Editor’s note: Paul recently purchased The Financial Rules For New College Graduates, then had some followup questions regarding mutual fund investments. Readers of the book…feel free to pepper me with your followups…

Dear Mike,

I’m on board 1000%1 when it comes to 100% equity mutual funds, the questions in my mind now are: “Which one(s) and how many?”

1) I’m finding many front-end load (5.50%-5.75%) managed funds with anywhere from 0.89% Expense Ratio to 1.40% (with the 1.20% range being the most common). I’m assuming that the lower the expense the better, but am I overstating the importance of this number?

2) Without splitting hairs about what the top 10 holdings are, the turnover within the fund itself, the risk and return vs category, how long the managers have been there and what their philosophy is, what are some of the key things you’d look for before settling on a fund?

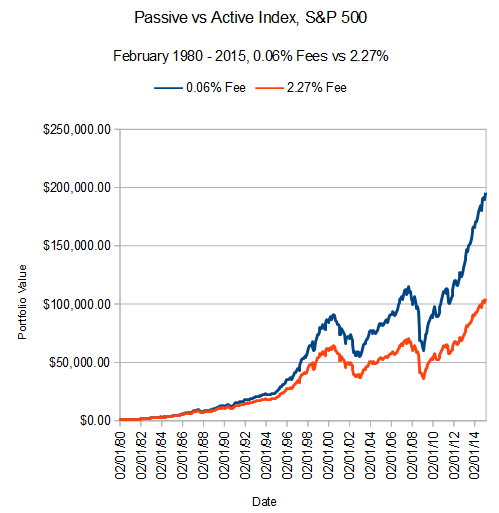

3) I’ve compared the 1 yr, 5 yr, 10 yr and Since inception returns of the funds. Many funds have returned 7-9% while some are well into the 10% and even 11% range. Would you put any stock (no pun intended) in those numbers when comparing and contrasting funds? Are these funds even worth looking into when an Index fund, through Vanguard for example, matches virtually every move the S&P 500 has made, returning the same 10.33% without the commission charge and SIGNIFICANTLY lower expense ratio (0.04%!!!)?

4) And, of course, is 1 fund enough, or would you explore the idea of having several?

Thank you for being willing to even read through this! Hopefully I haven’t strayed TOO far away from the simple approach I’ve attempted to internalize with your teachings.

–Paul F, Boston, MA

Dear Paul,

All great questions, I’ll take them one at a time

1. Front-end Load, Back-end Load – From my (consumer-driven, not industry-driven) perspective, these are all terrible, terrible fees and should be avoided. Never get a fund with them. Basically unconscionable. Can’t justify them at all. Only reason to pay these is if you are totally captive to an employer-sponsored plan and you have no choice of a no-load fund. If you are setting up your own investment plan, just eliminate them entirely.

On the other hand, from an industry (sales-driven) perspective, load funds are great. Makes the salesperson rich at the direct expense of the investor.

About the annual Expense Ratio…at this point 1% is kind of the industry marker. Less than 1% is a reasonable deal for an actively managed fund, over 1% is a little pricey for an actively managed fund. As I say in Ch.14 of my book, I don’t actually think paying for active management makes sense, but if you really want it then 1% is kind of the inflection point between cheap and expensive.

And finally, you are NOT overstating the importance of these numbers. They are – especially in the long run – the absolute key to not turning over between 20% and 50% of your lifetime investment gains to your investment managers. That’s not an exaggeration, its just math you can model out in a spreadsheet.

2. Fund factors to look for – For me (my big bias) the expense ratio is the #1 consideration. After that, of course you want to understand how active versus passive they are (my bias is for passive), how quick turnover is (my bias is for low turnover as it reduces costs and increases tax efficiency), how concentrated they are within the asset class (a case can be made for either diversification or concentration, depending on your overall goals and the rest of your investment plan), where it is in the risk spectrum (for a 20-something person I think you want to maximize risk in all long-term holdings. I still do and I’m in my mid-40s, and I will continue to maximize risk for my whole life, but that’s my bias for all my investments).

3. Time Horizon – For comparing returns, the 10 year and longest time horizons are the only relevant data points. I would ignore 1 to 5 year returns as essentially noise, since the right investment horizon is decades. If the manager is consistent in strategy, the long-term return will be what that particular market sector offers in the long run, which is all I’m looking for in an investment manager.

4. On Number of Funds – I’ll suggest a book for further reading by a guy I like: Lars Kroijer “Investing Demystified.” He doesn’t agree with me on my “risk maximization” point, but he and I agree on the efficient market hypothesis as a good starting point for most people. The reason I bring him up is he makes a case for owning a single “All World Markets” fund, which should be available from major discount brokers. After reading Kroijer you’d have a better sense of how many funds you’ll need. Whether just 1, or more.

As for me, I have just 3 funds in my 401K retirement account. All 3 are 100% equities:

1. US Small Cap,

2. Non-US Developed markets (Europe, Japan, NZ), and

3. an Emerging markets fund

I’m pretty happy with that and will probably never change it. Maybe I’ll re-balance once in a while if one starts to get too big relative to the others. But again, Kroijer’s book will probably explain well why that view makes sense to me.

What’s the best age to start a successful company? What is the average age of the founders of the most successful startup companies?

Most important of all, is it too late for me – at the ripe old age of 46 – to become a billionaire, founding the next SnapChat?

A new research paper co-authored by researchers from MIT, Northwestern University, and the US Census Bureau shows the surprising relationship between business startup success and the age of the founders.

We have an image from popular media that startup success is a young person’s game. Venture capital investors appear to target young founders, seeing in them the greatest chance for originality and high-energy. We celebrate the youth of the founders of Facebook and Google. In an earlier era, the founders of Microsoft and Dell all hit the big time before age 30.

In measuring the average age of successful entrepreneurs, and the average age of the founders of highly successful companies, the researchers used interesting data sets. They accessed and built databases from the Census Bureau showing the growth of all non-farm businesses with at least one employee, blended with IRS data showing the K-1 forms for pass-through businesses like S-corporations, and partnerships.

Unlike other studies which typically pick a group of successful businesses and look for patterns, these researchers studied the entire universe of startups in the United States over time in order to describe the most accurate correlations with success.

Author Ben Jones

It turns out that when you can track all startups in the US over time, surprising patterns around age emerge.

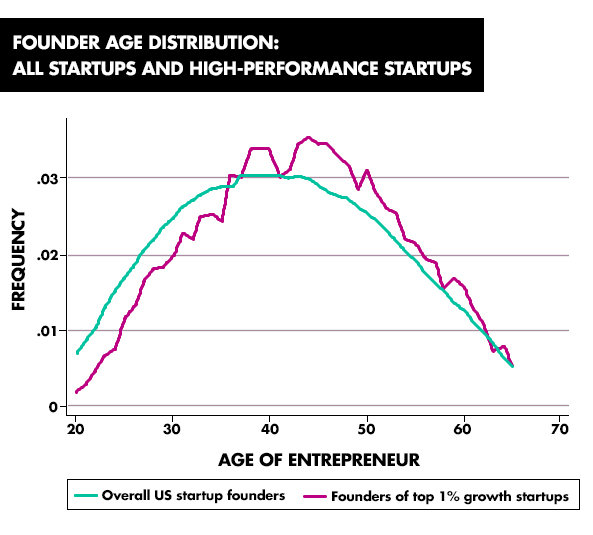

The researchers first discovered the average age of startup founders, which is a surprisingly non-youthful 41.9 years old.

In journalistic presentations of successful entrepreneurs, especially tech entrepreneurs, the authors note a strong impression of youth. Lists of “Top Entrepreneurs” or “Entrepreneurs to Watch” skew toward people in their twenties or early thirties. That just isn’t the reality of who founds companies in this country.

The researchers then calculated the age of extreme success in startups. This is important because while most startups do not lead to extraordinary greatness, a small number of highly successful companies produce outsized results. Maybe runaway success require a youthful disregard for precedent or a willingness to blow up the traditional way of doing things?

To found the disruptive mega-successes like Facebook, Google, Microsoft, and Dell – do you have to be young?

Younger Isn’t Necessarily Better

Their study zeroed-in on unusually “high-growth” companies, the type of company that creates an extraordinarily big economic impact. They calculated the average age of the founder of the top 0.1 percent of startups in terms of employment growth – in other words the best successes compared to 999 of its startup peers. Before I give the answer, want to guess the average age of founder for these companies?

The answer is 45.

In other words, the age of the founders of the very top startups, the one-a-thousand runaway successes, skewed even older and grayer than typical founders.

Beyond that average age for top performers, the researchers found that the probability of entrepreneurial success in general increased steadily with age.

50-something founders were almost twice as likely to succeed at the highest level than 30-something founders. Not only that, but business founders in their 20s were the least likely to succeed. All of this flies in the face of the popular image we get from financial media of Silicon Valley prodigies disrupting everything around them before they’ve been kicked off their parents’ health care plan.

Once we know that decidedly middle-aged founders do better, the logical explanation for this isn’t hard to guess. Youth may boast high energy and a disruptive disregard for the status quo, but age and experience bring even more important advantages to bear. The three most important of these appear to be deep experience in a particular industry, access to financial resources, and harder-to-measure factors like managerial experience and social capital.

If you were an investor looking to back a company in the hopes of outsized success, should you pick youth or age? The data shows you should give your money to the team with the grey hair.

And if you’re an entrepreneur trying to figure out if your best days are behind you, this research suggests the opposite. Your probability of success increases with age.

So, if you’re 45 or older, what are you waiting for?

A logical follow-up thought from this study is whether investors in startups are making an error. Do they back the kids, overlook the olds, and is that losing them money?

One of the authors of the paper, Ben Jones at Northwestern University, described to me two further anecdotal thoughts on that issue, when I talked to him about his paper.

First, young founders often seem to believe that their youth is an advantage, despite the data to the contrary. They self-perceive as “the next Mark Zuckerberg.” For better or worse, they have absorbed the media narrative around young disrupters, especially in technology.

Second, while venture capital investors back firms with founders younger than average, they tend to get thoughtful about their own biases.

Maybe they back younger founders because investors can cut a better deal for themselves? Or maybe investors are swayed by that same media narrative, despite the evidence collected by Jones and his co-authors? There’s potentially a lot of money at stake in the answer to these questions.

It’s January, the month named for Janus the two-faced Roman God who looked both backward to the past and forward to the future.

Looking back over 2016, I realized that I learned about three types of investment accounts, each of which – depending on your phase of life – might make for a nice New Year’s Financial Resolution.

Maybe best of all, all three investment accounts work well even if you start with small dollar amounts. And they each scale up to larger amounts, if you have the means.

Contemplating the start of a new year prompted me to divide these investment account ideas into three categories, past, present, and future. Or you could categorize them as investment accounts for the young, the middle-aged, and the old. I’ll start with the young.

People in your twenties: This one’s for you. The number one key to investment success is starting early in life, yet we often don’t for a variety of perfectly good reasons. The Acorns app addresses many of these barriers, through automatic regular deductions into a super-simple, low-cost, diversified portfolio. The app takes about five minutes and just $5 to get started. It’s mobile-friendly and has an intuitive interface. Acorns gives you a picture of your investment value now, but interestingly also shows you graphs of how your investing activity – when you stick with it month after month and year after year – will grow your account over the coming decades. I’m a big fan of anything that shows the awesome power of compound interest.

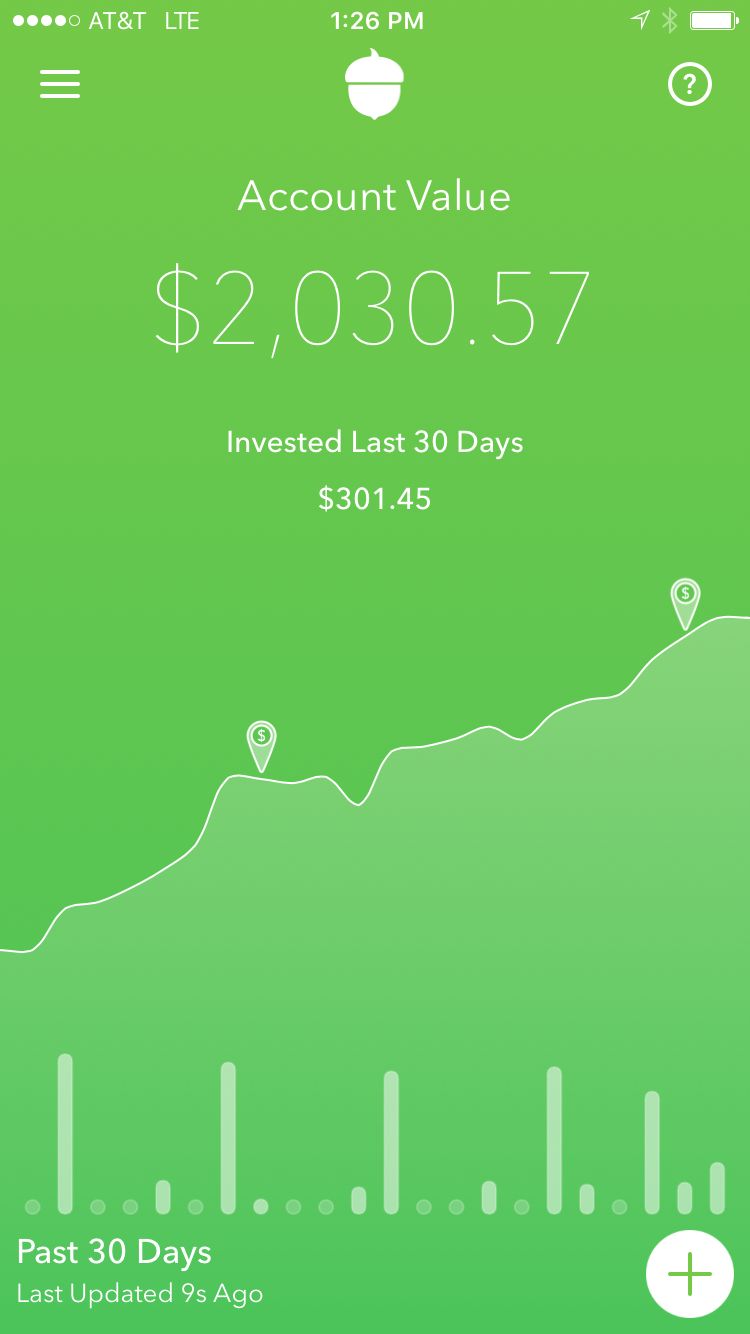

My Jan 1, 2017 balance, after just 7 months

Automatic deductions from your checking account into an investment account is not just A WAY to invest. It’s really THE ONLY WAY to invest for most people of modest means. In my experience, nobody has a surplus at the end of the month unless we’ve devised a trick to whisk our money out of our account before own greedy little hands spend it. The Acorns App is the latest, best, trick to do that automatic whisking. I set up a $50/week automatic program in May 2016, just before I wrote my blog post on it. This week I have more than $2,000 in my account, and I barely noticed how it got there. This is painless investing, made super simple.

If you are 20-something and wondering how to begin investing, here’s the solution to your New Year’s Resolution. If you have a 20-something in your life, send them an Acorns invitation link.[1]

Parents: This resolution is for you if you’re in my demographic. Two kids. Big college bills ahead (should they choose that path.) The more I’ve learned about 529 college savings accounts, the more I’d always recommend parents avoid them and build up tax-advantaged retirement accounts instead of 529s.

And yet, Sir Mix-A-Lot, let me add to that statement a big BUT:

529 accounts make a lot of sense for grandparents who have a surplus. Grandparents who have solved their retirement needs already can use 529s to help the younger generation. Grandparent 529s do not count against financial aid calculations. Also, unlike IRAs and 401(k)s, there’s no age or income limit on making contributions. Finally, 529s are even helpful for estate planning purposes. All of these factors make 529s a better deal for grandparents than parents.

So here’s my New Year’s resolution advice to parents: You might not prioritize 529s yourself (compared to a retirement account) but work to open up an account so that you can invite YOUR parents to contribute toward their grandchild’s college fund. Do it. It’s the right way to approach 529 accounts.

I am not yet part of the older generation – at least in my own mind – but opening a Donor Advised Fund (DAF) in 2017 is actually my own personal New Year’s Resolution.

The idea of a DAF is that you can make a charitable contribution this year – reaping an income tax benefit now – while parceling out charitable gifts over a longer period of time, even decades. Investments in the DAF can grow in a tax-advantaged way, while you take your own sweet time to decide who should receive your philanthropic dollars in the coming years.

If you already have an investment advisor or brokerage firm, you could ask them about the availability and terms for opening up a DAF with them. If they don’t offer DAFs or you don’t like their terms, you should know that a few of the online supermarket brokerages have account minimums as little as $5,000, and charge a reasonable 0.6 percent annual fee. The point is you don’t need $25 million to open up your own private foundation. A DAF makes tax-advantaged philanthropic-giving available to the masses.

But what is the real reason for a DAF, in my mind? And why is this my own New Years’ Resolution, and maybe could be yours too?

Just this: The DAF allows you to appoint trustees, who then share in the decision-making for future charitable gifts. I have in mind appointing my 6 year-old and 11 year-old as fellow trustees of my $5,000 DAF endowment. Could we three generate maybe $250 in investment income every year – a 5 percent annual return – that we then plan together to give away each year? That renewable $250 in annual giving – driven by conversations with my kids – is the real point of the DAF. What I’m really getting for my $5,000 contribution is something of immense value: a conversation-starter.

I know I can’t move the dial of any particular charity with just $250 per year, or even a one-time $5,000, but I can create a vehicle to talk about values with my kids. We can engage in a forward-looking conversation about the uses, and meaning, of wealth.

If you’re in the older generation, with an even bigger surplus, maybe that’s a useful New Years’ resolution for you too.

I wish you peace and prosperity in 2017, and welcome your input into what financial topics you would like to read about in the coming year.

[1] And if you sign up using this particular link (rather than the generic one I inserted above in the main section), I get a $5 referral fee and you get a $5 starter fee, because those Acorns people are clever and give out $5 referrals to both inviter and invitee. But I’m seriously not whoring myself and my blog for the $5. This app is good.

I downloaded a fin-tech app called Acorns a few weeks ago. I recommend you drop this blog post now, text your favorite twenty-something, and make sure they’ve downloaded this thing already. I am now an evangelizing convert.

Here’s a short list of problems many people have in getting started investing and building wealth.

No money (duh, obviously)

No time to figure out investing

No interest in following stock and bond markets

No confidence navigating investment choices

No plan for ongoing automation of investments

No experience avoiding high-cost service providers

Each of these problems afflicts twenty-somethings even more than the rest of us.

And yet, as any fifty year-old who wakes up from a few decades working and paying down debts learns (when they finally make that appointment with an investment advisor) even small amounts of money socked away decades ago would have made the problem of retirement and wealth-building so much easier.

Now, I really hate to endorse a specific product or company when I write about finance topics, because part of my whole “ex-banker in recovery” identity is to form opinions without the reality – or even appearance of – “selling a product.”

Having said that, I’m almost annoyed with myself to say: this is an awesome product and every investment beginner should be using it. The crazy thing about Acorns is that they’ve addressed all six of the problems I listed above.

No money?

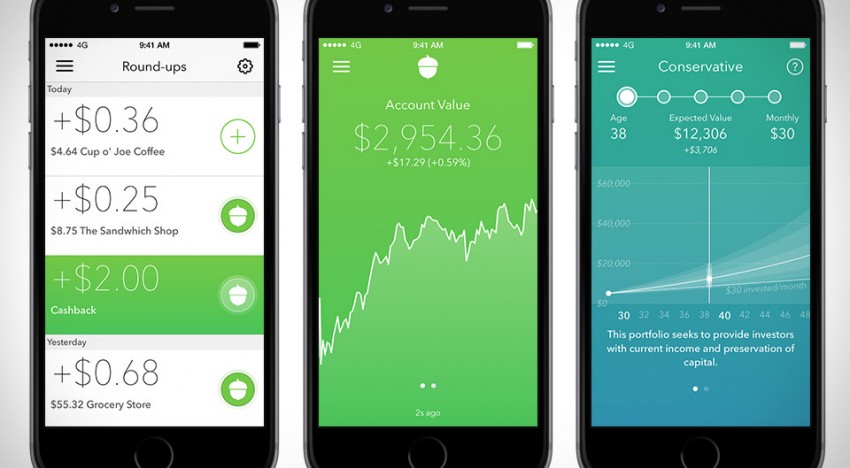

The app invites you to begin with an initial $5 bank transfer. The app’s opening pitch is that it will invest your “spare change.” They use a technique Bank of America pioneered about 10 years ago, which was to “round up” little transactional odd-lots – the equivalent of pocket change you’d throw into a coin jar at the end of the day – and invest it for you. Acorns tracks these spare change amounts from all accounts you choose to link – such as a debt, credit, or checking account – and automatically transfers it into an investment account. Pretty clever.

No time?

The app took about 5mins to get started, and another 3 minutes that first day entering a bit of personal data and linking bank accounts. I never spoke to a live human, which is great. I never set aside time to do it. I set it up on my phone, in between my kids talking to me about their day. “No, sweety, I didn’t really listen to your story about the turtle. Can’t you see Daddy’s moving money around with his phone? This is 2 minutes of sacred Daddy-time.” (I’m a really good parent.)

No interest?

After about 2 minutes of entering personal information, the app suggests one of five portfolios on a risk spectrum from “Conservative” to “Aggressive.” Each of these is built from a blend of Exchange Traded Funds (ETFs) to get you exposed to bonds and stocks, but without having to know anything about these things. While I personally find markets fascinating, I think the ultra-simplification makes sense for everyone who finds stock and bond markets utterly dull.

No confidence?

With no investment choice to make beyond one of five portfolios on a risk spectrum, app users don’t get stuck by the deadly indecision-problem – what behavioral economists call “the paradox of choice” – in which we avoid something entirely because we can’t face the problem of choosing between too many options.

Based on my age, income and wealth, the app suggested the merely “Moderately Aggressive” portfolio for me.

Bitching Black Camaro because YOLO

“Are you calling me old?” I hissed angrily into my phone. I chose the “Aggressive” portfolio instead, like the middle-aged man who rents the black Camaro convertible because #YOLO.

No plan for automation?

This, right here, is the most powerful part of the Acorns app, since automation is the key to moderate-income people getting wealthy. The app continuously pestered me to commit to an automatic investing program, either daily, weekly, or monthly, and in any amount, from as little as $1 per transfer. It prompted me so many times that I finally agree to do it weekly, in an amount affordable to me.

By the way, nobody’s accumulating much money based on the “spare change” gimmick I described above, but this automated-invested feature is what will make a twenty-something a millionaire in the long run, with hardly any suffering along the way.

Cost avoidance?

Acorns charges $1/month until you get $5,000 with them, after which they charge 0.25 percent per year on your portfolio. This is the kind of rock-bottom robo-advisor fee that has the investment advisory business a little freaked out right now. I like it.

Acorns’ limitations

Can I come up with some criticisms of this thing? Of course I can.

I personally wouldn’t choose a blend that includes even the 10 percent corporate and government bonds I got – despite the fact that I chose “Aggressive” as my allocation. Fortunately my “Aggressive” Acorns allocation is 90 percent risky, the way I like it.

A person confident and informed about investments could do all of what Acorns does without paying the Acorns fees, obviously. Their fees are low, but yes you could do this yourself, fee-less.

The simplicity of the app does not allow for a complete suite of investment activities. I happen to think simplicity almost always works better than complexity when it comes to our personal investments, but of course the entire money management industry is built on the opposite idea – the conceit that complex tools help us “beat the market.” Not only can you not execute butterfly call spreads or hedge foreign-exchange exposure with Acorns, but you can’t even buy individual stocks. Again, that’s a feature not a bug from my perspective, but shockingly not everyone sees things my way. (Not yet they don’t.)

If you already have some wealth, and your system works for you without too much cost, Acorns seems mostly unnecessary. It’s definitely geared toward the “just getting started” crowd.

On the other hand, I’m not even the right demographic for Acorns, and I’m a total convert.

I spent the morning of New Years Day with two artists talking about money. They asked questions about the meaning of money, and I tried to supply the answers as best I could.[1]

I waxed poetic about the importance of accumulating a small surplus every month, however tiny, which could add up, over time, to something significant.

They declared themselves indifferent to money, and I believe them.

One of their questions stunned me:

“What’s the point of even trying to save small amounts of money monthly if you don’t have something big, like a million dollars, to invest?” they asked. “Isn’t it just a waste of effort?”

Since they’d never had extra money – and they felt that if they tried to save now it wouldn’t add up to much at all – they figured it wasn’t worth even trying to generate a surplus on a monthly basis.

After I lifted my jaw off the floor I tried to persuade them that small sums today add up to big sums in the future through the magic of compound interest. I spluttered something inarticulate about “money generates money,” and probably failed to make any headway at all in trying to make them see my point.

In my own way in the last year I’ve been making the same mistake they make, I just didn’t realize it.

Lamott’s advice to prospective writers is to focus, every single day, on producing some kind of written work.

Many days, perhaps most days she argues, every writer (even the greats!) feel inadequate to the task of producing anything remotely worth reading. Writers as a rule are distracted people, full of self-loathing, or conversely, wracked by narcissism, all of which gets in the way of producing decent written material.

Lamott’s refrain is to force yourself, through habit, to produce something every day, however paltry it seems. “Just 300 words a day,” she urges, if that’s all you can manage. “Write a shitty first draft,” she pushes, it hardly matters what it’s about. Just start. And then keep going.

Lamott tells the story of her 10 year-old brother who procrastinated for three months on a major grade-school ornithology project. Dejected and daunted by the looming deadline, he froze in panic the night before it was due. Lamott describes how her father put his arm around his brother and gave him the key piece of advice on writing, and life -“Bird by bird, buddy. Just take it bird by bird.”

What does this have to do with my conversation with the artists?

Lamott says writers have to produce a written surplus, however tiny, every day. But I’ve been frozen by the enormity of my project.

The money guy’s perspective on art

My New Years Resolution is to finally write the book(s) that has been dancing around in my head for the past few years.

I realize that the problem with writing my book, however, is the same one my artist friends have. If I can’t be sure the whole finished product will be awesome and successful and read by tons of people – the literary-publishing equivalent of a million dollars invested – then what’s the point of even trying to write it?

I mean, why even start?

So, uh, naturally, I didn’t write it in 2013.

I’m a finance guy, so I guess I needed to see the absurdity of my non-starter attitude put into money terms by these artists.

Maybe Anne Lamott’s analogy can help you too.

So whether your New Year’s resolution is to save more money, or lose some weight, or build that life-size replica of the Pyramid of Giza you’ve always wanted in your backyard, I invite you to join me.

I’m going to do my best to produce a small surplus on the book every day, and not get daunted by the enormity of the whole task.

“Bird by bird, buddy. Just take it bird by bird.”

[1] They may make a short video of my answers. We shall see.

[2] I haven’t reviewed the book on this site because the topic is – as the title implies – writing, which doesn’t fit my finance theme. But if you want to read about the process of writing – then wow this is a good one.

On the other hand, from an industry (sales-driven) perspective, load funds are great. Makes the salesperson rich at the direct expense of the investor.

On the other hand, from an industry (sales-driven) perspective, load funds are great. Makes the salesperson rich at the direct expense of the investor.