And by “much interest” I mean the story made me want to stab my own hand with a sharp pencil.

I hate this sort of thing.

Not because of straight up corruption

Let’s leave aside the obvious problem of ‘economic development’ schemes like this, in which public entities give targeted incentives to a specific, private company: You know, because private individuals who benefit may feel quite ‘grateful’ to their public sponsors. Public sponsors in turn – elected and appointed officials – may then have an incentive to direct public funds to private beneficiaries to keep the ‘gratefulness’ cycle going.

That’s all obviously just straight up corruption and not really what I’m aiming for here in my critique of city-directed ‘economic incentives’ for private companies. [1]

What I really hate about this is something quite different, having to do with three business concepts: selection bias, market efficiency, and the structural short-run conflict between entrepreneurial goals and public policy goals.

Taken together, they greatly reduce the odds that this type of economic development works out for the public good in the long run.

I’ll address these in order.

Selection bias

Would you like your city (or state, or county) to grow companies focused on wooing public investment and public ‘economic development’ incentives? Or would you like your city to grow companies that focus on profitability without a public subsidy or public investment? Because the way you attract companies to your city (or state, or county) introduces a real selection bias to the pool of companies you end up with.

In my experience, the kind of startup company that takes public money – with all the attendant scrutiny, ‘job creation’ requirements and ‘salary’ minimums – is a different sort of company than one that achieves sustainability without that public money.

Market Efficiency

Private investors constantly scour the market for small but growing companies that provide a reasonable chance at future profits.

Small but growing companies in turn often seek direct investments from private investors known as ‘angel’ or ‘venture’ capitalists.

It’s not a perfect system, and market inefficiencies occasionally arise.

But when a company turns to public funds like this, what that signals to me is that private capital sources – the professional angel and venture capitalists – have already declined to invest in the growth of this company. That’s typically because professional angel and venture capitalists do not find the risk/reward profile of that investment sufficiently compelling.

Now, professional investors may be wrong to have overlooked the growth and profitability potential of these medical device companies.

The angel investing market may be inefficient.

Who knows? Maybe the City of San Antonio Economic Development team may have a market-beating strategy for identifying a positive risk/reward formula that private investors have declined to take. I mean, it could happen, right?

But I doubt it. And I would never bet on it.

The short-run conflict between entrepreneurship and public policy goals.

Look, here’s the biggest problem.

Public officials want to be seen to create “jobs.” At “good salaries.” That’s fine.

But entrepreneurs don’t seek to create jobs. At any salary.

Entrepreneurs, at least the good ones, want to create the least number of jobs possible. I’m not saying this because entrepreneurs are inherently mean-spirited, but rather, because hiring people is expensive.

Successful small companies – and big ones too – have to constantly try to eliminate jobs to make a company financially sustainable. The market is too darned competitive to survive when you’re burdened with too many people on the payroll. If public officials get the chance to dictate the number of jobs, and the salary minimums of jobs, I guess I have my doubts about how that business is being run.

You show me an entrepreneur willing to be told by a city entity how many people to hire, when to hire them, and what to pay them, then I will show you an entrepreneur who isn’t going to make it in the long run.

Because that’s what Romney’s firm Bain Capital is good at. They buy a company, wring out expensive costs (all those “good salary” jobs!) and then resell. In the short run, the more jobs you eliminate, the better. I’m not saying this to besmirch Romney’s record. I’m sure he was a fantastic capitalist. Cutting costs is what capitalists, and entrepreneurs do, and often that means eliminating jobs. But Romney as “job creator?” Give me a break.

I mention this to illustrate the short-run differences in goals between entrepreneurs and public policy officials

Ok, now back to San Antonio.

I hope I’m wrong

I hope to be completely wrong about this $1.75 million direct investment. Despite my misgivings, I will be thrilled when these three startup medical device companies spur innovation, trigger job growth, add to the ‘entrepreneurial ecosystem’ and even generate a positive return on public capital.

It could happen! I hope it happens!

But I would never, ever, choose to bet on it with my own money. And I’m sorry when the city chooses this for me.

[1] That kind of obvious corruption is what the New York Times had in mind in pointing out in 2012 that Dallas-based tax consultant G. Brint Ryan worked to secure tax breaks for private corporations in Texas while personally donating $250,000 and $150,000 for the Governor and Lieutenant Governor respectively. I don’t mean all that, since it’s all too obvious how each group benefits there at the expense of the public good. I mean, who could deny it with a straight face?

I joined my colleague at the San Antonio Express News to discuss the incoming Comptroller, as well as the fate of the controversial Texas Enterprise Fund.

A former student at Trinity sent me a Facebook message recently. He linked to an advertisement message for an investment advisory company that emphasized the importance of ‘rebalancing’ one’s investment portfolio every quarter or every year.

I realized I had not taught that principal at Trinity in our personal finance course last Spring. When the link came in on Facebook with the simple query from my student: “What is rebalancing?” I thought “Uh-oh, I missed that one.”

To make it up to that student, as well as to anyone else who might have the same question, here’s the quick explanation of rebalancing.

Rebalancing is one of those investment things you should do regularly, like brushing your teeth (only less frequently) or going to your college reunion (only more frequently). Once a year rebalancing is fine.

The point of rebalancing is to avoid two big No-Nos of investing:

1. Overexposure to one particular type of risk; and

2. The “Buy-high, Sell-low” investment behavior that everybody unwittingly does.

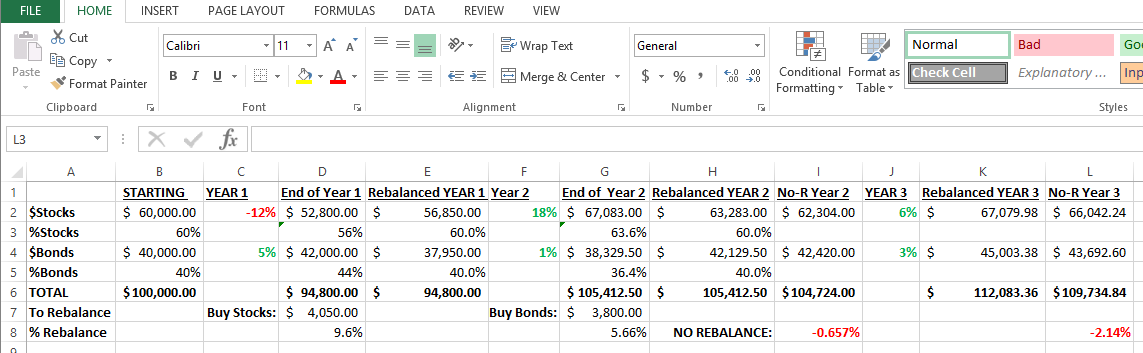

I’ll illustrate the simplest form of rebalancing with an example, assuming you have just two types of investments in your portfolio: a stock mutual fund and a bond mutual fund.

Let’s say you and your investment advisor agreed that you needed the 60/40 allocation to stocks and bonds that 98.75 percent of all investment advisors inevitably urge on their clients.

[Quick aside: I totally disagree with this allocation, and I’m not an investment advisor, so for both reasons please don’t think I’m recommending this for you. In fact I wouldn’t recommend it for the vast majority of people, but that’s a whole other column – or series of columns to come – in the future.]

Ok, back to my example, which will happen to match up – by pure coincidence! – with how 98.75 percent of your investment advisors have set up your portfolio.]

After one bad year in the stock market in our example here, let’s say stocks have dropped by 12 percent and bonds have returned a positive 5 percent, and now your portfolio allocation has shifted due to the market.

The new portfolio at the end of Year 1 now has a 56 percent stocks to 44 percent bonds allocation.

Here’s where the rebalancing part comes in.

When rebalancing at the end of the year you would sell some of your bonds – in my example 9.6% of your bond allocation so that it only makes up 40 percent of your portfolio again. With the proceeds of the bond sale you would purchase stocks, also returning stocks to just 60 percent of your portfolio. You would now begin Year 2 with your previously agreed-upon 60/40 asset allocation.

Next year, let’s say the stock market rebounds, returning a positive 18 percent, while bonds return just 1 percent overall.

Using numbers from my example, you end up with a 0.66% larger portfolio at the end of Year 2 through rebalancing. That may not seem like much, but those little amounts add up over time. If you have a $100,000 portfolio you would be $660 richer after just one rebalancing.

Let’s extend the example one more year. At the end of Year 2, before rebalancing, you have a 63.6% stocks and 36.4% bond mix. We’ll have to sell about 5.6 percent of our stocks to return to our preferred 60/40 mix.

In Year 3, let’s say stocks return a positive 8 percent and bonds return positive 3 percent. You will now have a portfolio 2.1% higher than if you had never rebalanced, or $2,100 on your original $100,000 portfolio. The math works in your favor this way with any asset allocation in which assets have different returns in different years. It also works just as well with more than two types of assets.

A screenshot of the spreadsheet I used for calculations

I’d like to list a few more important points about rebalancing, why it works, and also some caveats.

First, the act of regular rebalancing forces you to “Buy-low, Sell-high,” at least on a relative basis. Whichever asset class has outperformed the others will be the one you sell (high) and whichever asset class has underperformed will be the one you buy (low).

Second, while regular rebalancing makes sense, I doubt it makes sense to do this more than once a year. If you have a taxable account (a non-retirement account) then the tax costs of selling winners may outweigh the benefits. Also, frequent trading is always a mistake, so rebalance with moderation.

Third, because of point number two, if it’s possible for you, the best way to rebalance is not through selling existing investments, but rather through new investments. If you regularly contribute to an investment account, you can ‘rebalance’ your portfolio without tax consequences by simply purchasing more of whatever has become underweighted in your portfolio. This has the happy effect of allowing you to buy (relatively) low with your new investments, rather than to do what everybody else does, which is chase whatever hot sector has recently outperformed.

This may seem super-duper obvious and it is indeed super-duper easy to do.

But!

Most people don’t do it. After Year 1 of losing 12 percent in the stock market, for example, few people have the guts, rebalancing discipline, or a nudgy-enough financial advisor to remind them that their allocation is out of whack. Simple rebalancing will help correct that whack.

We get scared to buy something down 12 percent. After Year 2, we also have a hard time selling something that just soared 18 percent in a year. “Ride that winner!” we tell ourselves, to our later regret.

The U.S. stock market got quite volatile last week, and I couldn’t be happier.

Let me explain why, by way of the analogy of the 2011 fire at Lost Pines State Park.

Scorched earth and equity markets

Two weeks ago, I drove with my family near Lost Pines Forest, the ground zero of a devastating forest fire in 2011 that Wikipedia tells me was the most destructive wildfire in Texas history.

I had passed through Bastrop just weeks after that fire on our way to College Station, and I remember how utterly desolate the roadside forest appeared. Just a terrible vista of charred chimneys, missing their houses. Blackened trunks perched on scarred ground.

Now, however, the ecosystem is roaring back.

Fire leads to new growth

A friend of mine who teaches biology at Trinity University in San Antonio — she studies grassland ecosystems in particular — confirms what you can observe now at Lost Pines. The incredible rate of regrowth of the Lost Pines Forest happens because of the devastating fire.

In many areas, grass and forest ecosystems depend on periodic fires to remain healthy. The fire spurs growth. No fire in the past leads to less healthy growth in the future.

Regrowth of scorched earch

The forest fire stock market analogy

Just like periodic forest fires keep ecosystems healthy for grasses, plants and trees, periodic market crashes keep stock markets healthy for you and me, as long-term investors.

I credit Morgan Housel at the finance website Motley Fool for introducing me to this idea first — that stock markets must crash periodically in order to provide a decent return for the rest of us.

We typically complain, or fret, about stock market volatility. But you know what? That’s the wrong approach. The crashes help repel other people’s money from the market, which allows us long-term investors to earn a positive return.

To be perfectly clear about what I mean with my analogy: We need markets to crash periodically in order for them to “do their job” for us, which is to provide a decent positive return on our long-term surplus capital.

This positive view of market crashes — the financial equivalent of devastating wildfires — is so counterintuitive to our way of thinking and talking about the stock market that it just may alter the way you view the peripatetic ups and downs of equity markets. I hope so. That’s the point of this post.

Now, how exactly does it work that crashes and volatility are the keys to a decent positive long-term return for you, the long-term investor?

Think for a moment what the investment world would be like if stock markets always stayed stable. Zero volatility. Zero crashes. And let’s say in that stable world that stocks initially returned an average of 6 percent per year.

The only rational thing to do, with a market that provided that kind of positive return and perfect stability, would be for everyone to empty their bank accounts and pour money into the stock market. If people felt safe, they would put all their money into the stock market.

That decision by everybody would raise the price of stocks so much that future returns on stocks would decline, to something much less attractive. Given perfect stability, the market would attract as much money as it could take until future returns would approach the returns of other stable, store-of-value vehicles, like bank accounts.

Which is to say, if stocks were completely stable, we would all buy them until they offered a roughly 0 percent future return, just like bank accounts.

But the fact that you can get burned in stocks is exactly why not everybody empties out their banks accounts to bid up the prices of stocks. This relative scarcity of stock market capital leaves space for growth, like a forest that’s been cleared by a fire.

Stocks, thankfully, are not stable. People don’t feel safe. And that’s a good thing.

Do you need your money back before five years? Don’t bother with stocks. You may get burned.

The fact that people who need their money back within five years shouldn’t go anywhere near stocks — due to volatility — is part of the reason why stocks provide longer-term investors with a return above 0 percent.

Without crashes, the stock market would attract too much money. The periodic crash is therefore not a failure of markets or a glitch in the system. On the contrary, the periodic crash — like the forest fire — is a key to the whole system working correctly.

Here’s the topsy-turvy — but nevertheless true — logic of the relationship between volatility and stock market returns: Total stability would lead to “pricing for perfection,” which in turn could be destabilizing when underlying companies and the economy failed to achieve perfection. A volatile market, by contrast, stays just unattractive enough for short-term and speculative investors to allow for predictable, positive, long-term returns for long-term investors.

Long live the forest fire! Long live the volatility!

Teen romance novels for girls are not exactly the bread-and-butter of Bankers Anonymous book reviews, but stick with me for a little while, I’ve got my reasons.

Going Going by San Antonio poet and novelist Naomi Shihab Nye is not your typical teen romance novel, although it does follow the arc of a sixteen year-old downtown girl, Florrie, falling for an uptown boy.

Our heroine Florriedoes not shy away from political stances, nor does the novel Going Going. The political stance dominates the novel more than the romance.

Sixteen year-old Florrie asks us, the reader, one of life’s big questions: “What makes for a good city? Indeed her question is just another way of asking: “What makes for a good life?”

In real life, I live about 6 blocks away from the author of Going Going, so it turns out I know and love many of Florrie’s places too. Her protagonist bikes with arms outstretched down her favorite street, just as I have done, on that same street.

I picked up Nye’s Going Going (at San Antonio’s homegrown The Twig Book Shop) because the City of San Antonio – just like Florrie – is currently in a deep conversation with itself over “What makes for a good city?”

And Florrie has the answer, at least for her: The old mom-and-pop stores, the place-specific homegrown businesses, make for a good city. Chain businesses, by contrast, hurt the city and make life worse.

Florrie pores over old black-and-white postcards, which she collects avidly. She thrills to memories of her Lebanese immigrant grandfather, who founded the family’s Mexican restaurant. In Florrie’s statement of purpose, written for a school project, she writes about herself:

She loved Old Ladies, Elderly Men, Old Houses, Old Spoons, Old Books, Old Bowls, old Maps, Lace Curtains, Antique Bedspreads, Recipes, Remedies, Stories (but not the dumb stories about knights and battles, which did not interest her in the least), Vintage Postcards and Tintype Photographs, Doilies, Velvet Pillows, Black-and-White Movies, Rocking Chairs, and Vintage Toys, and best of all, she loved Old Buildings and Businesses run by Real People. She loved things that were Fading and Disappearing. How could she protect them in the World?

The enemy of all that she loves, Florrie writes, are “Big Business Corporations, Urban Development, and basically People with Too Many Dollar Bills.”

Florrie’s plan, which drives the story, is to organize a teenage, guerrilla-protest movement against chain stores. She enlists her family-and-friends circle in a boycott of the Wal-Marts, the Gaps, the Home Depots of San Antonio – any store not locally-owned. She then hosts a series of rallies against chain-store corporations in the city’s historic Main Plaza, later in front of a Wal-Mart, and finally on the touristic San Antonio River Walk, with mixed success.

In the end, the teenage activist achieves some media notice and notoriety through her protest, but not necessarily lasting change in the city.

Sympathy with Florrie

The author Naomi Nye clearly has tremendous sympathy with Florrie’s aesthetic and moral view of what makes for a good city. So do I.

Florrie is right to decry the homogenization of urban life.

Ever since the 20th Century combination of automobiles and air-conditioning made vast swaths of the American Southwest newly attractive, the cities of Texas, New Mexico, Nevada and Arizona have boomed in population.

Florrie and I don’t want this

What we’ve built – efficiently and affordably – to service these new populations are indistinguishable commercial strips filled with chain stores. Drive down any commercial-zoned highway in these Southwest cities and you’re assaulted with the same exact signage as any other highway – because it’s lined by the same exact chain stores. Their buildings look exactly like buildings in other places, their menu and service offerings fine-tuned to repeat the menu and service offerings of Anywhere, USA.

Where is the sense of place? Where is the sense of a local community?

You need to exit the main highways and turn onto the smaller streets to feel the interesting heterogeneity of locally-owned businesses. From these one-off buildings – with their store owners greeting you from behind the counter – neighborhoods and communities emerge.

San Antonio, TX – Florrie’s city, Nye’s city, my city – exploded upward in population in the past 50 years but imploded in terms of interesting cultural offerings. The blocks around the Alamo, to take the most high-profile and obvious example, are blighted with the same chain-owned Ripley’s fun-house and Rainforest Café offerings you can find in any place in the nation where tourists congregate in bored, hungry numbers.

As I’ve written before, I deeply admire Jane Jacobs’ view of successful cities, which is that a mix of the new and the old – even old shabby outdated buildings – help urban areas remain flexible and innovative.

Change in the last 10 years

Written 10 years ago and published in 2005, the interesting – maybe ironic – thing about reading Going Going in 2014 is that San Antonio has already changed quite a bit since then. The Mission Drive-In, identified in the novel as one of the last operating outdoor theatres, has since been converted to merely a visual – albeit attractive – simulacrum of itself. No more outdoor movies there.

Thousands of housing units have sprouted around Florrie’s neighborhood, utterly altering traffic flow and density in the near-downtown neighborhoods of San Antonio, and this looks to continue apace in the foreseeable future.

Going Going, among other things, is a love poem to San Antonio.[1] I thrilled to recognize many of Nye’s favorite places as my favorite places, from Liberty Bar to El Mirador, from San Fernando Cathedral, to the Rose Window at Mission San Jose.

She profiles real-live personages of Florrie’s neighborhood, like bow-tied Mike Casey on his bike, or movie rental Planet of the Tapes owner Angela pushing her baby, Wiley Francisco, in a stroller.[2]

The dangers of a museum mindset

Although I’m simpatico with Nye’s Florrie, I also found myself arguing quietly against a version of Florrie’s view in real-life San Antonio, which I’ve come to call the ‘museum mindset.’

Nye depicts Florrie as a zealot – albeit a sympathetic, spunky zealot – pushing the limits of the patience of her family and friends in the furtherance of her cause to save old buildings and locally-owned businesses.

Despite the fact that Florrie is only sixteen, she represents a deeply conservative[3] strain of thought.

Because she values old things and old ways and old technologies, her frame of reference naturally resists change. New developments, even beautiful or thoughtful or desperately needed ones, spark in her an instant nostalgia for a soon-to-be lost better age.

This deeply conservative attitude – the museum mindset – surrounds us in San Antonio, and has a big voice in the debate about the future of the city.

For every new development – and there are quite a few going on right now – there is an equal and opposite reaction of “Well there goes the uniqueness of my city,” “gentrification will naturally push out diversity,” “new businesses threaten residential life,” or “here come the Yuppies.”

I’m not in the real estate development business nor do I applaud every new change, but I’ve seen enough opposition-for-opposition’s-sake fights in the name of historic preservation to see the museum mindset as a threat to the city as well.

Preservationists sued, picketed, and went to jail to keep this 1950s-style gem from demolition

Examples of the museum mindset in San Antonio today

Five doors down from where I live, a “house-museum” somehow manages to preserve its 501c3 tax-exempt status, despite the fact that it opens to the public a mere 10 days out of the year. Except for those ten days, the building is totally empty all year, forming a hole in the neighborhood structure. It will not even open this year.[4]

The preservationist group that owns this house has a similar empty-old-house-as-museum project in Hudson Valley, New York. The board of trustees for the preservationist group that ‘runs’ the house-museum – a lawyer for Exxon Corporation and his two sisters – ran afoul of its neighbors in Hudson New York who grew tired of their house-museum charade in the Hudson Valley,[5] but so far my neighborhood in San Antonio allows it to continue.

Hudson Valley “museum house”

The building would make a lovely residential home, but for the past forty years it has been a C-grade museum instead. My best guess is this happens because of the incumbency of the museum mindset.[6]

In downtown San Antonio, this museum mindset favors preserving an old building, however decrepit, unused, or blighted, owned by the local school district, from demolition, removal, or renovation to make way for its current highest and best use. Preservationists have successfully check-mated the neighborhood school – a leading light in a struggling inner-city urban district – into eliminating green space for its kids. In order to preserve this haunted house in the school’s backyard – and ‘haunted house’ is literally how school administrators refer to this building privately – next year the kids will have zero yard space. Will teachers plan on encouraging jumping jacks next to desks in their classroom, or in between the cafeteria tables? I don’t know. I do know that blighted house will keep my kid indoors all next year, while bringing down property values all along its street.

So in my opinion the museum mindset, though helpful in fighting homogenization and strip malls, also hinders progress.

This debate in San Antonio will continue as the city figures out what makes for a good city, and what makes for a good life.

Hey kids! Want a haunted house instead of a playground?

Nye’s spunky character Florrie provides a useful answer as a starting point to the conversation, although Florrie and I would not agree on everything.

Florrie’s romance

To my pleasant surprise, Going Going does not resolve happily. The teenage Florrie does not keep the boy and live a mythical teenage romance. The relationship ends uneasily, with Florrie a little bit hurt, and a little bit wiser for the experience. Kind of like a real teenage romance.

I suppose the romance reflects unease with what Florrie’s boyfriend represents. He comes from the recognizably wealthier, sophisticated, more corporate part of town. Despite the kissing and their bike-riding adventures together, Florrie returns ultimately to the comfort of her parents, her brother, and a humble-but-more-loyal boy from her own neighborhood.

San Antonio’s debate

In growing into its adolescence over the past 50 years[7], San Antonio lost much of its unique character, a process so traumatic to its earlier roots that I don’t blame preservationists for seeking the comfort of the familiar and the loyal.

The older areas of town will struggle with this pull to a wealthier, sophisticated, and possibly more corporate future, and the conversation will not be easy. My guide in these things, Jane Jacobs, would say we need to keep some of the old buildings, but we also need to build some new. The best places, and a good life, consist of preserving a sense of history and place, while not stagnating or fetishizing the old ways. Resisting all change means stagnating and ultimately being left behind, and left out of the transforming process for urban landscapes.

I salute my neighbor Naomi Shihab Nye for adding to this conversation with Going Going.

[4] If you’d ever been inside this house museum you’d know this is no big loss to the public. I’d link to their website to give you a virtual tour, but of course, they don’t have one. That alone tells you what you need to know about their mission to serve the public. But hey! 501c3 status!

[5] From the Wikipedia entry on the Hudson Valley house owned by the same “preservationist” group that owns the house-museum five doors down from me: “Robert Perry, a Texas lawyer and friend of the family, named the trust the Perry-Gething Foundation. Local preservationists have filed complaints against Perry with the state and the Internal Revenue Service, angry that he keeps the house closed most of the year and resides in it himself for several weeks in the spring and fall. Perry responds that when he is present, the house is open by appointment. The tax code, he says, requires only that the foundation maintain the property and says nothing about it making the museum open to the public.”

[6] And possibly, Texans are more polite to their neighbors than New Yorkers.

[7] In this analogy, the creation of Hemisfair Park in 1968 kicked off the city’s adolescence with an horrific bulldozing of an historic neighborhood, to make way for the unapproachable, awkward, sullen park it is today. Here’s hoping the H-Park group will turn this ugly duckling into a swan. The presence of immovable, unused, empty, historic buildings in the park hinders rather than helps this process.

Below is the second in a series of 6 videos introducing the idea of using Excel to track your small business information. This series was created to support the educational mission of Accion Texas, a regional micro lending organization, but I hope it has value to others starting out with their own business who may not have used Excel in the past.