How important is homeownership to building wealth in the United States? I’d put it on a list of the top five most important things people should do.

Off the top of my head the other four are probably

Stay out of high-interest debt

Automate your savings and investments

Invest in risky, not safe, things

Invest for the long term, greater than 5 years.

As a top five action, why and how is homeownership important? And can it go wrong? Oh yes, it can go wrong. It’s been less than a decade since homeownership went terribly, horribly wrong for many, so even while I want to extol ownership, it’s worth reviewing painful lessons too.

In 2014, the last time the Federal Reserve published their Survey of Consumer Finances, reporting median homeowners’ net worth of $195 thousand compared to renters $5 thousand net worth. Homeowners have nearly 40 times as much net worth as renters.

Of course you scientists will point out that correlation does not imply causation, and also that causation goes both ways. People own a house because they have wealth, AND people have wealth because they own a house. Even so, the mechanism by which home ownership builds wealth matters.

Homeownership works to build wealth because of automation, tax advantages, and leverage.

By automation, I really mean to highlight the way in which paying a mortgage over 30 (or even better, 15) years steadily builds, month after month, year after year, your ownership in a valuable asset, and in a way that matches your monthly budget. Your monthly mortgage payment is a combination of interest and principal, and every bit of principal you pay adds a steady drip into your bucket of positive net worth. Sleep like Rip Van Winkle and then wake up 30 (or even better, 15) years later and boom! You own a valuable asset free and clear of debt.

By taxation, I really don’t want to highlight the mortgage interest tax deduction that everyone seems to know about already, and that quite frankly I’d be happy to see disappear.

Instead, the tax-reducing key to wealth building through a lifetime of home ownership is the capital gains tax exclusion of $250 thousand, or $500 thousand for a married couple. Home ownership doesn’t work like other investments. It works better. If you buy a house for $200,000, and then manage to net $450,000 when you sell it many years later, you have a $250,000 capital gain. Normally, Uncle Sam takes a cut of a wealth-gain like that, like 20 percent, or $50 thousand. But as long as certain conditions are met – you lived there 2 out of the last 5 years – then that entire $250 thousand gain is yours to keep, tax free.

In the bad old days – before 1997 – Congress only let you do this tax trick once in a lifetime. Since then, however, you can do it over and over as much as you like. Now doesn’t that make you love Congress more? Congress is WAY better than cockroaches, traffic jams, and Nickelback, even if it consistently polls worse.

By leverage, I mean that middle class people can’t normally borrow four times their money to buy a valuable asset. If you experience home inflation, that borrowing juices your return on investment in an extraordinary way.

Please forgive the oversimplified math I’ll use as an illustration of leverage: If you invest $50 thousand as a down payment and borrow $200 thousand for a home, and then the home goes up in value by 10 percent, what’s the immediate return on your investment? Hint: The answer isn’t 10%.

If you managed to sell your house with a 10% gain in value, you’d clear $75 thousand after repaying your loan. If you invest $50 thousand in a thing and net $25 thousand on that thing, you have a 50% return on investment. That’s the power of leverage.

When you combine automation, tax advantage, and leverage, you have a powerful wealth-building cocktail from home ownership.

Ready for the cold water to spoil your mojito? Home ownership as an investment can also go terribly wrong.

I was thinking of this recently because I checked a personal finance book out the library that has aged very badly, David Bach’s The Automatic Millionaire Homeowner.

Published in 2005, a few years before the 2008 Crisis, Bach’s book is a combination of good advice, like I reviewed above, and terrible advice.

Bach urges people with weak credit scores to check with their banks about alternative mortgages specifically tailored to them. Bach also describes in detail the opportunities for prospective homeowners to purchase with just 5 percent or 10 percent down, or even “no money down,” rather than seek the conventional 20 percent down-payment mortgage. Bach describes without apology the idea that your house could increase in value by 6 percent per year, every year for 30 years, turning your $200,000 starter home into something worth $1.1 million. In fact much of the book reads, in retrospect, like an excited exhortation to flip one’s way from a starter home to a millionaire mansion through risky mortgages, low money down, and price appreciation as far as the eye can see. Needless to say, that isn’t the way to do it.

I’m not saying low down payments, or buying with weak credit will always go wrong and should be forbidden. I’m just saying that, given what we experienced a few years later, we know it will lead to tears for many. And I’m not saying your house won’t appreciate, I’m just saying that a more normal annual price increase like 2 percent – in line with inflation – is a much better bet.

Good personal finance books are evergreen, and that one isn’t. If you want a good one however, may I suggest Bach’s excellently readable and important The Automatic Millionaire, in which he extols the concept of automating savings and investments, a key for most middle-class people to build wealth over a lifetime.

I had a weird thing happen to me recently that prompted thoughts on real estate investing, “eminent domain,” and BIG GUBMINT.

I (re-)learned that what you don’t know might hurt you, and also what you think you know about your constitutional rights might not be true.

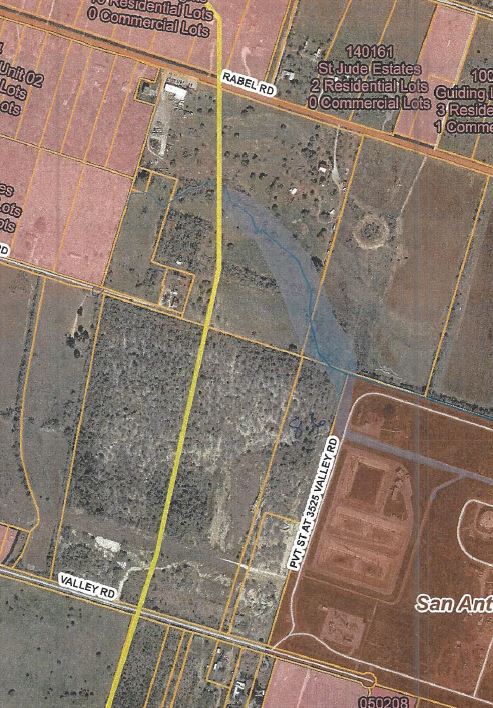

Through a series of unfortunate events, I became a one-fifth owner in a parcel of agricultural land in Southeast Bexar County, Texas.[1] I’ve been trying to sell it ever since. I have areas of investment expertise, but real estate development isn’t one of them. Which is probably why I found myself in this awkward spot.

Major Thoroughfares

Last fall I learned from our realtor that a 50-acre parcel of which I am a part-owner has a planned “Major Thoroughfare” running through the middle of it.

My realtor sent me the city parcel map and yup, there’s a bright yellow line cutting right through our property. As owners we can’t build on that. Any development done on the property has to make way for a future, theoretical, 120-foot wide road right down the middle.

A Road Runs Through It

Art Reinhardt, Assistant Director in the Transportation Department for the city of San Antonio explained to me that in 1978 – and then periodically updated afterwards – the City of San Antonio mapped out future theoretical roads, to account for growth.

The long-planned major thoroughfare is not built yet, and might not be built for decades, or even built at all, ever. But in the meantime, we can’t use that land for anything except a road.

All-in, the as yet non-existent “major thoroughfare” will take about five acres out of the parcel and make it unavailable for building. Multiply those five acres times the cost per acre, and we’re talking about real money lost by myself and my fellow owners.

At first, I thought the carved-out five acres would be no big deal. Because, well, I’m an American. And I was flipping through my copy of the US Constitution, as one does in one’s free time, and I re-read Article V of the Bill of Rights: “Nor shall any person…be deprived of life, liberty, or property, without due process of law; nor shall private property be taken for public use, without just compensation.”

This amendment is the basis for limitations on any government – city, state or federal – claiming “eminent domain” over private property, taking it for public use without paying the private property owner for that taking.

So no problem, I thought, the City of San Antonio will certainly pay us for that public use, right? I mean, I read it right there in the Fifth Amendment of the US Constitution. So, cool, I’m good.

That’s when I called city officials to test my theory.

Nope. There will be no compensation. I checked with multiple city officials familiar with this type of matter in the Planning, Transportation, and Office of Legal Counsel.

I further learned that even if an un-built but planned major thoroughfare exists, it will not show up in a title search, the typical due diligence step real estate purchasers use to be certain they have full to ownership with no liens or counter-claims from anyone, like an unpaid creditor or previous owner.

It seems the only practical way a buyer would know about this is through hiring a specialist attorney familiar with maps showing city plans for major thoroughfares. Something we clearly hadn’t done.

I talked to San Antonio attorney David Denton, a specialist in eminent domain and governmental real estate issues. He helped walk me through the legal particulars that would define an “eminent domain” case versus a “tough luck, private property owner” case.

Cities and other government entities obviously have rights and the need to restrict private usage through zoning, parcel platting, infrastructure requirements, and transportation. These may be considered ‘exactions’ imposed by a city government.

In legaleze, getting paid for eminent domain reasons hinges on whether there’s an ‘exaction’ (no compensation for the private land-owner) or a ‘taking’ (possible compensation for the private landowner.) Exactions provide government cover for a variety of legitimate uses, including it seems, future theoretical road access on this property. Denton also mentioned case law around the “proportionality” of the government’s requirements. I understand that to mean that if a higher proportion of a full property value was lost, it might start to resemble a ‘taking,’ but my situation didn’t rise to that level.

Lessons

One lesson, obviously, is don’t get into investing in things without really knowing what you’re doing. In other words, do as I say, not as I do.

Another lesson, more subtly, is that the world of real estate is not as simple as a bright line between private property rights and public or government property rights. We rarely can do precisely what we want with private land, and the public interest can impinge upon our theoretical property rights.

Please bring one of these to my rural land

The third lesson I learned along the way is that BIG GUBMINT can be serendipitously profitable. It turns out there’s private silver lining opportunity in this public impingement. As a developer buddy of mine explained, some investors seek out land like this, with a major thoroughfare plan running through it.

Here’s why. If the major thoroughfare did get built soon, I’d be sitting on a potential gold-mine (a very small-scale gold-mine, but still). Suddenly my rural land would become far more valuable from the expected increase in automobile traffic. I could lease it out to a Krispy Kreme or whatever fast food joint would build a store next to the major roadway cutting through the property.

Actually, who am I kidding? If we could lease to Krispy Kreme specifically, I would move into a trailer next door and never leave. I love that sugary goodness.

[1] I wrote once about my star-crossed real estate investment a while back, as it gave me insight into the “Agricultural Exemption” game that developers play, in which they run a cow over their land once a year at tax inspection time and the county collects only a tiny fraction of the land’s market value.

Since I like to write about finance, all of real life is merely raw material for finance lessons, so I beg your pardon while I talk about tax liens in my life.

A while back I described my astonishment at how low property taxes were for ‘agricultural exemption’ property that I happened to be eyeing for investment purposes. Long story short, I ended up buying a one-fifth interest in raw land in a rural part of the County where I live (Bexar County, TX) agricultural exemption included.

My property investment

I mention my property investment to illustrate the role of tax liens. Bear with me for a bit as I explain a sort of complicated situation.

I only bought one fifth of the property, while the other four-fifths remain owned by four siblings (not mine) who inherited the property. While the family dynamic is opaque to me (they were strangers to me before my investment), I understand that some siblings have sufficient money and some don’t, and some siblings care to pay attention to details like property taxes, and some don’t. Meanwhile, taxes on the parcel of land have gone unpaid for a few years.

This makes me extremely nervous for my investment.

Fail to pay property taxes, and you eventually run the risk of losing your property to the foreclosure power of the taxing authority, typically a city or town. Needless to say, I don’t want to lose this property, and if we leave taxes unpaid for too long, eventually Bexar County will take the land.

Tax lien lenders

Now, you may or may not have ever heard of ‘tax lien’ lenders and investors, so if not, let me be the first to illuminate for you a fascinating little section of the real estate finance world.

Ever since I registered my name on the property deed as partial owner last Spring, I have been inundated with solicitations from tax lien lenders. My name – along with the siblings – shows up publically as owners of a parcel with delinquent taxes owed. Hence, the solicitations.

The tax lien lenders offer to pay our property taxes now owed on the property. Meanwhile, if we did the deal, the lenders would use the real estate as collateral for the loan in the event I (and the sibling heirs) fail to pay back the loan in the future. Tax lien buyers (or in Texas, tax lien lenders) have the power to act like the municipality, and eventually take over the property for themselves in the event of non-payment.

In my complicated situation, with some of us owners unable to pay the taxes or possibly unwilling to put up money for the others for an indefinite amount of time, these lenders make some sense.

Partly I mention this whole anecdote because tax lien investing/lending is an obscure but important part of real estate and municipal finance.

Partly I mention this because tax lien investing may inspire a natural aversion. On the face of it, any lender who has the power to take away your property seems, I don’t know, scary? I mean, regular bankers seem unlikable enough. From a PR standpoint, however, the specific combined function of ‘tax collector’ and ‘money lender’ has an even tougher time getting a fair hearing. Those labels have served for thousands of years as biblical shorthand for enemies of the common people.

Personally, I have no problem with the solicitations to pay my taxes in exchange for an eight to twelve percent loan. We might need that solution.

The ironic thing here is that – in my old investing life – I was on the other side of this situation.

My tax-lien buying

I discovered tax lien investing in 2005 after buying a book called The 16 Percent Solution, in which the author explained a high-return and low-risk path to wealth through tax lien investing. Through my investment company I first started purchasing liens in New Jersey and New York, eventually branching out into Connecticut, Vermont, Rhode Island and even Mississippi.

Incidentally, I was a very unwelcome (meaning: Yankee) participant in my one Mississippi tax lien auction. I’m just happy to have gotten out of there in one piece. Bless your hearts, people of Wilkinson, Mississippi!

Tax lien investing and lending happens around the country, with state and local variations adding to the complexity. On the positive side, the interest rates earned seem very attractive, while the risk seems low. On the negative side – as I learned over the course of a few years of tax lien investing – it’s quite easy to lose money through tax lien investing as well.

As I purchased liens, I sometimes wondered about the complex situations that led people to become delinquent on their real estate taxes. Now I’m in one of these complex situations, and I sort of get it.

My situation

I don’t know when we will all be able to agree on paying the taxes. It may be a better idea to borrow the tax money – even if we have to pay eight to twelve percent on the loan – than to risk losing the property outright to the county via foreclosure. A loan may give us enough time to figure out an eventual solution – either by paying the taxes or selling the property.

Just add 2.3 children and a Viking stove and you’ve got the American Dream!

The “Rent v. Buy” discussion offers endless opportunities for debate.

We can talk about the opportunity to buy a piece of the mythical ‘American Dream’ – on the path to acquiring key accessories like a white picket fence, 2.3 children, and a Viking stove.

We can talk about the extraordinary risks taken by mortgage borrowers borrowing to the maximum before 2008 and the devastating financial losses many suffered in the aftermath of that financial crisis.

We can talk about the pride of fixing up one’s own dwelling as an owner. Or just as easily, we can note the smug satisfaction of calling Bob the superintendent and ordering it done. Make it quick, Bob!

Some of these preferences derive from personal leisure time preferences, risk tolerance, or lingering Leave It To Beaver fantasies. I don’t have any comment on those factors.

Are Leave It To Beaver fantasies leading you to home ownership?

I do have comments, however, on the financial implications of the Rent v. Buy debate.

Online calculators

You can find delightful Rent v Buy calculators online.

I do not recommend spending too much time with any of these online models, however, because ultimately the financial models depend on inputting assumptions about a bunch of unknowable future financial factors. Do you know what your income taxes and real estate taxes will look like five years into the future? Do you know the future rate of inflation, the rate of increase in rent, the insurance and repair costs of a home? I mean, if you had certainty and accurate insight into these things you’d be running a high frequency trading fund by now, not fiddling around with online rent v. buy calculators.

I’m in the ‘making things simple’ business, and I believe you only need to satisfy two conditions to make the move from rent to buy.

First thing: Do you have a steady, predictable income? If you do not, then home ownership is a terrible idea. It’s just too risky.

Second thing: Do you plan to stay in the same place for the next five years? If not, real estate values are too volatile to mess with, and the frictional costs of getting in and out of real estate ownership are too high – after factoring in brokerage, title, loan, and attorneys fees.

So that’s it: If you’ve got a steady income and plan to stay five years in the same place, then go for it.

Wait, I haven’t said this strongly enough.

Commodities Guy says: BUY! BUY! BUY!

Picture me for a moment like those commodity trading pits guys (who don’t really exist anymore) a phone in each ear and tie askew, hands gesticulating wildly and shouting “Buy! Buy! Buy!” into both phones simultaneously. That’s how strongly I feel about the financial advantages of home ownership, if you can satisfy my two conditions above.

In order of importance, here’s why home ownership offers powerful financial advantages.

Automatic Savings

I can’t prove this, but I’m convinced this is the most important financial reason to buy a home. Most of us have no extra money month-to-month, so the idea of putting money away for long–term investments is, let’s say, elusive. But when we own our home with a mortgage, we end up paying small chunks of principal in the ordinary course of paying for our shelter. Over 30 years many middle-class homeowners manage to sock away hundreds of thousands of dollars of wealth without much pain because it happens monthly, automatically, even sneakily.

Tax Advantages

Everybody talks about the mortgage interest tax deduction, which is fine, but not the most important tax advantage of home ownership. The most important tax advantage – by far – is that in most scenarios when you eventually sell your home, $250,000 of capital gains are tax free, or $500,000 for a married couple. No other financial asset offers that kind of tax-free growth in value. Not only that, but real estate taxes are deductible from federal income taxes, as are other mortgage expenses like ‘points.’ Home ownership is just a great big bundle of tax advantages, courtesy of your middle-class homeownership-pandering Congress. Thank you US Congress! We love you! Muah!

Inflation hedge

Hey gold bugs, you’ve got the wrong idea. Home ownership is an awesome inflation hedge, because you can reasonably expect the price of your home to go up in line with inflation. When you rent, inflation hurts. When you own, inflation helps. If you own a home, especially with a mortgage, you can be all, like, ”Inflation? Bring it on! I am hedged!”

Not an inflation hedge I endorse. But home ownership, yes!

Leverage

That’s finance-speak for buying more than you can actually afford, through borrowing. Of course being debt-free is a great idea that everyone should aspire to, but the leverage part of home ownership has long been a key part of middle-class wealth-building.

Outside of mortgages, lenders will never offer you 4-to-1 leverage, meaning the chance to buy a financial asset by only putting 20% upfront and paying off debt over time.

How does leverage work?

If you put down just 20% of the value of a thing, and then the thing goes up in value by 10%, with 4-to-1 leverage the value of your ownership in that thing increases by 50%. This is amazing! Obviously leverage (aka debt) is a double-edged sword and can lead to catastrophic losses if your thing goes down in value by 10% (or more!) But still. Leverage!

Small print disclaimer before my summary conclusion: I have not mentioned the issue of down payment (you need it!) and decent credit (you need it!) when deciding on Rent v. Buy. So there’s that to consider as well. But for now let’s focus on the simple message below.

The four factors above make ownership awesome. If you have a steady income and five years in the same place, BUY!

Three rates for mortgage brokers under the sky…

One for the Yellen on her dark throne

In the land of FOMC where the money’s born

The mortgage bond market sets the major interest rates we experience as real estate purchasers and mortgage borrowers. Because these rates are market-driven, they change from one day to the next, even from one moment to the next.

In my Lord of The Rates narrative from an earlier post the High Elves of the Mortgage Market own the 3 Mortgage Rates of Power, setting 30yr, 15yr, and short-term adjustable-rate mortgage (ARM) rates.

In an Earlier Age, I worked with those High Elves on the Goldman mortgage bond sales desk.

“Bid $1 Billion Fannie Mae 30year 5% in June”

“100-23+”

“Done.”

“Done.”

As fast as it took to read that, a mortgage-originating bank like Wells Fargo or Bank of America would promise to deliver a billion dollars worth of a diversified bundle of 30-year home mortgages, all with the same interest rate, two months from now, to Goldman’s mortgage bond structuring department. And the buyer responded with how much over face value they’d pay

The price Goldman paid for that bundle depended on an expectation of what price end-user bond buyers would pay for mortgage bonds, two months ahead.

Using Elven magic – known as securitization – our team at Rivendell would weave the dross of three thousand or so home mortgages into shimmering golden threads of valuable bonds, desired by investors all throughout Middle Earth.

That price paid – which again, fluctuated from moment to moment with the interest rate markets – ultimately drove the rate a home-buyer could lock in today.

The Fed funds rate – The One Rate To Rule Them All – anchors the interest rates that mortgage bond investors are willing to accept. And that One Rate To Rule Them All is about to go up.

Higher Rates Coming

When the Fed dropped the Fed funds rate in surprise moves in 2001, and again in 2008, mortgage bond investors accepted lower interest rates on their mortgage bonds. That lower rate allowed mortgage borrowers to save money, either by locking in new, cheaper, mortgage loans or through refinancing their existing mortgages.

Unfortunately, for home owners and buyers, we’re going the other way now.

When the Fed resets to a higher Fed funds rate – which it will do in either June or September this year – the bond investors of Middle Earth react by demanding higher returns on their bonds.

That demand for a higher return by bond buyers means mortgage originators will require future homebuyers to lock in higher rates on their mortgages. In addition, fewer borrowers will want to refinance, since they can’t save money that way.

Of course, I’m simplifying the timing. All interest rate markets are forward-looking, meaning that the probability of higher interest rates in the near term gets ‘priced in’ to interest rates throughout the mortgage system.

What I mean is this: The High Elves of Rivendell concern themselves with the future, even before it comes to pass. Professional mortgage bond investors already know rates will go up soon, so they’ve already begun to demand higher mortgage rates ahead of the FOMC’s move.

Still, higher rates will certainly affect real estate prices in the future.

Rates effect RE prices

At the risk of stating the obvious, higher mortgage rates tend to dampen the price of real estate.

With higher mortgage borrowing costs, home-buyers (as well as commercial real-estate buyers) typically can afford to buy less real estate for their money. So prices go down, or stay down, to match the newly-limited demand.

To give a quick example: A hobbit of Bag End with a $200,000 mortgage at 4% for 30 years on his burrow could expect to pay $956 per month.

That same hobbit, asked to lock in a 5% mortgage six months later – following an interest rate hike – would need to pay $1,075 per month. The $120 extra per month might be the difference between being able to afford the monthly cost of a new burrow – or not.

Since the real estate market – residential, commercial, and raw land alike – depends on borrowed money, the demand for real estate is very sensitive to interest rate changes like this.

Of course this was a huge reason why policy-makers desperately sought to keep rates low following the 2008 Credit debacle. Low interest rates provide a huge boost to real estate demand and therefore prices.

This in turn allowed the Sackville-Bagginses, in danger of foreclosure, the chance to work out their problems, sell at less of a loss, or deleverage their burrows less desperately.

Hopefully the Sackville-Bagginses have already locked in a low mortgage rate on their burrow, because it gets harder to afford real ownership once rates go up.

When the One Rate To Rule Them All jumps this year, the mortgage and real estate markets will be among the first to feel it.