This is the most expensive post I’ve ever written, as it cost me over $80 to conduct research. I took out two payday loans this month in downtown San Antonio, TX.

The natural joke to make here is “something, something, the death of journalism,” when finance columnists/bloggers need to take out monthly payday loans. Maybe instead the joke is on a different industry, as a former Goldman Vice President (“just a heartbeat away from the Presidency” as the thousands of us used to joke) ends up taking out payday loans. Or maybe you should just stop making jokes because this is how millions of your fellow citizens get money in between pay checks – like 12 million Americans per year, according to The Pew Charitable Trusts.

The Good

My basic starting assumption was that banks don’t really make personal loans anymore – credit cards kind of took over that niche market. A teller at my business bank – where I’ve had an account for twelve years – confirmed my assumption, saying they wouldn’t do it, and that few banks do. After the fact, I found out my personal bank does in fact make personal loans on good terms – 9 percent APR (Annual Percentage Rate) for 3 years on a $2,500 minimum, available in my checking account on the same day. But I believe they are the exception. And all that good deal of course depends on having good credit, which not everyone does.

So, assuming the payday lending filled a niche that banks vacated, I went on my quest for personal experience of the payday loan industry.

I borrowed $200 from Courtesy Loan Service on Broadway. The whole process took 90 minutes, start to finish. Much about this experience, in a strange way, suggested a quaint throwback to the Bailey Brothers Building and Loan from It’s a Wonderful Life. I mean that in the sense that a nice teller recorded my personal information in pen, by hand. She asked for three personal references and the name of my supervisor at work. I saw almost no evidence of computer technology. They appeared to use 5×7-inch paper notecards in a recipe box for tracking clients’ loans. Seriously. They ended up printing my loan on carbon copy paper, using what looked like a dot matrix printer.

I almost told them that 1983 called, and it needs its technology back. But of course the joke’s on me, because I’ll pay an equivalent of 102.31 percent annual interest on their loan, if I pay it off in installments over the next eight months as suggested. So who’s laughing now?

I also walked into Ace Cash on San Pedro Ave and borrowed $200. When I arrived, the teller behind the window pointed me to an electronic kiosk, where I could enter my application in just 5 minutes. These folks, by contrast, operate in 2016.

I filled in my personal information on screen, and then spent another 15 minutes on a three-way phone call confirming my identity with my personal bank. Finally, I walked back to the teller with my bank information confirmed, and showed her my driver’s license. I provided a reference – my wife – and my phone number, which the teller confirmed as legitimate by ringing me while I stood in front of her. She couldn’t have been nicer. In a clocked time of 32 minutes, I walked out the door with $200 cash in my hand. They have impressive technology, automation, and fraud-mitigation techniques.

The Bad

The interest rate here is not only absurd, but cruel. My $200 Ace loan cost me $51.52, for an APR of 336.72 percent, as clearly stated on my receipt. The effective interest rate will be even higher if I pay back the money faster than one month. That’s not a good look, to say the least. I say not good because one would expect these loans – like Courtesy’s Loans,’ violate usury laws, if such laws actually existed.[1]

The Ugly

But the fine print is also interesting.

Within my automated email from Ace – titled “Your Loan Document Enclosed,” – my loan document stated clearly “We do not make loans, but instead provide credit services.”

Then “In consideration for the credit services that we provide you under the Credit Services Agreement, you will agree to pay us a fee (the “CSO Fee”) equal to 25% of the Amount Financed of any Loan you accept from Lender. For example, if we arrange a $200 Loan for you, the CSO Fee would be $50.00.”

Which is, exactly, what we did.

Ok, so, to be clear, on top of the usury problem, there’s the whole lying problem. In Texas, unlike 19 other states where Ace Cash operates, Ace is not a “lender,” but rather a “Credit Services Provider,” and my $50 in interest is not “interest” but rather a “credit services fee.”

I’m not a lawyer and this is not a legal opinion, but obviously that’s a complete lie. And I understand legal fictions happen all the time and for good reasons explained by lobbyists over lobster bisque and that I shouldn’t trouble my pretty head about it. I’m just noting things.

I tend to think I’m more creditor and finance-industry friendly than my average fellow citizen. I usually think a competitive loan market provides the best chance for the best service, and interest rates reflect a reasonable combination of people’s personal credit and the true risks taken by the lender. I can make a strong case, for example, for the existence of sub-prime mortgage loans at elevated interest rates.

But Holy Bejebus Batman! 300%+ interest?

That’s some dark, exploitative, medieval shit right there.

Medieval Shit

The good news is they don’t actually kneecap you when you don’t pay, right? I hope.

But I’m not going to put that to the test. My paycheck arrives soon and I’ll pay these things off then.

[1] It’s super-difficult to tell if usury laws are even actually a thing. I know theoretically even the national credit card companies cap their rates at 29.99 percent. States seem to all set top interest rates, and then state lawmakers create giant loopholes through which payday lending companies can waltz. Your state, like mine, might say personal loans are capped at 24 percent, or commercial loans top out at 28 percent, or whatever. But there are massive categories of seeming exceptions that give the lie to whatever usury laws are supposed to limit.

Note: An ex-student of mine reached out to ask a question many face… Is it best to use savings and investments for graduate school, or to take out loans?

Dear Banker,

I saw you answered a question from a former student about paying down debt and being unemployed on your blog. So I thought I would give it a shot! I am going back to school in January for 1 year accelerated program that will cost 40k-50k, I am not quite sure yet.

Side note: I thankfully do not have loans from undergrad.

So I will have to take out student loans but I am unsure if I should take out the whole 40k-50k or use some of my assets to have less debt after I finish.

I currently have $9,000 in Betterment.com and individual investments with Capital One, $12,000 in Mairs and Power mutual fund that my parents put money in since I was a child. I also have $3,000 dollars in my savings account. I know I shouldn’t use all the money I’ve invested and saved but I was thinking maybe $10,000 dollars to have less students loans to pay back? I’m not sure what is a better decision financially. What would you suggest?

I saw your blog on Facebook and thought I would ask!

Thanks,

M.C. (San Antonio, TX)

—

Hi MC,

Thanks for your question and for thinking of me. I’d like to think a few of the things we talked about in class were helpful.

I hope post-College life is treating you well. Congrats on having real savings and investments at this point…this is really commendable. Plus, no undergrad debt is also a blessing. A good place to be! About your future decision to use savings vs. take out debt for a nursing degree:

I don’t think there’s a single obvious solution. You could approach this various ways and still be making the ‘right’ choice. Also, I’d probably need more info on your situation to give more confident advice. But, here’s the principles I would keep in mind:

1. Student loans – especially for a professional upgrade in skills – are not “bad debt.” Mostly they have low interest rates, with generous payback terms. If they help you achieve a good salary and life-satisfaction, they are “good debt.” $50K of nursing school debt is a lot, but manageable in the long run. The fact that you’ve got some savings and investments already also suggests that you are able to live below your means, which bodes well for your ability to pay back debt over time after you get training and when you are earning money again.

2. If any of your Betterment, Capital One, or Mairs & Power accounts investments are in retirement accounts – tax advantaged accounts like an IRA – don’t take any money out of there to spend now. You might pay taxes and penalties to extract the money, so its better to leave those for the next 40 years to accumulate compound returns.

3. For invested money not in retirement accounts, its ok to take the money out and spend some on a worthy project like a professional upgrade. BUT…if you’re able to resist taking money out, it’s better for you in the long run. It’s so very difficult to actually accumulate savings and investments – especially when you’re in your twenties – that I think you should try extremely hard to preserve it, invested in the markets. This will mean more debt (and therefore more risk) but it seems justifiable, at least to me.

4. Leaving money invested in stocks/ mutual funds is tax efficient (meaning, every time you sell you’ll owe taxes on the gains.).

5. It’s also slightly riskier (stocks/mutual funds can lose value). But the longer you can leave them alone untouched, the better your prospects for building wealth with that money.

6. I think, psychologically, its easier to save and invest if you already have something saved, rather than zero. So I wouldn’t want you to go to zero on your investments.

Those are my thoughts. Feel free to write back or call if you want to discuss/clarify/argue about any of this.

By the way, how do you like Betterment? I haven’t really explored it but it seems like the targeted solution for your demographic. I’ve been enjoying an app called Acorns which I quite like. I wrote about it here: http://www.bankers-anonymous.com/blog/check-out-this-acorns-thing/

Michael

—

MC’s response:

Thanks so much for getting back to me! I’m sorry it took me a while to respond I went away for a week right when you wrote me back.

I was thinking that it would be better in the long run to not touch my investments but taking out such a big loan does make me nauseous when I think about it. However, I think I will stick with that strategy because I know if I leave nursing school with no savings I won’t feel good about that either. Thanks for going through the pros and cons its way more helpful then my internet searches have been!

I don’t have an IRA right now but I know I should set up a Roth IRA soon but I wasn’t sure yet if I wanted to use that money for school.

As for Betterment, I really like it! I started an account in August 2011 and just give about 60 dollars a month. According to my performance chart my return rate is 37% with an allocation of 100% in stocks. If I had 80% stock and 20% bonds it would be 44% right now. My original allocation was actually 70% stocks and 30% bonds but after your class I decided to try 100% stocks which, just like Acorns, Betterment refers to as ‘aggressive”. The majority of the investments are in different Vanguard funds and iShares. I like that part of it as well because if I’m not mistaken to open these account individually sometimes you need 1,000 or up to 3,000 dollars. I think Betterment is great for people my age! I always tell my friends to sign up who don’t know anything about investing.

Thanks again for responding and teaching a great class I think all students should be required to take it!

MC

—

MC, Ok good luck! You’re going to do great, because you’ve already done the hard part, which is to begin saving and investing in your early 20s.

One of The Donald’s great strengths is that he latches onto a partial truth – or an unspoken but widely held belief – and then expands upon it for his own purposes. Obviously this can veer into disgusting territory, when it comes to expressing sexually insecure men’s feelings about women, or insecure workers’ feelings about economic threats from China or Mexico. As Matt Taibbi eloquently expressed, he effectively uses this same talent of partial truth-telling to bash government and media elites who do, in fact, disdain, misunderstand, or ignore ‘regular Americans.’ Trump scores these points against Establishment elites because really, we sense some truth in what he says, that others before him won’t say.

Earlier in the week Trump stepped in a pile of it when he expressed truths about US sovereign debt which political leaders cannot openly discuss. Unconstrained by good taste, judicious character, or political consistency – he can pop off in any direction, occasionally hitting on an important point that more people should understand. The Donald said:

“I’ve borrowed knowing that you can pay back with discounts. I’d borrow [as President, on behalf of the US] knowing that if the economy crashed, you could made a deal.”

This is so crazy that he said it – as a person running for President – that you kind of have to laugh at his gall. On the other hand, he’s right. This is what happens when countries borrow too much. And also, we don’t really know – or have any kind of open discussion in this country – about what constitutes too much national borrowing.

Those fingers tho…

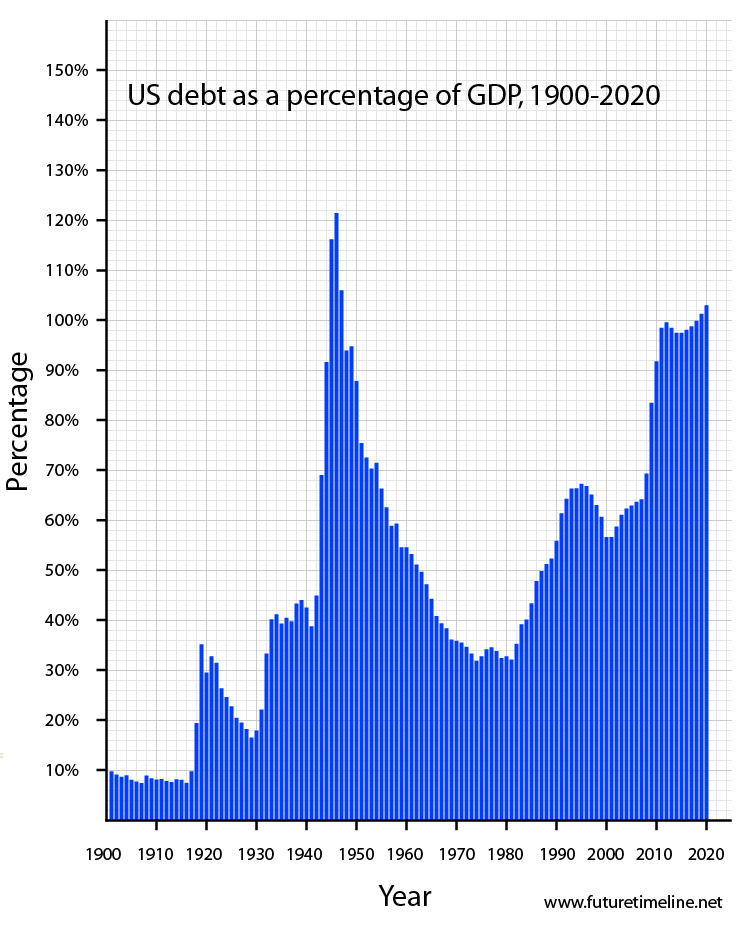

When I worked as an emerging market bond salesman in the late 1990s – slinging bonds from places like Pakistan, Ukraine, Ecuador, Argentina, Russia, and Ivory Coast – we used to put out economic research for our clients that pointed out that a 70% Debt/GDP ratio marked a kind of scary ‘Do Not Cross’ line. If the total amount of sovereign debt exceeded 70% of the economic output of country, you might have to start worrying about whether that country could reliably pay back its bonds. Once you hit 100% Debt/GDP, history seemed to show, emerging market countries would enter a red-zone of risky sovereign renegotiation, or possible default. Their cost of new borrowing would rise, which in turn would hurt their ability to service their existing debt. At between 70% and 100% Debt/GDP, countries could get into a vicious death-spiral of borrowing, ending in sovereign debt restructuring.

At that time, Japan alone among rich countries represented a weird exception to that guideline, with seemingly ‘safe’ bonds offered at very low interest, while maintaining a Debt/GDP ratio of around 100%. Post 9/11, the US and Europe embarked on a new low-interest era, and developed countries seemed to be able to borrow a greater amount than ever before, without adverse consequences. Debt was cheap, borrowing levels rose, and many more countries – developed, and emerging – breached ‘the red zone.’

Present-day debt levels

These days, the US (seemingly comfortably) shoulders a 100+% Debt/GDP ratio, while Japan’s ratio has climbed to 180%. Are either of these ratios too high?

By way of comparison, Greece – which effectively restructured its debt with the rest of Europe in recent years – only had a 150% Debt/GDP ratio. The US now enjoys a previously unthinkable Debt/GDP ratio, seemingly without consequences. I point out these ratios to say that it’s also not impossible that the US would have to renegotiate its debts at some point. Which is why, crazy as Trump is, he’s sort of inadvertently pointed out an important thing.

Don’t get me wrong. In no way do I ‘predict’ a US sovereign debt crisis is imminent.1 Permabears and goldbugs like Peter Schiff like to talk about a coming US debt crisis like it’s a guaranteed future – like it’s a rational reason to:

1. Start buying gold and

2. Buy empty farmland and build bomb shelters.

It’s not. Shortly after the 2008 Crisis in particular, commentators tried to argue that increasing our national debt at our post-Crisis rate would lead to financial Armaggedon. It didn’t.

I just think that – without any current limits on US sovereign borrowing, we might have the impression that we could borrow indefinitely.

Trump’s comments recently made explicit the problem of excessive borrowing that other countries have dealt with on a semi-regular basis. Greece, Pakistan, Ukraine, Ecuador, Argentina, Russia, and Ivory Coast – to name a few – have faced the problem of excessive debt in the past two decades and done exactly what Trump talked about. You sit down with your creditors and have a difficult, adult conversation. We “US exceptionalists” think this is ‘unthinkable’ but really it shouldn’t be. It happens and has happened on a regular basis with many countries. Plenty of unpleasant but semi-banal developments (war, recession, political instability, a Kanye/Miley Cyrus Democratic Party platform in 2024) could put the US’ ability borrow and pay its debts at risk.

Currency control

One of the great advantages Japan and the US hold over Greece (and the rest of the Eurozone) and many emerging market countries is that we control our own currency. Here again, The Donald is our resident genius, in explaining why this is such an advantage:

“First of all, you never have to default, because you print the money. I hate to tell you, okay, so there’s never a default.”

Again, this is totally irresponsible of him to say this out loud as a person running for President, but he’s technically correct and therefore to be credited with bringing complicated unspoken semi-truths to the surface. Dollar-denominated debt becomes only half as expensive in real terms, if you just double the amount of available money, or experience a quick bout of 100% inflation.

There are some nuances here that would make that harder than it sounds coming from Trump’s mouth. Like, you don’t get to trick your lenders more than once this way, because they (the lenders) quickly raise future interest rates to adjust to inflation.2 Also, significant sovereign debt obligations like Social Security, Medicare, federal pensions, and TIPS (an inflation-linked type of bond) adjust payments upward with inflation. But like I said, I admire Trump for bringing up an important unstated half-truth about currencies and sovereign debt.

The US also enjoys another huge advantage relating to its currency – the fact that everybody in the world still wants dollars as a preferred method of trade, and store of value.

The ‘Reserve Currency’ Advantage

In addition to our ability to inflate away too much debt, we enjoy the advantage of a special ‘reserve-currency’ status in the world which acts as an amazing kind of subsidy for our profligacy.

What do I mean by that? I mean something kind of like that joke about the two hunters and the hungry bear. We don’t have to run a great economy or run a great political system, we just have to run our operation better than all the other choices.3 So if you can create (at least the illusion of) the Rule of Law (China and Russia can’t), Growth (Europe and Japan can’t), and Political Predictability (Africa and Latin America can’t) at a Big Scale (Canada, Switzerland, New Zealand can’t) then you get to be the country that controllers of massive amounts of capital want to be invested in.

We attract excess Chinese, Saudi, Singaporean and Norwegian money into our bonds because where’s else can they park huge amounts of wealth? We may have deep structural problems, but so does everywhere else, to an even greater extent. From a sovereign debt perspective, we can outrun the bear better than the others. At least for now.

That’s the part, unfortunately, with which The Donald is not actually helping, though.

Some Ways In Which The Donald Isn’t So Genius

He’s perfectly correct in saying that if the US got in trouble with too much borrowing, we could sit down and renegotiate our obligations. Lots of countries have done this. He’s also perfectly correct that our control over our own currency allows us to ‘inflate away’ the problem, to some extent. What he’s absolutely putting at risk, however, is our special ability to ‘outrun the bear’ in the form of maintaining (at least the illusion of) the Rule of Law, Growth, and Political Predictability.

The following policies will not help our reserve currency status, which is really the key to the US’ sovereign borrowing advantage:

Building giant walls along our border

Threatening to default on our bonds

Threatening to massively devalue our currency

Forbidding entrance to and/or deporting people based on their religion

Threatening aggressive trade wars with major bond funders, like China

Promising to rewrite libel laws in order to quell journalistic enemies

Encouraging violence against political enemies during public rallies

Now, of course, The Donald will probably say he’s just kidding about all these things. He’s really a more serious person than that, you know he went to a really good school, and he’s really smart and handsome. Lots of women, and even the hispanics, you know, they like him. Maybe bond investors don’t take his little jokes and threats that seriously. Fine, maybe he’s just kidding about all that stuff.

But in my experience, the people who control real capital – the few thousands of wealth managers and bond traders on this planet who ultimately decide whether to continue to roll over the US debt every month – until now rolling it over like clockwork at attractive, low interest rates – in my experience they don’t fuck around.

And by “not fucking around,” I mean they really don’t appreciate heavily-indebted countries, led by hucksters, pushing trade wars and closed borders. They can choose whether – or not – to invest in bonds of countries led by an unserious racist xenophobe who jokingly threatens debt restructuring and inflation. Believe me, they don’t appreciate the joke.

I like our reserve currency advantage. We’ve built a good track record over time of responsibly handling our massive national debts. We’ve been a good bet, and just as importantly perceived to be a good bet up until now, for paying everyone back.

There’s quite a bit at stake here.

Post read (950) times.

predictions like this are always made by cranks and people with things to sell you ↩

Note: This post has a Texas bias and a version of it ran in the San Antonio Express News. However, there is no open-carry here on this blog, so you can bring your children.

I suggested in a recent post that it’s nearly impossible to fund a new business and there’s really no good way to go about it. The best thing you can hope for is just to be born rich.[1]

However, in the interest of keeping the American Dream alive (at least until Trump wins in November) I’ll mention a few non-traditional avenues to investigate if you’re starting a new company and looking for funding.

Each of the following non-bank options are lenders, meaning you’re getting a loan rather than a direct investment in your business.

Prosper.com

Prosper is not a small business lender per se, but rather an online source of 3-year fixed interest rate personal loans of up to $35,000. You can apply with them online for a variety of needs, including for your small business. You create a profile, describe the size of the loan you need and your planned use of the funds, and what interest rate you’d be willing to pay. The ‘lender’ will be numerous individual investors[2] grouped together by Prosper. They agree to fund you at your proposed interest rate, for as little as $25 per lender, or up to the full amount of your request. Prosper handles all the online mechanics of funding and payback of the loan. Since there’s no traditional bank involved, but rather thousands of individuals making decisions, I see Prosper as a reasonable, small-size, alternative for startups to consider.

In my state, Texas, you cannot be a lender on Prosper, but you can be a borrower. In the mid-2000s – back when Prosper first came out and I lived in New York – I funded a bunch of small loans, including small business loans. As an investor, Prosper worked fine for me.

Back in 2007 I also once tried to borrow $10,000 and was ‘funded’ by the collective interwebs at a reasonable 7.7% rate, but could not ultimately get through their due diligence process, which included a credit check (that part was fine) and review of my taxes (for some reason that befuddled them.)

Prosper reports $5 billion worth of loans funded since their inception, so I assume my own problems were idiosyncratic. So check it out.

LiftFund

Non-profit microlender Liftfund lends money to small businesses in 13 states, although they are headquartered in San Antonio.

[Important disclosure: I do periodic consulting gigs for LiftFund, so anything nice I might say about them should be filtered appropriately.]

They may, in fact, be your startup business’s only hope of getting a loan.

Whereas your traditional bank will not talk with you about a loan until two years have passed – and frankly your bank isn’t in the business of coaching small businesses – LiftFund not only will talk to you but considers supporting startups with educational resources a key part of their role.

When I say banks will neither coach you nor even talk to you about a loan for your startup, I’m not judging banks. Some of this, including the coaching part in particular, is not a money-maker.

I guess LiftFund can do this because of their not-for-profit mission. Like other non-profit business lenders they can do things which don’t maximize their bottom line. Loans range from as small as $500 to as large as $250,000. A bunch of friends of mine in business for less for than two years have gotten loans from LiftFund and their predecessor Accion, so I know this is a legit source.

Able Lending

File this one under “This is a really cool theory but it’s too new for me to have experience with it yet.”

Able Lending relies on a classic microcredit lending theory – that we won’t fail to pay back friends and family – to lend to startups less than two years old.

I recently met up with Mario Cardona – the one-man San Antonio branch office for 2-year-old Austin-based startup Able Lending.

Cardona explained that business owners seeking a loan from Able must first tap their own personal networks (Uncle Bob, your college roommate Janet, and your hair stylist Sam) and get a commitment from at least three different ‘backers’ for your loan. Step two, Able funds up to three times that committed amount, at a rate between 8 and 16%, for between $25,000 and $500,000. So after Bob, Janet and Sam together agree to lend you $25,000, Able funds $75,000. If you do a 3-year business loan, Able gets its portion of the loan paid back faster than your backers do, which is kind of a neat mechanism for ensuring that your backers are taking some risk on you. I think Able Lending depends on the feeling that you really, really, don’t want to let your personal backers down, so they feel more secure with your business loan.

Does it work? I don’t know yet, but would somebody please let me know if they have experience with Able Lending? I like the idea.

NextSeed

Like Able Lending, Next Seed is a total startup, so it’ll take some time to see how it goes. Also, like Able Lending and LiftFund, it’s based in Texas. Unlike those two, it is only registered right now to do business in Texas. Finally, like Prosper, it’s a crowd-sourced platform for borrowing money.

NextSeed is taking advantage of newly liberalized national and state laws to allow companies to raise debt and equity from non-accredited (meaning, non-wealthy) investors. Small businesses can sign up with NextSeed to raise between $25K and $1 million at a set interest rate. Investors/lenders – that could be you and me – lend in increments as small as $100 via this platform. NextSeed handles the funding and regular monthly payments.

I spoke with the founders, who believe they offer a more personal, fun mechanism for investing on the one hand, and an alternative source of capital for entrepreneurs on the other. They are currently doing deal number four, so it’s early days yet. I’m thinking about signing up and sending in a small amount of money to be a lender, partly to figure out the mechanisms and partly because Texans right now are shut out of participating in Prosper.

Crowd-funding thoughts

I’ve been reading and learning lately about the liberalization of crowd-funding rules to allow for non-wealthy people to participate. I remain concerned that

a) This is a not very-efficient way for business owners to access capital and

b) Some non-wealthy people, at some point, will lose their shirts. There will be tears.

Right now I’m of the mind that liberalizing laws to make more types of investments available for non-accredited investors is probably a net gain for society and the economy – principally that entrepreneurs get more opportunities to access capital. But given the nature of things like this, some people will bear the brunt of the “costs” of this liberalizing – via catastrophic, unexpected, losses. We’ll have generalized, socialized gains and concentrated, private losses. Sort of the exact opposite of the 2008 crisis and bailouts of TBTF banks.

[1] If I wrote the bible for small business owners I’d say that it’s easier for a camel to fit through the eye of a needle than it is to convince an affluent person or institution to back your startup company. I feel your pain. To take a more 21st Century analogy, raising money can be heavier lifting than you’ll find at 5:30am Crossfit gym. Traditional banks just don’t want to talk to small businesses until they’ve been in business for two years, with the tax returns and profit to show for it.

[2] Although I kind of assume that by now individual investors have been replaced, somewhat, by Prosper bots. Meaning, institutions or high-net individuals have profit-optimized the algorithm for funding X amount at Y credit rating and Z interest rate on Prosper, so things are pretty automated. An amateur individual lender like me – without an algorithm – is going to end up accepting a non-optimized interest rate for any given risk. Which is still probably fine.

My wife, who spent her formative years in College Station TX, asked me “why don’t Aggies eat barbecue beans?” Answer: “Because they keep falling through the holes in the grill.”

That’s not nice at all! And, most likely, not even true! Although I can’t be sure because I’ve only visited College Station myself a few times.

Aggie jokes popped into my mind because CardHub.com, an online aggregator of credit card information, published a mildly interesting report this past week ranking US cities in terms of their average expected time to pay off credit card debt.

The Ranking

Aggies, brace yourselves. College Station ranked 2,547 out of 2,547 cities. That’s dead last in the entire country in terms of capacity to pay off credit card balances in a timely way. Ugh.

It got me thinking about how the home of a distinguised research institution would have the ignominious distinction of being last in the country in terms of credit card debt sustainability.

By contrast, CardHub lists the city with the #1 ranked fastest time-to-payoff credit card debt as Cupertino, CA.

Methodology

CardHub’s method for rankings went as follows. They figured out average income per household in each of 2,547 cities, according to the US Census, as well as the average credit card balance in each city, as provided by credit bureau TransUnion.

CardHub assumed a 14% annual percentage rate on balances – and then assumed an affordable payment of existing balances each month, adjusted for average income in the city.

Using that data, CardHub calculated how many months – on average – it would take the residents of a city to pay off their credit card debt.

I describe their report as only “mildly interesting” because while it purports to show something novel about average indebtedness by municipality, it’s actually an interesting example of how financial statistics may mislead and just reflect demographics.

Is it just wealth?

Cupertino, CA – the #1 ranked city in the CardHub study – is an address which you may recognize as the home of Apple, the world’s most valuable company.

Of the top 10 cities ranked by time-to-payoff – all but one are in tech-rich California cities or affluent suburban-Boston cities of Massachusetts such as Lexington or Arlington. Of the top 30 cities, many others are recognizably wealthy suburbs, including Bloomfield Hills, MI, McLean, VA, and Chevy Chase, MD.

So I guess one way to look at these rankings is just to notice that residents of high-income and wealthy cities can pay off their debts more easily while residents of poorer cities – by definition – will take longer to pay off their debts. That’s sort of obvious, and also not very funny at all.

Another Aggie joke

But did you hear the one about the Aggie who won the Texas lottery but was told he’d have to receive the money in 20 yearly installments instead of a lump sum? He was so angry! “In that case,” he said, “just give me my dollar back!”

Ok, that isn’t nice at all, either. Also, seriously, you should never play the lottery.

Or another factor?

Besides the high income and wealth factor, which I think is sort of obvious (and again, not that funny) I was wracking my brain to figure out how a college town in Texas ranks dead last nationwide in terms of time-to-pay-off credit card debt.

The best I came up with is that a plurality of the population of College Station, TX is actually students – who naturally earn practically nothing – but who do incur credit card debt in the ordinary course of their studies.

I’m pretty sure my theory is correct. According to the US Census the median age of a College Station resident is 22.3 years, compared to the median age in the United States of 37.2. Furthermore, the population of College Station in 2010 was about 94,000, while Texas A&M reported a student population that year of about 49,000. So I think what CardHub’s time-to-payoff credit card rankings really highlight – at least at the bottom – is a population of students, in their debt-incurring phase of life, rather than their earnings phase of life.

College Students

Supporting my theory about the preponderance of a student population of a city is the fact that other cities ranking in the bottom of CardHub’s list of 2,547 include other college towns like San Marcos, TX (#2,532 and the home of Texas State University) and Provo, UT (#2,531 and the home of Brigham Young University).

So, I’ve come to believe, Aggies and College Station TX can’t be razzed for ranking dead last in the country on this measure. It’s just a demographic anomaly of a student-dominated city population. I spoke to Jill Gonzalez, an analyst at CardHub, who seconded my analysis, and named for me some other prominent college towns that ended up on the bottom of the list.

A third Aggie joke

Meanwhile, my father-in-law, a long-time Texas A&M professor and Aggie booster, sent me a link to Aggie jokes online, and I appreciated the one about what Aggies think Cheerios are: Donut seeds.

I like that one. Personally, I will never see Cheerios the same way again.

The actual point

Ok, the (semi) serious point of looking at a financial ranking like “time to payoff credit card debt” is that statistical financial rankings like this can often obscure reality. CardHub’s ranking of cities may be interpreted as a demographic ranking of wealthy cities at the top and college towns at the bottom.

Very likely the Aggies of College Station, TX aren’t worse at handling credit card debt than the rest of the country. They’re just students who haven’t begun to register any income yet.

Still, it’s tempting to make a make a few jokes, no? I’ll probably be run out of town for this post.

Editors Note: To avoid hate-mail from Texas A&M boosters, I’ve decided to remain anonymous, except for the fact that a version of this ran in the San Antonio Express News.

Scott Burns and Laurence J. Kotlikoff wrote The Clash of Generations: Saving Ourselves, Our Kids, and Our Economy, thought-provoking and highly readable financial policy book in 2012, featuring four “purple” policy proposals – “purple” meaning meant to appeal to both red and blue sides of the American political spectrum.

In the context of a 2016 Presidential contest featuring the unappealing choice between Know Nothingism (Trump), Socialism (Sanders), Nepotistic Oligarchy (Bush), and Nepotistic Pandering (Clinton),[1] I find it refreshing to read ideas designed to appeal to a broad spectrum of the right and left. Maybe you will too.

Inter-generational screwing

No, I’m not referring to an inappropriate Spring/Winter romance. Rather, Burns/Kotlikoff’s central thesis is that the older generation has – through a combination of tradition, neglect, and the compounding affects of fiscal policy – doomed the younger generations to financial deterioration and eventual financial wipeout.

Intergenerational burden

One of my favorite illustrations of the inequality between generations is the example of seniors gathering for a “Senior Coffee” breakfast at a McDonalds, featuring 55 cent coffee and $1 specials. It initially sounds innocuous.

It takes 10 low-wage McDonalds workers to fund one senior’s social security

However, with an average senior’s monthly Social Security check of $1,172, the authors point out that the average McDonald’s worker has to put in 1,172 hours (at $8.00/hour, that’s a 50 cent payroll tax from worker, and a 50 cent payroll tax from employer going to the Federal Government) to generate enough tax revenue for a single senior’s monthly check. With the typical Mcdonalds worker putting in 120 hours per month, it takes almost 10 minimum wage McDonalds workers to support each senior. We don’t usually view the different generations at odds this way, but that’s the kind of intergenerational burden the authors are talking about.

When they run through the runaway increases in federal health care costs [Medicare, plus increased prescription drug reimbursements (W Bush) and the Affordable Care Act (Obamacare)] in addition to unequal tax treatment, the ‘clash of generations’ seems both unfair and unsustainable.

This crisis sets up the background to their main four policy proposals.

Purple Policies

I like this book a lot, and their purple policies deserve to be part of any serious fiscal policy conversation (although which leaders would have that conversation, I’m actually not sure, such is our political discourse these days). I suspect the authors would have their own doubts about the political viability of their somewhat radical solutions, but would argue that the risks of inaction are too great, given the impending fiscal insolvency.

I’ll briefly describe below their four big policy ideas, with links to their further thoughts online.

Finally, after reviewing their policy ideas, I have one critique of the tone of the book’s early chapters.

Kotlikoff and Burns advocate a radical simplification of banking functions. Their proposal says that any and all banks (plus insurance companies, brokerages, credit unions, private equity firms) must fund themselves and be regulated as “mutual funds,” taking in actual deposits for every dollar invested in loans. No borrowing, full stop. Any company that prefers to leverage itself (hedge funds might want to) must operate under a “full-liability” regime, meaning losses are guaranteed personally by the business owners and executives. You can see why this is kind of appealing in the wake of the 2008 crisis and bailout of Wall Street.

[Incidentally, my own radical ‘purple plan’ addresses this same post-2008 moral hazard problem, but in a different way. My rule is: Any financial firm over a certain size (I don’t know how many would qualify but let’s say the biggest 25 firms, and any that are considered ‘systemically important’) get regulated like public utilities, with massive restrictions on executive pay. Of course, all financial firms are invited to get smaller through divestiture, sales, breakups, whatever, to get under the size limit and become systemically irrelevant. At that point, executives at the newly smaller firms can go back to paying themselves whatever they want. That’s my solution to the problem of “profits get privately enjoyed via executive compensation but any liabilities get socialized” when a systemically important financial institution gets bailed out.]

Their plan begins with individual vouchers for everyone for purchasing a basic plan to receive care from a private provider of their choice. Vouchers are individually ‘risk-adjusted,’ meaning documented medical conditions receive larger vouchers. Anybody is allowed to supplement with additional care out of their own pocket. Insurance companies providing standard care cannot deny coverage. For fiscal sanity, however, they advocate a panel of doctors to set strict budgets on the total cost of all federal vouchers, not to exceed 10% of GDP in any year. (death panels!)

Comprehensive health care policy is well beyond my ken to deeply comment on, but I do appreciate their attempt to set limits to how much public money is spent on health-care. Unfortunately there has to be some rationing of costs when we set a limit like 10% of GDP maximum. I know this a politically radioactive (again, death panels!) but seems like an important adult conversation to engage in.

Since tax policy is arguably the most important and least understood part of public policy, I appreciate the authors’ radical approach here.

For starters, they eliminate personal and corporate income tax (whoa!), which they argue is surprisingly regressive in its current form.

They replace it with a high 17.5% federal retail sales tax, as well as a tax on all consumption above $5,000 done abroad (to catch up you folks running over to Canada to do your shopping, to avoid the high retail tax).

To correct the regressive nature of consumption taxes, they would include a monthly ‘demogrant,’ effectively a transfer to all households, based on family composition, and meant to alleviate the sales tax burden (get to net zero tax) on families below the poverty line.

Estate Taxes in their plan

Interestingly (since I think estate taxes should be discussed more frequently) they would eliminate the federal estate tax, and replace it with a 15% inheritance tax above $1 million. The effect there, I think, would be to encourage estate planning that involves a greater number or recipients. If you had $10 million to pass to heirs, for example, and could pass it on tax free as long as recipients only got $999,999. I think lots of people would choose ten recipients, rather than pay 40% on amounts over 5.43 million (so, $1.828 million in taxes) when giving to a smaller number of heir under the current system. The effect is a wider distribution of inheritance, which is a reasonable goal for addressing intergenerational wealth transfers.

Burns and Kotlikoff address the problem of our unsustainable unfunded social security liabilities, and argue that funding retirement with real worker contributions (through a Personal Security Account PSA) is a necessary replacement system. Workers under age 60 would fund their accounts with a mandatory contribution of 8% of wages. Funds would be invested by the government, at zero cost, in global securities. The federal government would match contributions by the poor, disabled, and unemployed on a progressive basis.

In any case Burns and Kotlikoff argue there should be a government guarantee of at least a ‘zero real return’ for individuals, which seems like a reasonable solution to the fact that some people will find investing in global securities ‘too risky.’

I’ve skipped many of the details of each of their four policy plans, including quite a few specific provisions to address problems that would arise in the process of shifting from our current system to their radical purple solutions.

I’ve linked above to each of their plans because if you’re a policy nerd, you might enjoy reading through their radical and thoughtful solutions to pressing financial problems.

Ok, now one critique of their book.

A problematic first three chapters

I don’t particularly like their first few chapters, in which they lay out their alarming financial thesis in warnings bordering on Chicken Little-style.

The tone seems intended to strike extreme notes about our future financial doomsday.

The younger generation is getting financially screwed by the older generation! [2]

Fiscal deficits are forty times worse than anything the federal government reports!

Unless dramatic, politically impossible steps are taken soon (and they wont be!) the United States economy will sink into a morass worse than Greece! [3]

Specifically, they note that official estimates of government deficits systematically undercount unfunded public liabilities – for health care and social security in particular – and that the unchecked growth of these liabilities, in the long run, will completely overwhelm the United States’ economy. The losers in this scenario won’t be old folks today, but rather their grandchildren, who inherit the public liabilities. I believe this basic premise, and I believe it’s important to point out, but I guess I don’t like some of the hyperbolic ways its presented, and I don’t think the use of big future numbers tracking deficits is carefully interpreted.

One of the things I’ve noticed when describing compounding effects on money with long time periods is that you can quickly get into overwhelmingly large numbers. I have even done this trick myself in the service of making a dramatic point, but because it combines assumptions about an unknowable future with compounding effects, it’s not hard to mislead readers in the service of a particular thesis.

Between them Kotlikoff and Burns have written and published many serious books (and I have published precisely zero books, serious or otherwise, so what do I know?) but the tone of these first chapters struck me as BIG PUBLISHER driven.

“Make sure you make the case to the reader in Chapter One that everything will go to hell unless people buy this book and also legislators make the policy changes you advocate,” seems to have been the mandate handed down by BIG PUBLISHER.[4]

One problem with this tone is that, if the sky does not fall, and three years have since passed (the book came out in 2012) their dire warnings begin to look less true in retrospect. Or, even if true, (and FWIW I trust the economics behind their warnings) the consequences are less imminent or less dramatic than claimed.

Anyway, what I really mean to say is, their book is much better than the tone of their initial chapters would suggest.

[1] And those are just the leading candidates. Further down the ballot we get financial policies such as Fundamentalist Christianity (Carson, Huckabee), Fire Everyone (Fiorina), Shut Down Government (Paul), Shut Down Government And Burn All The Buildings Too (Cruz), Personal Bankruptcy At Any Moment Now (Rubio), Bully Everyone But Especially Unions (Christie), and I’m Just An Average Joe Son Of A Coalminer From Hellhole Scranton (Biden). And finally for completeness’ sake, I have no idea what they think about financial policy (Chafee, O’Malley, Pataki, Graham, Kasich, Jindal, Santorum).

[2] Somewhat charmingly, both authors are of an age eligible for social security, so they are really writing and advocating against their own self-interest, narrowly understood. If this book was written by a twenty-something, complaining about how the US financial system unfairly favors older people at the expense of younger people, it would read more as a call to intergenerational conflict by the aggrieved youth.

[3] This is the jacket cover language: “The United States is bankrupt, flat broke. Thanks to accounting that would make Enron blush, America’s insolvency goes far beyond what our leaders are disclosing. The United States is a fiscal basket case, in worse shape than the notoriously bailed-out countries of Greece, Ireland, and others.” None of these sentences are objectively true, at all.

[4] The publisher is academic, MIT Press, so its not really BIG PUBLISHER in any obvious sense. But still, the early tone feels marketing driven.

This is the most expensive post I’ve ever written, as it cost me over $80 to conduct research. I took out two payday loans this month in downtown San Antonio, TX.

This is the most expensive post I’ve ever written, as it cost me over $80 to conduct research. I took out two payday loans this month in downtown San Antonio, TX.