In real economic terms, and as the second-largest economic power in the world since 2005, China has been a global player for a few decades.

In global financial market terms, however, China became interesting to the rest of the world for the first time this Summer.

I use the word ‘interesting’ the way it’s meant in the disguised curse ‘may you live in interesting times.’’[1] Interesting financial problems in China became the world’s problems for the first time recently, as we witnessed the first global financial market-swoon attributed to trouble in Chinese financial markets.

Economy v. financial markets

China right now represents a case study in the difference between an ‘economy’ and ‘financial markets.’

We kind of already know that these two things – ‘economy’ and ‘financial markets’ – are distinct, but linked. Also, they interact.

The 2008 Crash in the United States was an example of trouble in the financial markets crashing the real economy, as excessive losses from sub-prime structured mortgages, followed by further excessive losses from illiquid structured products among financial firms, eventually caused construction halts, unemployment, and foreclosures – in other words, real-economy misery.

Causation just as typically runs the other way, in which a decline in real-economy profits leads to a slow-down in financial volumes and asset prices.

A real economy and its financial markets each influence the other, but can – for a time at least – differ drastically.

The distinction between the real economy and financial markets matters when viewing China’s struggle this year, especially in light of financial market fragility.

The real Chinese economy

I think we in the US forget to acknowledge – or in our narrow-minded patriotic competitiveness we prefer to overlook – the economic miracle of China.

For my part, I think the wealth gains for hundreds of millions of Chinese represents the greatest miracle for humanity over the last 50 years.

Among urban Chinese, only 10 percent could be considered middle class or above as recently as 2002. Just ten years later, 70 percent of urban Chinese achieved middle class or higher economic prosperity.

No society has ever developed that fast, on such a vast scale.

I can’t think of any social change as profound as the lifting of 500 million Chinese from poverty into relative middle-class prosperity in a single generation.

Whatever you think of the Chinese system (Is it Communist? Is it Capitalist? Is it a Socialist Market Economy with Chinese Characteristics? Who cares?) The economic miracle is real and amazing and to be celebrated.

Let’s not forget that gains in the real economy of China are real, impressive, and irreversible.

The Chinese financial system

And then there’s the Chinese financial system. Between lending, stock-investing and the currency, I mistrust all of it.

On the banking and lending side, to a degree we would find ludicrous in the US, Chinese lending institutions act with governmental direction. Back in my emerging market Wall Street bond days, a pattern developed with Chinese government-sponsored lending. State-supported investment banks in many provinces, known as ITICs, would periodically go bankrupt as a result of politically-directed lending.

A history of lending for non-economic reasons

Meanwhile private business and consumers – borrowers not connected to the government – traditionally find it difficult to access any bank credit at all

On the stock-investing side in China, this year has been a roller-coaster ride for the ages. Throughout the Spring, stocks blasted ever-upward, with numerous stocks and especially new issues hitting their daily ‘limit up,’ meaning trading halted once the price rose too much in one day. Come Summer, however, that process reversed, with numerous stocks and exchanges hitting their daily ‘limit down’ as stocks went into freefall.

Now, there’s nothing inherently wrong with volatile stock markets, except maybe various group’s reactions to the volatility.

The Chinese government, apparently seeing stock market instability as an existential threat, intervened numerous times since the market’s June 12 peak.

The ‘National Team’ is expected to support household investors

You can’t accuse the Chinese government of being inactive in the face of the stock-market crash. Probably that’s wise, because…

Chinese household investors, to the extent the financial press is accurate, appear to be counting on the power of the central government to prevent a market collapse.

This idea of the central government’s capacity to bail everyone out gets referred to in China as the ‘National Team,’ as in an investor saying: “I don’t worry about the Chinese stock market going down too much because we have the “National Team” on our side.

You can probably see how that line of thinking – if enough people follow it – will end in tears someday for the individual investor, or the central government, or both.

The roughly 40 percent – or estimated $5 Trillion in market value – drop in the Shanghai Composite Index since June 2015 naturally has all sides extremely anxious.

As I mentioned in the beginning, the most interesting thing for a US-based person, is the extent to which this all matters, for the first time, to global markets.

Before this past Summer, China’s financial sneezes had never caused the world financial markets to catch a cold. Now that’s happened for the first time and there’s no going back.

[1] Interestingly, I just learned from a simple Snopes.com search this curse isn’t Chinese at all, but probably dates to a letter by an American named Frederic R. Coudert written around 1936. Coudert attributed the phrase to British politician Austen Chamberlain (brother of the infamous Prime Minister Neville “Peace in our time” Chamberlain.) Robert Kennedy popularized it during a speech in 1966.

I enjoy and look forward to your advice every week. I am about to do as you (and a lot of other smart people) recommend and move our investments to several diversified equity index funds. My question: would you still suggest no index bond funds for someone in our age bracket? I am 71, and my wife is 65. We have a comfortable railroad pension and this year I started my Required Minimum Distribution (RMD.) We have modest money to transfer ($145,000) from Morgan Stanley to I was thinking Vanguard.

–Bob in San Antonio

Thanks, Bob for your question, which refers to my recent exhortation that 95% of people should have 95% of their money invested 95% of the time in diversified 100% equity index funds, and never sell.

The quick answer to your question is yes.

I still would give you the same advice, although with a few caveats. The first caveat of course is that this advice is free, and you get what you pay for!

Also, I don’t know your full situation so I’ll make base-case scenario assumptions and you can fill in the details. The key to the choice to remain 100% in equities (instead of bonds or some other fixed income) is your time horizon. Above a 5-year time horizon (my minimum for ‘investing’) then people should be in diversified equities rather than ‘safe’ bonds or savings.

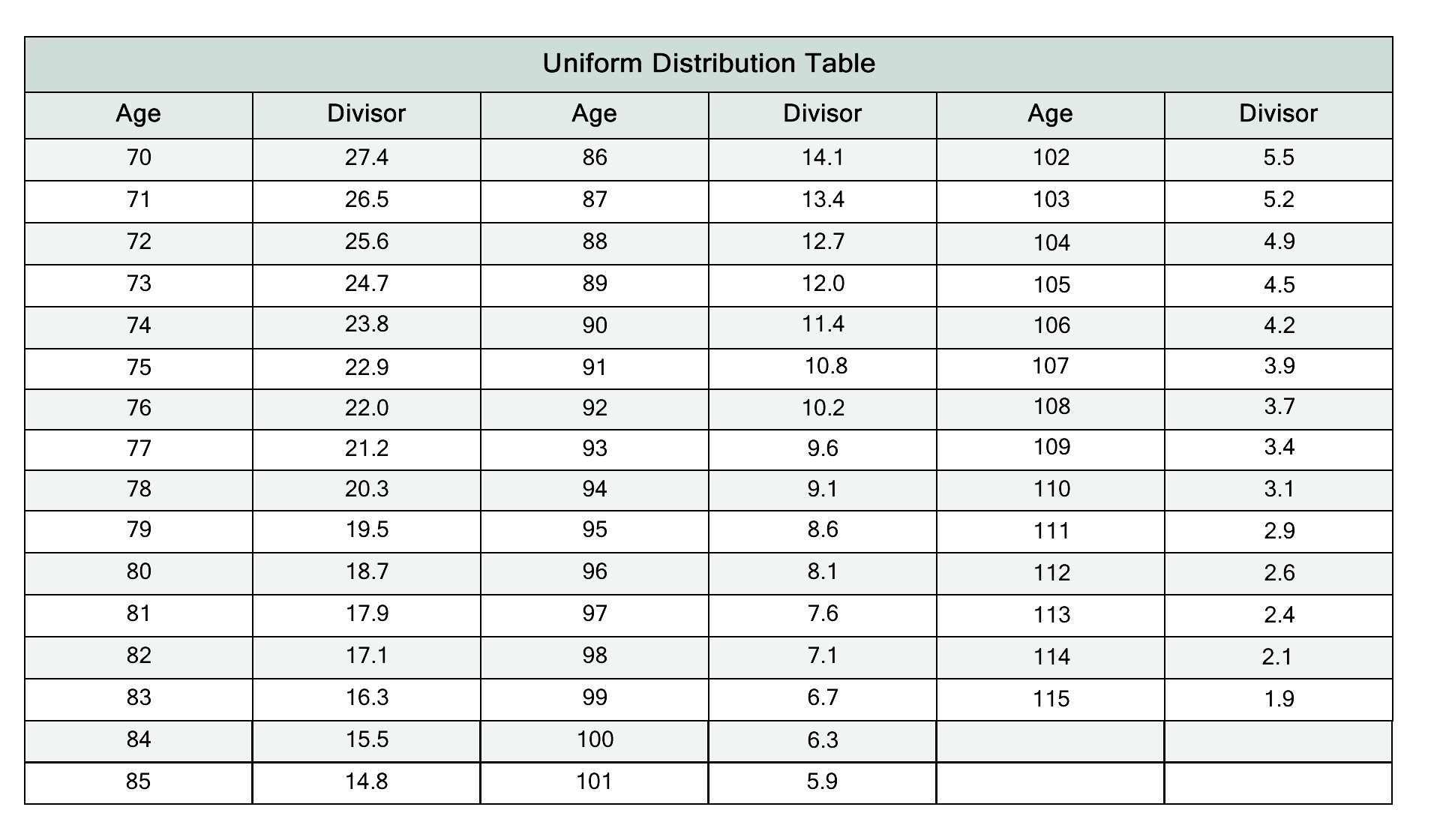

Now, you are 71 and your wife is 65, which puts your expected remaining lives (according to this Social Security actuarial table) at 13.4 and 20.2 years respectively. Given the way probabilities work, you should want to maximize your investment account for 20 years or longer, at least to support your wife (who is likely to outlive you). If you have heirs, your time horizon will be longer than even 20 years, and might really be measured in many decades.

Divide retirement assets by the divisor to calculate RMD

I’m assuming all along that you will not have to sell the funds in your account, and you won’t be spooked by market volatility, which can and will be substantial over the next 20 years. At the worst moments, sometime in the next 20 years, risky assets like stocks could lose 40% of their value from their peak, the sky will look like its falling (it won’t be), and you have to know yourself well enough to know whether you could stomach that kind of volatility without selling.

Pensions & Social Security act like a bond anyway

Another factor specific to your situation that makes 100% equities even more acceptably prudent is that your railroad pension looks and smells and acts like a bond. Meaning, it probably pays the same amount every year without any volatility, or maybe it adjust slightly upward for cost of living changes. Social Security works the same way. The fact that a huge portion of your income is fixed income and bond-like and safe and snug should make you even more comfortable with the idea that you can remain exposed to volatile equities.

Without your pension & social security – If you had only your equity portfolio to cover your expenses – you might be forced to sell some equities to cover your costs at an inopportune time, and then 100% equities would be less of a slam dunk.

Adjust for RMD?

Speaking of selling, the RMD could change your decision (and my advice) slightly.

You know you’ll have to withdraw some required minimum distribution (RMD) each year, based on the IRS rules and your expected lifespan. A reasonable case could be made that you should keep at least one year’s RMD in cash, since you know your time horizon on that amount of money is very short. Many reasonable people might advocate a few years’ RMD in cash for the same reason.

I think its just as reasonable, however, to decide instead to keep the account fully invested in 100% equities, betting that equities will outperform bonds more years than not, and that your twenty year time horizon still justifies the decision.

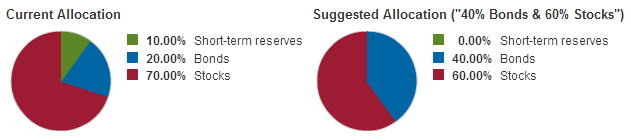

I totally disagree with this suggested asset allocation

The deciding factor between these reasonable scenarios, in my mind, is how ‘comfortable’ the ‘comfortable railroad pension’ really is. If your lifestyle costs are fully covered by the pension, and the retirement account subject to RMD rules is just extra money, then you can think of that investment account as intergenerational money. If you have heirs or a favorite philanthropy to pass money to, for example, then the time horizon for your account can be measured in decades, and you should undoubtedly stay 100% in equities. I’m confident that with a 20 year time horizon or greater, there will be more money in the end via equities than there would be if you invested in bonds.

The U.S. stock market got quite volatile last week, and I couldn’t be happier.

Let me explain why, by way of the analogy of the 2011 fire at Lost Pines State Park.

Scorched earth and equity markets

Two weeks ago, I drove with my family near Lost Pines Forest, the ground zero of a devastating forest fire in 2011 that Wikipedia tells me was the most destructive wildfire in Texas history.

I had passed through Bastrop just weeks after that fire on our way to College Station, and I remember how utterly desolate the roadside forest appeared. Just a terrible vista of charred chimneys, missing their houses. Blackened trunks perched on scarred ground.

Now, however, the ecosystem is roaring back.

Fire leads to new growth

A friend of mine who teaches biology at Trinity University in San Antonio — she studies grassland ecosystems in particular — confirms what you can observe now at Lost Pines. The incredible rate of regrowth of the Lost Pines Forest happens because of the devastating fire.

In many areas, grass and forest ecosystems depend on periodic fires to remain healthy. The fire spurs growth. No fire in the past leads to less healthy growth in the future.

Regrowth of scorched earch

The forest fire stock market analogy

Just like periodic forest fires keep ecosystems healthy for grasses, plants and trees, periodic market crashes keep stock markets healthy for you and me, as long-term investors.

I credit Morgan Housel at the finance website Motley Fool for introducing me to this idea first — that stock markets must crash periodically in order to provide a decent return for the rest of us.

We typically complain, or fret, about stock market volatility. But you know what? That’s the wrong approach. The crashes help repel other people’s money from the market, which allows us long-term investors to earn a positive return.

To be perfectly clear about what I mean with my analogy: We need markets to crash periodically in order for them to “do their job” for us, which is to provide a decent positive return on our long-term surplus capital.

This positive view of market crashes — the financial equivalent of devastating wildfires — is so counterintuitive to our way of thinking and talking about the stock market that it just may alter the way you view the peripatetic ups and downs of equity markets. I hope so. That’s the point of this post.

Now, how exactly does it work that crashes and volatility are the keys to a decent positive long-term return for you, the long-term investor?

Think for a moment what the investment world would be like if stock markets always stayed stable. Zero volatility. Zero crashes. And let’s say in that stable world that stocks initially returned an average of 6 percent per year.

The only rational thing to do, with a market that provided that kind of positive return and perfect stability, would be for everyone to empty their bank accounts and pour money into the stock market. If people felt safe, they would put all their money into the stock market.

That decision by everybody would raise the price of stocks so much that future returns on stocks would decline, to something much less attractive. Given perfect stability, the market would attract as much money as it could take until future returns would approach the returns of other stable, store-of-value vehicles, like bank accounts.

Which is to say, if stocks were completely stable, we would all buy them until they offered a roughly 0 percent future return, just like bank accounts.

But the fact that you can get burned in stocks is exactly why not everybody empties out their banks accounts to bid up the prices of stocks. This relative scarcity of stock market capital leaves space for growth, like a forest that’s been cleared by a fire.

Stocks, thankfully, are not stable. People don’t feel safe. And that’s a good thing.

Do you need your money back before five years? Don’t bother with stocks. You may get burned.

The fact that people who need their money back within five years shouldn’t go anywhere near stocks — due to volatility — is part of the reason why stocks provide longer-term investors with a return above 0 percent.

Without crashes, the stock market would attract too much money. The periodic crash is therefore not a failure of markets or a glitch in the system. On the contrary, the periodic crash — like the forest fire — is a key to the whole system working correctly.

Here’s the topsy-turvy — but nevertheless true — logic of the relationship between volatility and stock market returns: Total stability would lead to “pricing for perfection,” which in turn could be destabilizing when underlying companies and the economy failed to achieve perfection. A volatile market, by contrast, stays just unattractive enough for short-term and speculative investors to allow for predictable, positive, long-term returns for long-term investors.

Long live the forest fire! Long live the volatility!

For the next little bit I’ll use a specific made-up example, of a fictional pet insurance company[1] with ticker symbol PAWS.[2]

Let’s say PAWS shares trade at $100 per share, and I am planning to sell 1,000 3-month puts struck at $90 for $2.70. I bank $2,700 (1,000 shares x $2.70), and I give the put buyer the option to sell me 1,000 shares at $90 a piece at any time in the next 3 months. [For a definition of what a put is, I recommend starting here. and then read here.]

As a retail investor, I’m hoping the shares stay roughly where they are, and certainly above $90 per share for the next 3 months. If they drop below $90/share, I am forced to buy them at a price above the market.

Without getting into heavy math, we can see intuitively why an option on a stock would be more valuable, or cost more, for a more volatile stock. If you have a 3 month option on a stock, and the stock moves only slightly during those three months, the owner of the option will have no opportunity to profit. The more dramatically the stock moves during those three months, the more the owner of the option may profit.

Perhaps not intuitive at first glance, however, is the idea that an options trader (the pro, not you and me) cares almost exclusively about the volatility of the stock – the frequency and magnitude of price changes during the time period of his option – and not about the price direction of a stock, up or down.

An options trader trades “volatility” for a living rather than stocks, and the value of all calls and puts in an option trader’s portfolio fluctuates with the rise and fall of volatility, rather than the price of stocks.

In practice, that means that if the trader owns an option, he hopes (or can be said to have ‘bet’) that the stock becomes more volatile. Conversely, if he has sold an option, he hopes (or can be said to have ‘bet’) that the stock becomes less volatile over the time horizon of the option.

In practice the professional options trader – or “vol trader” as he or she may be known – has a portfolio which is net long or net short volatility. And just importantly, in most cases the vol trader will seek to be “flat” or neutral with respect to the underlying stock, or stock market, or whichever market he or she[3] trades.

Hedging market exposure to the stock in order to isolate volatility exposure

Do you want to go deeper down the options trading rabbit hole with me? Why not? Let’s hum a few more bars of the volatility tune to learn about what options traders actually do for a living.

When an options trader buys my 1,000 puts on PAWS struck at $90 per share he typically will want to leave his portfolio exposed to volatility, but not exposed to the underlying stock. After all, he’s a ‘Vol trader,’ with a view to the historical, present, and future value of volatility, but typically without any particular responsibility for a view on the historical, present and future price of the underlying stock. But initially, at least, he’s a little bit exposed to the price of the stock.

At the moment he begins to own my puts – with the right to sell me some 1,000 PAWS shares at $90 – he becomes ‘long’ volatility but slightly ‘short’ some notional amount of PAWS shares.

The notional ‘short’ PAWS shares needs some explanation. You see, he’s slightly short PAWS shares despite the fact that he hasn’t sold any yet.

Even though he hasn’t sold me any, there is some non-zero probability that he will end up selling me PAWS shares 3 months from now, so he has a contingent future short exposure to the stock, the contingency being that PAWS shares drop below $90 per share.

This positive probability of selling shares in the next 3 months makes the vol trader somewhat exposed to the direction of the market. And, generally speaking, a vol trader doesn’t want to be exposed to the direction of the market.

Notional market exposure and “the Delta”

Let’s assume the vol trader knows – and in fact he would know based on the measure of the historical volatility of PAWS shares – that there’s a 20% probability that PAWS stock goes below $90 in the next 3 months. That makes the options trader 20% “short” 1,000 shares of PAWS, on a probability-weighted basis.

In the options trading world this notional market exposure is known as the ‘Delta.’

The delta is used in practice to calculate how the options trader can hedge his market exposure to PAWS shares, which he doesn’t want. With a 20% short position on 1,000 shares, the right thing for the options trader to do is to purchase 200 shares of PAWS (20% of 1,000) at the market price of $100 per share.

This purchase – assuming he’s calculated the delta correctly – leaves him ‘market neutral’ with respect to the future price of PAWS but ‘long’ volatility with respect to future fluctuations – in either direction – in PAWS stock.

He’s long puts on 1,000 shares, and he’s also long enough shares to cover – on a probability-weighted basis – the expect amount of shares he may sell.

Now he’s good. And ready.

Trading the delta

The interesting part for an options trader begins as soon as he’s isolated his exposed to volatility only, so next I’ll describe good scenarios for the options trader.

Let’s assume PAWS drops the next day to $90 per share.

My fictional pet insurance company

For the next part I’m mostly going to ignore the option seller’s situation (my situation) however because – as noted earlier – no retail investor should be doing this.[4]

Our options trader, who is long the 1,000 puts and long 200 PAWS shares as a hedge, now has a great opportunity based on the market’s dramatic move downward. The delta of a $90 put with the market at $90 per share will be roughly 50%, meaning the trader is now 30% under-exposed to the underlying stock.

The delta changes, remember, because it reflects the probability-weighted exposure for an options trader to the stock market price over the remaining three months. Once the stock has dropped to $90, we can assume that there’s roughly a 50-50 chance that these puts will be exercised – meaning a 50-50 chance the trader will sell 1,000 shares to the put seller at $90, three months from now.

Our vol trader can, and should, purchase an additional 300 shares of PAWS to remain ‘market neutral’ to PAWS shares.

Once he buys 300 shares to add to his original 200 shares, he owns 500 shares total, and he owns 1,000 puts on PAWs with a Delta of 50. Once again, he’s good and ready.

He’s long volatility, but neutral to PAWS, exactly how a ‘vol’ trader should be.

The next day, PAWS rockets back upwards to a price of $100 per share.

Then what happens?

The original put seller (still me, I guess?) lets out a big sigh of relief that his puts are back ‘out of the money.’[5]

Interestingly, however, our options trader is also made happy by the quick move. He couldn’t care less that the puts he owns might expire unexercised, because he cares instead that the volatility of the stock has spiked.

Why is volatility so good for him?

The delta of the PAWS shares at $100 shifts back in this example to something close to 20%, leaving the trader ‘long’ PAWS shares by about 300 shares. The options trader, in order to shift back to ‘neutral’ on the PAWS stock, gets to sell 300 shares at $100.

This part is kind of cool, if you’re an options trader long ‘vol’ on PAWS.

In the course of two trading sessions, our options trades has bought 300 shares at $90 and sold 300 shares at $100, pocketing the riskless difference of $3,000. [300 shares x $10 price move.]

An options trader who is ‘long’ volatility will always have the happy circumstance of buying low and selling high in the course of ‘delta-hedging’ his exposure to the underlying stock.[6]

If PAWS shares go up again, to $110, his delta shrinks further and he will sell some of his original 200-share delta hedge at an even higher price. If PAWS shares drop, he will buy low at the new low share price to hedge his delta. All the while remaining ‘market neutral.’

The more the shares move over the course of the next three months the more the vol trader delta hedges profitably. Wash, Rinse, Repeat.

On the other hand if PAWS never moves over the three month period in our example, our options trader loses the money he spent on the premium.

That, in super-simplified form, is how options trading works.

The retail investor speculating in options rarely delta hedges or even understands how to calculate volatility, putting him at an extraordinary disadvantage with this type of speculating.

You can still get lucky with a leveraged long or short position, and everybody knows it is better to be lucky than good.

But again, I would only wish this type of retail speculating on my worst enemy.

[1] Here’s how I imagine pet insurance working: You pay $10/month to PAWS, and in return little Fifi gets medical costs covered up to a certain amount, plus some lump sum ($10K?) to compensate you in case Fifi goes missing or gets hit by a truck. I’m making this business up but I’m certain many dog owners would be willing to buy this type of insurance.

[2] I learned after I wrote this that there is an actual penny stock with ticker symbol PAWS and I’d recommend getting involved with that penny stock even less than I would recommend selling puts. Run away!

[3] Apologies in advance, I’m going to go all gender-specific in my pronouns for the rest of the post so I don’t have to keep adding “or she” to every clause. This is just to say that I’m sorry about this and I hope to make it up to you some day.

[4] But understand that the option seller (me in this example) begins to wet his pants because losses start quickly from here.

[5] Importantly, he has time to step away from his day-trading desk to change his pants.

[6] Of course this cuts both ways – an options trader who is ‘short’ volatility will be in the uncomfortable delta-hedging position of buying high and selling low if the underlying stock makes volatile moves over the life of the option.

Options trading begins with assumptions about future volatility based on past price volatility of the instrument

How Wall Street thinks about options trading

Non-professionals who engage in options typically do not understand the ‘currency’ in which they’re trading.

By ‘currency’, I don’t mean option-users remain unaware of their US dollars.

I mean that professional options traders use a mathematical valuation called ‘volatility’ which your average retail[1] options speculator does not even consider.

What is volatility?

Volatility – not the price of the stock or the price of the option – determines the value of an option. Volatility measures the underlying value of an option. Volatility also is how an options trader comes up with the price of an option in dollars.

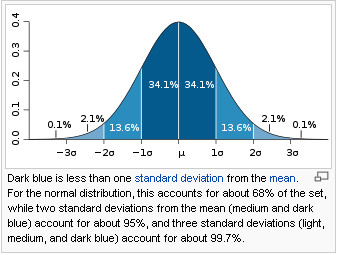

In math terms, volatility is expressed as a single number describing the frequency and magnitude of price changes over any given amount of time.

The mathematics of volatility – the single comparable number that describes the frequency and magnitude of price changes over any year – involve assuming a standard model for the distribution of prices. Some traders may use a ‘normal’ bell curve distribution of probable prices, but others can use ‘non-normal’ probability curves in sophisticated options trading.

Technically, the “annual volatility” of a stock is the standard deviation of yearly logarithmic returns on that stock.

A high ‘volatility’ number means the stock price spends significant periods of time outside of your ‘normal’ expected distribution. If the stock price lands on the outside ‘tails’ of a normal bell curve, the ‘vol’ number will be high. If the stock price trades within the high-probability tight band of a bell curve, the ‘vol’ number will be low.

If you buy or sell an option with a high ‘vol,’ the premium, or cost, of the option will be high, to reflect the expectation that the stock prices over time will land on the ‘tails’ of a normal bell curve. If you buy or sell an option with a low ‘vol,’ the premium or cost of the option will be low, reflecting its expected narrow trading band.

Did I lose you yet? That’s fine. You only need to remember one thing.

The important thing to remember is that if you don’t know how to calculate the mathematics of volatility then you have no idea what you are buying and selling when it comes to options. I’m fairly certain the author of the “sell puts!” newsletter did not explain the mathematics of ‘vol’ trading[2] to his audience.

[1] By ‘retail’ in this post I mean non-institutional investors. I mean: you and me.

[2] Come to think of it, trading options without understanding vol leaves you as blind as an individual who purchases stocks based on the ‘price’ of the stock, without modeling the underlying future cashflows of the company. Now wait, that would describe 99% of all individual stock investors. Hmmmmmm. What does that say about whether most of us should buy individual stocks? Let me think about that…

“When Issued” forward-trading of mortgage origination supply

The packaging of homeowner loans into plain vanilla mortgage bonds

The role of mortgage servicers and mortgage insurers in the bond market

This post will cover subsequent features of mortgage bond trading and structuring

The basics of mortgage trading – Prepayment risk!

The basics of CMOs – mortgage derivative structuring.

Recent market moves must have caused a bloodbath on most Wall Street mortgage desks

Contrary to popular wisdom, mortgage derivatives are not generally a risky business

Mortgage Trading – All about the prepayment risk

So how do mortgage bonds trade on Wall Street? How do investors think about the product?

Contrary to popular reports, plain-vanilla mortgage bond trading and investing remains among the safest type of investing from a ‘credit’ perspective. Investors can always expect their full principal and interest returned to them.[1]

Our simple FN 8720331 4% bond issued in October 2013 offers investors AAA-risk comparable to US Government bond risk and extreme liquidity, meaning an investor can sell the bond at any time and not pay much in transaction costs.

The main and only significant difference between our FN 4% bond and a similar US Treasury bond is the uncertainty of the timing of principal payments. Meaning, the US Treasury does not generally pay back its bond principal early, but a mortgage bond, by contrast, pays a little bit of principal, every single month. In addition, if any of the 2,000 underlying homeowners decides to sell or refinance his house, an unexpected principal repayment flows through to the bondholder.

Not if, but when

The risk to the bond-holder, therefore, is not if he’ll get paid back, but when. Since in our example 2,000 individual homeowners have the choice over when, anytime in the next 30 years, their individual mortgage gets paid back, the mortgage bond holder is subject to other people’s choices, which the investor cannot control.

The mortgage bond holder, by purchasing the bond, has implicitly sold 2,000 little 30-year options to homeowners.

In financial terms, when you sell an option you get paid a premium for that option. That premium shows up in the form of extra ‘yield,’ or investment return over comparable US Treasury bonds. This makes plain vanilla mortgage bonds ‘yield’ more than other AAA-rated bonds, but it also burdens the bond holder with ‘prepayment risk.’ Mortgage investors and mortgage traders spend all of their waking hours stressing about prepayment risk.

NSA-sized computer servers, and the greatest minds of our generation are dedicated right now, as I write this, to modeling prepayment risk in mortgage bonds. I didn’t say they were tapping the phones of those 2,000 homeowners to get a sense of when they will refinance, but I mean seriously, do you doubt it? There’s a lot of money at stake here, after all.

The problem of being a mortgage bond holder, just to dig a bit further into the prepayment problem, is that homeowners always exercise their option to refinance their home at the precisely wrong time, for bond investors. What do I mean by that?

Always on the losing end of volatile markets

I mean mortgage bond holders get paid early just when they don’t want to, and they don’t get paid back early when they would like to be paid early.

When rates drop strongly, for example, many more of our 2,000 homeowners will choose to refinance early to take advantage of the new interest rate savings. That uptick in refinancings will send early payments to the bond holder and amortize his 4% bond more quickly than expected. Unfortunately for the dedicated mortgage bond investor, however, he has to own mortgage bonds, that’s what he does for a living. So he needs to invest in new mortgage bonds to keep his money earning money. He will have to reinvest his cash at the new lower rate, which might only earn him 3%, since rates dropped strongly.

Rate hikes can be even more deadly. If mortgage rates jump to 6%, for example, many fewer of our 2,000 homeowners than usual will opt for refinancing. In fact, only people who move houses (or get foreclosed on) will pay off their mortgage early.

Few homeowners elect to refinance into higher interest rate mortgages. Hardly any prepayments flow to the bondholders to amortize the bond. Our bondholder anticipated a certain amount of prepayments and hoped to invest his proceeds at the new higher rates. He can’t. In the new 6% interest rate world, new mortgage bonds pay close to 6% but our mortgage bond investor still holds our dumb old 4% bond, with less-than-anticipated cash to put into the higher yielding bonds.[2]

The more that interest rates move, the worse off the mortgage bond holder fares, in both directions, because he’s short the prepayment option.

In times of volatile interest rate moves, the homeowner holds this very valuable option, and the bond holder suffers as a result.

Everything about mortgage trading and investing flows from this fundamental problem – the problem of prepayment risk.

Mortgage Servicing and Mortgage Derivatives – attempts to solve prepayment risk

The 2,000 individual homeowners paying their monthly mortgages underneath our theoretical $750 million Fannie 4% bond are really raw financial clay with which Wall Street artistes create financial sculptures.

If prepayment risk is the ultimate heavy burden of mortgages, the point of the financial sculpture of mortgage derivatives is to shift risk in ways to defy gravity, ultimately matching investor appetite for prepayment risk.

The mortgage servicer who separately pays interest and principal payments to bond-holders plays a key role in making these works of art possible

Simple mortgage derivatives

CMO – A Collateralized Mortgage Obligation is a generic term for relatively simple mortgage derivatives, first created 30 years ago, that typically shift prepayment risk forward or backward in time over the life of a mortgage bond.

A Wall Street bank may decide to sculpt our FNMA 4% bond into a CMO structure to split the timing of mortgage prepayments.

As a simple example, let’s assume three different investors want three different types of investments.

What a savings and loan bank wants

A traditional savings and loan bank might be looking for a place to park its cash for up to 2 years and is happy to earn a safe 2% return on its money. Our theoretical bank investor needs everything it is investing in a mortgage bond returned over the next 2 years to make its budget, and it cannot risk tying up its capital much past the next 2 years. Our savings and loan bank needs a CMO structured to receive lots of mortgage prepayments.

What an insurance company wants

An insurance company, by contrast, typically seeks long-term bond investments to match its need to meet its long-term liabilities, like life insurance payouts. The insurance company seeks a way to invest its capital for 10 years, but needs something more than a bank for that long term investment – it seeks a 4.5% return. In addition, the insurance company really does not want to receive early principal payments. The point is to keep its capital earning the 4.5% rate for as long as possible, so the insurance company really wants a CMO structured to help it avoid prepayments.

Limited pre-payment risk at attractive yields: Its what every white boy off the lake wants

Finally, a hedge fund has a flexible view of yield and the timing of return of capital, but thinks it has a better sense than the rest of the market on the true likely prepayment speed of this FNMA 4% October 2013 cohort. The hedge fund wants to earn extra yield and is willing to stomach the risk of a wider range of bond payment timing outcomes. In financial lingo we’d say the hedge fund earns the extra premium by being “short” a volatile pre-payment option. By buying the CMO with the most volatile outcome, the hedge fund has done the financial equivalent of selling many call and put options to homeowners, and it hopes to profit from this implied sale, if the interest rate environment turns out to be less volatile than expected.

Our clever Wall Street firm can assign our FNMA 4% bond to a CMO structure and instruct the mortgage servicer to follow a set algorithm as prepayments arrive over the next 30 years.

All principal payments first go to pay the bank’s CMO until that bond is completely paid off, followed by the hedge fund CMO, followed finally by the insurance company’s CMO.

For the bank’s CMO all principal payments – both the scheduled principal amortization and the unscheduled prepayments – get forwarded to this short-term bank CMO. As a result, this bond pays down extremely quickly and will likely return all capital to its holder within the 2 year time frame. There is some uncertainty about timing, but the fact that the bank CMO gets every single principal payment really limits the prepayment timing to within a nice, tight, short range.

The bank’s CMO structure also makes the next two CMOs created from the same FNMA 4% bond possible.

The hedge fund CMO only receives principal prepayments after the bank CMO has been fully paid off. As a result, the hedge fund knows it will not be subject to prepayments for some period of time in the very near future. As it is second in line for principal payments, this CMO acts kind of like a shock absorber for the other two bonds, and will be quite sensitive to changes in interest rates and therefore prepayment speeds. The investor in this type of bond, like a hedge fund, will likely believe it has a better read on prepayment risk than others in the market. Because it takes on the most prepayment risk of the three bond structures, the hedge fund will demand the most yield enhancement over comparable AAA bonds to compensate for this increased risk and uncertainty.

The insurance company’s CMO, as third in line for prepayments, has two layers of prepayment ‘protection.’ Although the timing of principal payments may ultimately differ significantly from the insurance company’s expectations, the two layers of protection cushion the prepayment risk and keep it within a tighter range than would be otherwise available from a plain-vanilla 4% FNMA bond.

By slicing up our mortgage bond pool to meet the demand of three separate investors, the Wall Street firm can, ideally, sell the entire pool at a higher implied price than would be otherwise available in a plain vanilla format. Happy customers, and higher fees, follow.

Interest only bonds and principal only bonds – another simple CMO structure

Because interest and principal payments for our $750 Million 4% FNMA bond can be easily separated by the mortgage servicer, Wall Street desks quickly figured out that some investors want interest only bonds, while others prefer to receive only principal.

Who would want an interest-only bond?

The first feature of an interest-only bond is its potentially volatile and leveraged nature – it fluctuates widely in value if you get the bet right. The second feature is that it moves in the opposite direction of most bonds due to changes in interest rates.

Most bonds go down in value as interest rates rise. But interest-only bonds created by mortgage pools will increase in value as rates rise. That’s because we expect prepayments will drop with a rise in rates, which means that you will receive interest payments on the 2,000 underlying pools for a much longer time, as fewer homeowners extinguish their mortgage through refinancing.

The price of an interest only bond will shoot upwards if interest rates unexpectedly shoot upwards and prepayment expectations drop accordingly.

If I as a mortgage investor need to hedge my mortgage portfolio against an unexpected rise in rates, I might shop for interest only bonds. If my entire portfolio is likely to lose value when rates rise, I benefit from the hedge of owning bonds that rise in value when rates rise.

Conversely, a bet on a principal only mortgage bond may be a type of bet on a decline in interest rates. Principal only mortgage derivatives will be especially sensitive to changes in rates.

Principal only mortgages trade at a discount to face value. If prepayments arrive more quickly than expected (due to, say, an unexpected increase in refinancing activity) the principal-only mortgage holder wins. Every principal payment is made at ‘par,’ causing an investment gain versus the discounted price at which the investor bought the entire principal-only mortgage derivative.

If for example I bought my principal only bond at 80 cents on the dollar, but 10% of my 2,000 underlying mortgages prepay early this month, I’ll get 10% of my investment returned to me at 100 cents on the dollar. That’s a win.

Funkier structures – More CMOs

Traditionally, mortgage structuring desks attracted some of the brainiest folks on Wall Street.[4]

With the raw material of a home mortgages, the creativity of these artistes knows few limits. Some CMOs provide precise prepayment certainty to risk-averse investors, as long as other ‘companion bonds’ serve as shock absorbers for unpredictable prepayment risk. Companion bonds will be retained by Wall Street mortgage desks comfortable with the risk, or may be bought by hedge funds with a higher risk appetite or a strong conviction about future prepayment risk.

Some CMOs offer floating interest rate structures to investors seeking to eliminate interest-rate risk exposure, while creating ever-more algorithmically complex ‘companion bonds.’

For those curious about the ever-awesomer financial sculptures the smartest minds of our generation can create, I recommend this Wikepedia page.

Recent market moves must have been ugly

Interest rates shot up more than 0.5% in May and June. For mortgage bond holders, interest-rate volatility generally hurts, and rising rates provide a double whammy to the problem.

There is no doubt this kind of movement is career-making and career-ending for Wall Street folks. Rates have been so low, for so long, that some mortgage desks will be positioned right, and many more will prove in retrospect to have been positioned wrong.

If you held a preponderance of IOs, or some extraordinary floating rate structures, or got massively short interest rates in April 2013, you’re probably ok.

For a great number of mortgage investors and traders, however, I suspect they didn’t save themselves from huge losses.

[1] Before you get smart-assed about all the scary bond losses you read about once in a Gretchen Morgenson article, let me reiterate that I said plain-vanilla mortgage bonds, not risky portions of mortgage-backed CDOs or sub-prime structured products.

[2] Adding insult to injury, if it’s an un-hedged mortgage bond position, his bond also trades significantly below par. So if he decides to sell the 4% bond to buy a 6%, he’ll take a loss. Rate hikes are hard on all bond investors, but especially mortgage bond investors.

[3] If you were born around the same time as me, it’s what you want Joel. Its what every white boy off the lake wants.

[4] Plenty of raw idiocy and barbaric types too, of course, like any testosterone-fueled environment, anywhere. For a humorous depiction of the brutal origins of the market, look no further than the original Michael Lewis classic, Liar’s Poker.

In real economic terms, and as the second-largest economic power in the world since 2005, China has been a global player for a few decades.

In real economic terms, and as the second-largest economic power in the world since 2005, China has been a global player for a few decades.