If you face the high-quality problem of finishing your life with too much money, you’ve probably already figured out that three groups, and three groups only, get your surplus: The government, your family, and your preferred charities. Of these, we typically all agree about leaving the lowest legal amount to the government. Then we face tremendous stress about how to allocate our fortune between the other two.

This post not only nudges you toward door number three (your favorite charities!) but advocates a tax-efficient, low-cost way to do it, available to people of even modest means.

But first, the problem of children.

Many choose to prioritize their children or relatives first, which is fine, whatever, it’s your dollar. My own personal starting point about inheritance discussions is this: children do not deserve free money.

However, I realize we’re not going to all agree on that one, and I’m not (yet) in a position to vastly increase federal estate taxes.

Meanwhile, what do people facing a wealth surplus worry about? Merrill Lynch – in a 2015 report titled “How Much Should I Give To My Family? On the Risks and Rewards of Giving ” – found two problems when they surveyed their high net-worth clients. First, 42 percent of respondents plan to pass on their assets only AFTER their death, rather than while they’re alive. Second, more than 60 percent of high net-worth clients worried about the potential negative effects of inherited wealth on their children.

The problem, as Merrill Lynch and other financial advisors will likely agree, is that those findings bump up against two well-known estate-planning principles.

First, giving away money during your lifetime – rather than after your death – is the most efficient way to minimize taxes on transferring your wealth. And 42 percent of Merrill Lynch respondents weren’t planning that. So now all we need is a (tax-efficient, low-cost) way to give money away while you’re still alive. Keep reading.

Second, the key to lowering stress in estate planning is to put your personal values in the center of the plan. More than 60 percent are stressed about the tension between their values and their children’s values, which means they have not sufficiently figured out answers to the questions: What do you believe in? What do you stand for? What people or organizations or values represent the highest expressions of meaning in your life?

If it’s all about your children, cool, give them the money. If you have other values you want to express as well, however, let’s talk about donor-advised funds for a moment.

Donor Advised Funds

What’s the best way to give away money during your lifetime? Although that’s too broad a question, I’m going to opine anyway. A very good way – surprisingly both affordable and flexible – seems to be donor-advised funds (DAF).

You should obviously be cautious when taking tax, legal, and financial advice from someone who writes a blog, but it seems to me a DAF offers tremendous advantages in a simpler – and therefore lower cost – way than a foundation or trust, especially if your estate will not require the Full Monty of intergenerational wealth planning.

Most of the major brokerage houses and investment firms offer donor-advised funds, which appear to a nice, low-cost way to accomplish an expression of your values in your lifetime – and beyond! – without setting up a potentially complicated and expensive legal structure, such as a foundation or trust.

Here are some basics when you contribute to a DAF:

You can enjoy a charitable gift tax benefit in the year of your gift.

Your assets continue to grow in value, tax free, over time.

You don’t have to designate all of your charitable beneficiaries now, because your appointed trustees – such as you and your children – can designate gifts to charities over time.

Giving involves a simple call or note to the brokerage firm, which then confirms the recipient charity is legit. After verifying that, the money for your donation goes out to the charity in just a few days’ time.

Mostly what the DAF gives you, as I view it, is time to enjoy giving while you are still alive. That’s time to make future decisions and hold conversations with your children or other designated trustees about your values. I also like the idea that you get a chance, during your lifetime, to observe and reflect on the effect of your gift. Is the charity actually fulfilling its mission? Is it fulfilling your mission? And then, why not actually get thanked in person, rather than the grimmer path of grateful recipients having to thank a plaque with your name on it?

I looked up three different well-known, name-brand brokerage companies to check out fees and account minimums on their DAFs.

All three charged 0.6% annual fees on DAFs, with reduced fees on accounts over $500,000.

The National Philanthropic Trust reports the average DAF reached $296,701 in 2014. but clearly you can open up one of these funds for far less. Two of the three brokerage firms I looked at offer opening account minimums of $5,000, while a third required a $25,000 minimum.

What that says to me is that tax-advantaged, value-driven charitable giving of your wealth – both in your lifetime and beyond – isn’t something only available to the extremely wealthy. Instead, pretty sophisticated philanthropic vehicles are available to Main Street investors, who just happen to have a little surplus.

You can give your assets to the DAF this year, enjoying all available tax advantages of that gift now, and spend future years giving to worthy causes.

You can do this over time in consultation with your children or designated trustees, affording you the satisfaction of giving, as well as the pleasure of talking about and expressing your highest values.

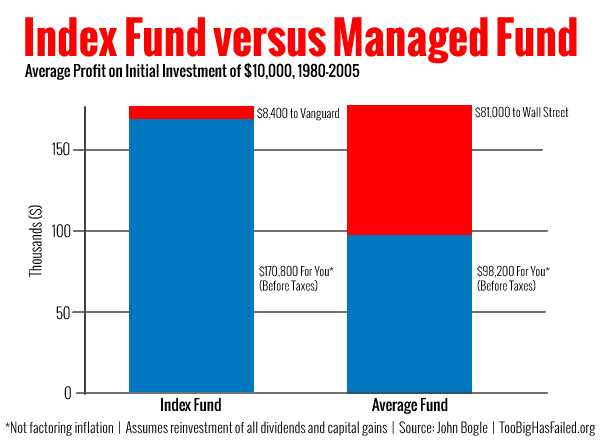

Lately I’ve taken to saying boldly and loudly to anyone who asks my opinion (and some who don’t!) that every academic study ever done on actively managed (high cost) mutual funds vs. passively managed index (low cost) mutual funds shows that, in aggregate, the actively managed funds under-perform the passively managed funds by approximately the difference in fees charged by actively managed funds.

That’s the central and ongoing conclusion of not just the first edition of Burton Malkiel’s A Random Walk Down Wall Street, but every updated edition since the book first appeared in 1973. Although Malkiel’s view has won the academic battle, still the combined marketing heft of the actively managed mutual fund industry has not yet conceded the war.

Investment strategist and and nationally syndicated columnist Scott Burns of Asset Builder – points out in this post yet another important article debunking the usefulness of actively managed mutual funds, when compared to their admittedly doughty but nevertheless more profitable younger siblings, index mutual funds.

If you’re curious to dip your toe into these ideas, I recommend starting with Scott Burns’ post, then move on to the article itself.

As a father of two daughters, I know I’ll never forget certain special times: their birth, Day 1 of Kindergarten, baby’s first piano recital, menacing the punk who is picking her up to go to the prom, and the police report I’ll file when she quits college to run off with the lead singer of that Norse Death Metal Band.[1]

Moments you never forget, like a first stock market investment

Dear readers, that stock market investment moment has arrived, so I thought I would bring you along with us on this beautiful father-daughter bonding journey.Grab your spreadsheets, and your handkerchiefs.

My daughter’s life savings

First, a confession:I am clearly a mean Daddy.

Until last week, my oldest had $370 in her bank account, the sum total of eight years of hoarding cash gifts from Aunts, Uncles, Grandparents, Santa Claus and the Tooth Fairy.In addition to the savings account, she also boasted $31 in cash that she scored at my Sunday evening poker game with the neighborhood dads.[3]

A few months ago I realized – here’s the mean Daddy part – that if she had a total of $500, I could take her hoard and buy some public shares in a custodial account.In that way I could simultaneously:

1.Remove her liquidity/temptation to buy Bratz Dolls (or something equally horrible)

2.Teach her valuable lessons in long-term investing, delayed gratification, and math.

Now, buying shares in public companies ranks #748 in the priority list for what eight year-old girls want to do with their life savings, but again, I am a mean Daddy and that’s the kind of cruelty I subject my daughters to.I’m an ex-banker, what did you expect?

The manipulation begins

I started in on the project a few weeks back.

“Do you know you have about $400 saved up?And do you know what would be fun to do with your money?”

Silence.

“We could pick a stock to buy and then track it in the newspaper, or even online!” I said cheerfully.Perhaps a bit too brightly.

“Okay…” she looks at me, with a healthy dose of mistrust.(I’m so proud of her.)

“So do you want to do that?” Picture me, with a hopeful face.

“Do you remember that plan I had for investing in a stock with your savings?”

“Kinda.”

“Let’s work on that today.”

I explain to her my plan, which is to walk around the kitchen, living room, and her bedroom, picking all the things that are made by big companies.And then from there I’ll have her pick which one would be the coolest company to invest in.

And also, I mumble to her in that fast voice explaining terms and conditions in the final 5 seconds of every car commercial or Levitra advertisement, we’ll need to pick a stock that we can invest in directly through the company, with an automatic dividend reinvestment plan, without having to go through a brokerage company.

Extra incentive

Then I told her if we did my stock investing plan with her $401 in life savings, I would kick in an extra $100, so she could have $500 total to invest in a company.She’s no Warren Buffett (yet) but I think she quickly understand the good deal I was offering.

And I knew that she needed at least $500 to invest in a company the way I preferred, which again was to pick a stock that we can invest directly in through the company, with an automatic dividend reinvestment plan, without having to go through a brokerage company

What we did

That afternoon, we spent 30 minutes with a pen and notebook, walking around the kitchen, living room, and her bedroom.We picked up objects and looked for the names of the companies that produced them.

Here’s what we wrote down:

*Johnson & Johnson – Lotion

*Macys – Couch

*Campbell’s Soup – Can of soup

*Colgate Palmolive – Soap

*Kellogg’s – Cereal

Maytag – Stove

Lakeshore – Wooden toys

*Sony – Stereo

Kenmore – Microwave

Viewsonic – Computer monitor

*Black & Decker – Coffee maker

*Apple – Computer

Bic – Lighter

Bayer – Vitamins

*Hewlett Packard – Printer

*Hasbro – toys

*CVS – Medicine

Morton’s – Salt

Kitchen Aid – Stove

Emerson – Clock radio

Sunbeam Products – Coffee grinder

Lands End – Lunchbox

*Target – Bag

Penguin Publishing – Cookbook

Biersdorf – Aquaphor

Milton-Bradley – Games

*Kimberly Clark – Kleenex

Pampers – Diapers

*Starbucks – Daddy’s coffee

Next, we opened up the Wall Street Journal[4] to the 1,000 largest stocks page, and whittled our list of companies to only those which appeared on this list – a smaller group – which I have identified above with an asterisk before the name.

Old-school stock picking – printed page and magic marker

I prefer her first stock investment to be made with a large, widely-followed company.

Finally, I asked her to choose among the large, public companies which five she felt most kindly toward, or which she thought made great products.

Her List

Her list was as follows:

Kellogg’s (Rice Krispies are loud loud loud!)

Apple (Mommy has an iPad and she is nice!)

Target (Fun shopping trips with Mommy!)

Starbucks (Daddy is an addict and clearly has a problem!)

Campbell’s Soup (Big Warhol fan!)

The final choice – DRIPs

The final choice of which company would get my daughter’s $500 came down to the very particular criteria imposed by Dad.

I wanted to teach my daughter a few key pieces of information about stock investing that I did not learn until relatively late in life. Namely:

1.You don’t have to invest through a brokerage company, but instead you can invest directly with many public companies, bypassing a layer of investment costs.If you are a buy-and-hold investor, this can save you money in fees over time without any inconvenience when it comes to trading – since you won’t be trading much.

2.You can set up a plan with companies to have any dividends directly reinvested in their stock.Traditionally these plans are known as DRIPs (Dividend Reinvestment Plans), and they allow investors to automatically purchase more shares – including fractional shares – with dividends.This is ideal for a kid with a 10-year (at least) investment time horizon, and who will not need to use dividends to cover her cost of living.DRIPs reduce reinvestment risk,[5] and they remove the temptation to spend investment income.In sum, they are awesome for my purposes with my 8 year-old daughter, and they are probably awesome for many adult buy-and-hold investors as well

So, I took the list of 5 preferred companies and looked up on line to see which ones offered DRIPs.

Our search among the 5 preferred companies

It turns out Apple is the least DRIPpy, as their investor relations page says it’s not possible to buy shares directly from the company.That’s fine, and seems like a perfectly reasonable position for the most valuable stock in the world.

Starbucks, Target, and Campbell’s Soup all offer a version of direct purchases from the company plus dividend reinvestment – in fact all via the same company – called Computer Share, which manages DRIPs programs for a number of companies.

I didn’t love the user interface for Computer Share, and each company specifies different terms: different minimum amounts, different costs to purchase, different costs to sell, and different reinvestment programs.

In my search for simplicity for my daughter, this wasn’t it, although I’m sure it’s a fine solution for many folks.

My daughter, admittedly, lost a bit of interest as I surfed the Interwebs reading about different programs for direct stock purchases.After looking over my shoulder for about 3 minutes, she disappeared for the next 30 minutes.She was either playing with her American Girl doll or playing Norse Death Metal Groupie.I’m not sure which.Daddy was busy.

“Aha!I found it!Kellogg’s allows us to invest directly and have automatic reinvestment of dividends, and they have a $500 minimum.So we’re good.So is Kellogg’s ok?”

“Um, ok Daddy, if you say so.”

“See?Isn’t this exciting?I’m excited.”

With her blessing I then took ten minutes online to open up the Custodian Account for a Minor, which involved my social security number, and inputting the bank account from which $500 would be drawn.

With that task completed, I returned to telling her a few things about investing in Kellogg’s stock.

I showed her on that page also that every quarter owners of the stock receive money in the form of dividends.Her dividends would buy more shares over time.

I told her that the total investment value of a company is the number of shares multiplied by the price of shares.I showed her in a spreadsheet how $500 would buy about 8 shares, with the stock price around $60/share.

I told her that her $500 could lose value, but that more often than not, in the long run, it will increase in value.

What I’m not trying to do with this investment

I’m excited about this project – admittedly about 8 times more excited than my daughter – but still this was a wonderful, awful, idea of mine.

But I know that my idea does not teach everything my daughter should know about stock investments.

We had nearly zero discussion about the relative money-making prospects of her first stock purchase.We barely talked about the attractiveness of Kellogg versus other companies – other than the fact that Rice Krispies are a very loud cereal (a big plus in the 8-year-old world) and other companies do not make Rice Krispies. Ultimately, greed can be an important motivator for stock investing, but I decided to downplay that for now.

I’ve told my daughter nothing about value investing vs. growth investing.

I’ve told her nothing about modeling future cash flows to identify the value underpinning her business ownership.

We know nothing about the management of Kellogg’s – for all I know Dennis Rodman is the new Chairman of the Board.

Dennis Rodman and new BFF Kim Jong Un

We didn’t read the latest annual report (although I downloaded it).

I have not exhaustively read the business news on Kellogg’s to help identify with her the known risks and opportunities of the company.

I’ve told my daughter nothing about properly diversifying a stock portfolio.I realize we’ve concentrated 100% of her equity portfolio in a single company, something I would never advocate for an adult.[6]

I’ve shown her, but de-emphasized, the importance of the historical price chart for the company, because it’s frankly not as useful as it appears.

I have not reviewed with her the freaky Black Swan events that can take a perfectly healthy-seeming company with a long history and destroy it quickly, in the process dis-Apparating[7] her $500.

What I am trying to do with this investment

Despite not covering everything, I feel good about four lessons which I have started to teach my daughter.

1. Our relationship to big business and the economy – We buy and use things, every day, made by big public companies.Those companies aren’t monsters. And they’re not the boss of us.If we have savings, we can be the boss of them.[8]

2. Math helps in the real world – Multiplication (a key 8 year-old skill to master) has a practical use in the real world, as do spreadsheets. The total market value of her investment at any time can be calculated by multiplying the share price by the number of shares she owns.

3. Investing money over time is possible, and important.

We can pick which investments to make from a wide variety of choices.It’s possible – although of course not guaranteed – that we can grow money through stock ownership, both when the companies pay dividends as well as when the share price goes up. In the long run, a variety of stock investments could make her money grow.In the short run, and in plenty of cases, she could lose money.

4. When possible, try for as little startup cost as possible

She can start investing her savings in public shares for as little as $500.

She does not need a brokerage company in order to invest in companies, but rather can invest in the companies directly, for about $15 in total cost.

She can set up a system to have regular dividends reinvested in those companies.

For now, that’s enough.

By the time she decides to sell – maybe that will be age 18 when she goes to college and needs spending money, or maybe age 19 when we enroll her in the convent to avoid the Norse Death Metal Singer – I expect we will have covered a few more investment lessons.

Disclosure statement: Other than the $500 Kellogg’s investment described here I have no direct investments in any of these companies mentioned, nor in any death metal bands, Norse or otherwise.

[1] Note: These last two are still in the distant future.My oldest daughter is only eight, thank the Good Lord.

[2] Note: That hasn’t happened yet either, because again, she’s eight.But I get weepy just thinking about what joy that milestone will bring to our family.

[3] Long story, short: She had a few premium hole cards early and a couple of good flops. Admittedly, also there was a little bit of crying when the pressure mounted.

[4] Yes, Daddy is a super-duper dinosaur.I read the Wall Street Journal, print version, every day.In this case though, I think the print version helped because we could physically hunt the page with our magic marker for the names of companies we’d found around the house.So, if your investment strategy involves a magic marker, I recommend a long-standing commitment to print journalism.

[5] Traditionally a bigger risk for bonds – the idea that you can’t invest your investment income at the same expected return as your initial investment – but still an issue for dividend stocks.

[7] She’s a Harry Potter fan, so she could relate to this description of her money.

[8] But listen, kid, don’t get any ideas about being the boss of Daddy, because only Daddy is the boss of Daddy.Doubts about this point are already a looming problem in the household.

If you face the high-quality problem of finishing your life with too much money, you’ve probably already figured out that three groups, and three groups only, get your surplus: The government, your family, and your preferred charities. Of these, we typically all agree about leaving the lowest legal amount to the government. Then we face tremendous stress about how to allocate our fortune between the other two.

If you face the high-quality problem of finishing your life with too much money, you’ve probably already figured out that three groups, and three groups only, get your surplus: The government, your family, and your preferred charities. Of these, we typically all agree about leaving the lowest legal amount to the government. Then we face tremendous stress about how to allocate our fortune between the other two. Second, the key to lowering stress in estate planning is to put your personal values in the center of the plan. More than 60 percent are stressed about the tension between their values and their children’s values, which means they have not sufficiently figured out answers to the questions: What do you believe in? What do you stand for? What people or organizations or values represent the highest expressions of meaning in your life?

Second, the key to lowering stress in estate planning is to put your personal values in the center of the plan. More than 60 percent are stressed about the tension between their values and their children’s values, which means they have not sufficiently figured out answers to the questions: What do you believe in? What do you stand for? What people or organizations or values represent the highest expressions of meaning in your life? Most of the major brokerage houses and investment firms offer donor-advised funds, which appear to a nice, low-cost way to accomplish an expression of your values in your lifetime – and beyond! – without setting up a potentially complicated and expensive legal structure, such as a foundation or trust.

Most of the major brokerage houses and investment firms offer donor-advised funds, which appear to a nice, low-cost way to accomplish an expression of your values in your lifetime – and beyond! – without setting up a potentially complicated and expensive legal structure, such as a foundation or trust. I looked up three different well-known, name-brand brokerage companies to check out fees and account minimums on their DAFs.

I looked up three different well-known, name-brand brokerage companies to check out fees and account minimums on their DAFs.