issue.

It is probably better if the grandparents’ money contribution is not from a 529. It’s hard to save on taxes AND avoid tipping the financial aid formula.