Stock markets worldwide will drop significantly tomorrow, and throughout the rest of the week, as US and global investors recalibrate their expectations of the United States due to the little-anticipated Donald Trump victory in today’s Presidential election.

Stock Market

From an individual investor perspective, I suddenly have deep regrets about two pieces of 100% rock-solid advice I’ve given out about personal investing in the stock market. The first is that there’s no particular advantage to owning ETFs over mutual funds, since nobody should really need to trade their personal stock holdings in the middle of the day. ETFs allow you to trade at any time when markets are open, whereas mutual fund investors can only trade based on the day’s closing price. But I’ve never believed any individual investor should be in a such a hurry to sell that a mid-day trade is better than an end-of-day trade.

With the victory of Donald Trump, I’m really sad that I have to wait until the end of tomorrow to sell stocks, rather than mid-day.

Implicit in this comment is my second deep regret. My advice has always been the Winston Churchillian rock-solid “Never, never, never never sell.”

But of course now I want to. It will take all my will-power to do nothing, as I watch stock market values plunge tomorrow.

******

In a seemingly unrelated vein, (but is it?) my favorite Tracy Chapman song “Why” goes like this:

“Why do the babies starve when there’s enough food to feed the world?

Why are the missiles called Peacekeepers, when they’re aimed to kill?

Why is a woman still not safe, when she’s in her home?

Love is Hate. War is Peace. No is Yes. We’re all free.”

No Gridlock

It’s both a cliche and a truism that Wall Street prefers gridlock in Washington. Gridlock is predictable. Gridlock is stable. It prevents wild swings in policy. A divided Executive and Legislative branch tempers drastic or rapid change in regulations.

With a newly elected and strongly Republican House and Senate, and Donald Trump appearing to have a “mandate” for his bat-shit crazy ideas, whims, and personal vendettas, who is going to be the check and balance on the worst ideas from that side of the aisle? Like Trump’s fiscal spending plan, for example, estimated by a bipartisan budget group to add $5 Trillion to the federal deficit? Like Trump’s continual threats to unilaterally alter trade agreements or punish our most important trading partners like Mexico and China?

******

Tracy Chapman continues singing in my head:

“But somebody’s gonna have to answer

The time is coming soon

When the blind remove their blinders

And the speechless speak the truth.”

******

US Treasurys

US Treasury bonds typically live in what the kids on the show Stranger Things would call The Upside Down. Meaning, if stocks go down, bonds go up. When stocks go up, bonds can go either sideways or down. And that’s what’s happening with a Trump victory tonight. A huge bond rally is happening right now, overnight, as I type this at midnight on Election night.

But also, this rally in US Treasury is a totally bonkers reaction to a Trump victory, since Trump actually threatened to renegotiate US sovereign debts, if need be. No responsible financial or political US leader has ever made that threat. We’ve never defaulted, or threatened to default. Alexander Hamilton’s lasting contribution1 to our country’s strength is our rock solid credit, ever since 1789. Threatening US Treasury default is the kind of Third-World bush-league bullshit disruption that bond people don’t appreciate, and which I wrote last summer would have unknowable but possibly catastrophic consequences for our country, which actually is heavily indebted but treated like a safe bet in world markets. Until now.

Back to you, Tracy:

“But somebody’s gonna have to answer

The time is coming soon

Amidst all these questions and contradictions

There’re some who seek the truth.

Love is Hate

War is Peace

No is Yes

We’re all Free.”

Why?

Post read (627) times.

Outside of inspiring Ron Chernow and Lin-Manuel Miranda’s book and show, respectively ↩

This Presidential election is absolutely not about economic policy.

To pretend that you’re choosing your presidential candidate in the 2016 election based on economic policy – after this campaign season – is as absurd as claiming you used to purchase Playboy for the articles.

Even so, let’s pretend for a moment that this election was about economic issues. Where do the two major candidates stand?

Trade

First, Trump. Trump introduced himself to the Presidential race in June 2015 by threatening to impose a 35% tax on manufacturing from Mexico. He frequently claims that he would unilaterally renegotiate better trade deals with China, Japan, Saudi Arabia, and Mexico. Although the Republican Party historically has a clearer track record than the Democratic Party of supporting increased international trade, Trump appears somewhat to the left of Bernie Sanders when it comes to trade liberalization. I have the strong impression that he not only does not support international trade, but he also does not really understand how trade agreements work. Trade wars make almost everyone poorer.

Clinton claims to support increased trade, but has chosen to oppose the already-negotiated Trans-Pacific Partnership (TPP), because it might not create jobs, at good wages, while protecting national security. See, again, that’s not how international trade treaties work. Nobody gets a guaranteed job, at a guaranteed “good wage” from a negotiated trade treaty. Some people over time, in fact, lose their jobs or get a worse wage, while other people – like consumers and many business owners – benefit from trade. I think she knows this. Trump appears uninformed, while Clinton appears the opposite of straightforward.

Wall Street

Trump’s stance vis-à-vis Wall Street remains unclear to me. I mean, he’s promised to lower top corporate tax rates from 35 percent to 15 percent, as well as top personal income tax rates to 33 percent, from the current 39.6 percent. That is presumably welcomed in the canyon-lands of lower Manhattan, or wherever executives expect a substantial payday.

In addition, his approach to encouraging economic growth is to roll back or lower government regulations, which might also be welcomed in some parts of Wall Street.

On the other hand, can we be certain he won’t just round up top executives like Jamie Dimon from JP Morgan and Lloyd Blankfein from Goldman Sachs and have them fight – gladiator-style while wearing giant sumo suits – in the middle of Times Square? The winner gets his Wall Street firm automatically nationalized and re-branded “Trump Money,” while the losing executive is drawn-and-quartered by the Budweiser Clydesdales from the 9/11 ad, on live television. Are we sure that won’t happen? Consider the ratings potential! Other than that, I think he’d be fine for Wall Street.

Clinton’s approach, by contrast, appears more predictable. She posits that “Wall Street must work for Main Street,” risky firms must be monitored more closely, and that senior executives must be held responsible for firm losses, each of which might make Wall Street wary of her presidency.

On the other hand, you and I both know what those paid speeches were for. I personally would have no problem getting paid $1.8 million to give 8 boring speeches to Wall Street firms. In fact, I’m just checking my calendar now…Hang on, let’s see, yup, I’m wide open for the next few weeks, so Lloyd, send me a Snap.

Taxes

Speaking of taxes, Trump would repeal the Death Tax, otherwise known as the estate tax, and otherwise known as my favorite tax.

Clinton proposes increasing estate taxes by reverting back to their 2009 level, and increasing taxes on some of the largest estates. I prefer Clinton’s approach, naturally.

Both Clinton and Trump have stated support for eliminating the carried-interest tax break enjoyed by private equity and hedge fund owners, for which I applaud them both. Neither will do it because #campaigncontributions but still, it’s a great thought.

As a side note on taxes: I have zero problem with Trump’s tax return showing nearly a billion dollars in business losses in 1995, which might have relieved him of paying income taxes for the following 15 years or so. I’m sorry to say, Virginia, that the income tax game is a bit rigged in favor of the wealthy. We shouldn’t expect people to pay taxes they don’t legally owe. Trump’s tax-free status is probably entirely legal based on our current tax code, so don’t get mad at him for that.

Energy Policy

Trump proposes a grab-bag of energy-policy liberalization approaches. On his website he announces plans to “rescind all job-destroying Obama executive actions. Mr. Trump will reduce and eliminate all barriers to responsible energy production,” which includes encouraging coal production, and additional oil and gas drilling, in particular on federal lands. It seem plausible to me that this anti-regulation approach would lower the cost of energy for most people and businesses, and thereby provide economic stimulus to the economy.

Clinton has a more mixed approach, which we can intuit from the fact that her official campaign “energy policy” presentation is really expressed in terms of environmental policy, climate change, and an economic safety net for displaced coal workers. As Secretary of State she promoted the “Global Shale Gas Initiative” (read: she promoted fracking), although she has subsequently called for “smart regulations” of the industry in her book Hard Choices. We should probably expect higher energy costs as a result of her administration.

Also, maybe our coastal cities won’t be underwater in twenty years? It’s a trade-off.

Love the gridlock

We have had imperfect candidates for a long time. Often we even elect them to the highest office. So far at least, the inertia of our constitutional system has kept our electoral mistakes manageable. We’ve had a good political run surviving 228 years of imperfect leaders. I’m going to adopt the optimistic view that we’ll survive this next President, and hopefully the next 228 years as well.

The “Washington gridlock” we all claim to hate may be our best insurance against candidates we don’t like. The system, by design, stymies the Executive branch, and that’s a good thing. I’m frightened by this election, but I’m trying to take the long view. I will certainly vote.

Finally, I mentioned Playboy above because economic policy means absolutely nothing this time around.

The centerfold of this campaign has been all about sexual harassment, locker-room talk, “stamina,” testosterone levels, former President Bill Clinton’s womanizing, fat-shaming, and tiny fingers. I suspect we will all vote according to where we stand on these important issues, not the economy.

With Bill Weld (former two-term MA governor) joining the bottom of the Libertarian Party ticket alongside Gary Johnson (former two-term NM governor), I have to say I’m intrigued.

They can count on:

Elected office experience (far more than the presumptive GOP nominee)

Track record (far more, etc)

A decent runway on an issue that some portion of the electorate cares deeply about (pot legalization). They are “on the right side of history,” in terms of what will happen over the next 10 years.

Totally pissed off wings of the major parties, that dislike their respective leaders, opening the way for outsized third-party success in 2016.

I’m not saying they’ll win or anything, or even necessarily gain any electoral college votes, but they could be a significant factor in the election, especially in a number of states. They are worthy of attention and coverage in any case.

One of The Donald’s great strengths is that he latches onto a partial truth – or an unspoken but widely held belief – and then expands upon it for his own purposes. Obviously this can veer into disgusting territory, when it comes to expressing sexually insecure men’s feelings about women, or insecure workers’ feelings about economic threats from China or Mexico. As Matt Taibbi eloquently expressed, he effectively uses this same talent of partial truth-telling to bash government and media elites who do, in fact, disdain, misunderstand, or ignore ‘regular Americans.’ Trump scores these points against Establishment elites because really, we sense some truth in what he says, that others before him won’t say.

Earlier in the week Trump stepped in a pile of it when he expressed truths about US sovereign debt which political leaders cannot openly discuss. Unconstrained by good taste, judicious character, or political consistency – he can pop off in any direction, occasionally hitting on an important point that more people should understand. The Donald said:

“I’ve borrowed knowing that you can pay back with discounts. I’d borrow [as President, on behalf of the US] knowing that if the economy crashed, you could made a deal.”

This is so crazy that he said it – as a person running for President – that you kind of have to laugh at his gall. On the other hand, he’s right. This is what happens when countries borrow too much. And also, we don’t really know – or have any kind of open discussion in this country – about what constitutes too much national borrowing.

Those fingers tho…

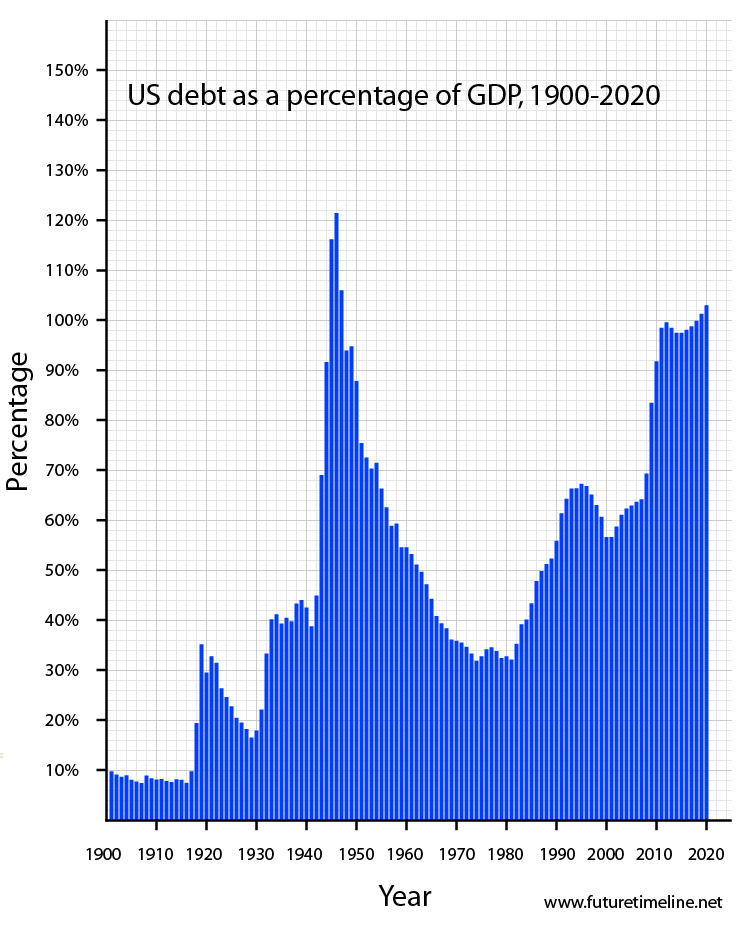

When I worked as an emerging market bond salesman in the late 1990s – slinging bonds from places like Pakistan, Ukraine, Ecuador, Argentina, Russia, and Ivory Coast – we used to put out economic research for our clients that pointed out that a 70% Debt/GDP ratio marked a kind of scary ‘Do Not Cross’ line. If the total amount of sovereign debt exceeded 70% of the economic output of country, you might have to start worrying about whether that country could reliably pay back its bonds. Once you hit 100% Debt/GDP, history seemed to show, emerging market countries would enter a red-zone of risky sovereign renegotiation, or possible default. Their cost of new borrowing would rise, which in turn would hurt their ability to service their existing debt. At between 70% and 100% Debt/GDP, countries could get into a vicious death-spiral of borrowing, ending in sovereign debt restructuring.

At that time, Japan alone among rich countries represented a weird exception to that guideline, with seemingly ‘safe’ bonds offered at very low interest, while maintaining a Debt/GDP ratio of around 100%. Post 9/11, the US and Europe embarked on a new low-interest era, and developed countries seemed to be able to borrow a greater amount than ever before, without adverse consequences. Debt was cheap, borrowing levels rose, and many more countries – developed, and emerging – breached ‘the red zone.’

Present-day debt levels

These days, the US (seemingly comfortably) shoulders a 100+% Debt/GDP ratio, while Japan’s ratio has climbed to 180%. Are either of these ratios too high?

By way of comparison, Greece – which effectively restructured its debt with the rest of Europe in recent years – only had a 150% Debt/GDP ratio. The US now enjoys a previously unthinkable Debt/GDP ratio, seemingly without consequences. I point out these ratios to say that it’s also not impossible that the US would have to renegotiate its debts at some point. Which is why, crazy as Trump is, he’s sort of inadvertently pointed out an important thing.

Don’t get me wrong. In no way do I ‘predict’ a US sovereign debt crisis is imminent.1 Permabears and goldbugs like Peter Schiff like to talk about a coming US debt crisis like it’s a guaranteed future – like it’s a rational reason to:

1. Start buying gold and

2. Buy empty farmland and build bomb shelters.

It’s not. Shortly after the 2008 Crisis in particular, commentators tried to argue that increasing our national debt at our post-Crisis rate would lead to financial Armaggedon. It didn’t.

I just think that – without any current limits on US sovereign borrowing, we might have the impression that we could borrow indefinitely.

Trump’s comments recently made explicit the problem of excessive borrowing that other countries have dealt with on a semi-regular basis. Greece, Pakistan, Ukraine, Ecuador, Argentina, Russia, and Ivory Coast – to name a few – have faced the problem of excessive debt in the past two decades and done exactly what Trump talked about. You sit down with your creditors and have a difficult, adult conversation. We “US exceptionalists” think this is ‘unthinkable’ but really it shouldn’t be. It happens and has happened on a regular basis with many countries. Plenty of unpleasant but semi-banal developments (war, recession, political instability, a Kanye/Miley Cyrus Democratic Party platform in 2024) could put the US’ ability borrow and pay its debts at risk.

Currency control

One of the great advantages Japan and the US hold over Greece (and the rest of the Eurozone) and many emerging market countries is that we control our own currency. Here again, The Donald is our resident genius, in explaining why this is such an advantage:

“First of all, you never have to default, because you print the money. I hate to tell you, okay, so there’s never a default.”

Again, this is totally irresponsible of him to say this out loud as a person running for President, but he’s technically correct and therefore to be credited with bringing complicated unspoken semi-truths to the surface. Dollar-denominated debt becomes only half as expensive in real terms, if you just double the amount of available money, or experience a quick bout of 100% inflation.

There are some nuances here that would make that harder than it sounds coming from Trump’s mouth. Like, you don’t get to trick your lenders more than once this way, because they (the lenders) quickly raise future interest rates to adjust to inflation.2 Also, significant sovereign debt obligations like Social Security, Medicare, federal pensions, and TIPS (an inflation-linked type of bond) adjust payments upward with inflation. But like I said, I admire Trump for bringing up an important unstated half-truth about currencies and sovereign debt.

The US also enjoys another huge advantage relating to its currency – the fact that everybody in the world still wants dollars as a preferred method of trade, and store of value.

The ‘Reserve Currency’ Advantage

In addition to our ability to inflate away too much debt, we enjoy the advantage of a special ‘reserve-currency’ status in the world which acts as an amazing kind of subsidy for our profligacy.

What do I mean by that? I mean something kind of like that joke about the two hunters and the hungry bear. We don’t have to run a great economy or run a great political system, we just have to run our operation better than all the other choices.3 So if you can create (at least the illusion of) the Rule of Law (China and Russia can’t), Growth (Europe and Japan can’t), and Political Predictability (Africa and Latin America can’t) at a Big Scale (Canada, Switzerland, New Zealand can’t) then you get to be the country that controllers of massive amounts of capital want to be invested in.

We attract excess Chinese, Saudi, Singaporean and Norwegian money into our bonds because where’s else can they park huge amounts of wealth? We may have deep structural problems, but so does everywhere else, to an even greater extent. From a sovereign debt perspective, we can outrun the bear better than the others. At least for now.

That’s the part, unfortunately, with which The Donald is not actually helping, though.

Some Ways In Which The Donald Isn’t So Genius

He’s perfectly correct in saying that if the US got in trouble with too much borrowing, we could sit down and renegotiate our obligations. Lots of countries have done this. He’s also perfectly correct that our control over our own currency allows us to ‘inflate away’ the problem, to some extent. What he’s absolutely putting at risk, however, is our special ability to ‘outrun the bear’ in the form of maintaining (at least the illusion of) the Rule of Law, Growth, and Political Predictability.

The following policies will not help our reserve currency status, which is really the key to the US’ sovereign borrowing advantage:

Building giant walls along our border

Threatening to default on our bonds

Threatening to massively devalue our currency

Forbidding entrance to and/or deporting people based on their religion

Threatening aggressive trade wars with major bond funders, like China

Promising to rewrite libel laws in order to quell journalistic enemies

Encouraging violence against political enemies during public rallies

Now, of course, The Donald will probably say he’s just kidding about all these things. He’s really a more serious person than that, you know he went to a really good school, and he’s really smart and handsome. Lots of women, and even the hispanics, you know, they like him. Maybe bond investors don’t take his little jokes and threats that seriously. Fine, maybe he’s just kidding about all that stuff.

But in my experience, the people who control real capital – the few thousands of wealth managers and bond traders on this planet who ultimately decide whether to continue to roll over the US debt every month – until now rolling it over like clockwork at attractive, low interest rates – in my experience they don’t fuck around.

And by “not fucking around,” I mean they really don’t appreciate heavily-indebted countries, led by hucksters, pushing trade wars and closed borders. They can choose whether – or not – to invest in bonds of countries led by an unserious racist xenophobe who jokingly threatens debt restructuring and inflation. Believe me, they don’t appreciate the joke.

I like our reserve currency advantage. We’ve built a good track record over time of responsibly handling our massive national debts. We’ve been a good bet, and just as importantly perceived to be a good bet up until now, for paying everyone back.

There’s quite a bit at stake here.

Post read (1028) times.

predictions like this are always made by cranks and people with things to sell you ↩

Greg Jefferson and I recorded a short conversation, that may be of interest. The whole ‘Facebook Live’ video is here, with shorter YouTube clip versions below, broken out by topic.

We discussed the inaugural post of Greg’s blog, in which he explains why his hometown Muncie, Indiana is a great place for Trump to gather support. While the commentariat generally cannot imagine anyone voting for Trump, Greg could easily imagine his grandmother warming to his combination of xenophobia/racism, response to economic malaise, and a need to “Make America Great Again.” The discussion of Greg’s Trump blog-post here:

3. The best thing I’ve ever read about Fintech was this blog post. Complaining about existing regulation seems to be the major business strategy of Uber, is the point of that post, under “Strategy #5.” This came up recently because Austin, TX voted to enforce existing regulation of its legacy taxi business. That will cause Uber/Lyft to pick up their ball and go home, at least until their lobby regroups and overwhelms Austin. San Antonians, always the lame sibling to Austin, are obviously rejoicing that – for once – we’ve solved a problem one year ahead of Austin.

Stock markets worldwide will drop significantly tomorrow, and throughout the rest of the week, as US and global investors recalibrate their expectations of the United States due to the little-anticipated Donald Trump victory in today’s Presidential election.

Stock markets worldwide will drop significantly tomorrow, and throughout the rest of the week, as US and global investors recalibrate their expectations of the United States due to the little-anticipated Donald Trump victory in today’s Presidential election.