At the end of July the Trump administration quietly killed a retirement program called MyRA , intended to help lower and middle-income people begin investing for retirement.

Good riddance.

If you are of a certain political cast of mind, you might see the end of the MyRA as another hit job by Wall Street and Big Business against the little guy, just struggling to get started.

That’s not the way I see MyRA’s demise. The real reason this program stunk was the limitation that MyRA holders had to exclusively buy US government bonds, which are simply a terrible asset for retirement investing.

The Obama administration created the MyRA in 2014 to provide starter retirement accounts for workers without access to a 401(k)-style plan. The impulse behind the program, and some design elements of the MyRA, weren’t bad.

MyRA was free to both workers and business owners (yay!), encouraged automated contributions through payroll deductions (yay!), could be opened for contributions of as little as $5 per month (yay!) and simplified investing by putting all money into a special US government Thrift Savings Plan known as the G-Fund (boo!).

The G-Fund is government-guaranteed, so participants in the MyRA would never lose money, although investment returns would remain a blend of government bond interest rates, recently around 2% per year.

Anyone affected by the MyRA discontinuance will now need to roll over their funds to a Roth IRA account, although in reality very few people will be affected. Only approximately 30,000 accounts were opened since 2014, with a mere $34 million overall.

The reported $10 million a year it would cost to run it – the stated reason why the Trump Administration ended the MyRA – wasn’t that much either. The reason to end the program, in my mind, wasn’t the cost of the program or the impulse, but rather a huge design flaw – namely that all participants could only buy government debt.

If I were paranoid about the creation of the MyRA (hint: I’m not paranoid) I could connect the dots of the MyRA rules as an insidious Obama administration plot to force poor people to buy government bonds in order to finance our excessive national debt. That was a hot take among a certain type of political mind at the time of MyRA’s creation. It isn’t the real reason this program stunk.

Let me connect the dots in a different way that gets to the heart of the bad design of the MyRA. If you invest for retirement, you by definition invest for the longest run. You invest for your remaining lifetime, or even beyond. At the very least, you invest many decades into your future. As I’ve written many times before and will continue to write until my little fingers get too sore and arthritic for more writing, long-run investing needs to be dedicated to risky assets with a potential for higher returns.

Unless you are already very wealthy and are in a pure wealth-preservation mode (maybe 1 percent of you) retirement investing specifically needs to skew heavily toward higher-return assets. Riskier assets. Like stocks. (fine print: diversified, hopefully indexed, or at least low-cost, mutual funds. But I digress.) Poor people and people just starting to invest – the specific targets of the MyRA program – cannot afford to buy only US government bonds in their retirement account. Their retirement money can’t grow enough with government bonds. That design flaw just killed me. By limiting the returns that MyRA investors could obtain, the design condemned investors to a terrible retirement account that undermined the whole point of long-term compound interest growth.

Let’s do a simple compound growth comparison between a worker making a one time retirement investment for thirty years earning a US government bond return – like 2 percent per year – versus a long-term moderate stock-like growth – like 6 percent per year. That mere 4 percent difference in annual returns will result in 3.7 times more money, thirty years later, for the stock investor. It’s likely the difference between having enough and not having enough in retirement.

I think I know why the Obama administration did it, which was to prevent nominal investment losses for people just starting out. But a bad design does not justify good intentions. MyRA, by forcing its customers to purchase government bonds only, marginalized retirement investing for a group that was already marginalized.

Now that the MyRA is dead, which is fine, we’re still stuck with the policy problem that the MyRA attempted to address.

Namely, the great challenge in finance is encouraging people with limited income and financial knowledge to start savings and investment. How do people who haven’t invested before even get started?

This unsolved problem really explains the lack of uptake for President George W. Bush’s proposal to shift the responsibility for retirement savings from Social Security to individual investment accounts, later (mis-)labeled as “privatizing Social Security.”

If you leave poor or financially unsophisticated people in charge of their own personal retirement, and they fail to save enough, ripping Social Security away leaves Grandma in a cruel spot in her old age.

In the decade since that Bush-era idea ignominiously died, fin-tech companies like Qapital, Acorns, Betterment, and Wealthfront have begun to chip away at this unsolved problem, by radical simplification of the savings and investment process, and by making automated contributions easy to set up via a mobile phone app. Still, they haven’t solved the public policy problem that most people do not save enough and most people who haven’t yet saved enough don’t even know where to begin.

The MyRA was, in that sense, a noble attempt at addressing a tough problem. But limiting the investment options to government bonds – in a horrifically low interest rate environment no less – meant that it would only do a disservice to the people it purported to help.

With a little time to go before tax day, you’ve still got time to fully fund – up to $5,500 or $6,500 if you’re at least 50 years old – your Individual Retirement Account (IRA). As a certain former Governor of California used to say in the movies: Do it.

Today’s lesson is a departure from the solid, sensible, (maybe boring?) advice I’d usually give you regarding IRAs, and instead is about a do-it-yourself (DIY) version of IRAs that you should know about. But you shouldn’t necessarily “do it.”

But first, the boring, correct thing you should do with your retirement money: Set up automatic regular contributions to a low-cost (probably indexed) 100 percent stock fund at a brokerage house, and never, ever, sell. Also, be sure to do this starting at age 22. That’s how you guarantee your wealthy retirement.

While most of my retirement money is sensibly invested as described above, a portion of my retirement money is in a self-directed IRA. What does that mean? That means I like to make things difficult for myself. For some good reasons, and some bad reasons, which I’ll explain.

A self-directed IRA greatly expands the category of things you can purchase into your IRA. With a self-directed IRA, You can buy real estate, like raw land, a commercial building, or even a house. (You can’t live in a house owned by your IRA, however, that’s a clear No-no.) With a self-directed IRA you can invest directly in a hedge fund, a venture capital fund, or simply shares in a privately-held business or limited partnership. (Although you can’t own a business that also pays you a salary, that’s also a clear No-no.) You can even buy physical commodities like gold, for example. (You shouldn’t, but you can.).

The folks at the self-directed IRA service provider I use offer further examples of odd but potentially interesting ways to invest that go beyond the bread-and-butter stocks-and-bonds of a traditional brokerage or bank IRA. Some clever real estate folks, for example, by options on real estate for small sums of money, and then line up real estate buyers above their option price. This form of real estate flipping is a difficult but cool trick that could turn a very small IRA into something meaningful. I don’t really recommend you try this at home, I’m just mentioning things that some folks do in their self-directed IRA.

There’s definitely nothing ‘guaranteed’ about self-directed IRAs. In fact, it’s probably safe to say that one of the main disadvantages of a self-directed IRA is that there’s (almost) nobody to sue when things go wrong. That’s your own self-inflicted wound when you lose money.

An analogy I like to use for a self-directed IRAs is that it’s a lot like building your own car in your own garage. It will take a lot more work than the alternative. You probably need specialized knowledge. It may cost you more money than buying your basic Hyundai at the dealership. You can install some cool tricked-out features if you have particular skills. Still, most people would be better off, with most of their money, if they just went to a professional brokerage instead of building their own investment vehicle.

But if you build it yourself and then the brakes fail going down hill, well then I don’t know what to tell you except you made some bad choices. And also, like, you should have gone to GEICO.

The best reason for opening a self-directed IRA – probably – is that you really derive a lot of satisfaction from the act of investing itself. Maybe you enjoy taking risks. Maybe you have a very particular expertise in real estate or private investing or high-interest lending. Possibly you have access to unusual deal flow because of your professional background. Those are the scenarios that lend themselves best to self-directed IRA investing.

Mobile homes, Yay! (Not the actual mobile home in Arkansas)

Personally, I’ve done this now for seven years.

The service I use in Texas, Quest IRA out of Houston allows me to invest in some weird things, which I’ve found fun. My wife’s IRA, for example, receives regular monthly payments on a mobile home loan in Arkansas. Whenever a monthly payment comes in, I forward her a note saying “Yay Mobile Homes!” (True story.)

From my own IRA, I’m currently lending money to a friend here in San Antonio who needed to buy a piece of property and erect a structure for his business. It felt nice, beyond the annual interest rate I earn, to offer him an easier option than a bank for that purpose.

In my self-directed 401K, I acquired a fractional interest in an odd-ball piece of land in Bexar County that has at times enhanced my knowledge of real estate arcana and other times has frustrated the heck out of me. I plan to write about some of that arcana next week.

In investing via my self-directed IRA, I violate all sorts of investing rules that I urge on other people. Things like:

Don’t spend any more than the minimal time necessary on investing activities. Guilty as charged.

Have an expert analyze all the risks. Since I don’t know all the risks I’m taking, and since a professional money manager hasn’t looked into them for me, there are certainly more than the usual number of unknowns in these investments.

Don’t lend money to friends, as you risk losing both the money and the friend.

Don’t pay higher fees than necessary.

I know I pay higher fees for my self-directed IRA accounts than I do for my basic index stock fund at a major discount brokerage. I get charged an average of 0.15 percent management fee on assets with my basic stock index fund, or let’s say $150 per $100,000 per year. Although the self-directed accounts don’t have a management fee, I pay in the range of $1,000 per year, or let’s say 1 percent for a variety of account fees, on $100,000. In other words, this is more than six times more expensive than my basic stock index fund.

So again, this is as much about the fun of DIY than anything else. Have I convinced you not to do this yet? Heck, I’ve almost convinced myself. Just kidding, I enjoy it too much. And also, I probably need better hobbies.

Hey you, it’s April 12th. If you think the way I think (Let’s just make pretend together for a moment) you’re wondering how you’ll be able to fund your tax-advantaged individual IRA contribution for 2015 by Tax Day, Monday April 18th. Less than a week from now!

Ideally, you’re like, “Ha, ha, no problem. I have that $5,500 maximum contribution right here in my savings account that my favorite blogger Michael wants me to put in. ($6,500 if you’re over 50!)”

But I can’t target this post for the both of you readers who actually scrimped and saved the $5,500 this year. I’m writing for the real, not the ideal.

Which means you should still make your contribution this week, and let’s vow together to do better next year.

But how do we do better next year? That’s the big problem.

Regular automatic transfers

The only technique I’ve ever believed in – when it comes to actually saving money for the purposes of investing – is regular automatic transfers.

Regular automatic transfers are why 401K investing works so well, because your money gets taken out of your paycheck and then invested without you getting your greedy little hands on it.

Regular automatic transfers are often why paying off a mortgage over 30 years can reliably build up middle-class wealth. You simply get in the habit of making your house payments automatically every month, and presto! Thirty years later you have an actual positive net worth via your house.

Regular automatic transfers are why new fintech solutions like Digit, Qapital, Dyme, Acorns, and Betterment all offer to slip little tiny bits of your forgettable change out of your bank account and into a savings or investment account, to at least kick-start your investing habit, or to help you pay down debt. I don’t use any of these services, but their regular automatic transfers game is on point.

$15 a day

On short notice – between now and the end of this week for example – could I come up with $5,500 to put into my IRA? Well if you put it that way, not really.

What about maybe monthly? Do I have an extra $458 per month, after paying for the kids’ needs, and eating out, and losing money at my weekly poker game with the neighborhood dads? (That’s the $5,500 maximum allowable IRA contribution divided by 12, but you knew that.) Who’s got that kind of money? So again, not really.

To get there, how about breaking $5,500 down into the smallest possible increment? Could I save up $15 per day?

I’ve written about the fact that my caffeine addiction already leads me to waste most of that amount of money on most days. Have you ever tracked your “indefensible” expenditures? How hard would it be to save $15 per day? Maybe pretty hard, but my guess is it’s only doable via regular automated transfers.

My bank

Inspired by that thought, I logged into my bank where I have both a checking account and a savings account.

I checked my bank’s transfer set-up online, and I saw I could program it to shift money from my checking account into my savings account once a week. I didn’t see an option for daily transfers, although ideally I’d do that instead.

Money transfers from one place to the other

Would I be able to handle an automated $105 per week transfer? (That’s $15 per day, but you knew that)

Something tells me I could. Something tells me that even though transferring $5,500 in early April each year might drive me crazy, the thought of transferring $15 a day (in weekly $105 increments) might be doable. So I set it up to do just that, for the next two years. Would you like to join me in this experiment?

Irrational behavior

I’ll be the first to admit it, regular automatic transfers aren’t “rational,” in the sense that traditional economists assume we are rational people when it comes to money. Why should it matter if I’m moving money from one account to the other on a weekly basis, without affecting my overall net worth? It should not matter in the least. So this isn’t rational, but neither are we when it comes to money. We are all a little bit crazy when it comes to money.

Not for everyone

Another caveat. Regular automatic transfers out of a checking account into a savings account – or better yet, into an investment account outside the reach of your greedy little hands – won’t work for everyone. Some of us will raid that “sacred account” as soon as it accumulates a little bit of money. My only advice – if you think this will be a risk for you – is to make the destination account as difficult-to-access as possible.

Maybe try this: Write down your investment account password on a piece of paper, then rip that paper into tiny pieces. Now eat the bits of paper.

What? You don’t think that will work either? Forget it, sorry, it was just a thought. I guess we’re all irrational in different ways.

The federal government – following an idea proposed during Obama’s January 2014 State of the Union address – will role out a new simplified IRA plan later this year, designed as a starter retirement account, known by the catchy name MyRA.

Geared to lower- and middle-income earners, the accounts will have the following features:

1. Automatic deduction of contributions from payroll (that’s a good thing).

2. Same income limits, contribution limits and tax treatment as the Roth IRA – post-tax contribution, $5,500 total per year, $129,000 income per individual (that’s fine).

3. A maximum size of $15,000 total before investors need to roll it over to a private IRA (that seems arbitrary).

First, one half of all Americans have zero retirement savings.

Second, half of all full-time workers have no access to an employer-sponsored retirement plan (like a 401K or 403b), and that number climbs to 75% for part-time workers.

Third, lots of people who had retirement accounts invested in public markets lost money in the last financial crisis.

These are all admirable problems to tackle, although the existing IRA accounts are already available to anyone not covered by an employer’s plan.

Will the MyRA actually force small business owners to enroll employees?

The most interesting innovation appears to be the automatic enrollment by employers and automatic deduction of employee paychecks feature of MyRAs, although I can already hear the cries of “Nanny State” and “Government Don’t Tell Me How To Run My Small Business Or How To Save Money.”

Not one of his best ideas

I cannot tell from the White House memo how coercive the MyRA enrollment will be. Does every small business have to enroll their employees if they don’t offer a retirement account? I just can’t believe the current Congress would pass anything that resembles coercion against small businesses. So my guess is that this MyRA becomes an optional program, and this most innovative part of the MyRA program disappears.

What remains after Congress eliminates automatic enrollment, however, is a disservice to lower- and middle- income employees.

Without automatic enrollment, the MyRA seems to address the first two problems – zero savings and zero employer-sponsored retirement plans – by creating an account with tremendously similar features as the existing Roth IRA plans, but with one terrible feature.

The terrible feature

Your only option is to invest in US government debt.

The interest rate will vary over time according to prevailing interest rates, but, by design, this will be most secure dollar-denominated investment available, and therefore the lowest yielding.

The current 1 year rate offered by the “G Fund” is 1.89%. After inflation, the return on your money in a MyRA is close to zero.

Although the G Fund rate – and therefore your expected return – will go up or down with changing interest rates over time, the way the income yield on US government debt works is that it will only ever barely exceed the rate of inflation over time, almost by definition, as a result of market forces.

The fact that your income will be available upon retirement ‘tax-free’ like a Roth IRA is close to meaningless, since there will be hardly any income to enjoy, tax-free.

This is unacceptable as a product for retirement savings, and unacceptable to market as a vehicle for lower- and middle-income employees, who badly need the benefit of higher compound returns, even more than other retirees.

The memo describing the MyRA boasts that MyRA investors may rest assured that they cannot lose their principal. They can be confident that their retirement savings will not be subject to the kind of volatility that we’ve seen in recent years.

What the memo does not spell out, but that make the MyRA troubling, are the following key ideas about retirement investing:

1. Over longer time horizons – say between 5 years (70% of the time) to 15 years (95% of the time) to 20 years (99.5% of the time) – stocks win. The volatility of the stock market ceases to be a risk when compared to investing in bonds. This is because despite the volatility of stocks in the short run, stocks always offer a superior return in the long run. Retirement savings – the most long-run investing that individuals do – must skew toward higher-risk, higher-return products like stocks, and away from bonds [For more on this idea, see this post on “100% equities for the long run.”]

2. The long-run risk of investing in bonds in a retirement account is the terrible loss of purchasing power due to inflation, as well as the missed opportunity of long-term wealth accumulation from higher-risk, higher return investments.

In sum, if the MyRA only lets investors earn the “G Fund” rate of return, it’s totally unsuited for anybody’s retirement account.

An even more cynical view

Now let’s apply a paranoid Wall Street skeptic’s eye for a moment.

I do not believe the Obama administration has an evil master plan here.

They are not proposing to automatically deduct a portion of salaries from poorly paid, unsophisticated folks with no other retirement money and thereby extract the limited savings of the country’s underclass to fund the nation’s debt, at a good-for-the-government-but-bad-for-the-poor long-term interest rate. I don’t believe that comes from a Dr. Evil plot deep inside the Treasury Department.

On the other hand, that would be the actual result of this MyRA plan.

One man’s investment is another man’s debt

What is obvious to Wall Street folks but less obvious to Main Street folks is that the bonds we buy for investment are the borrowing mechanism of the companies and governments who issue bonds. My bond investment = the (company/government) bond issuer’s borrowing.

When I earn a 3% return on a Coca Cola bond over ten years, that just means Coca Cola borrowed money from me at a 3% interest rate for ten years. When you buy a municipal water company bond at 4%, that just means the municipal water company took out a loan at 4% from lenders.

When the US Government offers a 1.89% “G Fund” return to lower-income workers in a MyRA, that also means the US Government borrows money from its lower-income workers at 1.89%. Which, while not intended as such, creates an evil result.

I will offer you 1.89% on your One. Million. Dollars.

While it’s not an evil plot, it is a terrible plan.

To encourage lower-income (and presumably less-sophisticated) workers to earn a paltry 1.89% return on their longest-term investment is unconscionable retirement planning for the nation’s poorest, that just happens to, simultaneously, fund US government debt at a cheap interest rate.

Please see related posts on the IRA account investing:

This picture comes up when you type ‘ira investing sexy’ into Google Docs. Just FYI.

Dear Banker,

I’m ready to purchase IRAs for my husband and me. We had fun as young 20-somethings and didn’t start saving anything for retirement until our 30s, and even then, sometimes one of us was not always able to set aside money into the 401K/403b offered by employers. So, I figured an IRA would be a good option to help set aside additional funds for retirement. We already have life insurance squared away and are debt-free, apart from our mortgage, and have emergency funds set aside for miscellaneous emergencies (I’m a planner!). I’d rather be taxed now, so I know a Roth IRA would meet that requirement, but what else should I look for? I’m interested in opening the accounts with $2,000 each since I understand we won’t be held to a minimum monthly deposit towards the account that way.

Thanks for any suggestions you might have!

Jessica in San Antonio, TX

Dear Jessica,

I’ll answer some of your questions quickly, and then go back and fill in the details to the same questions below.

Should you do it?

Yes

When should you do it?

Yesterday

Roth IRA vs. Traditional IRA?

Doesn’t matter

How much should I invest?

$2,000 each for you and your spouse is great.

For 2013 and 2014 the maximum amount per person is $5,500

What to invest in?

A low-cost, diversified, equities-only, mutual fund.

With whom should I open the account?

Well, since none of the fund companies are paying me through advertising, I’m reluctant to name…Ok, fine: Vanguard.

Since you may want more details with each of these topics, I flesh out my answers below.

Sorta funny, sorta true

Should you do it?

Yes.

If you have any surplus money available for savings and investment – in your case, $4,000 this year – open your IRAs before doing almost any other savings or investment activity.

Because IRAs offer-tax advantaged investing, it’s virtually impossible to beat the returns in an IRA account when compared to any other investment account.

Why do I say that? There are several reasons, all having to do with ‘after-tax’ calculations.

Tax advantages in the year you contribute to an IRA

If your income tax rate is, for example, 25%, then you need to earn $2,500 in order to have the equivalent of $2,000 available to invest in an account.

For non-IRA investing, right off the bat, $500 goes to the IRS, and $2,000 goes in your bank.

When you invest in a traditional IRA, however, the full contribution amount can be deducted from your taxable income. The result – at a 25% tax rate – is that you have 25% more money to invest.

Another way of saying this is that you got a 25% ‘return’ on your after-tax investment just by putting money into a traditional IRA when compared to investing through a non-IRA account.

Does this matter in the long run? Yes!

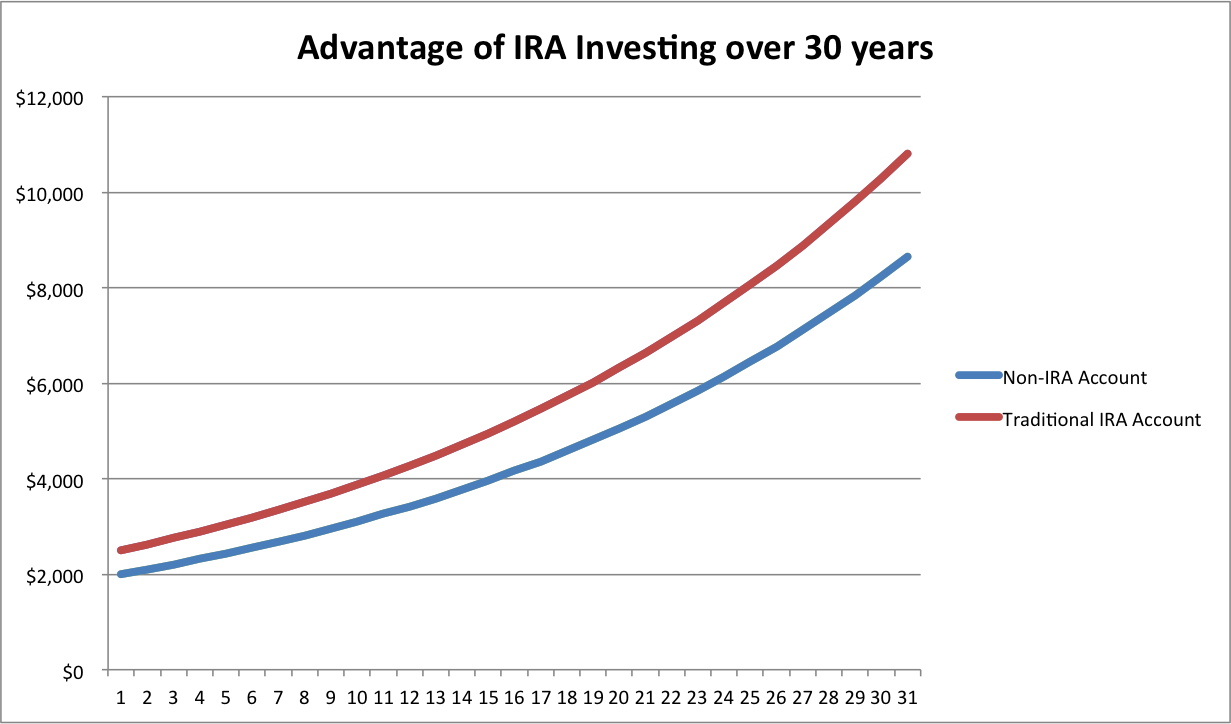

Here are some calculations, using the magical powers of compound interest math, to illustrate the long-term difference in outcomes between IRA investing and non-IRA[1] investing.

Invest $2,500 in 2013 in an IRA for 30 years and earn 5% per year. Result: $10,805.

Invest $2,000 in 2013 in a non-IRA for 30 years and earn 5% per year. Result $8,644.

$500 tax advantage grows to $2,000 in 30 years at 5% return

That’s more than a $2,000 differential in the end, an amount higher than your initial contribution amount. The greater the return assumption over the 30 years, the higher the final difference between IRA and non-IRA accounts.

If you invest this way, every year for 30 years, always choosing the $2,500 tax-advantaged IRA contribution rather than the $2,000 after-tax contribution, earning 5% per year on each contribution, you will have $174,402 rather than $139,522, a difference of $34,880.

Tax advantages of transactions inside your account

Any time you sell a stock or mutual fund position in a traditional (non-IRA) investment account you must pay taxes that year on any appreciation (or gains) in the investment. If you held the stock for less than a year you will owe your regular income tax rate of 25% on the money you made.

IRAs, like Ginsu knives: But Wait! There’s More!

Even if you held the stock for more than a year you would owe long-term capital gains, probably 15% in your case. If you receive dividends or bond payments within your investment account, those will also be taxed at high rates such as 25%. Giving back 15-25% of your investment gains when the stock went up is incredibly destructive to your future wealth-building plan.

For this reason, actively buying and selling stocks in a traditional investment account makes about as much financial sense as stabbing your money with a Ginsu Knife.[2]

If you plan to sell any investments in your account over the next 30 years, you will do yourself a huge favor if those investments remain shielded from taxation within an IRA.

This poet knows thrift like Bo knows baseball

Tax advantages of retirement income from the Roth IRA

I see from your question, Jessica, that you’re oriented toward a Roth IRA rather than a traditional IRA. If you open up a Roth instead of a traditional IRA – and I don’t blame you if you do – you do not reap the income tax benefits in the year you invested. You would instead enjoy tax-free income in your retirement years when you take the money out, which is also quite awesome.

Roth IRA or Traditional IRA? Both are great!

The most important financial comparison is not between a traditional IRA and a Roth IRA, but rather between a non-IRA and an IRA account

In your retirement years, when you sell your investments for income, a Roth IRA is more valuable than a non-IRA account because of the difference in after-tax income.

If you have a 25% income tax bracket in your retirement years, for example, your $10,000 in Roth IRA income is the equivalent of $12,500 in non-IRA income.

Ok, time to move on to the next answer to your questions.

When should you do it?

Yesterday.

I answer “yesterday” in a nod to the old investing saw “When is the best time to invest?” for which the correct answer is always “thirty years ago.”

The most important factor for racking up impressive investment returns is the passage of time. Due, as always, to the magic of compound interest.

The good news, however, is that if you open your IRA now, in your 40s, you actually can take advantage of the next thirty years. By the time you and your husband retire and need to live off your investments, you will have invested “thirty years ago.” You will enjoy Madame President Cyrus’ administration in 2043 that much more if you feel wealthy.

Madame President Cyrus in 2043, when your IRA has grown for thirty years

Kristen Bell or Jennifer Lawrence? Do not make me choose

Both the Traditional IRA and Roth IRA beat any non-IRA option available.

Confidently choosing one over the other would require you to compare today’s income tax rates to future income tax rates in your retirement, something you can guess at, but with no certainty.

Your planned $2,000 each for you and your husband is great to start. The more the merrier.

Again, a $5,500 upper limit for you if you’re under age 50. A $6,500 upper limit if you’re aged 50 or older.

The income limits for IRA contributions are maddeningly complex for such a simple investment vehicle, a point which I tried to make last year (probably unsuccessfully) through this purposefully confusing infographic. For your purposes, however, the $2,000 is a great place to start, and I agree you’ll avoid charges from most investment companies with a $2,000 minimum.

A quick aside on the subject of minimum investments:

I taught a personal finance course to college students last Spring, and one of my mandatory assignments for these 18-22 year olds was to open their own IRA. I figured that even if they only had $100, and even if that $100 went into the wrong product, the practical and pedagogical benefit of opening the account and researching the account would more than make up for the inefficiency, cost, and their lack of any actual income that required tax-deferral. My theory was perfectly sound. Just ask me.

In practice, the assignment really pissed them off. They didn’t have $100 extra (so they claimed), and they quickly discovered very limited options for their minimal investment amounts (a bank CD for example), and fees on top of that, if their balance remained below something like $1,000 or $2,000. I endured a few weeks of complaints and hissing with steely resolve until my co-teacher intervened and made the assignment optional. Probably saved my tires from being slashed.

The lesson: I’m a real pain in the ass as a teacher.

Also, IRAs don’t make sense for less than an initial $1,000 to $2,000.

What to invest in?

Jessica, I want to make your life easy. Trust me on this next one.

An entire Trillion dollar industry – known around these parts as the Financial Infotainment Industrial Complex – would like you to pay extraordinary, mostly obscured, fees for a very ordinary financial service.

The industry would also like you to believe that an entire universe of options must be sifted through, parsed professionally, opined upon, and cleverly navigated. You don’t have time for that. You don’t need that.

What you want with your 30-year time horizon until retirement is the chance to receive the returns of broad equity markets. Not beat the market, just get the market returns.

So, your goal is:

1. Pay minimal fees

2. Earn the market return

3. With a 30-year horizon, you need 100% equities. You cannot afford the low returns of anything less risky.[7]

The words you need to know are: “a low-cost (probably indexed) mutual fund covering a broad sector of either US or global equities”[8]

Keep asking for that, and only that, until you get it.

One illustration of index versus managed funds

With whom should I open the account?

Vanguard doesn’t pay me to say this (which sucks for me)[9] but they pioneered this type of investing decades ago, and so they deserve credit for doing the right thing, early on. My own retirement account is with them.

At this point, dozens of other mutual fund companies offer a similarly awesome “low-cost (probably indexed) mutual fund covering a broad sector of either US or global equities.”

If you or a friend or family member already has an account or a relationship with any of these other fine companies, by all means open up an account with that other company. I believe in signing up for the fewest number of service providers.

But do not let them talk you into anything more complex (read: expensive and unnecessary) than what I described in quotes above.

Jessica, I hope that helps, and congrats on getting going with your IRAs.

[1] By “Non-IRA” I just mean any old investment account that you might buy stocks in. A regular taxable account. Something not tax-advantaged like an IRA or 401K plan.

[2] After which, of course, the knife will remain sharp and cut easily through a ripe tomato.

[5] Don’t make me choose, I don’t want to break either of their gentle hearts.

[6] Incidentally – and not relevant to your original question – if I had plenty of disposable wealth and income and a large traditional IRA, I’d probably convert it to a Roth IRA.

[8] Global is better than US, for a variety of theoretical reasons simply explained in this book I recently reviewed, but investing in a broadly diversified US equity index is also not ‘wrong’ for your purposes.

Karen Blumenthal’s column in The Wall Street Journal over the weekend featured two of my favorite topics, self-directed IRAs and entrepreneurship, in a combined article.The details in the article, as well as the details of using a self-directed IRA to fund a small company, are complex.

·You can’t lend money personally to the firm

·You can’t guarantee a loan to the firm

·You can’t ‘self-deal,’ which might prohibit taking a salary from the company

But, the article goes on to describe, you may be able to fund, or buy early shares in, a start-up company.While of course by definition this involves extraordinary risk, it’s also the kind of thing which could in rare cases lead to a Mitt Romney-sized IRA.

Only a few investments in IRAs are outright banned by the IRS, such as life insurance and certain collectibles, as well as one’s own home.

For mid-career entrepreneurs or angel investors with some built-up retirement savings, it’s an intriguing thought that many do not know about.

At the end of July the Trump administration quietly killed a retirement program called MyRA , intended to help lower and middle-income people begin investing for retirement.

At the end of July the Trump administration quietly killed a retirement program called MyRA , intended to help lower and middle-income people begin investing for retirement.