I enjoy and look forward to your advice every week. I am about to do as you (and a lot of other smart people) recommend and move our investments to several diversified equity index funds. My question: would you still suggest no index bond funds for someone in our age bracket? I am 71, and my wife is 65. We have a comfortable railroad pension and this year I started my Required Minimum Distribution (RMD.) We have modest money to transfer ($145,000) from Morgan Stanley to I was thinking Vanguard.

–Bob in San Antonio

Thanks, Bob for your question, which refers to my recent exhortation that 95% of people should have 95% of their money invested 95% of the time in diversified 100% equity index funds, and never sell.

The quick answer to your question is yes.

I still would give you the same advice, although with a few caveats. The first caveat of course is that this advice is free, and you get what you pay for!

Also, I don’t know your full situation so I’ll make base-case scenario assumptions and you can fill in the details. The key to the choice to remain 100% in equities (instead of bonds or some other fixed income) is your time horizon. Above a 5-year time horizon (my minimum for ‘investing’) then people should be in diversified equities rather than ‘safe’ bonds or savings.

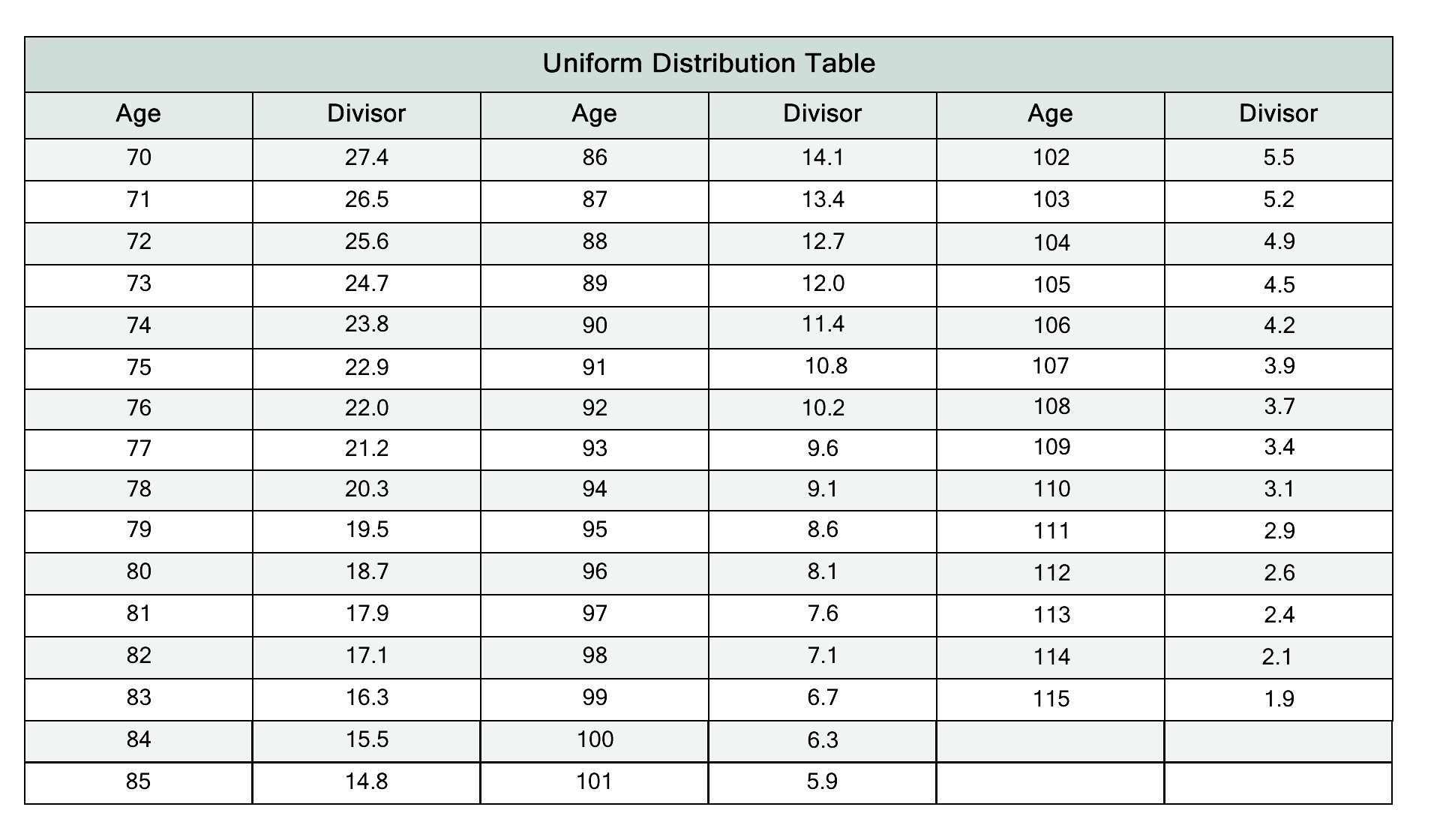

Now, you are 71 and your wife is 65, which puts your expected remaining lives (according to this Social Security actuarial table) at 13.4 and 20.2 years respectively. Given the way probabilities work, you should want to maximize your investment account for 20 years or longer, at least to support your wife (who is likely to outlive you). If you have heirs, your time horizon will be longer than even 20 years, and might really be measured in many decades.

Divide retirement assets by the divisor to calculate RMD

I’m assuming all along that you will not have to sell the funds in your account, and you won’t be spooked by market volatility, which can and will be substantial over the next 20 years. At the worst moments, sometime in the next 20 years, risky assets like stocks could lose 40% of their value from their peak, the sky will look like its falling (it won’t be), and you have to know yourself well enough to know whether you could stomach that kind of volatility without selling.

Pensions & Social Security act like a bond anyway

Another factor specific to your situation that makes 100% equities even more acceptably prudent is that your railroad pension looks and smells and acts like a bond. Meaning, it probably pays the same amount every year without any volatility, or maybe it adjust slightly upward for cost of living changes. Social Security works the same way. The fact that a huge portion of your income is fixed income and bond-like and safe and snug should make you even more comfortable with the idea that you can remain exposed to volatile equities.

Without your pension & social security – If you had only your equity portfolio to cover your expenses – you might be forced to sell some equities to cover your costs at an inopportune time, and then 100% equities would be less of a slam dunk.

Adjust for RMD?

Speaking of selling, the RMD could change your decision (and my advice) slightly.

You know you’ll have to withdraw some required minimum distribution (RMD) each year, based on the IRS rules and your expected lifespan. A reasonable case could be made that you should keep at least one year’s RMD in cash, since you know your time horizon on that amount of money is very short. Many reasonable people might advocate a few years’ RMD in cash for the same reason.

I think its just as reasonable, however, to decide instead to keep the account fully invested in 100% equities, betting that equities will outperform bonds more years than not, and that your twenty year time horizon still justifies the decision.

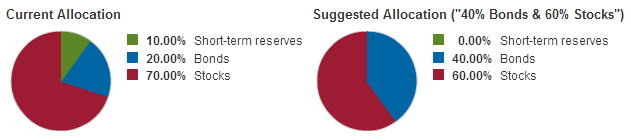

I totally disagree with this suggested asset allocation

The deciding factor between these reasonable scenarios, in my mind, is how ‘comfortable’ the ‘comfortable railroad pension’ really is. If your lifestyle costs are fully covered by the pension, and the retirement account subject to RMD rules is just extra money, then you can think of that investment account as intergenerational money. If you have heirs or a favorite philanthropy to pass money to, for example, then the time horizon for your account can be measured in decades, and you should undoubtedly stay 100% in equities. I’m confident that with a 20 year time horizon or greater, there will be more money in the end via equities than there would be if you invested in bonds.

This picture comes up when you type ‘ira investing sexy’ into Google Docs. Just FYI.

Dear Banker,

I’m ready to purchase IRAs for my husband and me. We had fun as young 20-somethings and didn’t start saving anything for retirement until our 30s, and even then, sometimes one of us was not always able to set aside money into the 401K/403b offered by employers. So, I figured an IRA would be a good option to help set aside additional funds for retirement. We already have life insurance squared away and are debt-free, apart from our mortgage, and have emergency funds set aside for miscellaneous emergencies (I’m a planner!). I’d rather be taxed now, so I know a Roth IRA would meet that requirement, but what else should I look for? I’m interested in opening the accounts with $2,000 each since I understand we won’t be held to a minimum monthly deposit towards the account that way.

Thanks for any suggestions you might have!

Jessica in San Antonio, TX

Dear Jessica,

I’ll answer some of your questions quickly, and then go back and fill in the details to the same questions below.

Should you do it?

Yes

When should you do it?

Yesterday

Roth IRA vs. Traditional IRA?

Doesn’t matter

How much should I invest?

$2,000 each for you and your spouse is great.

For 2013 and 2014 the maximum amount per person is $5,500

What to invest in?

A low-cost, diversified, equities-only, mutual fund.

With whom should I open the account?

Well, since none of the fund companies are paying me through advertising, I’m reluctant to name…Ok, fine: Vanguard.

Since you may want more details with each of these topics, I flesh out my answers below.

Sorta funny, sorta true

Should you do it?

Yes.

If you have any surplus money available for savings and investment – in your case, $4,000 this year – open your IRAs before doing almost any other savings or investment activity.

Because IRAs offer-tax advantaged investing, it’s virtually impossible to beat the returns in an IRA account when compared to any other investment account.

Why do I say that? There are several reasons, all having to do with ‘after-tax’ calculations.

Tax advantages in the year you contribute to an IRA

If your income tax rate is, for example, 25%, then you need to earn $2,500 in order to have the equivalent of $2,000 available to invest in an account.

For non-IRA investing, right off the bat, $500 goes to the IRS, and $2,000 goes in your bank.

When you invest in a traditional IRA, however, the full contribution amount can be deducted from your taxable income. The result – at a 25% tax rate – is that you have 25% more money to invest.

Another way of saying this is that you got a 25% ‘return’ on your after-tax investment just by putting money into a traditional IRA when compared to investing through a non-IRA account.

Does this matter in the long run? Yes!

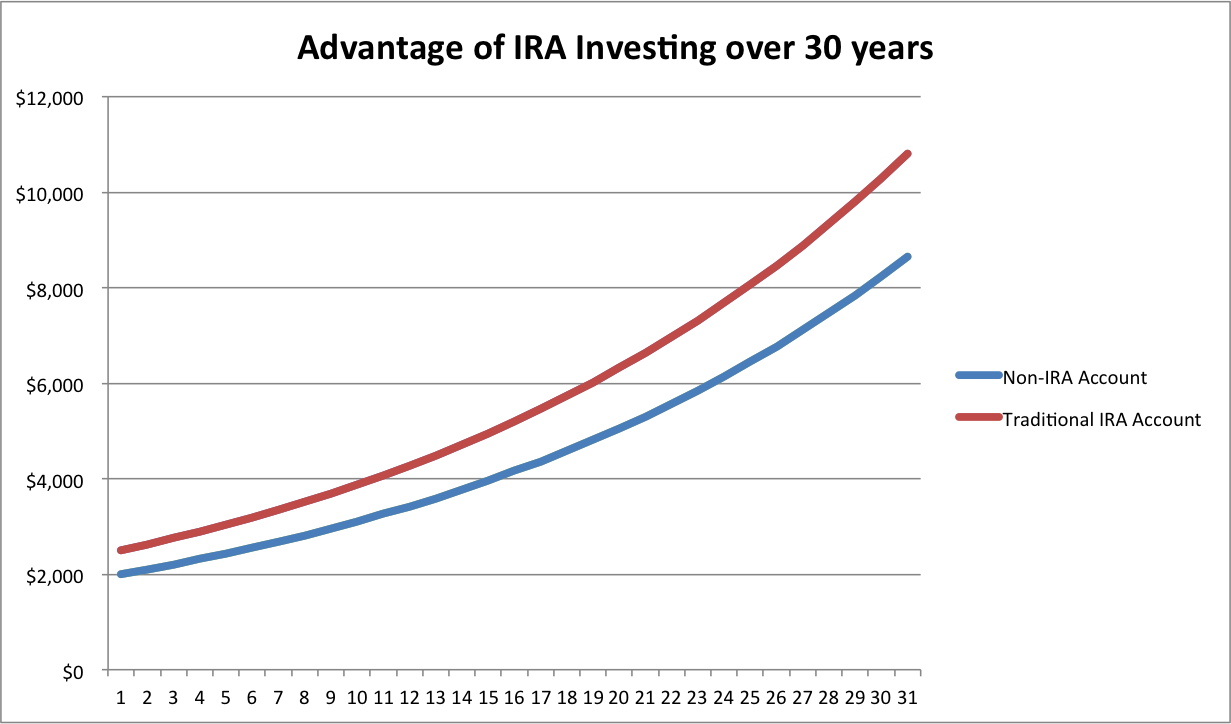

Here are some calculations, using the magical powers of compound interest math, to illustrate the long-term difference in outcomes between IRA investing and non-IRA[1] investing.

Invest $2,500 in 2013 in an IRA for 30 years and earn 5% per year. Result: $10,805.

Invest $2,000 in 2013 in a non-IRA for 30 years and earn 5% per year. Result $8,644.

$500 tax advantage grows to $2,000 in 30 years at 5% return

That’s more than a $2,000 differential in the end, an amount higher than your initial contribution amount. The greater the return assumption over the 30 years, the higher the final difference between IRA and non-IRA accounts.

If you invest this way, every year for 30 years, always choosing the $2,500 tax-advantaged IRA contribution rather than the $2,000 after-tax contribution, earning 5% per year on each contribution, you will have $174,402 rather than $139,522, a difference of $34,880.

Tax advantages of transactions inside your account

Any time you sell a stock or mutual fund position in a traditional (non-IRA) investment account you must pay taxes that year on any appreciation (or gains) in the investment. If you held the stock for less than a year you will owe your regular income tax rate of 25% on the money you made.

IRAs, like Ginsu knives: But Wait! There’s More!

Even if you held the stock for more than a year you would owe long-term capital gains, probably 15% in your case. If you receive dividends or bond payments within your investment account, those will also be taxed at high rates such as 25%. Giving back 15-25% of your investment gains when the stock went up is incredibly destructive to your future wealth-building plan.

For this reason, actively buying and selling stocks in a traditional investment account makes about as much financial sense as stabbing your money with a Ginsu Knife.[2]

If you plan to sell any investments in your account over the next 30 years, you will do yourself a huge favor if those investments remain shielded from taxation within an IRA.

This poet knows thrift like Bo knows baseball

Tax advantages of retirement income from the Roth IRA

I see from your question, Jessica, that you’re oriented toward a Roth IRA rather than a traditional IRA. If you open up a Roth instead of a traditional IRA – and I don’t blame you if you do – you do not reap the income tax benefits in the year you invested. You would instead enjoy tax-free income in your retirement years when you take the money out, which is also quite awesome.

Roth IRA or Traditional IRA? Both are great!

The most important financial comparison is not between a traditional IRA and a Roth IRA, but rather between a non-IRA and an IRA account

In your retirement years, when you sell your investments for income, a Roth IRA is more valuable than a non-IRA account because of the difference in after-tax income.

If you have a 25% income tax bracket in your retirement years, for example, your $10,000 in Roth IRA income is the equivalent of $12,500 in non-IRA income.

Ok, time to move on to the next answer to your questions.

When should you do it?

Yesterday.

I answer “yesterday” in a nod to the old investing saw “When is the best time to invest?” for which the correct answer is always “thirty years ago.”

The most important factor for racking up impressive investment returns is the passage of time. Due, as always, to the magic of compound interest.

The good news, however, is that if you open your IRA now, in your 40s, you actually can take advantage of the next thirty years. By the time you and your husband retire and need to live off your investments, you will have invested “thirty years ago.” You will enjoy Madame President Cyrus’ administration in 2043 that much more if you feel wealthy.

Madame President Cyrus in 2043, when your IRA has grown for thirty years

Kristen Bell or Jennifer Lawrence? Do not make me choose

Both the Traditional IRA and Roth IRA beat any non-IRA option available.

Confidently choosing one over the other would require you to compare today’s income tax rates to future income tax rates in your retirement, something you can guess at, but with no certainty.

Your planned $2,000 each for you and your husband is great to start. The more the merrier.

Again, a $5,500 upper limit for you if you’re under age 50. A $6,500 upper limit if you’re aged 50 or older.

The income limits for IRA contributions are maddeningly complex for such a simple investment vehicle, a point which I tried to make last year (probably unsuccessfully) through this purposefully confusing infographic. For your purposes, however, the $2,000 is a great place to start, and I agree you’ll avoid charges from most investment companies with a $2,000 minimum.

A quick aside on the subject of minimum investments:

I taught a personal finance course to college students last Spring, and one of my mandatory assignments for these 18-22 year olds was to open their own IRA. I figured that even if they only had $100, and even if that $100 went into the wrong product, the practical and pedagogical benefit of opening the account and researching the account would more than make up for the inefficiency, cost, and their lack of any actual income that required tax-deferral. My theory was perfectly sound. Just ask me.

In practice, the assignment really pissed them off. They didn’t have $100 extra (so they claimed), and they quickly discovered very limited options for their minimal investment amounts (a bank CD for example), and fees on top of that, if their balance remained below something like $1,000 or $2,000. I endured a few weeks of complaints and hissing with steely resolve until my co-teacher intervened and made the assignment optional. Probably saved my tires from being slashed.

The lesson: I’m a real pain in the ass as a teacher.

Also, IRAs don’t make sense for less than an initial $1,000 to $2,000.

What to invest in?

Jessica, I want to make your life easy. Trust me on this next one.

An entire Trillion dollar industry – known around these parts as the Financial Infotainment Industrial Complex – would like you to pay extraordinary, mostly obscured, fees for a very ordinary financial service.

The industry would also like you to believe that an entire universe of options must be sifted through, parsed professionally, opined upon, and cleverly navigated. You don’t have time for that. You don’t need that.

What you want with your 30-year time horizon until retirement is the chance to receive the returns of broad equity markets. Not beat the market, just get the market returns.

So, your goal is:

1. Pay minimal fees

2. Earn the market return

3. With a 30-year horizon, you need 100% equities. You cannot afford the low returns of anything less risky.[7]

The words you need to know are: “a low-cost (probably indexed) mutual fund covering a broad sector of either US or global equities”[8]

Keep asking for that, and only that, until you get it.

One illustration of index versus managed funds

With whom should I open the account?

Vanguard doesn’t pay me to say this (which sucks for me)[9] but they pioneered this type of investing decades ago, and so they deserve credit for doing the right thing, early on. My own retirement account is with them.

At this point, dozens of other mutual fund companies offer a similarly awesome “low-cost (probably indexed) mutual fund covering a broad sector of either US or global equities.”

If you or a friend or family member already has an account or a relationship with any of these other fine companies, by all means open up an account with that other company. I believe in signing up for the fewest number of service providers.

But do not let them talk you into anything more complex (read: expensive and unnecessary) than what I described in quotes above.

Jessica, I hope that helps, and congrats on getting going with your IRAs.

[1] By “Non-IRA” I just mean any old investment account that you might buy stocks in. A regular taxable account. Something not tax-advantaged like an IRA or 401K plan.

[2] After which, of course, the knife will remain sharp and cut easily through a ripe tomato.

[5] Don’t make me choose, I don’t want to break either of their gentle hearts.

[6] Incidentally – and not relevant to your original question – if I had plenty of disposable wealth and income and a large traditional IRA, I’d probably convert it to a Roth IRA.

[8] Global is better than US, for a variety of theoretical reasons simply explained in this book I recently reviewed, but investing in a broadly diversified US equity index is also not ‘wrong’ for your purposes.

Hi Michael,

Hi Michael,