The personal financial statement would be used to talk to any bank or lender about getting a loan. Even prior to that, it could be used by you to determine whether your startup idea makes financial sense at this time.

I think we should talk about inequality far more than we do. Even if I do not agree with the speaker, I would like to engage in the dialogue with anyone who speaks intelligently about the topic.

I’m embarrased to admit I haven’t yet read Pinketty’s Capital, but I will.

In the meantime, this is worth watching.

I don’t love his “We rich people should care about inequality because of the future pitchforks we face, so let’s be self-interested and work for more equality.”

I would prefer an argument that includes an ethical component, something along the lines of “equality helps increase human dignity.”

In his favor, however, he’s smart, provocative, and trying to be non-ideological, all of which I appreciate. Also, I like the examples he gives of the City of Seattle, and the Henry Ford theory of wages. Worth watching.

The headline is from The Twilight Zone movie, from when I was about 10 years old. As for the rest of the movie after that first moment, I experienced it as an audio-only event. I just stared down at my feet, too freaked out to look up above the seat in front of me.

Corporate pension-funding, analogous to long-term retirement planning or college funding for individuals, really comes down to small choices that we make today that have extraordinary consequences thirty years in the future.

This is the kind of thing which we – and our leaders – should worry about late at night.

Instead of course we focus on strategizing about which reality TV star ought to release a sex tape to revive her career, or which NFL player’s ongoing pattern of domestic abuse will cause a ‘distraction’ to his team during Sunday’s game.

I guess I’m just saying we’re typically not spending enough time worrying about the really scary things, like under-funded pension liabilities.

The WSJ article details that Congress passed, and Obama signed, a transportation bill that happens to contain a provision to allow companies temporary relief from fully funding their pension obligations. In the fine print of the article we learn that the pension-funding obligation comes from calculations of current interest rates, which are extraordinarily low. What companies wanted, and our leaders delivered, was a pension-funding formula that took into account interest rates of the last 25 years, rather than the last 2 years. This is a key difference.

Here’s how I assume it works: If you observe that prevailing interest rates of, say, 10 year bonds are at 2%, then you have to make the assumption that all money invested in bonds for the next ten years will return just 2% per year. That’s reasonable. And from there you can calculate how much money you’ll have in 10 years, using compound interest. (see how I always work in a link to that idea?)

The problem is that if you assume only a 2% return on your money, then you need to invest a lot more money today in order to actually have enough to meet the future obligations of your pension plan.

If you could instead assume a bond rate of return of 6% – because that was the average interest rate over the past 25 years – then you need a lot less money to fund your pension plan. Problem magically solved. Companies are happy. CEOs are happy. Workers who depend on pensions eventually are unhappy. But hey! As Meatloaf says, 2 out 3 ain’t bad.

As I’ve written previously, the low returns of bonds are a major drawback of a low interest rate environment, when you have to have enough money for the long run. Endowments and charities and pensions that previously depended on a healthy bond portfolio to kick out 5-6% returns every year are stuck either generating less money for the long run, or they’re going far out onto the risky end of the investment spectrum (over-allocating to stocks or more exotic risks) to make the numbers work.

Or, as we saw yesterday, just pretend you can get the returns on bonds that we got over the past 25 years. Ignore our actual historically low interest rates now with magical-thinking assumptions.

By the way, what happens when companies underfund their pensions?

If a company disappears or goes bust, the federal government (and therefore you and me, via taxes) picks up the unfunded pension liability through an agency known as the Pension Benefit Guaranty Corporation. Just as the FDIC guarantees bank deposits (up to a certain size) and insurance regulators guarantee insurance payouts (when an insurance company fails), so does the PBGC pick up pension obligations when a private company with a pension goes bust. In 2010 for example, 147 companies with pension failed, and the PBGC paid our $5.6 Billion in liabilities to pensioners.

A big factor in the GM and Chrysler bankruptcy and bailouts of 2008, for example, had to do with the government pension guaranties.

For some time before 2008, GM and Chrysler had morphed from car manufacturers with large pension plans into giant pension-liability companies that also happened to make some cars (that not enough people actually buy anymore.)

I can’t claim to know the details of the agreement signed into law yesterday, but using tricks like a 25 year average on historic interest rates, rather than current interest rates, should keep us up all night, rather frightened.

My morning commute this summer means driving the two young lovelies to their respective kid camps. I like driving in heavy traffic as much as I enjoy hauling over-heated kitchen garbage out to the brown bin in the garage in August. Which is to say, I often have my crinkled-nose sad face on when commuting.

One benefit of being stuck in 8 a.m. traffic headed north on U.S. 281, however, is the chance to reflect on my favorite analogy about investment fund fees and risky markets.

Picture me in traffic, in my dark red — although for my own pretentious reasons I insist friends refer to the color of my car as “Crimson” — Hyundai Elantra. This hot number accelerates from O to 60 in just under 4.3 minutes.

So we’re crawling along around 3 miles per hour, and I glance over my left shoulder at the electric blue Corvette next to me.

A key fact to know, which hardly needs spelling out, is that the owner of that pretty blue Corvette paid approximately three and a half times what I paid for my Hyundai.

I exchange a “Whaddyaknow?” grimace in solidarity with the middle-aged man behind the wheel of his sports car, since we’re both stuck behind a few miles of bumper-to-bumper commuters.

My investment fund fees analogy hinges on the key fact that my crimson Hyundai and my buddy-in-traffic’s electric blue Corvette are in the process of accomplishing exactly the same thing, despite an obvious difference in price — and an obvious difference in status.

Shiny, fast, and expensive!

Because both of us are moving nowhere fast.

Now, here’s my great traffic and investment fund analogy in full:

With your investments, your primary goal is to get from point A to point B. Specifically, to turn some amount of money you have today into some larger amount of money in the future.

The speed at which traffic flows is the market returns of any given year.

Sometimes you’ll flow along nicely up 281 at 65 miles an hour with not much traffic. That’s like earning a cool 12 percent from the stock market for the year without breaking a sweat.

On other occasions you’ll ease onto the nearly empty Pickle Parkway — also known as State Highway 130 — and legally cruise at 85 miles an hour. That’s what it feels like to earn 20 percent or more from the stock market.

And then, in the worst times, you’re stuck behind a four-car pileup, sweating and swearing and unable to move or even get off the highway. We had that kind of year in 2008, when everyone in stocks lost about 35 percent.

Here’s where my analogy really kicks in, though. For the vast majority of driving situations, like the vast majority of investing situations, we get what everybody else gets and there’s not much we can do about it.

As my daughters’ pre-school teachers like to remind them: The best (investing) attitude is ‘You get what you get and you don’t get upset.’ Maybe you already know this idea, and you set it to good use when you buy an investment fund. But I know most of us don’t act like we know it.

Practically the entire personal investing industry is built on the false conceit that you, the consumer, can buy a financial vehicle that can go faster than someone else’s vehicle — essentially to “beat the market.” In reality, that’s incredibly rare.

Without breaking the law, heading onto the shoulder lane or driving recklessly at an elevated risk of hurting yourself or others, you cannot generally beat the rate of traffic, whether you drive an electric blue Corvette or a crimson Hyundai Elantra.

And the same goes for investment funds. You can pay more for a mutual fund or hedge fund, but almost none of them reliably “beat the market.” Every rigorous academic study of financial funds ever done concludes this way: The difference in market returns between high-cost and low-cost funds is, in aggregate, the cost of the funds’ management fee. The difference in market returns, in aggregate, favors the low-cost fund.

Traditional mutual funds charge between 0.75 percent and 1.5 percent management fees, or between $750 and $1,500 per $100,000 investment per year. If you buy an index fund — the Hyundai Elantras of the investment world — you will pay between 0.1 percent and 0.5 percent management fees, or $100 to $500 per $100,000 in the account.

The entire financial industry would like you to think that the extra cost buys you something, but I’m here to tell you the straight fact that you’re paying three and a half times more to get exactly the same investment performance.

My immediate thought was that deflated feeling I got when I heard, in 1995, that the College Board would recenter the SAT to 500, because average scores kept dropping. Ugh. How would I know whether my SAT scores are higher than my kids’ scores? We can’t even compare now.

How will kids develop a competitive drive if they don’t know how their old man did on the SAT?

I remember when not every kid would get a shiny ribbons for “participation.” Instead, we would only get the giant trophy if you WON, and pummeled your youthful opponent into abject submission.

I mean, I remember when I used to walk all the way to school, uphill both ways, in a driving blizzard. And back for lunch.

And we loved it.

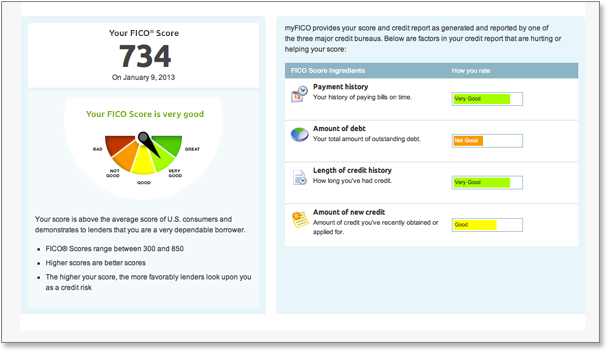

FICO scores

Anyway…back to FICO. According to the WSJ this morning, the makers of FICO will drop ‘settled’ delinquent accounts from their formula for calculating their key number used by practically every US lender in consumer credit decision-making. The result is that for people who had made late payments or let debts go to collections – but later paid or settled the accounts – the negative mark on their credit will drop off quickly.

The second change in the FICO formula is to de-emphasize the negative effect of delinquent medical bills.

Since FICO scores have traditionally been quite sensitive to a history of delinquent payments, the result is that millions of people could see their scores rise as a result of the formula change. Higher scores theoretically means that more people will have access to credit.

The point of the FICO score – for lenders – is to offer a snapshot of the probability of future consumer loan defaults. Fair Isaac says they studied whether the history of delinquent – but paid – accounts mattered to calculating these probabilities. Following the study, they said they could reliably drop the paid collection accounts, as well as lower the impact of medical delinquency and still maintain the same predicative power in the score.

A caveat

Although this change made the front page of the WSJ this morning, the real impact could be completely unrealized. Deep in the article Fair Isaac Corp says they will implement this more forgiving FICO formula via a new score called “FICO 9,” which makes it sound like this is just a supplemental score that banks could decide to pay attention to, or not.

Lenders make their own decision about what FICO score to buy, and they may not choose to shift from traditional FICO to FICO 9.

Like a college deciding to review the ACT rather than the SAT. So we’ll have to see whether banks adopt the new score or just ignore it.

I periodically produce instructional videos for a local micro lender named Accion Texas. They support and lend to young and startup companies that might otherwise get overlooked by the traditional banking industry. In fact one of the key conditions of being an Accion Texas customer is a prior rejection for a bank loan application.

The point of this video I made is to introduce Accion’s customers and potential customers to the value of tracking your startup costs in a spreadsheet. Since I am a huge proponent of entrepreneurship for building wealth, and since many entrepreneurs are not necessarily spreadsheet whizzes, I figured this may have appeal beyond just Accion Texas customers. I hope it will be useful to you.