Q: We moved away from San Antonio last summer. Our prior APR, with 11 years left on our mortgage, was 3.25 percent. The interest rate for our new house was 5.25 percent. We took out a 30-year loan with plans to refinance it into a 15-year when interest rates go down. Now I’m not sure when they will ever go down. Or, when they start to go down, how long do we wait? Our old 3.25 percent seems like a dream now. If it gets to 4 should we jump on that? Will it get to 4 in the next year?

-Jeff J, Nashville, TN

A:

You have many high-salience mortgage questions in a very short note! I’ll address each one.

One of my rules is to not forecast markets. Neither stock markets nor interest rates markets. Partly that’s because I will always be wrong and I don’t like being wrong. Partly it’s because it really bothers me when finance media people pretend they can predict the future. In reality, that specific habit of forecasting by otherwise supposedly serious finance media people should earn them a fortune-teller’s cap (with all the stars and lightning bolts) to signal their likely accuracy.

Having said all that, I still have some guideposts for you to watch for the future.

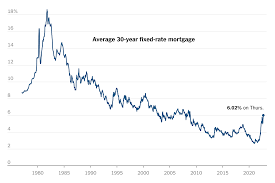

The Federal Reserve last raised the benchmark fed funds interest rate on July 26, completing its eleventh hike after more than a year of very aggressive interest rate rises. National mortgage rates changed a lot in the last 16 months as a result. While the Fed does not directly control mortgage rates, the benchmark fed funds rate plays an important anchoring role in setting 15-year and 30-year mortgage rates. All that means is that while future interest rate predictions are impossible to make, the first thing that would have to happen for mortgage rates to come down dramatically is the Federal Reserve signaling they are done raising rates. They have not yet signaled that. So you have a ways to wait still for the first guidepost.

The next guidepost would be that the Fed intends to actually lower rates. Usually that happens because a recession has begun or some other shock to the system forces the Fed to lower rates. That hasn’t happened yet either. Once the Fed signals an intention to lower rates – or actually starts to do it – then you can sharpen your pencil to pick a target for refinancing your mortgage.

Mortgage rates as of this writing (with “no points”) are above 6 percent for 15 years and above 7 percent for 30 years, making your current 5.25 percent 30 year mortgage comparatively attractive right now. You are very much not incentivized to refinance at current rates.

“How much would interest rates have to drop to make it worthwhile to refinance?” is the logical and popular follow-up question. Mortgage lenders, because they earn fees every time you refinance, would have you refinance with a 1 percent improvement in your interest rate. To answer one of your questions directly, I probably wouldn’t bother refinancing into a 4 percent mortgage rate. Reasonable people can differ on this but for myself, I probably wouldn’t do it until I could drop my interest rate by 2 percent points from my current mortgage. There are just too many fees, “points,” and closing costs to make it financially worthwhile to refinance for a minor improvement in rates.

If you have the extra monthly cash flow required, and you prefer to be in a 15-year mortgage, I’d still look for a 2 percent interest rate improvement over your existing 30-year mortgage to make that change. In your case therefore I’d personally wait until the 15-year mortgage rate hit 3.25 to do it. That’s pretty far away from here and it seems unlikely – barring an emergency crisis or recession – that interest rates will get that low next year.

One other semi-tangential thought for you to watch over the next few years, while waiting for lower interest rates.

In the olden days of the late ‘90s and early 2000s, mortgage rates were roughly around current levels and many people found it advantageous to use floating rate mortgages – known as Adjustable Rate Mortgages (ARMs).

ARMs got a bad name following the 2008 mortgage crisis, mostly because sub-prime ARMs were a particularly painful product that caused a lot of misery. ARMs would start out for 3 years or 5 years at an affordable fixed rate – 4 or 5 or 6 percent for example – but then adjust upward at the end up the time period into a much higher floating rate with 25 or 27 years remaining on the mortgage. For sub-prime borrowers, the rates adjusted upwards into usurious rates like 12 to 14 percent at the end of the fixed rate period. People lost their homes as a result.

But for prime borrowers, ARMs were not inherently terrible, just somewhat risky. I purchased homes with an ARM (twice!) without doing myself harm. I mention this not because you should necessarily refinance into an ARM, but rather to just remind you that these products exist, they are not inherently evil, and there could come a time when it would make sense to consider refinancing into an ARM.

But not yet. Not to get too technical on the shape of the interest rate curve, but ARMs are generally attractive when short-term interest rates are much lower than medium to long-term interest rates. As of this writing, short-term interest rates in the US are remarkably and unusually flat-to-inverted, meaning short term interest rates are actually higher than long term rates. This makes ARMs particularly unattractive right now. So they are definitely not a solution to your problem today.

It’s not impossible, however, that ARMs rates could become attractive before traditional 15 or 30 year mortgages do. Just something to watch out for in the next few years while you hope for improved rates for refinancing your mortgage.

With national unemployment spiking this spring at 14.7 percent and climbing – and severe hardship in certain sectors like hospitality, tourism, oil and gas, and retail – the need for mortgage relief is also high, and climbing.

Anticipating this trouble, the Coronavirus Aid, Relief and Economic Security (CARES) Act passed March 27th granted some relief for mortgage borrowers.

Three unequivocal benefits for financially stressed mortgage borrowers granted by the CARES Act are:

You likely qualify for automatic mortgage forbearance with your bank, simply by asking

The forbearance agreement with your bank will not be reported to the credit bureaus, potentially protecting your credit score and credit report, and

Residential foreclosure procedures are all temporarily frozen, at least until May 18th. Evictions are not enforceable until at least July 18th.

If you must suspend or lower your monthly mortgage payments because the COVID recession created a household financial emergency, then this relief is welcome.

Nationwide mortgage relief like this is rare, because banks really, really, like to be paid on time, every month.

The passage of time is strange right now in the COVID pandemic, right? What does “on time” even mean? For example, everyone acknowledges the month of April lasted, like, 5 years.

My man Benjamin Franklin wrote in The Way To Wealth about how time passes, depending on whether you primarily lend money or borrow money.

“Creditors have better memories than debtors; creditors are a superstitious sect, great observers of set days and times,”

Franklin wrote back in 1758.

For debtors with a mortgage, however, time passes differently, says Franklin.

“If you bear your debt in mind, the time which at first seemed so long, will, as it lessens, appear extremely short: Time will seem to have added wings to his heels as well as his shoulders. ‘Those have a short Lent, who owe money to be paid at Easter.’”

Anyway, as another mortgage payment day approaches on winged heels, forbearance options seem particularly important right now. If you have to ask for a break right now, you have to ask for a break.

The CARES Act says that if you have a home mortgage with any kind of federal backing – whether from from the Federal Housing Authority, or Veteran’s Administration, US Department of Agriculture or the mortgage insurance giants Fannie Mae or Freddie Mac – then you have the right to request forbearance on your mortgage. Very few people have a mortgage not administered in some way by these federal institutions, even if you didn’t know it already. Only a small percentage of private mortgages would not qualify for automatic forbearance under the CARES Act.

Out of curiosity, I looked up my own mortgage on the specially-created Fannie Mae and Freddie Mac websites for this purpose and found that indeed mine is covered by Freddie Mac, so I would qualify for forbearance if I chose to.

Incidentally, you may wonder why – if you only deal with your own bank and never with Fannie or Freddie – your mortgage shows up as qualifying on their websites? It’s very likely because your mortgage has been packaged up by Wall Street and sold into a mortgage bond that Fannie or Freddie guarantees.

Anyway, I found I have the right to request a fairly automatic forbearance on my mortgage, and so do you.

What would that look like? Forbearance comes in different flavors. Simply by stating financial hardship, and without having to present evidence, I could cease payments for a 180-day period. Then that could be extended by another 180 days at the end of the first period, at my request.

In addition, banks are forbidden from charging extra late fees or penalties, beyond the normal interest rate. Further, your bank is obligated by CARES – and subsequent guidance from the Consumer Financial Protection Bureau – to report a loan in forbearance as “current” to the credit bureaus, rather than delinquent for non-payment, as it normally would. So, even while not paying your mortgage for 6 months or a year, your credit would be fine.

Heck, this sounds so good, it’s a wonder anybody pays on their mortgage anymore!

Not so fast. If you have some assets and income and were wondering about entering into a forbearance agreement in order to get strategic financial relief, the CARES Act is not a great deal, according to Wendy Kowalik of financial consultancy Predico Partners.

One version of forbearance you can get is a 3 or 6 month payment suspension, followed by a lump sum payment at the end of that time period to get back on track. That probably isn’t what most people expect. And it’s totally unaffordable to most.

According to the Wells Fargo FAQ, maybe missed payments would be only due a long time from now, but it’s equally clear that that is only one possibility, among many.

Says Kowalik, “every conversation I’ve had – the assumption is that of course they are going to tack payments on to the end of the mortgage,” meaning 10 or 15 or 25 years from now, at the end of a mortgage term. “But if you have any liquidity, the likelihood is the bank will require you to pay the lump sum to get current on your mortgage right away.” That should worry most people considering a forbearance request.

Another version is a repayment plan that divides up the missed payments into a 3, 6, or 9 month repayment schedule. But that higher mortgage payment may then also become unaffordable. And prior to repayment, it will not be possible to draw further on lines of credit, or even to refinance the mortgage, without curing the forbearance.

Wendy Kowalik of Predico Partners

A key point that Kowalik worries borrowers are not considering is that the banks themselves set the terms of repayment. If your bank decides your assets or income can handle it, they will demand faster repayment. Failure to comply then could affect your credit. None of the CARES Act protections extend past a year, which means that the normal enforcement mechanisms – credit reporting, foreclosure, and eviction – are all back on the table a year from now, if not sooner.

Kowalik thinks borrowers who have a choice should be very wary of putting themselves into temporary relief that will cause even more hardship within a year. Understood that way, the CARES Act is quite bank friendly after all, in the sense that they can set the terms of repayment.

The key, says Kowalik, is this.

“Don’t go into this lightly. It looks like assistance. It looks like a simple answer to help me with my current cash flow, but that may not be the case. There is a lot of devil in the details, and I would hate for people to get surprises.”

“And about the Wells Fargo website that says ‘We want you to know we are here to help,’ Kowalik said, “Well, that just about killed me.”

I’m not the right age for reverse mortgages1 but a reader asked me for my help. Some deep-down part of me will always be a mortgage guy, so I decided to learn more about these things.2

The reader, named Jesse, aged 73, called to relay his experience trying to get a reverse mortgage on his house, and to ask for my advice.

For Jesse, his idea was to use the money he could pull out of his house to help pay for taxes and insurance in the coming years.

Although I had never paid much attention to reverse mortgages, I previously had a vaguely negative feeling about them. I’ll describe those and sure, there are reasons to be cautious.

In the course of following up on Jesse’s inquiry, I also earned a bunch of unique and kind of awesome features of reverse mortgages which I had never seen in any other loan product. My overall thought is that under the right circumstances, these could be very useful mortgages.

No Payments, Ever

The first weird thing is that a borrower can decide to never make any principal and interest payments on the loan. For life! The debt accrues interest of course but the borrower can choose to never pay on that interest or principal. The lender gets paid back eventually, when the house is either sold or the owner dies, but in the meantime the loan doesn’t require any payments. Ever. I’ve never seen that on a loan structure before.

Second, as long as the homeowner complies with the mortgage agreement – which means staying current on taxes and insurance – neither the homeowner nor the homeowner’s spouse can be evicted from the house. Ever. It’s a bank loan backed by collateral, but the bank can’t take the collateral for the life of the borrowers. This is also something I’ve never seen before.

As it turned out, Jesse couldn’t move forward with the reverse mortgage, however, because his husband Ralph is only 51, and Texas requires both spouses to be over age 62.4

Other states have more lenient spousal rules, but Texas has its own way of doing things, as you may have heard.

I’ll describe my three previous issues with reverse mortgages, as well as my evolving views.

Complexity is the Enemy of the Good

An important worry is that as a relatively unusual loan product, consumers could be more likely to make bad choices about a thing they don’t understand very well. Even a traditional home mortgage can seem complex but it resembles other products we’re familiar with, like an automobile loan or a personal loan.

A reverse mortgage, by contrast, acts a bit like a retirement account or annuity, in that you can take money out over time as you get older. It’s also a bit like a credit card or home equity line of credit, in that it “revolves,” meaning you can take money out but also pay it back as often as you like. But it’s also different than a credit card or home equity loan, because you don’t have to pay it back with regular or even any payments (until you die). One of my guiding principles of finance is simplicity. Reverse mortgages may be a complicated form of debt for some people, and complicated is the enemy of the good.

Somewhat reducing my fear, however, is that every prospective reverse mortgage borrower must take a financial counseling course by phone, mandated by the Federal Housing Authority (FHA), which regulates reverse mortgages. Guy Stidham, owner of Mortgage of Texas and Financial LLC, a San Antonio-based mortgage broker who offers both traditional and reverse mortgages, says these courses cost about $150 and take a few weeks to schedule, which serves as a kind of “cooling off” function for prospective borrowers.5

Borrowing capacity

One of the more complicated topics of a reverse mortgage is how much you can borrow. Big picture, you should know two things: First, you can generally borrow much less initially with a reverse mortgage than with a traditional mortgage. Second, the amount you can borrow against your house trends upward over time, at the same rate as your mortgage’s interest rate. Let me fill in a few details on this issue.

Your initial borrowing amount is calculated according to an FHA formula by taking into account three things: The value of your house, your interest rate, and your age.

The FHA says that the younger you are, the less you can borrow against your house. This makes sense since time will eat away at your home equity, and you are not required to make payments on a reverse mortgage. The FHA also says that the higher the interest rate, the less you can borrow. This also makes sense because a higher interest rate, compounding over time with no payments, will also eat away at your home equity.

With an online calculator you can see how much of your home value you are allowed to borrow against. If you test out the calculator, you’ll see a 70 year-old charged 4.5 percent can borrow less than 50 percent against their house. The typical range of borrowing is between 40 and 65 percent of home value, substantially less than the 80 percent standard with a traditional mortgage.

Here’s a weird quirk of reverse mortgages, however, The amount you can borrow against your house increases over time, precisely in line with the interest rate you are charged. If you’re charged 5 percent interest, your available borrowing limit increases by 5 percent per year. For reverse mortgage borrowers using this as a home equity line of credit, the annually increased borrowing capacity will seem like a cool feature. For people concerned with reverse mortgages eating up your home equity, this increased borrowing capacity may seem pernicious.

I won’t rule either way, except to say that debt in all forms is always a drug, which may be used for good or evil. The increasing borrowing limit just ups your dosage of the drug over time.

Are these high cost mortgages?

My second big worry was that reverse mortgage would be high cost products for borrowers. This fear turns out to be somewhat true, although there’s some nuance to the cost issue.

The biggest cost of a reverse mortgage is mandatory mortgage insurance. Reverse mortgage borrowers are charged by the Federal Housing Authority (FHA) 2 percent of the appraised home value. For a $500,000 appraised home, the FHA would charge $10,000, which would be rolled into your loan balance at the time of origination. The FHA also charges 0.5 percent annually on the balance, as further insurance against losses. I think this is the biggest contributor to reverse mortgage costing more than traditional mortgages.

Next, what kind of interest rate should we expect on a reverse mortgage?

Most reverse mortgages charge a variable interest rate. According to Greg Groh, a reverse mortgage originator with All Reverse Mortgage, last week the starting variable interest rate was 4.32 percent which, added to the insurance cost, would mean a borrower’s cost of 4.82 percent.

What do I think of those rates? They’re slightly higher than a traditional mortgage, but also less than the rate I’m currently charged for my home equity line of credit, on which I pay 5.49 percent, and happily so. So, the floating interest rate isn’t a big knock on reverse mortgages.

Joe DeMarkey, Strategic Business Development Leader of Reverse Mortgage Funding estimated fixed rates now between 4.375 and 5.125 percent, in the same ballpark as a traditional 30-year mortgage. So, again, the cost of a reverse mortgage isn’t particularly from an above-market interest rate.

DeMarkey points out that 80 percent of reverse mortgages have floating interest rates rather than fixed rates. With floating rate loans, the initial interest rate often starts out reasonably low but there’s always a risk that future higher interest rates make that same debt more expensive later.

Broker commissions and origination fees

Stidham allows that a broker like him can be compensated more by the lender to sell a reverse mortgage in part because they are a less competitive product. His fee for brokering a reverse mortgage could be up to 3 times higher than with a traditional mortgage.

Finally, there’s the issue of origination fees. The maximum origination fee is capped at $6,000, and would actually be smaller for smaller loans.

Closing costs like attorney fees, title insurance, and bank appraisals are all basically the same as a traditional mortgage. Groh reports that a reverse mortgage bank appraisal cost might run slightly higher, but on the order of $550 for a reverse mortgage appraisal rather than $450 for a traditional mortgage. Not a big deal there. The main big cost difference, as I said earlier, is the FHA-charged insurance, which is pretty hefty.

Servicing Details

The servicing component of reverse mortgages is slightly different than for a traditional mortgage. Since borrowers must live in their house, does that force a sale if an elderly person moves out to a nursing facility? Yes, and no.

Borrowers may live outside of the home up to 12 continuous months, meaning even an extended hospital stay or stint in a nursing home does not trigger any change with the mortgage.

Each year a lender sends an “occupancy certificate” letter to the home which must be signed and returned, according to Cliff Auerswald of All Reverse Mortgage. If the borrower does not return that certificate, then the servicer may send someone over to do a drive-by inspection of the property.

If the borrower decided to leave the home for more than 12 months, then in fact the loan would become due. For that reason, any borrower who doesn’t plan to stay in their home “for life,” should probably look for another product rather than a reverse mortgage.

Hollowing out Equity

My third big problem with reverse mortgages was that they clashed with my traditional view of the incredible wealth building potential of home ownership– a way to automatically build up a store of wealth by making affordable monthly principal and interest payments on your house over a few decades. Because reverse mortgages drain that value over time, they made me want shout “Wait…But that’s…that’s not how it’s supposed to work!”

Look, my strongest advice would be to fully pay down your home mortgage over 15 to 30 years, don’t borrow against your house, and depend solely on accumulated retirement savings plus social security to support you in your old age. There’s nothing wrong with that advice except for the fact that it sounds a bit like: “My strongest advice to you is to be rich in your old age.”

And, you know, that’s not very actionable advice by the time you actually retire.

If you can’t be rich, my second strongest recommendation would be to take out a home equity line of credit, since these are revolving lines, they allow you to flexibly borrow as needed, and act like a low-interest emergency credit card. They are awesome and we used one to renovate our kitchen and paint our house. I love my HELOC. A reverse mortgage therefore is really a third-best option, but it seems to me a pretty fine choice under many scenarios.

As my wife reminded me recently, one of my other long-standing theories of personal finance is that kids shouldn’t inherit stuff. Since we don’t intend to bequeath our house to our girls, I shouldn’t be opposed to draining the house of our home equity once we hit our 70s or 80s. At that age, the goal shouldn’t be to continuously build up assets (For what? For whom?) but rather to spend money to make our lives better.

If we planned to stay in our house, my wife and I recently agreed we’d be open to a reverse mortgage in our 70s.

This post is a combination of a couple of columns I wrote for the newspaper, combined into one long post. ↩

A reverse mortgage, sometimes called a home equity conversion mortgage (aka HECM), is targeted to 62 year olds and up. Home equity, I should clarify, is the difference between the value of a house and the amount of debt on the house. That means a $300,000 house with a $100,000 mortgage has $200,000 in home equity. A reverse mortgage is a kind of home equity loan, specifically to borrow in old age without having to make payments, if you don’t want to. ↩

As an aside, Jesse wondered if discrimination from the bank was at play because he’s gay. I told him he should hope for that, as a class-action attorney could solve all his financial needs and he wouldn’t need the mortgage any more. Alas, Texas law says your spouse can’t be younger than 62 to take a reverse mortgage, whereas in other states your spouse can be younger than 62. It’s age discrimination, not LGBT discrimination. No big discrimination win for Jesse. ↩

Disclosure: I have done consulting projects for Stidham in the past. ↩

I love everything about banks but I realize I might hold a minority view on that one. Maybe you don’t like banks as much as I do. If so, this one’s for you.

Today is about seller-financing, which is a way to cut out banks from a traditional bank function.

Seller-financing happens when:

Traditional banks can’t or won’t lend money to facilitate the sale of something expensive. Usually, but not always, real estate.

The buyer doesn’t have enough cash to buy the thing outright and needs to make installment payments, and

The seller doesn’t mind being paid in installments, including interest, over time.

Traditional banks have their comfort zone for lending. Situations that fall outside of their comfort zone become eligible for seller-financing. Typically there’s something non-standard about the property or the buyer or the situation that makes a bank loan impossible. Or sometimes, more simply, buyer and seller don’t prefer to use a bank for some reason, so they agree to structure up a loan directly from the seller to the buyer.

I sat down for lunch recently with Bill and Alison Mencarow of Kerrville, Texas, publishers of The Paper Source newsletter, which is the single most important source of wisdom and advice on creating, buying, and selling seller-financed notes.

I’ve been an off-again, on-again subscriber to their newsletter for a dozen years now, but to my chagrin had never met them in person, despite the fact that they live just a short ride up the road from me.

I don’t necessarily recommend you get involved as a buyer, seller, or investor in seller-financed notes. Because, well, read on. But if you DO ever decide to get involved, you have to subscribe to their newsletter.

Anyway, I used to invest in this business, as a purchaser of secondary seller-financed notes, bought at less than face value. When all went well, as a buyer I would collect regular interest and principal payments. If the note payer refinanced or sold their property I would get paid off early, and I would make an even higher return than the stated interest rate on the note because of the discount at which I bought the note. It can be, and was at times, a lucrative business.

I prefer to write about finance topics for which I have some expertise. What’s an expert, you ask? I define an expert as someone who has lost money doing that financial activity. By that definition, I am a clear expert in seller financing.

What I like best about the Mencarow’s newsletter is that while they support investors in the seller-financed notes business, one of their main themes is how things can go wrong. Like, really wrong.

In my old investment days, I purchased seller-financed residential mortgages, seller-financed commercial mortgages, and seller-financed business notes. In the creation of these seller-financed notes, almost by definition, something non-standard is going on.

Maybe the buyer has weak or non-existent credit and the traditional bank turned them down for a loan. Maybe the buyer did not have a sufficient down payment for a bank loan. Maybe the property needed a ton of renovation, so could not get appraised near the selling price. Or maybe, similar to the “all-cash” theme I wrote about last week, the participants in the transaction prefer to avoid banks so that their financial activity remains “invisible” to financial authorities. Any one of these scenarios increases the risks for the person collecting installment payments over time.

I’ve also been on the other side of the transaction, offering installment credit to a buyer so that I could unload a property more quickly. I used this technique to sell a 4-unit commercial property in upstate New York that needed renovation. Two separate buyers defaulted on the notes, one after the other, and twice the property came back in my possession. In each case the property returned in worse condition than before. All the copper wiring got stripped out of the property one of those times, as it turned out my buyer had a, let’s say, familiarity with folks who knew how get a good price for scrap metal. Seller-financing to him did not lead to a happy result for me.

I’ve also had numerous experiences of people ceasing to pay on their notes. Sometimes they pay a bit late, and then a little bit later still, and then the payments just stop coming. I’ve spent more time than I care to admit writing letters, sending emails, making phone calls. Sure, I’ve hired lawyers to enforce on the notes too. Sometimes this works and sometimes you end up taking a big loss.

The Mencarow’s newsletter serves as a guide to common mistakes in buying and enforcing payments on notes, including fraud, as well as the many ways investors can get way over their head or underwater through seller-financing.

Experiencing this a few times partly explains why I appreciate banks a lot.

A version of this post ran in the San Antonio Express News and Houston Chronicle

One of the things that makes finance endlessly fascinating (to me!) is that perfectly sound logic for one situation turns out to be perfect madness in another situation.

In my best moments I appreciate the ironies and contradictions. In my worst moments I despair for people whipsawed by the seeming complexities of financial choices.

Most middle-class folks grapple with one of these important choices – a home mortgage – at least once in their life. I’m a big fan of the choice to buy a home with a mortgage but even there, a controversial battle rages.

Anti-debt

Dave Ramsey

On one side of the ring stand the anti-debt gurus like Dave Ramsey. While Ramsey really wants his followers to pay cash for their homes (which is fairly absurd), he has strong rules about what to do if you decide to borrow. For example, Ramsey says

Always make at least a 20% down payment, to avoid high interest charges and expensive private mortgage insurance.

Always get a 15-year mortgage rather than a 30-year mortgage because you will pay it off sooner, typically enjoy a lower interest rate, and you’ll pay significantly less interest over the life of the loan.

Never take on mortgage debt with a monthly payment that will command more than 25% of your take-home pay.

Always avoid adjustable rate mortgages which shift the risk of higher interest rates from the lender to you.

Never borrow additional home equity in the form of a home equity loan or line of credit.1

Ramsey – who built a real estate fortune and then went bankrupt by the age of 30 – preaches a low-debt or (preferably) no-debt financial lifestyle as a curative for people with past debt problems. He knows of what he speaks, and he has a certain strong logic for his points.

On the other hand, personally, I’ve broken each and every one of his rules. So I can’t actually advocate following his advice.

Since Edelman’s contrarian position flies in the face of conventional wisdom, I enjoy presenting his points even more.

Only make the bare minimum down payment on your house – thereby freeing up your remaining capital for investing in the market, where you can earn an annual return higher than what you pay on your mortgage debt.

Always get a 30-year mortgage rather than a 15-year mortgage, to take advantage of the tax deduction on mortgage interest.

Never pay off your mortgage early or at all, because mortgages are the best way to borrow extremely cheaply. Again, use the borrowed money to invest profitably in the market.

If the value of your house rises, consider freeing up the equity to invest, through a home equity loan or line, rather then let your net worth stay locked up and unused in the form of your house. That way, Edelman says, if the value of your house drops you’ll at least have withdrawn the money and have use of it for emergencies.

Quickly paying down and eliminating your monthly mortgage payment is not an important goal because, as a homeowner, you’ll always have to pay insurance and real estate taxes anyway. Since you can’t eliminate those obligations, why bother trying to eliminate your mortgage payment?

You get the idea. When Ramsey says “Zig” Edelman says “Zag.”

Edelman presents some compelling math for his arguments. If you accept his assumptions then you could end up wealthier in the long run.

However, Edelman does not account for the psychological difficulty of saving money. Specifically, many of us benefit from the ‘forced savings’ of paying a mortgage, and few will have the discipline to take the extra monthly cash flow as a result of a 30 year mortgage and invest it for the long run, rather than squander it on iced latte frappuccinos.

As a result, I’m pretty sure some portion of people who take Edelman’s advice to heart will end up like the proverbial broke guy having to wear a barrel for pants. It kind of all depends on your specific situation.

My choices

In my own life I’ve had both adjustable rate mortgages and fixed rate mortgages. I’ve borrowed more than the conventional 80% limit. I’ve had 15-year and 30-year loans. I’ve paid extra principal on a biweekly basis, and I’ve also borrowed heavily against my home equity line of credit. I’d like to think I had compelling logic for each decision, or at least a sober mind for understanding what I was doing.

How to decide

I think my point is that the more wholly convinced a guru is, the less certain you should be. The stronger they lean in, the less likely they are to be correct in all circumstances, for all people. Ramsey’s got a great plan, for example, for people who’ve been bankrupt in the past or who have a history of debt problems. Edelman’s approach is closer to my own experience because he’s linking some risk-taking to long-term wealth creation, which I tend to do in my own life. But where you fall on the risk spectrum is a key determinant of their relevancy to your own situation.

Big Ideas vs Little Ideas

Nate Silver’s 2012 book The Signal And The Noise presents the dichotomy of a guru or pundit’s ‘big idea’ vs. ‘small ideas.’ While punditry rewards people who have ‘big ideas’ and ‘hot takes’ on topics, the reality is that certainty and big ideas come at a cost. Predicting the future – one of Nate Silver’s specialties – is a difficult business for people with big ideas. They rarely get it right. Instead, Silver advocates adopting a nimbler approach to observing the world. When I read gurus like Ramsey and Edelman, I remind myself that their certainty is a sign of the ‘big idea’ thinking that Silver warns against, when we might be served better by smaller ideas, more responsive to changing conditions.

The more certain I am, the less likely I am to be wholly right.

Three rates for mortgage brokers under the sky…

One for the Yellen on her dark throne

In the land of FOMC where the money’s born

The mortgage bond market sets the major interest rates we experience as real estate purchasers and mortgage borrowers. Because these rates are market-driven, they change from one day to the next, even from one moment to the next.

In my Lord of The Rates narrative from an earlier post the High Elves of the Mortgage Market own the 3 Mortgage Rates of Power, setting 30yr, 15yr, and short-term adjustable-rate mortgage (ARM) rates.

In an Earlier Age, I worked with those High Elves on the Goldman mortgage bond sales desk.

“Bid $1 Billion Fannie Mae 30year 5% in June”

“100-23+”

“Done.”

“Done.”

As fast as it took to read that, a mortgage-originating bank like Wells Fargo or Bank of America would promise to deliver a billion dollars worth of a diversified bundle of 30-year home mortgages, all with the same interest rate, two months from now, to Goldman’s mortgage bond structuring department. And the buyer responded with how much over face value they’d pay

The price Goldman paid for that bundle depended on an expectation of what price end-user bond buyers would pay for mortgage bonds, two months ahead.

Using Elven magic – known as securitization – our team at Rivendell would weave the dross of three thousand or so home mortgages into shimmering golden threads of valuable bonds, desired by investors all throughout Middle Earth.

That price paid – which again, fluctuated from moment to moment with the interest rate markets – ultimately drove the rate a home-buyer could lock in today.

The Fed funds rate – The One Rate To Rule Them All – anchors the interest rates that mortgage bond investors are willing to accept. And that One Rate To Rule Them All is about to go up.

Higher Rates Coming

When the Fed dropped the Fed funds rate in surprise moves in 2001, and again in 2008, mortgage bond investors accepted lower interest rates on their mortgage bonds. That lower rate allowed mortgage borrowers to save money, either by locking in new, cheaper, mortgage loans or through refinancing their existing mortgages.

Unfortunately, for home owners and buyers, we’re going the other way now.

When the Fed resets to a higher Fed funds rate – which it will do in either June or September this year – the bond investors of Middle Earth react by demanding higher returns on their bonds.

That demand for a higher return by bond buyers means mortgage originators will require future homebuyers to lock in higher rates on their mortgages. In addition, fewer borrowers will want to refinance, since they can’t save money that way.

Of course, I’m simplifying the timing. All interest rate markets are forward-looking, meaning that the probability of higher interest rates in the near term gets ‘priced in’ to interest rates throughout the mortgage system.

What I mean is this: The High Elves of Rivendell concern themselves with the future, even before it comes to pass. Professional mortgage bond investors already know rates will go up soon, so they’ve already begun to demand higher mortgage rates ahead of the FOMC’s move.

Still, higher rates will certainly affect real estate prices in the future.

Rates effect RE prices

At the risk of stating the obvious, higher mortgage rates tend to dampen the price of real estate.

With higher mortgage borrowing costs, home-buyers (as well as commercial real-estate buyers) typically can afford to buy less real estate for their money. So prices go down, or stay down, to match the newly-limited demand.

To give a quick example: A hobbit of Bag End with a $200,000 mortgage at 4% for 30 years on his burrow could expect to pay $956 per month.

That same hobbit, asked to lock in a 5% mortgage six months later – following an interest rate hike – would need to pay $1,075 per month. The $120 extra per month might be the difference between being able to afford the monthly cost of a new burrow – or not.

Since the real estate market – residential, commercial, and raw land alike – depends on borrowed money, the demand for real estate is very sensitive to interest rate changes like this.

Of course this was a huge reason why policy-makers desperately sought to keep rates low following the 2008 Credit debacle. Low interest rates provide a huge boost to real estate demand and therefore prices.

This in turn allowed the Sackville-Bagginses, in danger of foreclosure, the chance to work out their problems, sell at less of a loss, or deleverage their burrows less desperately.

Hopefully the Sackville-Bagginses have already locked in a low mortgage rate on their burrow, because it gets harder to afford real ownership once rates go up.

When the One Rate To Rule Them All jumps this year, the mortgage and real estate markets will be among the first to feel it.