Rather than say, “this is how you should invest,” I prefer to say (and write about) “this is how you should NOT invest.”

I can think of at least three reasons for my preference.

First, I know many more terrible ways to invest than I know good ways.

Second, exotic bad ideas make for more interesting conversation (and reading) than boring good ideas.

Third, by focusing on the negative exhortation, I safely hide behind the critic’s shaming attack of “You didn’t do THAT did you?” rather than the advisor’s defensive apology, “I’m sorry I suggested you do THAT and it didn’t work out. But hey! The theory was solid!”

This is all a lead-in before I poke my head out of my turtle shell to give positive advice about how you should invest, before I quickly return to my more comfortable space of how not to invest.

How to Invest

Are you ready for the most important, boring, good idea on how to invest?

You should invest via dollar-cost averaging in no-load, low-cost, diversified, 100 percent equity index mutual funds, and never sell. Ninety-five percent of you should do that, 95 percent of the time, with 95 percent of your investible assets.

Phew, I said it. That paragraph right there is a trillion dollar financial advisory industry sliced, diced, chopped, shredded, sautéed, and reduced to two sentences, and served on a beautiful platter for you. If you don’t understand all the words, don’t worry, just print them out, bring them to your financial advisor and demand only that. Every time he tries to deviate from that plan, just point back to those two sentences and say, “I want only this.”

You’re welcome.

How Not To Invest

Ok, now let me retreat to my more comfortable critic’s shell and tell you how – given that central piece of advice – you should NOT invest.

You should not invest your money for less than 5 years. When I say ‘invest,’ I don’t mean buy some investment product with a view to selling it the next day, the next month, or even next year. I think five years is kind of the minimum investment horizon I’d endorse. Also, when investing, the best time horizon for selling is ‘never.’

You should not invest in ‘safe’ products, like money markets and bank CDs, annuities and bonds. Since this contradicts most of what the banking and financial industry advocates, perhaps I should clarify this point. Money markets and banks CDs work wonderfully for saving money – to buy a fancy new pantsuit or a personal robot, for example, or some other essential purchase. Unfortunately, saving money offers almost no return on your money, and often a negative real return after taking into account taxes and inflation. Saving money is not the same as investing money. Annuities and bonds offer a wonderful psychological feeling of comfort. But that comfortable feeling is also not the same thing as investing. Parking money – when you can’t afford to lose any principal – is different from investing money. Investing money always involves the possibility of loss. Incidentally, I know your investment account is currently allocated to 60 percent stocks and 40 percent bonds (because everybody’s is.) I’m not your investment advisor, you’re not paying me one way or the other, so I don’t really care, but I’ll just point out that 40 percent of your investment account is poorly allocated.

You should not invest in funds without checking the cost of the fund. Most of us would not dream of buying an ice cream sandwich at the Dollar Store without verifying its price first. I mean, I’ll take it out of the freezer and bring it to the cashier without knowing the price (maybe!) but I’m not too ashamed to ask ‘Hey, by the way, how much is this thing?’ (Although admittedly there are some things I wouldn’t do for a Klondike bar.) Can we have a show of hands from mutual fund investors who know the cost of the funds they bought? In my anecdotal experience, not even one in three investors knows the management fees of their funds. People who have worked in the finance industry usually know enough to ask, but even there I don’t think even one in two bothers to check ahead of time. FYI, it’s costing you a lot more than the price of an ice cream sandwich.

Speaking of upfront payments, there is absolutely no reason to pay upfront fees for a fund, known as the fund’s ‘sales load.’ No reason at all. Do not do this. Oh, you didn’t know how much you’re paying in ‘sales load?’ See rule number 3.

Don’t time the market. If you have investible assets ready to go right now into the market, just put them in the market, and forget what I wrote above about dollar-cost averaging. If, instead, you invest based on your monthly surplus, just set up autopilot investing from your paycheck or bank account and never alter that based on ‘timing’ concerns. There’s never a good time or bad time to be in the market. I mean, obviously there is, but there’s absolutely no reliable way you’ll know it ahead of time.1 Every academic study ever done concludes the same way: Timing is a mug’s game. You can’t win that way.

If you’re not a financial professional, try not to spend too much time, energy, or brain space on this investing task. Simplicity and modesty can actually put you way ahead of the pros trying to do fancy things with their investment portfolios. Most of the exotic products don’t work better than the simple products, but they do tend to cost more, and they tend to go wrong in unexpected ways, at the most inopportune times. Keep it simple, smarty.

So that’s about it. If that all doesn’t work out for you, I’m sorry. But hey! The theory was solid.

Malkiel’s central thesis – that equity markets are so efficient at pricing stocks relative to their risk that the vast majority of investors would do best to buy an index mutual fund rather than invest in individual stocks or buy an actively managed mutual fund – has utterly demolished the other side in the battle of investment ideas, even if the war of investment ideas rages on in the world, oblivious to the total intellectual victory of one side.

Since a majority of individual equity investors – in addition to institutional investors – do not yet embrace in practice the Random Walk’s Efficient Market Hypothesis, more should probably read this book to realize that the battle has already been decided.

Lately it does feel as if the tide is turning – as both more individuals and more institutions realize that although some individuals and some managers may ‘beat the market’ some of the time, few managers beat the market often enough to justify their fees. And further, that even if some managers did regularly beat the market in the past, it’s quite difficult to know in advance which ones will beat the market in the future. The resulting logical choice that more and more people make – despite the extraordinary marketing efforts of the Financial Infotainment Industrial Complex – is to purchase index funds.

A Random Walk‘s impact

How important is Burton Malkiel and his book? One measure of his book’s impact is the index mutual fund industry.

At the publication of the first edition of A Random Walk in 1973, the ‘index fund’ did not yet exist, and instead was something Malkiel mused about:

“What we need is a no-load, minimum management-fee mutual fund that simply buys the hundreds of stocks making up the broad stock-market averages and does no trading from security to security in an attempt to catch the winners. Whenever below-average performance on the part of any mutual fund is noticed, fund spokesmen are quick to point out, ‘You can’t buy the averages.’ Its time the public could”

Shortly thereafter, John Bogle at Vanguard proposed the creation of the S&P 500 index, which became available to the general public in 1976. Malkiel became a director at Vanguard fund and may take considerable credit for the intellectual authorship of this superior idea.

The Tide is Turning

After reading Malkiel’s A Random Walk, I was fascinated to learn about the following shifts in the mutual fund landscape in favor of indexing:

For eight years in a row leading up to 2013, domestic (US) actively managed equity funds experienced net outflows, while domestic index funds experienced inflows.

Steady Growth of Index Fund Investing. Source: icifactbook.org

Of the $167 Billion in net new money invested in mutual funds1 in 2013, $114 Billion went to index mutual funds.

As a result of these trends, equity index funds, as a share of all equity mutual funds, has hit a high of 18.4% in 2013, up in a steady increase almost every year from just 9.5% in 2000.

Malkiel’s book does not explain all of this shift, nor did it cause it, but it has provided the popular intellectual justification behind the investment of hundreds of Billions of dollars per year. That’s a pretty cool legacy that should at least be added to his Wikipedia page or something.

Great writing

Malkiel carefully navigates that difficult ridge line between technical writing that includes academic research, including probabilities and statistical methods, and fundamental security analysis – upon which he bases his ideas – and popular interpretations and advice for the average investor.

While stock prices may be random, his writing is anything but random. He’s careful and logical and subtly funny too.

I expected the academic case for the Efficient Market Hypothesis – for which A Random Walk is most famous – but I am pleasantly surprised at how practical, accessible and prescriptive the rest of the book is on constructing an individual’s investment portfolio.

How to value stocks – two ways

Malkiel posits two ways to determine the value for any stock.

In plainest terms, you have to determine all of the future cash flows of a security, and then apply the discounted cash flows formula to determine the present value of all future cash flows. The sum of all discounted cash flows equals the fundamental value of a security.

The great thing about this technique is that you can know the actual worth of a stock, for example.2

Furthermore, asset prices periodically revert back to fundamental values, so if you can do this technique you can know in a sense where prices are headed, at some point in the future.

Many investors – including probably the majority of mutual fund portfolio managers, Wall Street analysts, and stock-picking hedge fund managers – employ fundamental valuation techniques when selecting stocks. Certain bottom-up investors, also known as value investors, believe that they can achieve impressive results using fundamental valuation techniques.

This guy has practiced fundamental investing pretty successfully

Graham’s most famous student Warren Buffet seems to have done pretty well using this technique.

The terrible thing about this technique is that:

a) Its incredibly hard – ok it’s impossible – to actually know what all future cash flows of a stock will be – so we end up adopting models of the future that include substantial guesswork about earnings growth (or shrinkage);

b) The appropriate mathematical discount rate for determining the present value of all future cash flows is also always an estimate, introducing a further element of imprecision to what appeared at first to be a precise process, and;

c) Market prices can remain widely divergent – above and below – from fundamental value for long periods of time. “The market can remain irrational longer than you can remain solvent” is an old Wall Street phrase that captures just this type of problem with fundamental analysis. It’s an unfortunate but true statement that sentiment and irrational factors – the eternal struggle between fear and greed – and technical factors such as the ebb and flow of investment funds – can set the price of stocks far away from fundamental value for long periods of time.

So fundamental value techniques, explained by Malkiel as well as critiqued by Malkiel, are a commonly used technique but not a panacea for stock market investing.

Investor Sentiment – Malkiel credits Economist John Maynard Keynes as an early proponent of the truism that the combined madness and wisdom crowds – also known as investor sentiment – can carry along the price of individual stocks as well as the general level of the market, irrespective of fundamental value. Believers in the theory of investor sentiment may invest with the idea that they can anticipate future interest in a stock or in the market by understanding investing crowd psychology.

When it comes time to sell, the price of a stock will be buoyed by other believers in the ‘story’ of the stock or the market, willing to buy in at the same or higher prices. Even for fundamental value investors, an owner in equities has to depend to some extent on the future participation of others in order to receive value in the secondary market for any shares sold.

This is sometime described by the shorthand phrase ‘The Greater Fool’ theory of investing. Meaning, I don’t necessarily need to know anything about a stock’s fundamentals as long as a Greater Fool than me is willing to buy my shares when I want to sell.

The great thing about ‘investor sentiment’ investing – which by the way I would posit 99.5% of all individual investors depend on much more than fundamental value investing – is that you don’t need to do much homework or heavy math. Just get a ‘feel’ for the direction of the market or the ‘story’ of the stock, and away you go. Again, this is basically how everyone invests in stocks in practice.

I mean, do you know any non-professional stock investors who model out all future cash flows and then apply an appropriate discount to obtain a present value? No? Me neither.

The problem with investing largely on this theory, however, should be obvious for a number of reasons:

a) While irrational exuberance (and its evil twin “irrational lugubriousness”3) can dominate for some time, it’s a ridiculously blind way to invest. We all do it of course, but we’re blind. And we should acknowledge our blindness in advance.

b) Bubbles grow out of Greater Fool theory investing, and the end of bubbles is always ugly and painful.

c) Sentiment can and does change much faster than fundamentals, adding unwarranted volatility to markets as well as possibly to unwarranted activity in our own investing. We humans change our minds twice a day before breakfast and four times on Thursdays. That kind of volatility of sentiment tends to hurt our investment portfolios.

Financial bubbles arise from ‘investor sentiment’ investing

So which way of investing is right? Neither!

As investors we often adhere – at least in theory – to one of these two methods.4 But neither tends to serve us well, or well enough, to achieve an edge over any other investors.

Malkiel advances the Solomonaic wisdom5 that both theories are right, and both are wrong.

Certainly both fundamental value and investor sentiment do determine market prices in a confusing, seemingly random, combination. The problem is that with most stocks we compete with hundreds, thousands, or tens of thousands of extremely smart and knowledgeable investors. With so much competition to achieve the best returns for our capital, we rarely have the chance to outguess others in a profitable way.

We try and try, but as Malkiel’s and others’ academic research has shown, precious few professionals can achieve a better result than the market as a whole. As individuals we have even less chance to outperform than the professionals.

‘Tis The Gift To Be Simple

Malkiel’s famous conclusion in A Random Walk is that most people would do best by trying to simply earn the market returns of the broad market – rather than attempt vainly to ‘beat’ the market.

As the old Shaker dance goes, ‘tis the gift to be simple, ‘tis a gift to be free. The modest, simple, low-cost index fund beats managed funds most of the time, and it also beats an overwhelming majority of actively managed funds over extended periods of time.

Since all mutual funds in aggregate are made up of the entire market, logically the aggregate returns of all mutual funds will reflect the aggregate returns of the entire market. Roughly half will ‘beat the market’ in any given year, and roughly half will underperform the market. However, past performance – as the clichéd disclosure goes – does not predict future results.

With each successive year you compare actively managed mutual funds to market returns, fewer and fewer actually ‘beat the market.’

In practice this is what academic studies confirm, except for the fact that actively managed mutual funds tend to lag, in aggregate, market returns by approximately the fees they charge. Which fees tend to range from 0.75 to 1.5% of assets.

Index mutual funds by contrast tend to charge 0.1% to 0.35% fees and so tend to underperform their respective markets by a much smaller amount.

Forty years later, hundreds of billions of dollars flow into index mutual funds annually, in large part due to Malkiel’s popular presentation of these simple ideas.

Final thoughts and caveats on index investing

S&P500 not entirely diversified

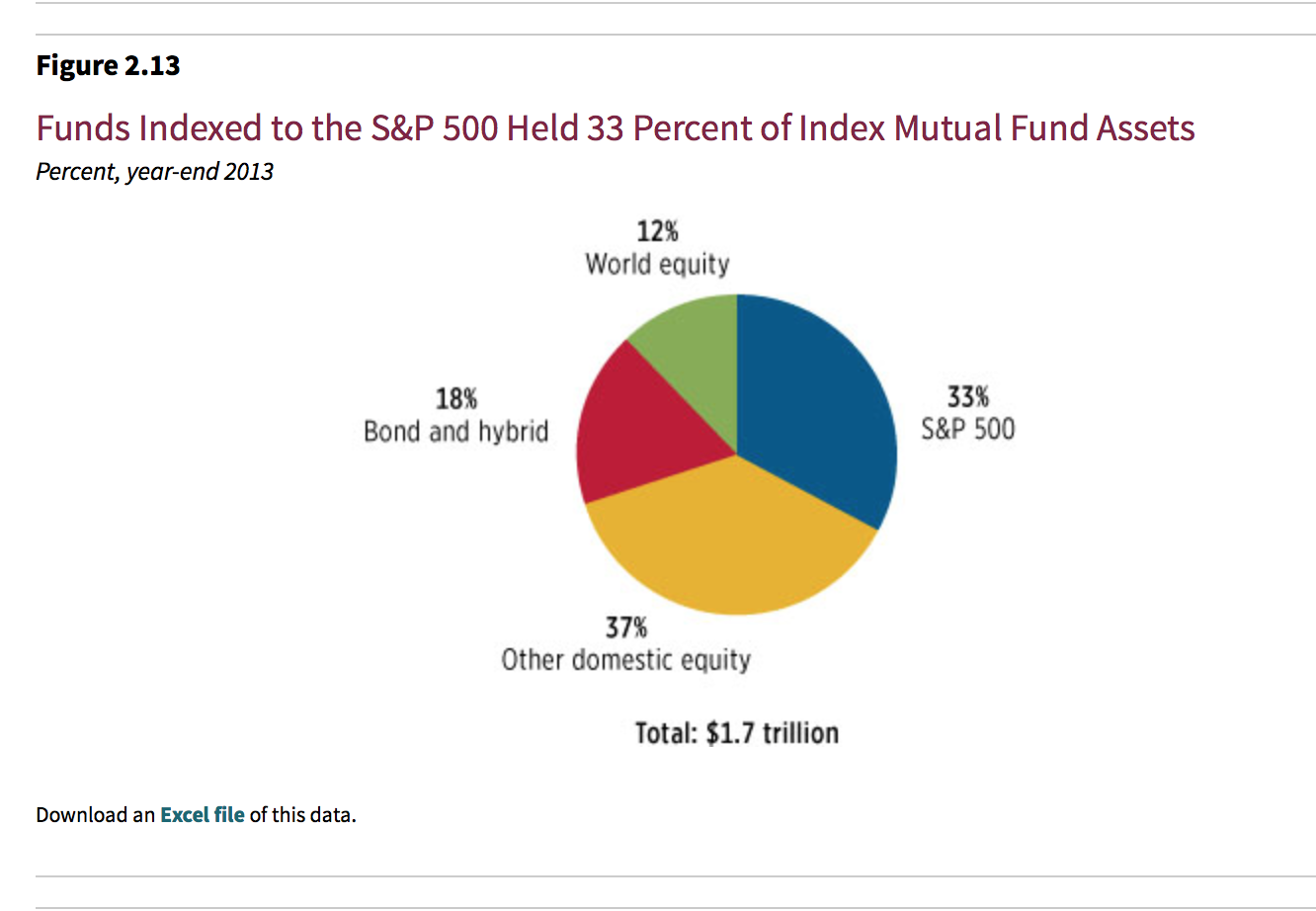

About one third of all indexed investment money currently resides in S&P 500 index mutual funds. The S&P 500 Index consists of the largest 500 US companies, which make up 75% of total stock market value in the United States. As such, this index serves pretty well as a proxy for market exposure, but investors should understand that it consists of only large companies and only US-based companies.

S&P500 share of Index Funds. Source: ICIFactbook.org

Investors in the most popular index fund do not get the diversification of ‘mid-cap’ or ‘small cap’ companies, many of which may ‘beat the market’ in any given year or even long period of years. Furthermore, some research suggests that smaller capitalization stocks may outperform larger capitalization stocks in the long run. This may be because smaller companies appropriately offer higher returns because they are smaller and possibly inherently riskier. I don’t think the research is definitive on this point, but at the very least investors in the S&P 500 should know that they’re only getting exposure to 75% of the US stock market, and only the biggest companies.

Perhaps more importantly, investors in the S&P500 index forgo exposure to the majority of public companies – approximately 60% – that are not listed on the US stock exchanges. S&P500 index investors miss direct exposure to the public companies of Europe, Japan, Australia, Africa, Latin America, China, and India – any of which may ‘beat the market’ represented by large cap US companies. Of course, equity markets are linked and responsive to one another, and the largest US public companies have extraordinary exposure to non-US growth, but the effects are indirect. S&P 500 index investors should know they are not as geographically diverse as they could, and probably should be.

Author Lars Kroijer argues in his book Investing Demystified, persuasively I think, that the logical approach for someone who embraces the Efficient Market Hypothesis of A Random Walk is to invest in an ‘all world equities’ index. This product exists, and offers a cheap, maximally diversified way to wholly embrace Malkiel’s approach.

Market-weighting indexes have drawbacks

The next problem with the S&P 500 index is that it is designed as a market-weighted index, meaning investors get their money allocated to the component stocks of the index in their current market-capitalizations proportion.

Here’s the problem with that. If Apple Inc makes up 3% of the S&P 500 index, and investor sentiment pushes up the value of Apple shares when the iShoe gets announced, such that the weighting of Apple becomes 3.1% of the largest 500 companies in the US, then index funds are forced to buy more Apple, to remain in line with market-weightings.

Admit it. You would totally buy the iShoe

This type of forced buying acts to further push up shares of Apple. A self-reinforcing market mechanism – when buying forces more buying – creates a troubling feedback loop that probably pushes the stock away from fundamental value and possibly creates opportunities for non-indexed money to take advantage of index money.

Its not terribly hard to see how the largest capitalization stocks could be pushed to prices higher than fundamentally warranted as a result of too much S&P 500 index money for example, which would tend to dampen returns for investors in the largest capitalization stocks.6

As Malkiel describes repeatedly throughout A Random Walk, certain smart investments cease to be as smart when everybody does them. The success of the S&P 500 index mutual funds in particular may make future investing in the S&P 500 index less attractive for the purposes of achieving broad market returns.

Defined by the report as “new fund sales less redemptions combined with net exchanges” ↩

Or annuities, private companies, bonds, longevity insurance, oil and gas leases, or income-generating real estate. If a financial instrument has cash flow, this is the way to value it. By the way, as a side note, how do I know gold isn’t a real investment? No cash flow. ↩

Thank you. Thank you very much. In the future, when I am Fed Chairman, I will just whip that phrase out during a Great Recession to show how the market is excessively pessimistic and stocks are about to soar. Then later I will have it trademarked. Who wouldn’t buy my next book titled ‘irrational lugubriousness?’ It has a nice ring to it. ↩

In practice, as I mentioned before, 99.5% of all individuals just punt with the investor sentiment method. ↩

By that I mean: Split the baby in half, leaving nobody happy. ↩

That, Alanis, is a much better example of irony than the proverbial black fly in the Chardonnay, which is really just an example of something that’s kind of a bummer. ↩

The only “C” I got in college was in Intermediate Macroeconomics, but I remember one economics term that I really loved — the “Giffen Good.”

With ordinary, rational, economic behavior, we expect that when prices go up, people buy less, and when prices go down, people buy more. We buy more things, for example, at Wal-Mart and Costco because of their low prices. We buy fewer things at Nordstrom because of their higher prices. Makes sense, right?

Sir Robert Giffen

A Giffen Good — named for a 19th Century Scottish economist named Sir Robert Giffen — is an odd thing. It’s something that people buy more of as the price goes up. With a Giffen Good, people act in exactly the opposite way we would normally expect them to in response to the price of things.

When you look up Giffen Good in Wikipedia — as I just did to refresh my memory — you read that little evidence exists for Giffen Goods in the real world, and people do not generally purchase more of something when the price goes up.

When it comes to our investments, however, I totally disagree with Wikipedia.

Ever since learning about Giffen Goods, I see them everywhere, as well as what’s known by analogy as “Giffen Behavior.”

Outside of the investing world, I remember reading with much interest the story of a guy trying to get rid of his mattress. He posted a “Free Mattress, Used” notice on Craig’s List, and got no responses. When he posted “Mattress, used, just $10,” he had to turn away interested buyers who lined up with their trucks to try to take advantage of a great bargain. That’s a Giffen Good.

Here’s an example of a Giffen Good from the art world: Imagine if I landed on Earth knowing nothing about art and somebody offered me the Edvard Munch painting “The Scream” for $1,000 to hang in my living room.

I’d offer you $75 for this, because I love a bargain.

I don’t know about you, but I might just think, “Whoa, that’s kind of a lot of money, and although there’s something neat about the painting, it’s still a bit creepy.”

And then I might think, “How about I give you $75 for it?” Because I love a bargain.

Of course, knowing that somebody else paid $120 million for it last year changes its attractiveness to me. Would I sell every single one of my worldly possessions right now to own “The Scream?”

Duh. I’m a finance guy. Of course I would. That painting is the ultimate Giffen Good.

Shifting from the absurd to the irrelevant, a concept like Bitcoin suddenly became everybody’s most desired tulip bulb last year when the price starting shooting upward, making it the Giffen Good of 2013.

And now lets return to the core of ordinary investment behavior: Discretionarily-managed equity mutual funds typically charge 0.75 to 1.5 percent management fees, while equity index mutual funds typically charge one-third of that amount in management fees, despite offering the same long-term results, according to every academic study that’s ever been done. Like, ever.

Most investors figure — wrongly — that if the fees on the discretionarily managed equity funds are higher, they must be a better product. The lower-priced index mutual funds just seem less attractive. That’s a Giffen Good.

In fact, much of the time, the entire stock market is an example of a Giffen Good. We really don’t want to own stocks when they fall in price. On the other hand, we really, really, really get interested in stocks after they’ve jumped 10 to 15 percent a year for a couple years in a row. This is madness, of course, but it’s also exactly what drives much investing activity.

Most of the time, indexing wins

Beware of your own Giffen Behavior.

Final note: Real, live economists reading this may object to my imprecise adaptation of an economic term for the popular illustration of a personal finance concept. In anticipation of their objection, I can only show them my previously mentioned “C” on my college transcript. Also, lighten up, dismal scientists.

My morning commute this summer means driving the two young lovelies to their respective kid camps. I like driving in heavy traffic as much as I enjoy hauling over-heated kitchen garbage out to the brown bin in the garage in August. Which is to say, I often have my crinkled-nose sad face on when commuting.

One benefit of being stuck in 8 a.m. traffic headed north on U.S. 281, however, is the chance to reflect on my favorite analogy about investment fund fees and risky markets.

Picture me in traffic, in my dark red — although for my own pretentious reasons I insist friends refer to the color of my car as “Crimson” — Hyundai Elantra. This hot number accelerates from O to 60 in just under 4.3 minutes.

So we’re crawling along around 3 miles per hour, and I glance over my left shoulder at the electric blue Corvette next to me.

A key fact to know, which hardly needs spelling out, is that the owner of that pretty blue Corvette paid approximately three and a half times what I paid for my Hyundai.

I exchange a “Whaddyaknow?” grimace in solidarity with the middle-aged man behind the wheel of his sports car, since we’re both stuck behind a few miles of bumper-to-bumper commuters.

My investment fund fees analogy hinges on the key fact that my crimson Hyundai and my buddy-in-traffic’s electric blue Corvette are in the process of accomplishing exactly the same thing, despite an obvious difference in price — and an obvious difference in status.

Shiny, fast, and expensive!

Because both of us are moving nowhere fast.

Now, here’s my great traffic and investment fund analogy in full:

With your investments, your primary goal is to get from point A to point B. Specifically, to turn some amount of money you have today into some larger amount of money in the future.

The speed at which traffic flows is the market returns of any given year.

Sometimes you’ll flow along nicely up 281 at 65 miles an hour with not much traffic. That’s like earning a cool 12 percent from the stock market for the year without breaking a sweat.

On other occasions you’ll ease onto the nearly empty Pickle Parkway — also known as State Highway 130 — and legally cruise at 85 miles an hour. That’s what it feels like to earn 20 percent or more from the stock market.

And then, in the worst times, you’re stuck behind a four-car pileup, sweating and swearing and unable to move or even get off the highway. We had that kind of year in 2008, when everyone in stocks lost about 35 percent.

Here’s where my analogy really kicks in, though. For the vast majority of driving situations, like the vast majority of investing situations, we get what everybody else gets and there’s not much we can do about it.

As my daughters’ pre-school teachers like to remind them: The best (investing) attitude is ‘You get what you get and you don’t get upset.’ Maybe you already know this idea, and you set it to good use when you buy an investment fund. But I know most of us don’t act like we know it.

Practically the entire personal investing industry is built on the false conceit that you, the consumer, can buy a financial vehicle that can go faster than someone else’s vehicle — essentially to “beat the market.” In reality, that’s incredibly rare.

Without breaking the law, heading onto the shoulder lane or driving recklessly at an elevated risk of hurting yourself or others, you cannot generally beat the rate of traffic, whether you drive an electric blue Corvette or a crimson Hyundai Elantra.

And the same goes for investment funds. You can pay more for a mutual fund or hedge fund, but almost none of them reliably “beat the market.” Every rigorous academic study of financial funds ever done concludes this way: The difference in market returns between high-cost and low-cost funds is, in aggregate, the cost of the funds’ management fee. The difference in market returns, in aggregate, favors the low-cost fund.

Traditional mutual funds charge between 0.75 percent and 1.5 percent management fees, or between $750 and $1,500 per $100,000 investment per year. If you buy an index fund — the Hyundai Elantras of the investment world — you will pay between 0.1 percent and 0.5 percent management fees, or $100 to $500 per $100,000 in the account.

The entire financial industry would like you to think that the extra cost buys you something, but I’m here to tell you the straight fact that you’re paying three and a half times more to get exactly the same investment performance.

Editor’s Note: Author and recovering hedge funder Lars Kroijer provided this guest-post, making the case that most of us would be better off acknowledging we do not have an edge over markets. Most of us can’t consistently “beat the market,” but many of us pay a lot in fees to try.

Edge over the markets, do you have it, and the 7 Porsche cars it may cost you to find out

by Lars Kroijer

Most literature or media on finance today tells us how to make money. We are bombarded with stock tips about the next Apple or Google, read articles on how India or biotech investing are the next hot thing, or told how some star investment manager’s outstanding performance is set to continue. The implicit message is that only the uninformed few fail to heed this advice and those that do end up poorer as a result. We wouldn’t want that to be us!

What if we started with a very different premise? The premise that markets are actually quite efficient. Even if some people are able to outperform the markets, most people are not among them. In financial jargon, most people do not have edge over the financial markets, which is to say that they can’t perform better than the financial market through active selection of investments different from that made by the market. Embracing and understanding this absence of edge as an investor is a key premise of the investment methods suggested in my recent book Investing Demystified (Financial Times Publishing), and something I believe is critical for all investors to understand.

Consider these two investments portfolios:

A) S&P500 Index Tracker Portfolio like an ETF or index fund.

B) A portfolio consisting of a number of stocks from the S&P 500 – any number of stocks from that index that you think will outperform the index. It could be one stock or 499 stocks, or anything in between, or even the 500 stocks weighted differently from the index (which is based on market value weighting).

If you can ensure the consistent outperformance of portfolio B over portfolio A, even after the higher fees and expenses associated with creating portfolio B, you have edge investing in the S&P500. If you can’t, you don’t have edge.

At first glance it may seem easy to have edge in the S&P500. All you have to do is pick a subset of 500 stocks that will do better than the rest, and surely there are a number of predictable duds in there. In fact, all you would have to do is to find one dud, omit that from the rest and you would already be ahead. How hard can that be? Similarly, all you would have to do is to pick one winner and you would also be ahead.

Although the examples in this piece are from the stock market, investors can have edge in virtually any kind of investment all over the world. In fact there are so many different ways to have edge that it may seem like an admission of ignorance to some to renounce all of them. Their gut instinct may tell them that not only do they want to have edge, but the idea of not even trying to gain it is a cheap surrender. They want to take on the markets and outperform as a vindication that they “get it” or are somehow of a superior intellect or street-smart. Whatever works!

The Competition

When considering your edge who is it exactly that you have edge over? The other market participants obviously, but instead of a faceless mass, think about whom they actually are and what knowledge they have and analysis they undertake.

Can you have an edge investing in Microsoft?

Imagine the portfolio manager of the technology focused fund for a highly rated mutual fund / unit trust who like us is looking at Microsoft. Let’s call them Ability Tech and the fund manager Susan.

Susan and Ability have easy access to all the research that is written about Microsoft including the 80 page in-depth reports from research analysts from all the major banks including places like Morgan Stanley or Goldman Sachs that have followed Microsoft and all its competitors since Bill Gates started the business. The analysts know all of the business lines of Microsoft, down to the programmers who write the code to the marketing groups that come up with the great ads. They may have worked at Microsoft or its competitors, and perhaps went to Harvard or Stanford with senior members of the management team. On top of that, the analysts speak frequently with the trading groups of their banks who are among the market leaders in the trading of the Microsoft shares and can see market moves faster and more accurately than almost any trader.

All research analysts will talk to Susan regularly and at great length because of the commissions Ability’s trading generates. Microsoft is a big position for Ability and Susan reads all the reports thoroughly – it’s important to know what the market thinks. Susan enjoys the technical product development aspects of Microsoft and she feels she talks the same language as techies, partly because she knew some of them from when she studied computer science at MIT. But Susan’s somewhat “nerdy” demeanour is balanced out by her “gut feel” colleague, who see bigger picture trends in the technology sector and specifically sees how Microsoft is perceived in the market and ability to respond to a changing business environment.

Susan and her colleagues frequently go to IT conferences and have meetings with senior people from Microsoft and peer companies, and are on first name basis with most of them. Microsoft also arranged for Ability to visit the senior management at offices around the world, both in sales roles and developers, and Susan also talks to some of the leading clients.

Like the research analysts from the banks, Ability has an army of expert PhD’s who study sales trends and spot new potential challenges (they were among the first to spot Facebook and Google). Further, Ability has economists who study the US and global financial system in detail as the world economy will impact the performance of Microsoft. Ability also has mathematicians with trading pattern recognition technology to help with the analysis.

Susan loves reading books about technology and every finance/investing book she can get her hands on, including all the Buffett and value investor books.

Susan and her team know everything there is to know about the stocks she follows (including a few things she probably shouldn’t know, but she keeps that close to her chest), some of which are much smaller and less well researched than Microsoft. She has among the best ratings among fund managers in a couple of the comparison sites, but doesn’t pay too much attention to that. After doing this for over twenty years she knows how quickly things can change and instead focuses on remaining at the top of her game.

Does Susan have edge?

This man appears to have a market edge. He is ridiculously rare.

Do you think you have edge over Susan and the thousands of people like her? If you do, you might be brilliant, arrogant, the next Warren Buffett or George Soros, be lucky, or all of the above. If you don’t, you don’t have edge. Most people don’t. Most people are better off admitting to themselves that once a company is listed on an exchange and has a market price, then we are better off assuming that this is a price that reflects the stock’s true value, incorporating a future positive return for the stock, but also a risk that things don’t go according to plan. So it’s not that all publicly listed companies are good – far from it – but rather that we don’t know better than to assume that their stock prices incorporate an expectation of a fair future return to the shareholders given the risks. We don’t have edge.

When I ran my hedge fund I would always think about the fictitious Susan and Ability. I would think of someone super clever, well connected, product savvy yet street-smart who had been around the block and seen the inside stories of success and failure. And then I would convince myself that we should not be involved in trades unless we clearly thought we had edge over them. It is hard to convince yourself that this is possible, and unfortunately even harder sometimes for it to actually be true.

The costs add up

On average individual investors trying to beat the markets would not systematically pick underperforming stocks – on average they would pick stocks that perform like the overall market. They would have a sub-optimal portfolio that would not be as well diversified, but in my view the main underperformance comes from the costs incurred.

The most obvious cost when you trade a stock is the commission to trade. While that has been lowered dramatically with online trading platforms it is far from the only cost. A few others to consider:

Bid/offer spread

Price impact

Transaction tax

Turnover

Information/research cost

Capital gains tax

Transfer charge

Custody charge

Advisory charge

Your time?

Depending on your circumstances and size of portfolio you may find that it costs more than 1% each time you trade the portfolio (the low fixed online charge per trade is only a small commission percentage if you trade large amounts). This is certainly less than it used to be decades ago, but for someone who is frequently trading their portfolio it will be a major impediment to performance. In addition capital gains taxation tends to be far higher for frequent traders and the “hidden fees” like custody or direct or indirect costs of the research and information gathering come on top. The more this adds up to, the greater the edge someone will have to have to just keep up with the market.

Can trading stocks or FX make you cool like Tom Cruise?

I recently saw a particularly cringe-worthy advertisement where a broker compared trading on their platform to being a fighter pilot, complete with Tom Cruise style Ray-Ban sunglasses and an adoring blonde. I remember thinking “I would love to sell something to whoever falls for that”. The platform makes more money the more frequently you trade, and they obviously think you trade more if you think it’ll make you be like Tom Cruise.

You just have to pick your moment?

Warren Buffett is quoted as saying that “just because markets are efficient most of the time does not mean that they are efficient all of the time”. To quote Buffett in investing is like quoting Tiger Woods in golf. He is a world famous investor with a long history of being right, so we are all bound to feel a little deferential.

Buffett might be right of course. Markets might be perfectly efficient some or even most of the time and horribly inefficient at other times. But how should we mere mortal investors know which is when? Can you predict when these moments of inefficiency occur or recognize them when you see them? Clearly we can’t all see the inefficiencies at the same time or the market impact of many investors trying to do the same thing would rectify any inefficiency in an instant. But can you as an individual investor spot a time of inefficiency?

I think that it is incredibly hard to have edge in the market even occasionally, but that some people have it, even most the time. But you have to be honest with yourself. If you have a long history of picking moments where you spotted a great opportunity, moved in to take advantage of it and then exited with a profit, then you may indeed occasionally have edge. You should use this edge to get rich.

For the sceptics

Some readers will think this is a load of rubbish. It may be that they consider themselves among the sophisticated investors who can outperform the market. You might of course be in the very small minority of people where this is the case, but if you are going to claim edge and actively manage your own portfolio I would encourage you to consider a couple of things:

Be clear about why you have edge to beat the market, and be sure you are not guilty of selective memory. Unlike predicting the winner of Saturday’s football game, predicting that Google was going to double when it later did makes us appear wise and informed, and perhaps we are subconsciously more likely to remember that than when we proclaimed Enron a doubler. Because we add and take money out of our accounts continuously we are unlikely to keep close track of our exact performance and can continue the delusion indefinitely.

Do not trade frequently. If you turn over your portfolio more than once per year you should have a really good reason to do so. The all-in costs of trading are high and greatly reduce long-term returns.

Regardless of whether you have edge or not, be sure to think a lot about risk levels, taxes, liquidity, and how your investment portfolio correlates with the rest of your assets and liabilities.

Do not start panicking if things go against you.

You may decide you have edge in one sector, geography, or asset class. That’s fine. Do exploit this edge, but also make sure it does not lead to undue geographic or sector concentration and invest like someone without edge in the rest of your portfolio.

Continuously reconsider your edge. There is no shame and likely good money in acknowledging that you belong to the vast majority of people that don’t have edge. Investors who initially do well in the markets will often think it was skill rather than luck based on that first experience. Many reconsider later…

The cost of time spent managing the portfolio are individual (we value our time differently) and while some consider it a fun hobby or game akin to betting even, others consider it a chore they would rather avoid. Someone may spend 10 hours “work time” per week on their portfolio which at an “opportunity cost” of time of £50 per hour for 40 weeks/year is £20,000 per year on top of all the other costs discussed. This clearly makes no sense for a £100,000 portfolio, and is too costly even for a £1million portfolio, and on top of all everything else they would benefit from less time spent.

Should we give our money to Susan and Ability?

Going back to the beginning, if you conclude that Susan is as plugged in and informed as anyone could be, why not just give her our money and let her make us rich?

Many investors do give their money to the many Ability Tech type products and Fidelity and its peers continuously develop mutual funds for everything you can imagine. There are funds for industrials, defensive stocks (and defence sector stocks for that matter), gold stocks, oil stocks, telecoms, financials, technology, plus many geographic variations. In my view many investors have become “fund pickers” instead of “stock pickers”. Even today, years after the benefits of index tracking have become clear to many investors there is perhaps £85 invested with managers that try to outperform the index (“active” managers) for every £15 invested in index trackers.

When investors pick from the smorgasbord of tempting-looking funds how do they know which ones are going to outperform going forward?

Is it because they have a feeling that IT stocks will outperform the wider markets?

If so, are you effectively claiming edge by suggesting that you can pick sub-sets of the market that will outperform the wider markets? Consistently picking outperforming sectors would be an amazing skill.

Is it because of Susan’s impressive resume (you think that someone with her impressive background will find a way to outperform the market)?

If so, your edge is essentially saying that you know someone who has edge (Susan), which is really another form of edge? This is the kind of edge many investors into hedge funds claim. They’ll say stuff like “through our painstaking research process we select the few outstanding managers who consistently outperform”. Maybe so, but that is also a case of edge.

Is it because they feel Ability Tech has come up with some magic formula that will ensure their continued outperformance in their funds generally?

There is little data to suggest that that you can objectively pick which mutual funds are going to outperform going forward.

Is it because your financial advisor considers it a sound choice?

First figure out if the advisor has a financial incentive to give you the advice, like a cut of the fees. The world is moving towards greater clarity on how advisors get paid, making it easier to understand if there is a financial incentive to recommend some products – keep in mind that comparison sites also get a cut of the often hefty active manager fees. Now consider if your advisor really has the edge required to make this active choice. Unless she has a long history of getting these calls right I would question if she has the special edge that eludes most (and would she really share this incredibly unique insight if she had it?).

They have done so well in the past?

Countless studies confirm that past performance is a poor predictor of future performance. If life was only so easy – you just pick the winners and away you go…

We are also often driven by the urge to do something proactive to better our investment returns instead of passively standing by. And what better than investing with a strong performing manager from a reputable firm in a hot sector we have researched?

Mutual fund/unit trust charges vary greatly. Some charge up-front fees (though less frequently than in the past), but all charge an annual management fee and expenses (for things like audit, legal, etc.), in addition to the cost of making the investments. The all-in costs span a wide range, but if you assume that a total of 2.5% per year that is probably not too far off. So if someone manages £100 for you, the all-in costs of doing this will amount to approximately £2.5 per year come rain or shine.

If markets are steaming ahead and are up 20%+ every year, paying 1/10th to the well-known steward of your money may seem a fair deal. The trouble is that no markets go up 20% per year every year. We can perhaps expect equity markets to be up 4-5% on average per year above inflation so you need to pick a mutual fund that will outperform the markets by 2% before your costs to be no worse off than if you had picked the index tracking ETF, assuming ETF fees and expenses of 0.5% per year.

You need to be able to pick the best mutual fund out of 10 for it to make sense!

To give an idea of how much the fees impact over time consider the example of investing £100 for 30 years. Suppose the markets return 7% per year (5% real return plus 2% inflation a fairly standard expectation) and the difference becomes all too obvious over time (2% fee disadvantage in this case compared to a tracker fund).

Ability Tech and its many competitors go to great lengths to show their data in the brightest light, but a convincing number of studies show that the average professional investor does not beat the market over time, but in fact underperform by approximately the fees.

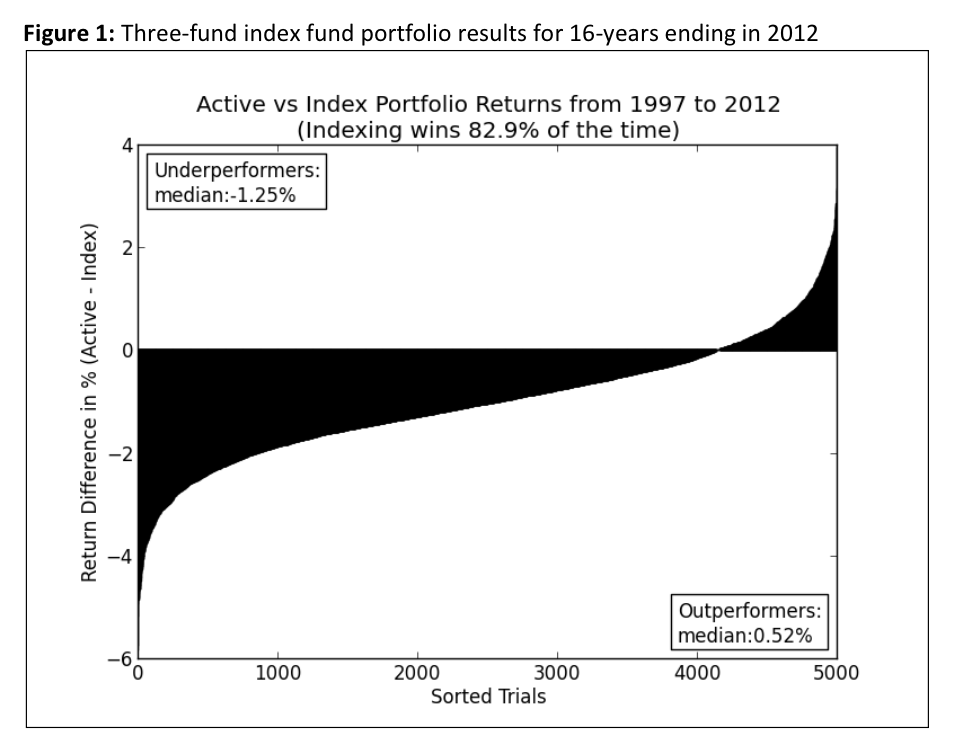

There is of course the possibility that you are somehow able to pick only the best performing funds. Take the example that you had £100 to invest in either an index tracker, or a mutual fund that had a cost disadvantage of 2% per year compared to the tracker. Suppose further that the market made a return of 7% per year for the next ten years, and that the standard deviation (standard measure of risk that gives an idea of the range of returns you can expect and with what frequency) of each mutual fund performance relative to the average mutual fund performance was 5% (the mutual funds predominantly own the same stocks as the index and their performance will be fairly similar as a result).

Comparing an actively managed portfolio to an index tracker is unfortunately not as simple as subtracting 2% from the index tracker to get to the actively managed return. The returns will vary from year to year, and in some years the actively managed fund will outperform the index it is tracking. Some funds will even outperform the index over the ten year period; if you can pick the outperforming fund consistently, you have edge. If you can’t, you should buy the index.

In approximately 90% of the cases in the ten year example above the index tracker would outperform the actively managed mutual fund, which is roughly in line with what historical studies suggest. So in order for it to make sense to pick a mutual fund over the index tracker you have to be able to pick the 10% best performing mutual funds. That would be pretty impressive.

If you did not have edge and blindly picked a mutual fund instead of the index tracker you would on average be about £30 worse off on your £100 investment after ten years because of the higher costs.

The lifetime savings from admitting no ‘edge’ add up to seven porsches

To put in perspective the cumulative impact over a saver’s life consider someone earning £50,000 a year on average between ages 25-67 who puts aside 10% of savings in the equity markets (ignoring tax) – that is roughly what a senior London Underground train driver makes. If equity markets perform similarly to how they have in the past (so about 5% per year above inflation) the average difference in money for the saver at retirement for someone who invested with an active fund manager compared to a product that simply tracks the market will be the equivalent of the value of about 7 Porsche cars (or approximately £280,000 in today’s money). Think about this – a fairly typical saver left poorer by a staggering total amount of money over a life time with the money going to the financial sector. The finance sector won’t like you doing it, but unless you have an amazing ability to pick only the best active fund managers, buy the product that replicates the market and you’ll be much better off in the long run.

While you can bet your bottom dollar that the 10% of mutual funds that outperformed the index would market their special skills in advertisements, historical performance is not only poor predictors of future returns, but it can be very hard to distinguish between what has been chance (luck) and skill (edge). Just like one out of 1024 coin flippers would come up heads 10 flips in a row, some managers would do better simply out of luck. In reality the odds are much worse in the financial markets as fees and costs eat into the returns. However ask the manager who has outperformed five years in a row (every 50th coin flipper…) and she will disagree with the argument that she was just lucky, even as some invariably are. Likewise some managers underperform the market several years in a row simply due to bad luck, but those disappear from the scene and thus introduce a selection bias where only the winners remain. Sometimes this makes the industry appear more successful than it has actually been.

Edge can take many forms

While the discussion above may suggest that having edge involves picking winning stocks or successful active managers only, there are many ways investors implicitly claim edge in their investments, often without having it. Examples include:

Will midcaps outperform large caps?

Will Buffett continue his outperformance?

Will emerging markets outperform developed markets the next decade?

Will tech stocks do better than financial stocks?

Will Germany outperform the UK?

Similarly, the discussion of edge is not exclusive to stock markets. You can have investment edge in many things other than the stock market and profit greatly from that edge. Examples include:

Will Greece default on its loans?

Will the price of oil increase further?

Will the USD/GBP exchange rate reach 2 again?

Will the property market increase/decrease?

Will interest rates remain low?

The list goes on…

Investing without edge

For someone to accept that they don’t have edge is a key “aha” moment in their investing lives, and perhaps without knowing it at first, they will be much better off as a result. At this point you are hopefully at least considering a couple of things:

Edge is hard to achieve and it is important to be realistic about if you have it.

Conceding edge is a sensible and very liberating conclusion for most investors. It makes life lot easier (and wealthier) to acknowledge that you can’t better the aggregate knowledge of a market swamped with thousands of experts that study Microsoft and the wider markets.

Once you have conceded edge you are unfortunately not done. In fact you have only arrived at the starting point and started your journey as an investor who has conceded edge. There is every change that you will be a far wealthier investor as a result of this.

For the edgeless investor it makes sense to pick the most diversified and cheapest portfolio of world equities and combining that with some government and potentially corporate bonds through cheap index tracking products that suit your risk and tax profile. Do this while considering your non-investment assets/liabilities, time horizon of investment, and a few other things, and you are doing extremely well. Once you embrace that you don’t have edge it is fortunately pretty intuitive and really not that difficult to put together a simple and powerful investment portfolio. More on that in the next blog post!

In this discussion with author Lars Kroijer we talk about the main assumption of his book Investing Demystified – which I happen to completely endorse – which is that ‘beating the market’ lies somewhere between highly unlikely and impossible. The goal for individuals should be, instead, to earn market returns. Common behaviors that most investors do, like

1. Paying extra management fees to an active portfolio manager, or

2. Stock picking yourself in order to ‘beat the market’

is a fool’s game, and will ultimately prove unnecessarily costly.

Later in the interview I asked Kroijer to describe his earlier book, Money Mavericks.

Lars: Everyone’s got sort of their angle. My angle is really to start with asking a question of the investor, which is; do you have edge? Are you able to beat the markets? I don’t even make that call for you but I try to illustrate it is incredibly hard to have edge, and that most people have no shot in hell whatsoever of attaining it. Incidentally, that means that people like you are I are not necessarily hypocrites because it’s entirely consistent with our former lives to say we worked in the financial markets; we’ve bought and sold products, and as well informed as anyone. So if we didn’t have edge, edge doesn’t exist.

You could say I’m a hedge-fund manager, and I sold edge for a living, and I certainly thought I had it. But that doesn’t mean that most people, or even that many people have it. I start with the premise in this book of saying do you have it. Then I go on to explain it’s really bloody hard to have it. If you don’t have it, which most people don’t, what should you do?

Essentially, this is a book written for my mom. It kind of is. You wouldn’t believe, but as a former hedge-fund manager, every time I talk to my mom, who’s a retired schoolteacher, she’d always say which stock should I buy. I’d say mom, you could buy an index. And she’s like no, no. Then she’d say stuff like Dansker bonds have done so well, I should be buying it. And I’d be like no, don’t do that. She’s certainly not alone in that position.

Michael: I completely agree with you, and when I think about how your book lays out four simple rules, starting with the one that you should be exposed to the broadest, most global index portfolio, and I have not done that, in terms of I am US-centric and small-caps centric, so I don’t have the broadest exposure. On the other hand, there is no gap between what you advocate, in terms of can you beat the market, and the way in which I invest, which is always I assume from the get-go ‑‑ and this is why that part of it resonated with me ‑‑ so clearly I, like you, say you can’t beat the market. The goal should not be to beat the market. The goal is to expose yourself to the appropriate allocation to risky markets, appropriate to your own personal situation. And then get the market return.

Lars: You want to capture the equity-risk premium.

Michael: The entire finance-marketing machine is about can you beat the market. Beating the market is a complete fool’s game. I think it’s particularly interesting, the other reason I wanted to talk to you, is because you’ve worked in the hedge-fund world, you’ve been a hedge-fund manager, an advisor to hedge funds. I worked on Wall Street. I founded my own fund, and it’s all about that theory that you can, in a sense, have an edge in the market. Yet, the more you know about how it actually works, the more extremely bright people, with the highest powered computing power and the most cutting-edge ideas ‑‑ and you think about the power they had, and we had, and the chances of any retail investor or in fact any of those investors themselves beating the market, or as you say, having edge, is just impossible.

Lars: Add to that they’re at a huge cost disadvantage, informational disadvantage, analytical disadvantage. It’s so unlikely, and this is why always start with you’ve got to convince people they can’t. That’s actually probably the toughest thing. You’re fighting not only against conventional wisdom, but you’re also fighting this almost innate thing we have, that you somehow have to actively do something. You somehow have to pick Google or whatever.

You have to have a view, and you’re smart, you’re educated, doing something to improve your retirement income, or whatever you’re doing. What you and I are advocating is essentially do nothing. Admit you can’t. I think that rubs a lot of people the wrong way.

Michael: You need to bring humility to the situation. I cannot do better than the market. I can do the market but I can’t do better. It’s a very hard, humble approach, but in my opinion and in your opinion it’s the correct approach.

Lars: Yeah. And I also think we’re extremely guilty of selective memory. We remember our winners. That adds to the feeling. It’s a bit like when you ask guys whether they’re an above-average driver. 90% will say they’re above average.

If you ask stock pickers whether they do better than average, 90% of stock pickers would say yes, even more than that. I think there’s a lot of that, a huge degree of selective memory. It’s a shame because I think it really hurts people in the long run.

Michael: It makes conversations along the lines of what you mentioned with your mother conversations with me and other friends and retail investors in stocks ‑‑ hey, I’ve got this great new stock. I’m such a bummer when I talk to them because I say really? I don’t know what to say.

Lars: The alternative is to say you don’t know what you’re talking about, which is not an all together pleasant thing to say. It’s not how you make friends. Certainly not when you’re moving to a new town, like you did.

Michael: I’ve written about this on my site before, but essentially when somebody talks about individual stocks, to me what I’m hearing is I went to Vegas. I put money on 32 and 17 on the roulette wheel. Look how I did. I just don’t know how to respond to that. That’s fabulous, you hit 17 once. I don’t know what to say.

Lars: This is conventional wisdom because to most other people that person will sound smart and educated. They will say here’s why I found this brilliant stock and here’s why it’s going to do great. Most people in the room will consider that person really smart, educated, and someone who’s got it. They’ll sound clever about something we all care about, namely our savings. And you think if I could only have that, I’d want that. It’s tough to go against that.

This is why I think the biggest part of this book is if I could get people to question that. Maybe even accept they can’t beat the market. Then that would be the greatest accomplishment. I think a lot of the rest follows. I haven’t come up with any particularly brilliant theory here. It’s sort of academic theory implemented in the real world and that’s pretty straightforward.

Michael: It cuts against the grain of what I call on my site “Financial Infotainment Industrial Complex,” which is there’s a lot of people invested in the idea that markets can be beaten, that individual investors can play a role.

Lars: Think of how many people would lose their jobs?

Michael: Yeah, it’s an entire machine around this idea. It’s very hard to fight against that. It’s very boring to fight against that. I joked about it in my review; your book is purposefully hey, I have some boring news for you. Here’s the way to get the returns on the market and sleep better at night.

Lars: I sort of compared going to the dentist. You really ought to do it once in a while and think about it. I completely agree with you. I mentioned in the book ‑‑ when I thought about writing this book, it was one of these things that slowly took form, but there’s this ad up for one of these direct-trading platform websites. And there was a guy who was embraced by a very attractive, scantily dressed woman. He was wearing Top Gun sunglasses, with a fighter jet in the background. It said something like “Take control of your stock market picks.”

I thought fuck; are you kidding me? Really? Whoever falls for that, I’d love to sell them something.

Michael: Oh yeah, they’d be a great mark.

Lars: You also hear a lot about the quick trading sort of high-turnover platforms. It’s something like 85-90% of the people on there will lose money. You have a lot of these companies, their clients, 85-90% will lose money.

It’s almost akin to gambling. You can argue is it gambling, which is a regulated industry in a lot of countries, for good reason, because it costs you a lot of money. And I think certain parts of this circus is the same. But it’s very tough to regulate, and I’m not saying you should. But it could cost a lot of people a lot of money.

I feel very strongly about this. I’m not saying edge doesn’t exist. I’m saying it’s really hard to have it. And you’ve got to be clear in your head why you do, and what your edge is.

Michael: I have not read [Kroijer’s previous book] Money Mavericks but give me a preview so when I do read it, what am I going to get?

Lars: It’s a very different book. Money Mavericks is essentially the book of how someone with my background, a regular kid from Denmark ends up starting and running a hedge fund in London, and all the trials and tribulations, humiliations and all that you go through in that process. I thought when I wrote it lots of things have been written about hedge funds, and a lot of it’s wrong. Namely this whole idea that we’ll all drive Ferraris and date Playboy Bunnies and do lots of cocaine.

I thought very little was written from a first-hand perspective, someone who’s actually set up a fund and gone through the fund raising and trying to put together a team. And the humbling failures, and successes, so I thought let me try to write that. I did. I found myself enjoying the process of writing it, which I guess was part of the reason I did it. But then it got published, and it ended up doing really well.

I was actually kind of pleased about that because I thought it’s very nonsensationalist. We didn’t make billions, we didn’t lose billions. No one defrauded us and we didn’t defraud anyone. So those are the four things you normally think about when you think of hedge funds.

Michael: If you’re trying to sell books, yes.

Lars: Yeah, so this is none of that. It’s just a story of some guy starting a hedge fund, how it all worked out, all the little anecdotes. I was really pleased that resonated. In fact, the best feedback I got was from people in the industry who were like yeah, that’s exactly what it was like. I’m sure you would appreciate it because you’d have lived a lot of it. Begging for money.

Michael: No, that’s my second [imaginary] book. My first [imaginary] book is personal finance. My second book is gonna be that experience, your books in reverse.

Lars: I think you’d enjoy it. That resonates with a lot of people, including what you also would’ve experienced, this whole undertone of anyone can start a hedge fund; I’m going to quit my job and raise 50 million dollars. I’m going to build a track record and then raise another couple of hundred million. Then I’m going to be rich and happy. The number of times I’ve heard some version of that makes me want to puke. When you’re actually doing it you realize how incredibly hard it is.

Michael: Very stressful.

Lars: It impacts your health, your life, your family, all of that. Then that’s before you try to make or lose money.

Michael: You actually have to do it, get a return that people are happy with, and they’re happy to stick with you. Does your fund exist still?

Lars: No, it’s just my own money. I had incredibly fortuitous timing. I returned all capital in early ’08. But no skill, it was for mainly my own reasons, sanity, health, and family. I’ve been lucky.

Michael: As we always say better lucky than good. That’s more important.

Lars: For me there was a big part of that. I thought let’s quit while you’re ahead. To be honest, I have yet to wake up one day where I miss it. I get to wake up one morning where I wish I was heading to Mayfair to turn on to Bloomberg and be at it.

Rather than say, “this is how you should invest,” I prefer to say (and write about) “this is how you should NOT invest.”

Rather than say, “this is how you should invest,” I prefer to say (and write about) “this is how you should NOT invest.”