Editor’s note: Paul recently purchased The Financial Rules For New College Graduates, then had some followup questions regarding mutual fund investments. Readers of the book…feel free to pepper me with your followups…

Dear Mike,

I’m on board 1000%1 when it comes to 100% equity mutual funds, the questions in my mind now are: “Which one(s) and how many?”

1) I’m finding many front-end load (5.50%-5.75%) managed funds with anywhere from 0.89% Expense Ratio to 1.40% (with the 1.20% range being the most common). I’m assuming that the lower the expense the better, but am I overstating the importance of this number?

2) Without splitting hairs about what the top 10 holdings are, the turnover within the fund itself, the risk and return vs category, how long the managers have been there and what their philosophy is, what are some of the key things you’d look for before settling on a fund?

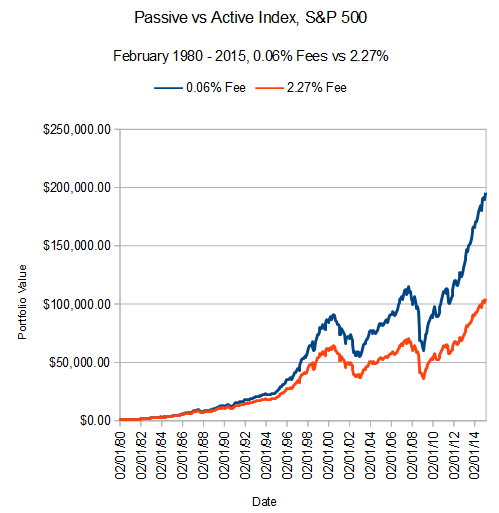

3) I’ve compared the 1 yr, 5 yr, 10 yr and Since inception returns of the funds. Many funds have returned 7-9% while some are well into the 10% and even 11% range. Would you put any stock (no pun intended) in those numbers when comparing and contrasting funds? Are these funds even worth looking into when an Index fund, through Vanguard for example, matches virtually every move the S&P 500 has made, returning the same 10.33% without the commission charge and SIGNIFICANTLY lower expense ratio (0.04%!!!)?

4) And, of course, is 1 fund enough, or would you explore the idea of having several?

Thank you for being willing to even read through this! Hopefully I haven’t strayed TOO far away from the simple approach I’ve attempted to internalize with your teachings.

–Paul F, Boston, MA

Dear Paul,

All great questions, I’ll take them one at a time

1. Front-end Load, Back-end Load – From my (consumer-driven, not industry-driven) perspective, these are all terrible, terrible fees and should be avoided. Never get a fund with them. Basically unconscionable. Can’t justify them at all. Only reason to pay these is if you are totally captive to an employer-sponsored plan and you have no choice of a no-load fund. If you are setting up your own investment plan, just eliminate them entirely.

On the other hand, from an industry (sales-driven) perspective, load funds are great. Makes the salesperson rich at the direct expense of the investor.

About the annual Expense Ratio…at this point 1% is kind of the industry marker. Less than 1% is a reasonable deal for an actively managed fund, over 1% is a little pricey for an actively managed fund. As I say in Ch.14 of my book, I don’t actually think paying for active management makes sense, but if you really want it then 1% is kind of the inflection point between cheap and expensive.

And finally, you are NOT overstating the importance of these numbers. They are – especially in the long run – the absolute key to not turning over between 20% and 50% of your lifetime investment gains to your investment managers. That’s not an exaggeration, its just math you can model out in a spreadsheet.

2. Fund factors to look for – For me (my big bias) the expense ratio is the #1 consideration. After that, of course you want to understand how active versus passive they are (my bias is for passive), how quick turnover is (my bias is for low turnover as it reduces costs and increases tax efficiency), how concentrated they are within the asset class (a case can be made for either diversification or concentration, depending on your overall goals and the rest of your investment plan), where it is in the risk spectrum (for a 20-something person I think you want to maximize risk in all long-term holdings. I still do and I’m in my mid-40s, and I will continue to maximize risk for my whole life, but that’s my bias for all my investments).

3. Time Horizon – For comparing returns, the 10 year and longest time horizons are the only relevant data points. I would ignore 1 to 5 year returns as essentially noise, since the right investment horizon is decades. If the manager is consistent in strategy, the long-term return will be what that particular market sector offers in the long run, which is all I’m looking for in an investment manager.

4. On Number of Funds – I’ll suggest a book for further reading by a guy I like: Lars Kroijer “Investing Demystified.” He doesn’t agree with me on my “risk maximization” point, but he and I agree on the efficient market hypothesis as a good starting point for most people. The reason I bring him up is he makes a case for owning a single “All World Markets” fund, which should be available from major discount brokers. After reading Kroijer you’d have a better sense of how many funds you’ll need. Whether just 1, or more.

As for me, I have just 3 funds in my 401K retirement account. All 3 are 100% equities:

1. US Small Cap,

2. Non-US Developed markets (Europe, Japan, NZ), and

3. an Emerging markets fund

I’m pretty happy with that and will probably never change it. Maybe I’ll re-balance once in a while if one starts to get too big relative to the others. But again, Kroijer’s book will probably explain well why that view makes sense to me.

I suspect readers of my column on calculating investment returns responded “ok, yes, fine, thanks for the theoretical treatise, but tell me how do I make money?”

Interestingly, MO stock can tell us a thing or two about that question as well. A contrarian like me cannot resist the opportunity to discuss MO in terms of:

Socially responsible investing vs. sin investing, and

To summarize those ideas: I don’t like the costs of a typical socially conscious mutual fund; it’s difficult to match up large public companies with one’s specific moral compass; and the returns of such funds may not keep up with the broader market.

In fact, the opposite of ‘socially conscious’ investing – aka ‘sin’ investing – may be a far better idea, at least for making money on your money.

While our choice to avoid buying a company like Altria was not market moving,[1] that choice multiplied by many billions of dollars by other similarly-situated investors can leave socially unappealing companies like Altria undervalued. In other words, the fact that cigarette smoking is totally disgusting is the key to Altria’s attractiveness as a stock.

The fund – formerly known by the catchy name ‘Vice Fund’ but now going by the more staid ‘USA Mutuals Barrier Fund’ – has had a good record beating a broad market index by nearly 2% per year for the past decade.

I generally do not believe that mutual funds can consistently outperform comparable market benchmarks.

Yet even an ‘efficient markets’ guy like me can imagine that systematic aversion by some investors to some ‘sin industry’ companies creates opportunity for other investors.

By the way, I’m not advocating actually investing in this fund, because the management fees, at 1.46%, run well above what I would consider for my own account or recommend for others. But I think their success may – possibly – highlight an inefficiency in an otherwise extraordinarily efficient market.

Most Successful Company In The World

Finance writer Morgan Housel featured MO stock, Altria, a few weeks ago in a post on the Motley Fool site calling it “the most successful company in the world.”

Before identifying Altria as his featured company, he described the long-run returns of stock ownership:

One dollar invested in this company in 1968 was worth $6,638 yesterday…that’s an annual return of 20.6% per year for nearly half a century…What company is this?

On Innovation and stock investing

And then Housel built the suspense before revealing the company as Altria, tongue firmly in cheek:

…It had to have been revolutionary. It had to have been innovative. It must be in an industry that changed the world – probably the biggest trend of the 20th Century. It must have done something no other company could do.

And then Housel goes on to reveal – in a way that thrills an incorrigible contrarian like myself – that this world-beating stock is in an unattractive industry, one that suffered massive declines and lawsuits over the past 30 years.

Most interestingly to Housel, and to me for that matter, tobacco as an industry barely innovates at all. And that, Housel goes on to say, is another key to its success.

Innovation is super-expensive. Innovation is risky! Innovative companies frequently die. Innovative companies in rapidly evolving industries get beaten by newer upstarts.

By the way, Tesla Motors, to name one public company that I’m reasonably certain will be dead in 5 years, despite its $25B market cap, is an innovative company.

But that doesn’t make it a good stock to own.

Tobacco delivery is not innovative, but rather something far more valuable for a stock: It’s profitable.

A few final thoughts

I don’t own MO, except probably tucked away as one of a few thousand companies in some broad index fund I own in a retirement account.

I have absolutely zero opinion on whether one should or should not own MO stock for investment purposes.

Would a few people mark their calendars for five years on Tesla and let me know how I did with my call? Because I AM SO RIGHT.

[1] My daughter’s stock picking is NOT YET market moving. But look out, Bill Ackman, she’s gunning for you.

And by “much interest” I mean the story made me want to stab my own hand with a sharp pencil.

I hate this sort of thing.

Not because of straight up corruption

Let’s leave aside the obvious problem of ‘economic development’ schemes like this, in which public entities give targeted incentives to a specific, private company: You know, because private individuals who benefit may feel quite ‘grateful’ to their public sponsors. Public sponsors in turn – elected and appointed officials – may then have an incentive to direct public funds to private beneficiaries to keep the ‘gratefulness’ cycle going.

That’s all obviously just straight up corruption and not really what I’m aiming for here in my critique of city-directed ‘economic incentives’ for private companies. [1]

What I really hate about this is something quite different, having to do with three business concepts: selection bias, market efficiency, and the structural short-run conflict between entrepreneurial goals and public policy goals.

Taken together, they greatly reduce the odds that this type of economic development works out for the public good in the long run.

I’ll address these in order.

Selection bias

Would you like your city (or state, or county) to grow companies focused on wooing public investment and public ‘economic development’ incentives? Or would you like your city to grow companies that focus on profitability without a public subsidy or public investment? Because the way you attract companies to your city (or state, or county) introduces a real selection bias to the pool of companies you end up with.

In my experience, the kind of startup company that takes public money – with all the attendant scrutiny, ‘job creation’ requirements and ‘salary’ minimums – is a different sort of company than one that achieves sustainability without that public money.

Market Efficiency

Private investors constantly scour the market for small but growing companies that provide a reasonable chance at future profits.

Small but growing companies in turn often seek direct investments from private investors known as ‘angel’ or ‘venture’ capitalists.

It’s not a perfect system, and market inefficiencies occasionally arise.

But when a company turns to public funds like this, what that signals to me is that private capital sources – the professional angel and venture capitalists – have already declined to invest in the growth of this company. That’s typically because professional angel and venture capitalists do not find the risk/reward profile of that investment sufficiently compelling.

Now, professional investors may be wrong to have overlooked the growth and profitability potential of these medical device companies.

The angel investing market may be inefficient.

Who knows? Maybe the City of San Antonio Economic Development team may have a market-beating strategy for identifying a positive risk/reward formula that private investors have declined to take. I mean, it could happen, right?

But I doubt it. And I would never bet on it.

The short-run conflict between entrepreneurship and public policy goals.

Look, here’s the biggest problem.

Public officials want to be seen to create “jobs.” At “good salaries.” That’s fine.

But entrepreneurs don’t seek to create jobs. At any salary.

Entrepreneurs, at least the good ones, want to create the least number of jobs possible. I’m not saying this because entrepreneurs are inherently mean-spirited, but rather, because hiring people is expensive.

Successful small companies – and big ones too – have to constantly try to eliminate jobs to make a company financially sustainable. The market is too darned competitive to survive when you’re burdened with too many people on the payroll. If public officials get the chance to dictate the number of jobs, and the salary minimums of jobs, I guess I have my doubts about how that business is being run.

You show me an entrepreneur willing to be told by a city entity how many people to hire, when to hire them, and what to pay them, then I will show you an entrepreneur who isn’t going to make it in the long run.

Because that’s what Romney’s firm Bain Capital is good at. They buy a company, wring out expensive costs (all those “good salary” jobs!) and then resell. In the short run, the more jobs you eliminate, the better. I’m not saying this to besmirch Romney’s record. I’m sure he was a fantastic capitalist. Cutting costs is what capitalists, and entrepreneurs do, and often that means eliminating jobs. But Romney as “job creator?” Give me a break.

I mention this to illustrate the short-run differences in goals between entrepreneurs and public policy officials

Ok, now back to San Antonio.

I hope I’m wrong

I hope to be completely wrong about this $1.75 million direct investment. Despite my misgivings, I will be thrilled when these three startup medical device companies spur innovation, trigger job growth, add to the ‘entrepreneurial ecosystem’ and even generate a positive return on public capital.

It could happen! I hope it happens!

But I would never, ever, choose to bet on it with my own money. And I’m sorry when the city chooses this for me.

[1] That kind of obvious corruption is what the New York Times had in mind in pointing out in 2012 that Dallas-based tax consultant G. Brint Ryan worked to secure tax breaks for private corporations in Texas while personally donating $250,000 and $150,000 for the Governor and Lieutenant Governor respectively. I don’t mean all that, since it’s all too obvious how each group benefits there at the expense of the public good. I mean, who could deny it with a straight face?

Editor’s Note: A version of this appeared in the San Antonio Express News. Dignowity Hill is a historic neighborhood in San Antonio balanced precariously – for the moment – on the cusp of hipsterism, about to fall into the ‘gentrified’ category. For anyone who has strongly held opinions about gentrification, let me assure you this post has nothing to do with Dignowity Hill, or gentrification. Thank you.

My friend recently asked me what I thought about his idea of buying a small plot of land he saw for sale in Dignowity Hill, as a short-term investment. Less than $10,000.

“The East Side is getting ready to boom,” he tells me. Agreed.

“Dignowity Hill has so much charm and a ton of new investment activity nearby, with the Hays Street Bridge and Brewery, and prices will be going up.” Yup, probably.

“I like the idea of investing for a couple of years, then cashing out.” Ok, now I knew he was on the wrong track, and I told him so.

Markets are more efficient than you think

What I believe my friend did not take into account is the idea that he has hundreds – actually make that probably thousands – of competitors for that single parcel on Dignowity Hill. Those competitors mean he will not likely get a bargain.

Most middle class people, certainly most homeowners, understand the basics of real estate investing. That means hundreds of thousands of people – in San Antonio alone – have the knowledge necessary to buy that parcel, and certainly tens of thousands of people in the city have available cash to pick up a plot of land at less than $10,000.

Of those tens of thousands, I’d estimate many hundreds to a few thousand San Antonio residents actively look for real estate opportunities. I don’t think it’s unreasonable to expect that hundreds of San Antonians have seen this exact parcel, and up until now, have not made a bona fide offer to purchase it, at, or very near, the listed price.

This is not to say definitively that the parcel is a bad investment. Frankly I have no idea. I never looked at it. But I do know that markets with hundreds of potential buyers are pretty efficient at price discovery, and the parcel will not be a screaming bargain for my friend.

Will the East Side boom? Sure. Is Dignowity Hill totally cool? Yeah. Could prices double in a few years? I wouldn’t be surprised.

But the current offering price of the parcel will take into account all of these factors. Any reasonably efficient market aggregates opinions and is forward-looking – meaning my friend would have to pay now for the likely boom, the coolness, and the chance of doubling.

My entire point with this anecdote is this: although we may not see the competition in front of us, many markets are extremely efficient at reflecting all the unseen competition for investments. Real estate is less efficient than some markets, but it’s really not so inefficient that a part-time speculator like my friend will grab a great bargain.

Before concluding, I want to point out two other reasons my friend should be cautious.

Short-term time horizons

If you need to sell any investment within five years, then I don’t call that an investment, that’s something like a speculation. There’s nothing inherently wrong with speculating, only that it tends to work up until the point when it doesn’t any more, and then it ends up looking a lot like gambling in retrospect.

Real estate inefficiency

Real estate – as a speculation or as an investment – is terribly inefficient to buy and sell. Most real estate transactions require you to get an appraisal, do a title search, pay a realtor, and possibly an attorney, all of which add up quickly.

To invest $10,000 in the stock market, for example, will cost you less than $20 to do the transaction at an online discount broker. To invest $10,000 in real estate – unless you have distinct professional discounts or built-in advantages – might run you 1,000 in fees, easily.

I’m not saying I don’t love real estate as a long-term investment. I love real estate. Most of my non-retirement net worth comes from real estate ownership, of my home. But for small, short-term investments, I would rarely recommend real estate, much less real estate speculation.

Editor’s Note: Author and recovering hedge funder Lars Kroijer provided this guest-post, making the case that most of us would be better off acknowledging we do not have an edge over markets. Most of us can’t consistently “beat the market,” but many of us pay a lot in fees to try.

Edge over the markets, do you have it, and the 7 Porsche cars it may cost you to find out

by Lars Kroijer

Most literature or media on finance today tells us how to make money. We are bombarded with stock tips about the next Apple or Google, read articles on how India or biotech investing are the next hot thing, or told how some star investment manager’s outstanding performance is set to continue. The implicit message is that only the uninformed few fail to heed this advice and those that do end up poorer as a result. We wouldn’t want that to be us!

What if we started with a very different premise? The premise that markets are actually quite efficient. Even if some people are able to outperform the markets, most people are not among them. In financial jargon, most people do not have edge over the financial markets, which is to say that they can’t perform better than the financial market through active selection of investments different from that made by the market. Embracing and understanding this absence of edge as an investor is a key premise of the investment methods suggested in my recent book Investing Demystified (Financial Times Publishing), and something I believe is critical for all investors to understand.

Consider these two investments portfolios:

A) S&P500 Index Tracker Portfolio like an ETF or index fund.

B) A portfolio consisting of a number of stocks from the S&P 500 – any number of stocks from that index that you think will outperform the index. It could be one stock or 499 stocks, or anything in between, or even the 500 stocks weighted differently from the index (which is based on market value weighting).

If you can ensure the consistent outperformance of portfolio B over portfolio A, even after the higher fees and expenses associated with creating portfolio B, you have edge investing in the S&P500. If you can’t, you don’t have edge.

At first glance it may seem easy to have edge in the S&P500. All you have to do is pick a subset of 500 stocks that will do better than the rest, and surely there are a number of predictable duds in there. In fact, all you would have to do is to find one dud, omit that from the rest and you would already be ahead. How hard can that be? Similarly, all you would have to do is to pick one winner and you would also be ahead.

Although the examples in this piece are from the stock market, investors can have edge in virtually any kind of investment all over the world. In fact there are so many different ways to have edge that it may seem like an admission of ignorance to some to renounce all of them. Their gut instinct may tell them that not only do they want to have edge, but the idea of not even trying to gain it is a cheap surrender. They want to take on the markets and outperform as a vindication that they “get it” or are somehow of a superior intellect or street-smart. Whatever works!

The Competition

When considering your edge who is it exactly that you have edge over? The other market participants obviously, but instead of a faceless mass, think about whom they actually are and what knowledge they have and analysis they undertake.

Can you have an edge investing in Microsoft?

Imagine the portfolio manager of the technology focused fund for a highly rated mutual fund / unit trust who like us is looking at Microsoft. Let’s call them Ability Tech and the fund manager Susan.

Susan and Ability have easy access to all the research that is written about Microsoft including the 80 page in-depth reports from research analysts from all the major banks including places like Morgan Stanley or Goldman Sachs that have followed Microsoft and all its competitors since Bill Gates started the business. The analysts know all of the business lines of Microsoft, down to the programmers who write the code to the marketing groups that come up with the great ads. They may have worked at Microsoft or its competitors, and perhaps went to Harvard or Stanford with senior members of the management team. On top of that, the analysts speak frequently with the trading groups of their banks who are among the market leaders in the trading of the Microsoft shares and can see market moves faster and more accurately than almost any trader.

All research analysts will talk to Susan regularly and at great length because of the commissions Ability’s trading generates. Microsoft is a big position for Ability and Susan reads all the reports thoroughly – it’s important to know what the market thinks. Susan enjoys the technical product development aspects of Microsoft and she feels she talks the same language as techies, partly because she knew some of them from when she studied computer science at MIT. But Susan’s somewhat “nerdy” demeanour is balanced out by her “gut feel” colleague, who see bigger picture trends in the technology sector and specifically sees how Microsoft is perceived in the market and ability to respond to a changing business environment.

Susan and her colleagues frequently go to IT conferences and have meetings with senior people from Microsoft and peer companies, and are on first name basis with most of them. Microsoft also arranged for Ability to visit the senior management at offices around the world, both in sales roles and developers, and Susan also talks to some of the leading clients.

Like the research analysts from the banks, Ability has an army of expert PhD’s who study sales trends and spot new potential challenges (they were among the first to spot Facebook and Google). Further, Ability has economists who study the US and global financial system in detail as the world economy will impact the performance of Microsoft. Ability also has mathematicians with trading pattern recognition technology to help with the analysis.

Susan loves reading books about technology and every finance/investing book she can get her hands on, including all the Buffett and value investor books.

Susan and her team know everything there is to know about the stocks she follows (including a few things she probably shouldn’t know, but she keeps that close to her chest), some of which are much smaller and less well researched than Microsoft. She has among the best ratings among fund managers in a couple of the comparison sites, but doesn’t pay too much attention to that. After doing this for over twenty years she knows how quickly things can change and instead focuses on remaining at the top of her game.

Does Susan have edge?

This man appears to have a market edge. He is ridiculously rare.

Do you think you have edge over Susan and the thousands of people like her? If you do, you might be brilliant, arrogant, the next Warren Buffett or George Soros, be lucky, or all of the above. If you don’t, you don’t have edge. Most people don’t. Most people are better off admitting to themselves that once a company is listed on an exchange and has a market price, then we are better off assuming that this is a price that reflects the stock’s true value, incorporating a future positive return for the stock, but also a risk that things don’t go according to plan. So it’s not that all publicly listed companies are good – far from it – but rather that we don’t know better than to assume that their stock prices incorporate an expectation of a fair future return to the shareholders given the risks. We don’t have edge.

When I ran my hedge fund I would always think about the fictitious Susan and Ability. I would think of someone super clever, well connected, product savvy yet street-smart who had been around the block and seen the inside stories of success and failure. And then I would convince myself that we should not be involved in trades unless we clearly thought we had edge over them. It is hard to convince yourself that this is possible, and unfortunately even harder sometimes for it to actually be true.

The costs add up

On average individual investors trying to beat the markets would not systematically pick underperforming stocks – on average they would pick stocks that perform like the overall market. They would have a sub-optimal portfolio that would not be as well diversified, but in my view the main underperformance comes from the costs incurred.

The most obvious cost when you trade a stock is the commission to trade. While that has been lowered dramatically with online trading platforms it is far from the only cost. A few others to consider:

Bid/offer spread

Price impact

Transaction tax

Turnover

Information/research cost

Capital gains tax

Transfer charge

Custody charge

Advisory charge

Your time?

Depending on your circumstances and size of portfolio you may find that it costs more than 1% each time you trade the portfolio (the low fixed online charge per trade is only a small commission percentage if you trade large amounts). This is certainly less than it used to be decades ago, but for someone who is frequently trading their portfolio it will be a major impediment to performance. In addition capital gains taxation tends to be far higher for frequent traders and the “hidden fees” like custody or direct or indirect costs of the research and information gathering come on top. The more this adds up to, the greater the edge someone will have to have to just keep up with the market.

Can trading stocks or FX make you cool like Tom Cruise?

I recently saw a particularly cringe-worthy advertisement where a broker compared trading on their platform to being a fighter pilot, complete with Tom Cruise style Ray-Ban sunglasses and an adoring blonde. I remember thinking “I would love to sell something to whoever falls for that”. The platform makes more money the more frequently you trade, and they obviously think you trade more if you think it’ll make you be like Tom Cruise.

You just have to pick your moment?

Warren Buffett is quoted as saying that “just because markets are efficient most of the time does not mean that they are efficient all of the time”. To quote Buffett in investing is like quoting Tiger Woods in golf. He is a world famous investor with a long history of being right, so we are all bound to feel a little deferential.

Buffett might be right of course. Markets might be perfectly efficient some or even most of the time and horribly inefficient at other times. But how should we mere mortal investors know which is when? Can you predict when these moments of inefficiency occur or recognize them when you see them? Clearly we can’t all see the inefficiencies at the same time or the market impact of many investors trying to do the same thing would rectify any inefficiency in an instant. But can you as an individual investor spot a time of inefficiency?

I think that it is incredibly hard to have edge in the market even occasionally, but that some people have it, even most the time. But you have to be honest with yourself. If you have a long history of picking moments where you spotted a great opportunity, moved in to take advantage of it and then exited with a profit, then you may indeed occasionally have edge. You should use this edge to get rich.

For the sceptics

Some readers will think this is a load of rubbish. It may be that they consider themselves among the sophisticated investors who can outperform the market. You might of course be in the very small minority of people where this is the case, but if you are going to claim edge and actively manage your own portfolio I would encourage you to consider a couple of things:

Be clear about why you have edge to beat the market, and be sure you are not guilty of selective memory. Unlike predicting the winner of Saturday’s football game, predicting that Google was going to double when it later did makes us appear wise and informed, and perhaps we are subconsciously more likely to remember that than when we proclaimed Enron a doubler. Because we add and take money out of our accounts continuously we are unlikely to keep close track of our exact performance and can continue the delusion indefinitely.

Do not trade frequently. If you turn over your portfolio more than once per year you should have a really good reason to do so. The all-in costs of trading are high and greatly reduce long-term returns.

Regardless of whether you have edge or not, be sure to think a lot about risk levels, taxes, liquidity, and how your investment portfolio correlates with the rest of your assets and liabilities.

Do not start panicking if things go against you.

You may decide you have edge in one sector, geography, or asset class. That’s fine. Do exploit this edge, but also make sure it does not lead to undue geographic or sector concentration and invest like someone without edge in the rest of your portfolio.

Continuously reconsider your edge. There is no shame and likely good money in acknowledging that you belong to the vast majority of people that don’t have edge. Investors who initially do well in the markets will often think it was skill rather than luck based on that first experience. Many reconsider later…

The cost of time spent managing the portfolio are individual (we value our time differently) and while some consider it a fun hobby or game akin to betting even, others consider it a chore they would rather avoid. Someone may spend 10 hours “work time” per week on their portfolio which at an “opportunity cost” of time of £50 per hour for 40 weeks/year is £20,000 per year on top of all the other costs discussed. This clearly makes no sense for a £100,000 portfolio, and is too costly even for a £1million portfolio, and on top of all everything else they would benefit from less time spent.

Should we give our money to Susan and Ability?

Going back to the beginning, if you conclude that Susan is as plugged in and informed as anyone could be, why not just give her our money and let her make us rich?

Many investors do give their money to the many Ability Tech type products and Fidelity and its peers continuously develop mutual funds for everything you can imagine. There are funds for industrials, defensive stocks (and defence sector stocks for that matter), gold stocks, oil stocks, telecoms, financials, technology, plus many geographic variations. In my view many investors have become “fund pickers” instead of “stock pickers”. Even today, years after the benefits of index tracking have become clear to many investors there is perhaps £85 invested with managers that try to outperform the index (“active” managers) for every £15 invested in index trackers.

When investors pick from the smorgasbord of tempting-looking funds how do they know which ones are going to outperform going forward?

Is it because they have a feeling that IT stocks will outperform the wider markets?

If so, are you effectively claiming edge by suggesting that you can pick sub-sets of the market that will outperform the wider markets? Consistently picking outperforming sectors would be an amazing skill.

Is it because of Susan’s impressive resume (you think that someone with her impressive background will find a way to outperform the market)?

If so, your edge is essentially saying that you know someone who has edge (Susan), which is really another form of edge? This is the kind of edge many investors into hedge funds claim. They’ll say stuff like “through our painstaking research process we select the few outstanding managers who consistently outperform”. Maybe so, but that is also a case of edge.

Is it because they feel Ability Tech has come up with some magic formula that will ensure their continued outperformance in their funds generally?

There is little data to suggest that that you can objectively pick which mutual funds are going to outperform going forward.

Is it because your financial advisor considers it a sound choice?

First figure out if the advisor has a financial incentive to give you the advice, like a cut of the fees. The world is moving towards greater clarity on how advisors get paid, making it easier to understand if there is a financial incentive to recommend some products – keep in mind that comparison sites also get a cut of the often hefty active manager fees. Now consider if your advisor really has the edge required to make this active choice. Unless she has a long history of getting these calls right I would question if she has the special edge that eludes most (and would she really share this incredibly unique insight if she had it?).

They have done so well in the past?

Countless studies confirm that past performance is a poor predictor of future performance. If life was only so easy – you just pick the winners and away you go…

We are also often driven by the urge to do something proactive to better our investment returns instead of passively standing by. And what better than investing with a strong performing manager from a reputable firm in a hot sector we have researched?

Mutual fund/unit trust charges vary greatly. Some charge up-front fees (though less frequently than in the past), but all charge an annual management fee and expenses (for things like audit, legal, etc.), in addition to the cost of making the investments. The all-in costs span a wide range, but if you assume that a total of 2.5% per year that is probably not too far off. So if someone manages £100 for you, the all-in costs of doing this will amount to approximately £2.5 per year come rain or shine.

If markets are steaming ahead and are up 20%+ every year, paying 1/10th to the well-known steward of your money may seem a fair deal. The trouble is that no markets go up 20% per year every year. We can perhaps expect equity markets to be up 4-5% on average per year above inflation so you need to pick a mutual fund that will outperform the markets by 2% before your costs to be no worse off than if you had picked the index tracking ETF, assuming ETF fees and expenses of 0.5% per year.

You need to be able to pick the best mutual fund out of 10 for it to make sense!

To give an idea of how much the fees impact over time consider the example of investing £100 for 30 years. Suppose the markets return 7% per year (5% real return plus 2% inflation a fairly standard expectation) and the difference becomes all too obvious over time (2% fee disadvantage in this case compared to a tracker fund).

Ability Tech and its many competitors go to great lengths to show their data in the brightest light, but a convincing number of studies show that the average professional investor does not beat the market over time, but in fact underperform by approximately the fees.

There is of course the possibility that you are somehow able to pick only the best performing funds. Take the example that you had £100 to invest in either an index tracker, or a mutual fund that had a cost disadvantage of 2% per year compared to the tracker. Suppose further that the market made a return of 7% per year for the next ten years, and that the standard deviation (standard measure of risk that gives an idea of the range of returns you can expect and with what frequency) of each mutual fund performance relative to the average mutual fund performance was 5% (the mutual funds predominantly own the same stocks as the index and their performance will be fairly similar as a result).

Comparing an actively managed portfolio to an index tracker is unfortunately not as simple as subtracting 2% from the index tracker to get to the actively managed return. The returns will vary from year to year, and in some years the actively managed fund will outperform the index it is tracking. Some funds will even outperform the index over the ten year period; if you can pick the outperforming fund consistently, you have edge. If you can’t, you should buy the index.

In approximately 90% of the cases in the ten year example above the index tracker would outperform the actively managed mutual fund, which is roughly in line with what historical studies suggest. So in order for it to make sense to pick a mutual fund over the index tracker you have to be able to pick the 10% best performing mutual funds. That would be pretty impressive.

If you did not have edge and blindly picked a mutual fund instead of the index tracker you would on average be about £30 worse off on your £100 investment after ten years because of the higher costs.

The lifetime savings from admitting no ‘edge’ add up to seven porsches

To put in perspective the cumulative impact over a saver’s life consider someone earning £50,000 a year on average between ages 25-67 who puts aside 10% of savings in the equity markets (ignoring tax) – that is roughly what a senior London Underground train driver makes. If equity markets perform similarly to how they have in the past (so about 5% per year above inflation) the average difference in money for the saver at retirement for someone who invested with an active fund manager compared to a product that simply tracks the market will be the equivalent of the value of about 7 Porsche cars (or approximately £280,000 in today’s money). Think about this – a fairly typical saver left poorer by a staggering total amount of money over a life time with the money going to the financial sector. The finance sector won’t like you doing it, but unless you have an amazing ability to pick only the best active fund managers, buy the product that replicates the market and you’ll be much better off in the long run.

While you can bet your bottom dollar that the 10% of mutual funds that outperformed the index would market their special skills in advertisements, historical performance is not only poor predictors of future returns, but it can be very hard to distinguish between what has been chance (luck) and skill (edge). Just like one out of 1024 coin flippers would come up heads 10 flips in a row, some managers would do better simply out of luck. In reality the odds are much worse in the financial markets as fees and costs eat into the returns. However ask the manager who has outperformed five years in a row (every 50th coin flipper…) and she will disagree with the argument that she was just lucky, even as some invariably are. Likewise some managers underperform the market several years in a row simply due to bad luck, but those disappear from the scene and thus introduce a selection bias where only the winners remain. Sometimes this makes the industry appear more successful than it has actually been.

Edge can take many forms

While the discussion above may suggest that having edge involves picking winning stocks or successful active managers only, there are many ways investors implicitly claim edge in their investments, often without having it. Examples include:

Will midcaps outperform large caps?

Will Buffett continue his outperformance?

Will emerging markets outperform developed markets the next decade?

Will tech stocks do better than financial stocks?

Will Germany outperform the UK?

Similarly, the discussion of edge is not exclusive to stock markets. You can have investment edge in many things other than the stock market and profit greatly from that edge. Examples include:

Will Greece default on its loans?

Will the price of oil increase further?

Will the USD/GBP exchange rate reach 2 again?

Will the property market increase/decrease?

Will interest rates remain low?

The list goes on…

Investing without edge

For someone to accept that they don’t have edge is a key “aha” moment in their investing lives, and perhaps without knowing it at first, they will be much better off as a result. At this point you are hopefully at least considering a couple of things:

Edge is hard to achieve and it is important to be realistic about if you have it.

Conceding edge is a sensible and very liberating conclusion for most investors. It makes life lot easier (and wealthier) to acknowledge that you can’t better the aggregate knowledge of a market swamped with thousands of experts that study Microsoft and the wider markets.

Once you have conceded edge you are unfortunately not done. In fact you have only arrived at the starting point and started your journey as an investor who has conceded edge. There is every change that you will be a far wealthier investor as a result of this.

For the edgeless investor it makes sense to pick the most diversified and cheapest portfolio of world equities and combining that with some government and potentially corporate bonds through cheap index tracking products that suit your risk and tax profile. Do this while considering your non-investment assets/liabilities, time horizon of investment, and a few other things, and you are doing extremely well. Once you embrace that you don’t have edge it is fortunately pretty intuitive and really not that difficult to put together a simple and powerful investment portfolio. More on that in the next blog post!

In this discussion with author Lars Kroijer we talk about the main assumption of his book Investing Demystified – which I happen to completely endorse – which is that ‘beating the market’ lies somewhere between highly unlikely and impossible. The goal for individuals should be, instead, to earn market returns. Common behaviors that most investors do, like

1. Paying extra management fees to an active portfolio manager, or

2. Stock picking yourself in order to ‘beat the market’

is a fool’s game, and will ultimately prove unnecessarily costly.

Later in the interview I asked Kroijer to describe his earlier book, Money Mavericks.

Lars: Everyone’s got sort of their angle. My angle is really to start with asking a question of the investor, which is; do you have edge? Are you able to beat the markets? I don’t even make that call for you but I try to illustrate it is incredibly hard to have edge, and that most people have no shot in hell whatsoever of attaining it. Incidentally, that means that people like you are I are not necessarily hypocrites because it’s entirely consistent with our former lives to say we worked in the financial markets; we’ve bought and sold products, and as well informed as anyone. So if we didn’t have edge, edge doesn’t exist.

You could say I’m a hedge-fund manager, and I sold edge for a living, and I certainly thought I had it. But that doesn’t mean that most people, or even that many people have it. I start with the premise in this book of saying do you have it. Then I go on to explain it’s really bloody hard to have it. If you don’t have it, which most people don’t, what should you do?

Essentially, this is a book written for my mom. It kind of is. You wouldn’t believe, but as a former hedge-fund manager, every time I talk to my mom, who’s a retired schoolteacher, she’d always say which stock should I buy. I’d say mom, you could buy an index. And she’s like no, no. Then she’d say stuff like Dansker bonds have done so well, I should be buying it. And I’d be like no, don’t do that. She’s certainly not alone in that position.

Michael: I completely agree with you, and when I think about how your book lays out four simple rules, starting with the one that you should be exposed to the broadest, most global index portfolio, and I have not done that, in terms of I am US-centric and small-caps centric, so I don’t have the broadest exposure. On the other hand, there is no gap between what you advocate, in terms of can you beat the market, and the way in which I invest, which is always I assume from the get-go ‑‑ and this is why that part of it resonated with me ‑‑ so clearly I, like you, say you can’t beat the market. The goal should not be to beat the market. The goal is to expose yourself to the appropriate allocation to risky markets, appropriate to your own personal situation. And then get the market return.

Lars: You want to capture the equity-risk premium.

Michael: The entire finance-marketing machine is about can you beat the market. Beating the market is a complete fool’s game. I think it’s particularly interesting, the other reason I wanted to talk to you, is because you’ve worked in the hedge-fund world, you’ve been a hedge-fund manager, an advisor to hedge funds. I worked on Wall Street. I founded my own fund, and it’s all about that theory that you can, in a sense, have an edge in the market. Yet, the more you know about how it actually works, the more extremely bright people, with the highest powered computing power and the most cutting-edge ideas ‑‑ and you think about the power they had, and we had, and the chances of any retail investor or in fact any of those investors themselves beating the market, or as you say, having edge, is just impossible.

Lars: Add to that they’re at a huge cost disadvantage, informational disadvantage, analytical disadvantage. It’s so unlikely, and this is why always start with you’ve got to convince people they can’t. That’s actually probably the toughest thing. You’re fighting not only against conventional wisdom, but you’re also fighting this almost innate thing we have, that you somehow have to actively do something. You somehow have to pick Google or whatever.

You have to have a view, and you’re smart, you’re educated, doing something to improve your retirement income, or whatever you’re doing. What you and I are advocating is essentially do nothing. Admit you can’t. I think that rubs a lot of people the wrong way.

Michael: You need to bring humility to the situation. I cannot do better than the market. I can do the market but I can’t do better. It’s a very hard, humble approach, but in my opinion and in your opinion it’s the correct approach.

Lars: Yeah. And I also think we’re extremely guilty of selective memory. We remember our winners. That adds to the feeling. It’s a bit like when you ask guys whether they’re an above-average driver. 90% will say they’re above average.

If you ask stock pickers whether they do better than average, 90% of stock pickers would say yes, even more than that. I think there’s a lot of that, a huge degree of selective memory. It’s a shame because I think it really hurts people in the long run.

Michael: It makes conversations along the lines of what you mentioned with your mother conversations with me and other friends and retail investors in stocks ‑‑ hey, I’ve got this great new stock. I’m such a bummer when I talk to them because I say really? I don’t know what to say.

Lars: The alternative is to say you don’t know what you’re talking about, which is not an all together pleasant thing to say. It’s not how you make friends. Certainly not when you’re moving to a new town, like you did.

Michael: I’ve written about this on my site before, but essentially when somebody talks about individual stocks, to me what I’m hearing is I went to Vegas. I put money on 32 and 17 on the roulette wheel. Look how I did. I just don’t know how to respond to that. That’s fabulous, you hit 17 once. I don’t know what to say.

Lars: This is conventional wisdom because to most other people that person will sound smart and educated. They will say here’s why I found this brilliant stock and here’s why it’s going to do great. Most people in the room will consider that person really smart, educated, and someone who’s got it. They’ll sound clever about something we all care about, namely our savings. And you think if I could only have that, I’d want that. It’s tough to go against that.

This is why I think the biggest part of this book is if I could get people to question that. Maybe even accept they can’t beat the market. Then that would be the greatest accomplishment. I think a lot of the rest follows. I haven’t come up with any particularly brilliant theory here. It’s sort of academic theory implemented in the real world and that’s pretty straightforward.

Michael: It cuts against the grain of what I call on my site “Financial Infotainment Industrial Complex,” which is there’s a lot of people invested in the idea that markets can be beaten, that individual investors can play a role.

Lars: Think of how many people would lose their jobs?

Michael: Yeah, it’s an entire machine around this idea. It’s very hard to fight against that. It’s very boring to fight against that. I joked about it in my review; your book is purposefully hey, I have some boring news for you. Here’s the way to get the returns on the market and sleep better at night.

Lars: I sort of compared going to the dentist. You really ought to do it once in a while and think about it. I completely agree with you. I mentioned in the book ‑‑ when I thought about writing this book, it was one of these things that slowly took form, but there’s this ad up for one of these direct-trading platform websites. And there was a guy who was embraced by a very attractive, scantily dressed woman. He was wearing Top Gun sunglasses, with a fighter jet in the background. It said something like “Take control of your stock market picks.”

I thought fuck; are you kidding me? Really? Whoever falls for that, I’d love to sell them something.

Michael: Oh yeah, they’d be a great mark.

Lars: You also hear a lot about the quick trading sort of high-turnover platforms. It’s something like 85-90% of the people on there will lose money. You have a lot of these companies, their clients, 85-90% will lose money.

It’s almost akin to gambling. You can argue is it gambling, which is a regulated industry in a lot of countries, for good reason, because it costs you a lot of money. And I think certain parts of this circus is the same. But it’s very tough to regulate, and I’m not saying you should. But it could cost a lot of people a lot of money.

I feel very strongly about this. I’m not saying edge doesn’t exist. I’m saying it’s really hard to have it. And you’ve got to be clear in your head why you do, and what your edge is.

Michael: I have not read [Kroijer’s previous book] Money Mavericks but give me a preview so when I do read it, what am I going to get?

Lars: It’s a very different book. Money Mavericks is essentially the book of how someone with my background, a regular kid from Denmark ends up starting and running a hedge fund in London, and all the trials and tribulations, humiliations and all that you go through in that process. I thought when I wrote it lots of things have been written about hedge funds, and a lot of it’s wrong. Namely this whole idea that we’ll all drive Ferraris and date Playboy Bunnies and do lots of cocaine.

I thought very little was written from a first-hand perspective, someone who’s actually set up a fund and gone through the fund raising and trying to put together a team. And the humbling failures, and successes, so I thought let me try to write that. I did. I found myself enjoying the process of writing it, which I guess was part of the reason I did it. But then it got published, and it ended up doing really well.

I was actually kind of pleased about that because I thought it’s very nonsensationalist. We didn’t make billions, we didn’t lose billions. No one defrauded us and we didn’t defraud anyone. So those are the four things you normally think about when you think of hedge funds.

Michael: If you’re trying to sell books, yes.

Lars: Yeah, so this is none of that. It’s just a story of some guy starting a hedge fund, how it all worked out, all the little anecdotes. I was really pleased that resonated. In fact, the best feedback I got was from people in the industry who were like yeah, that’s exactly what it was like. I’m sure you would appreciate it because you’d have lived a lot of it. Begging for money.

Michael: No, that’s my second [imaginary] book. My first [imaginary] book is personal finance. My second book is gonna be that experience, your books in reverse.

Lars: I think you’d enjoy it. That resonates with a lot of people, including what you also would’ve experienced, this whole undertone of anyone can start a hedge fund; I’m going to quit my job and raise 50 million dollars. I’m going to build a track record and then raise another couple of hundred million. Then I’m going to be rich and happy. The number of times I’ve heard some version of that makes me want to puke. When you’re actually doing it you realize how incredibly hard it is.

Michael: Very stressful.

Lars: It impacts your health, your life, your family, all of that. Then that’s before you try to make or lose money.

Michael: You actually have to do it, get a return that people are happy with, and they’re happy to stick with you. Does your fund exist still?

Lars: No, it’s just my own money. I had incredibly fortuitous timing. I returned all capital in early ’08. But no skill, it was for mainly my own reasons, sanity, health, and family. I’ve been lucky.

Michael: As we always say better lucky than good. That’s more important.

Lars: For me there was a big part of that. I thought let’s quit while you’re ahead. To be honest, I have yet to wake up one day where I miss it. I get to wake up one morning where I wish I was heading to Mayfair to turn on to Bloomberg and be at it.

On the other hand, from an industry (sales-driven) perspective, load funds are great. Makes the salesperson rich at the direct expense of the investor.

On the other hand, from an industry (sales-driven) perspective, load funds are great. Makes the salesperson rich at the direct expense of the investor.